The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Average Cost of Pawnshop Loans: A Good Alternative to Payday Loans and Credit Cards?

Some people who need cash—fast—consider going to a pawnshop. How does a pawnshop work? A pawnshop gives you money for your valuables; then later when you repay your debt on time, gives you your goods back. A pawnshop loan might not be a bad idea, as long as:

- you wouldn't be devastated by losing the item you pawn

- you can pay back your debt within 6 months (typical pawnshop loan length)

- you don't have a cheaper way to borrow money

Pawnshop loans are relatively expensive, but they are usually a cheaper way to get funds than using a payday lender; and a credit card may not be the best option, especially if you have poor credit. Pawnshops are more common in the UK than you might realize. There are more than 1,200 pawnshop outlets as members of the National Pawnshop Association (NPA), scattered around the country in both big cities and small towns.

How a Payday Loan Works

Dealing with a pawnbroker is usually quite straightforward. Bring your valuable(s) to a pawnshop where a broker will value your product and give you a loan. Typically, a pawnbroker will offer a loan up to 60% of the second-hand value of your item(s). Besides bringing your valuables to the pawn shop, you'll also need a form of ID and proof of address, for instance:

- Passport

- National ID card

- Driving licence

- Utility bill

- Bank statement

You'll need to complete a loan application and receive Pre Contract Information (SECCI) that highlights the terms of the agreement (including a 14-day cooling off period). Remember, this is a loan—you are not selling your valuables to the shop. Instead, they hold the valuables as collateral for the loan, in case you don't pay it back. Typically, you have 6 to 7 months to pay the loan back, although you can pay it back even sooner if you have the money to do so, which will save you interest payments.

Average Cost of Pawnshops in the UK

Exchanging valuables for a pawnshop loan will typically cost between 5% and 10% per month, which is the equivalent of 80% to 200% APR, or more. This makes pawnshop loans very expensive compared to the credit cards, but cheaper than payday loans.

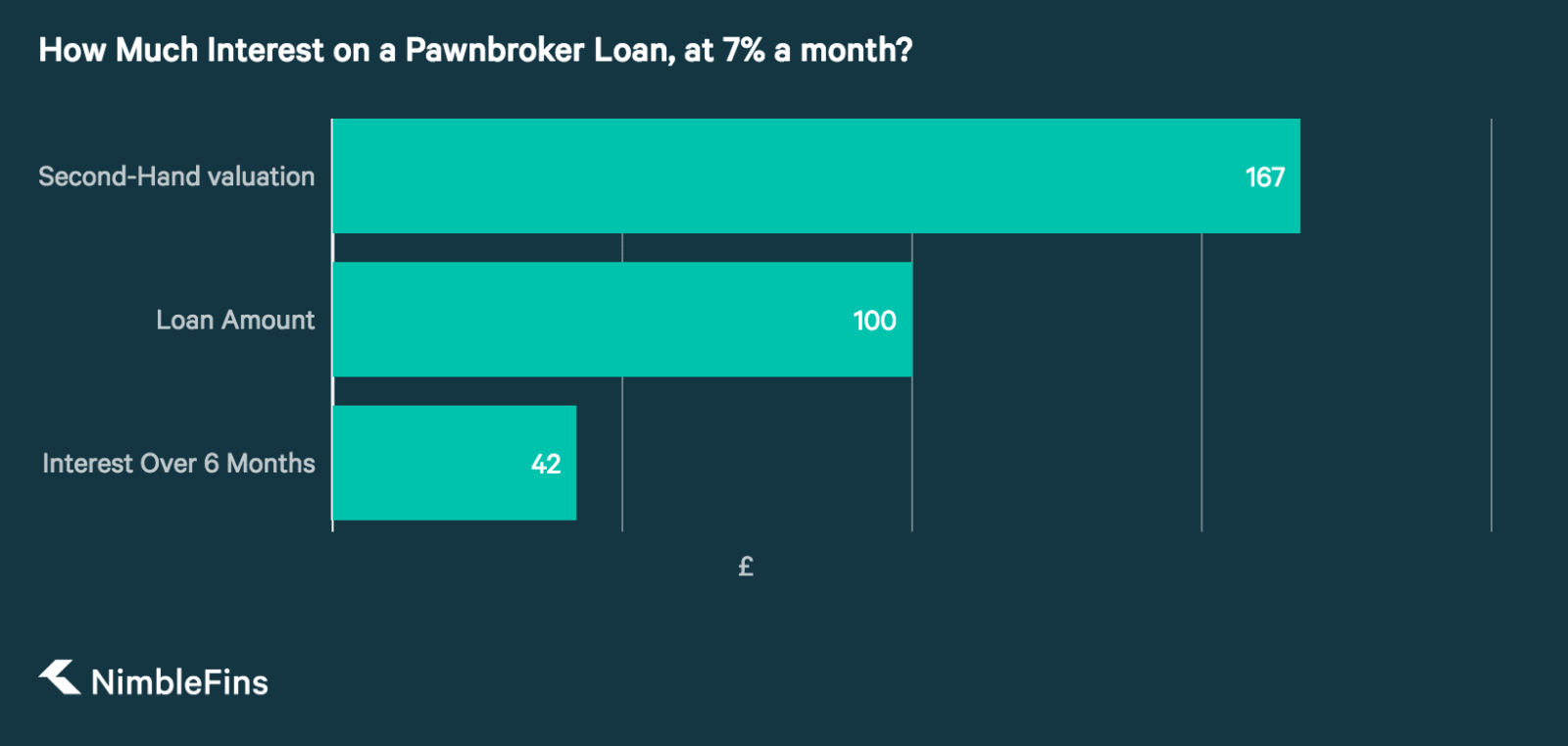

Pawnshop Loan Example

For example, a customer who needs money pawns their gold ring (the most commonly pawned item) at a local shop. The pawnshop gives the ring a second-hand value of £167, offering a six-month loan of 60% of the value or £100 with an interest rate of 7% per month.

At the end of six months, the customer returns to pay back the loan (plus interest) and retrieve their gold ring. The amount owed would be the original £100 loan plus interest of £42 (we calculate the total interest due as 6 months times the monthly interest charge of £7 per month).

| Interest on a 6-Month, £100 payday loan at 7% | ||

|---|---|---|

| Monthly Interest | £100 times 7% | £7 |

| Total Interest | £7 times 6 months | £42 |

What Happens if You Can't Pay Back the Loan in Six Months?

If you don't have money to pay your debt at the end of the pawn shop agreement (usually 6 - 7 months), then you don't get your valuables back.

If you borrowed less than £75 then the pawnbroker takes ownership, and will keep all proceeds when your item is sold. If you borrowed more than £75, then the pawnshop can sell your goods—in this case, if the sales price is more than the amount you owe them (including interest and any other costs, such as auction costs) then you get the difference. If the original loan was for more than £100, then the pawnbroker must notify you in advance before they sell it. In close to 90% of pawnshop loans, the customer pays back the money owed and takes back possession of their valuables.

Pawnshop vs Credit Card

Credit cards are usually a cheaper way to borrow money than a pawnshop loan. The average credit card APR is 20.7%, although there are 0% APR cards in the UK market in the form of 0% balance transfer and 0% purchase cards. However, there are other factors to consider.

If time is of the essence, a pawnshop loan provides funds faster than taking out a new credit card. You can offer your valuables and have cash in your hand within hours. Also, those with poor credit may prefer a pawnshop loan to avoid further credit checks that accompany a credit card application, especially if they already have household debt. For reference, those who would only qualify for a credit-building card would likely pay at least 34.9% APR on a credit card balance; cash rates are even higher. In most cases, there is no compound interest on a pawnshop loan and all amounts are due in a single payment at the end, so there's no need to worry about making monthly payments like on a credit card.

Pawnshop vs Payday Loan

Generally speaking, a pawnshop loan is cheaper than a payday loan. The average payday loan APR is 1,250%, although rates can be as high as 1,500% (0.8% a day) on a payday loan. While the FCA has limited the amount of interest and default fees on a payday loan, they are still a very expensive way to borrow. In fact, the average person pays back £165 for each £100 borrowed on a payday loan. Plus, missing a payment can mean an additional £15 default fee.

How to Find a Pawnbroker?

Both large chains and independent pawnbrokers operate throughout the UK. Some of the larger chains are H&T (over 180 stores), Cash Converters (over 200 stores), Albemarle & Bond (over 100 stores) and the Money Shop (hundreds of stores).

Be picky about choosing a pawnbroker—find one that is local to you and a member of the National Pawnbrokers' Association (NPA). NPA members follow a code of conduct, providing an additional level of comfort and protection.