Endsleigh Landlord Insurance Review: What You Need To Know

Endsleigh Landlord Insurance Review: What You Need To Know

Good for

- Non-standard property cover

- Tailor your policy to suit you

- Knowledgable and understanding customer advisors

- Very competitive prices

- Excellent standard cover

Bad for

- Cancellation fees

- Rent guarantee not offered

- Underwritten by many providers so difficult to deal directly with insurer

As seen on

When you hear the name Endsleigh the first thought that may come to mind is student insurance. However, since their partnership with the National Union of Students (NUS) in 1965 they have expanded their insurance offer, offering a variety of policies including landlord insurance. But how good is their landlord insurance compared to other big-name providers on the market?

Well, upon first impression it appears that Endsleigh provides a solid landlord insurance offer.

The company overall has earned itself a 3.6 star rating from Trustpilot across over 3,400 reviews+, indicating an ‘average’ customer experience. When looking at landlord insurance specifically, we think Endsleigh’s landlord insurance offer is a good quality product on the market in terms of features.

However, during our deep dive into Endsleigh’s insurance offer we found that not all reviews and ratings were quite as glowing as those we’ve just mentioned. Only 45% of Endsleigh customers would recommend their insurance offer to a friend, although it’s important to note that this covers the whole of Endsleigh and not just their landlord insurance offer.

In this review we will cover everything you need to know about Endsleigh’s landlord insurance offer, providing you with an unbiased review of its features, customer ratings and feedback as well as its price compared to its competitors.

In This Review

- Endsleigh Landlord Insurance: Overall Review

- How to Claim

- Endsleigh Landlord insurance: discounts and savings

- FAQ’s

Compare Landlord Insurance

Get started with only one form to fill out. Find the insurance you need today.

Endsleigh Landlord Insurance Overall Review

With over 25 years in the landlord insurance market, Endsleigh works with a panel of leading insurers to help find the right policy for you that accommodates your needs. Because of this, Endsleigh pride themselves in providing a variety of different options for cover. These range from commercial properties to blocks of flats, charity insurance and even for residential properties with non-standard construction, something that many competitors do not cover.

It is perhaps no surprise then that Endsleigh has earned praise from its customers and experts alike. Indeed, Endsleigh were a finalist at the 2019 Insurance Choice Awards for the ‘Best Landlord Insurance Provider’ category, and Endsleigh was a finalist at the UK Broker Awards in 2023.

Taking a look at their customer feedback, Endsleigh appears to have earned a reputation of being a solidly decent landlord insurance provider. With a 4.8 star rating from Smart Money People and an ‘average’ rating from Trustpilot of 3.6 out of 5, it certainly seems that Endsleigh is worthy of consideration.

Nevertheless, whilst customer feedback for their Landlord insurance specifically is overwhelmingly positive there are still some customers who have been left disappointed.

One reviewer, for example, was particularly frustrated, saying “Endsleigh are trying to charge me £110 cancellation fee on a policy worth £277” whilst another was unhappy with the support they received from their tradespersons, “If you are a landlord, avoid this company like the plague. They are cheap and support very bad engineers”.

Of course, context is important here and the positive reviews overwhelmingly outweigh the negative. Taking this into consideration, the question remains: what is the truth behind Endsleigh’s landlord insurance offer?

First, let’s take a look at the benefits of choosing Endsleigh over other insurance providers.

Why choose Endsleigh Landlord insurance?

Endsleigh’s standard landlord insurance offer is certainly impressive, and there are some unique features that set them apart from their competitors.

- Experienced provider: with over 25 years' experience in the landlord market, Endsleigh come equipped with the knowledge you need in case things go wrong

- Covers a variety of property types: these include student lets, commercial property, portfolios and even non-standard rental properties

- 24 hour claims line: meaning you can always contact Endsleigh if you have a query, concern or need to make an urgent claim in the case of an emergency

- Tailor your policy to suit your needs: as Endsleigh work with a panel of insurance providers, this means they will provide you with a variety of options to suit your needs, all of which can be tailored to suit you

- Multiple property cover: you can cover up to 4 properties in one policy—and a multi-property policy could get you a cheaper deal, too!

Endsleigh Landlord insurance reviews and ratings

|

Endsleigh Customer Ratings | |

|---|---|

|

Smart Money People Rating^ | 4.8 out of 5 (landlord insurance specific) |

|

Trustpilot Rating | 3.6 out of 5 |

|

Reviews.io Rating | 2.9 out of 5 |

Endsleigh as a whole (I.e., not landlord insurance specifically) has earned mixed reviews, scoring an ‘average’ 3.6 out of 5 on Trustpilot but a disappointing 2.9 out of 5 on Reviews.io. For their overall home insurance offer consisting of buildings and contents insurance they have been rated only 2 stars out of 5 by Fairerfinance’s experts. Again, it’s important to note this score does not reflect their landlord insurance offer specifically.

When we do look at landlord insurance specific reviews however, Endsleigh appears to perform more strongly. For example, Endsleigh score a whopping 4.8 out of 5 on Smart Money People, based on 600+ reviews.

Let’s take a look at what Endsleigh’s customers themselves have to say.. .

What does Endsleigh Landlord insurance do well?

We reviewed feedback left by hundreds of customers and noticed many commented on their competitive prices and helpful staff, particularly that they felt their needs were listened to. Others also call out the fact that the process of taking out landlord insurance as well as amending their policies is hassle-free.

“I used Endsleigh for landlord insurance for a year. I found the staff helpful and the process of application was easy. Endsleigh also specialise in more unusual insurance so of you struggle to get insured elsewhere”

“As I will no longer be a landlord soon, and therefore not require a renewal on my policy I called to ask if I need to cancel, or simply not just renew. The customer service girl was extremely polite and helpful”

“I was stressed because I'd gone on line and found my Landlord Insurance hadn't renewed, yet I'd given my credit card details to renew over the phone. All was well, which she smoothly and efficiently handled and confirmed, clear explanation re timing, changes being made to online information etc"

“Have been with Endsleigh for over 20 years as a private landlord with several properties. Endsleigh give me insurance at a competitive price. Great cover and personal service”

“Prepared to listen to customer needs. Explains policy and payment details clearly. Friendly and professional”

What could Endsleigh Landlord insurance improve on?

Whilst the majority of reviews are positive, there are some negative customer experiences that are important to take into consideration. During our research we found the most common complaints were focused on difficult customer service, delays in paying out when a claim has been made and also being unable to make the claim itself.

"I opted for auto renewal but was still bombarded with emails, then after the money had been taken from my bank account to have to send a load of paperwork to your office with information that you have had for the last 3 year, won't be doing automatic renewal again I think it is just as easy to shop around."

“When making a reasonable claim Endsleigh were guilty of denying previous conversations, failing to contact when promised, phone conversations cutting off with unusual regularity, new evidence required with follow up calls, failure to respond to emails. I would strongly advise against considering taking out landlord insurance with this firm”

“Terrible insurer. Never do landlord insurance with these guys. They don't pay out for emergency cover and charge you a premium for their services. On their policy it clearly states, they will pay out if the general functioning of the house is compromised. However when 2 out of my 4 tenants texted saying the sink and bath were blocked (draining very slowly) I was told that, they don't cover this”

“I took out a Landlord insurance after seeing a promotion from one of their 'appointed agents' offering a high cashback rate...total garbage and mis-leading! I haven't been paid my cashback and my insurance hasn't even been confirmed as yet!”

“Have used them for landlord insurance when my boiler broke down. They sent a joker of an engineer who scheduled to arrive at 1-2 but arrived at 8pm...he literally peeked at the boiler...and claimed it was a maintenance issue and was not covered which is not possible as it was serviced a less then 6 months ago”

As with any product review context is important. Sometimes frustration and complaints are a result of customers simply not knowing or understanding what is covered under their policy. The documentation given to you when you agree to take out landlord insurance is often full of jargon and can be a lot of information to digest, so of course details can be overlooked.

Take this scenario, for example. If you find that there is a leak in one of your rented properties and you wish to make a claim, you may find that your policy will cover the costs of fixing the damage caused by the leak, rather than the leak itself. It sounds almost counter-intuitive and may lead to you to becoming quite annoyed with your insurance provider when they tell you this is outlined in your policy documentation.

It is for these reasons that we always recommend reading your policy wording carefully so you know your rights and don’t get caught out.

How much is Endsleigh Landlord insurance?

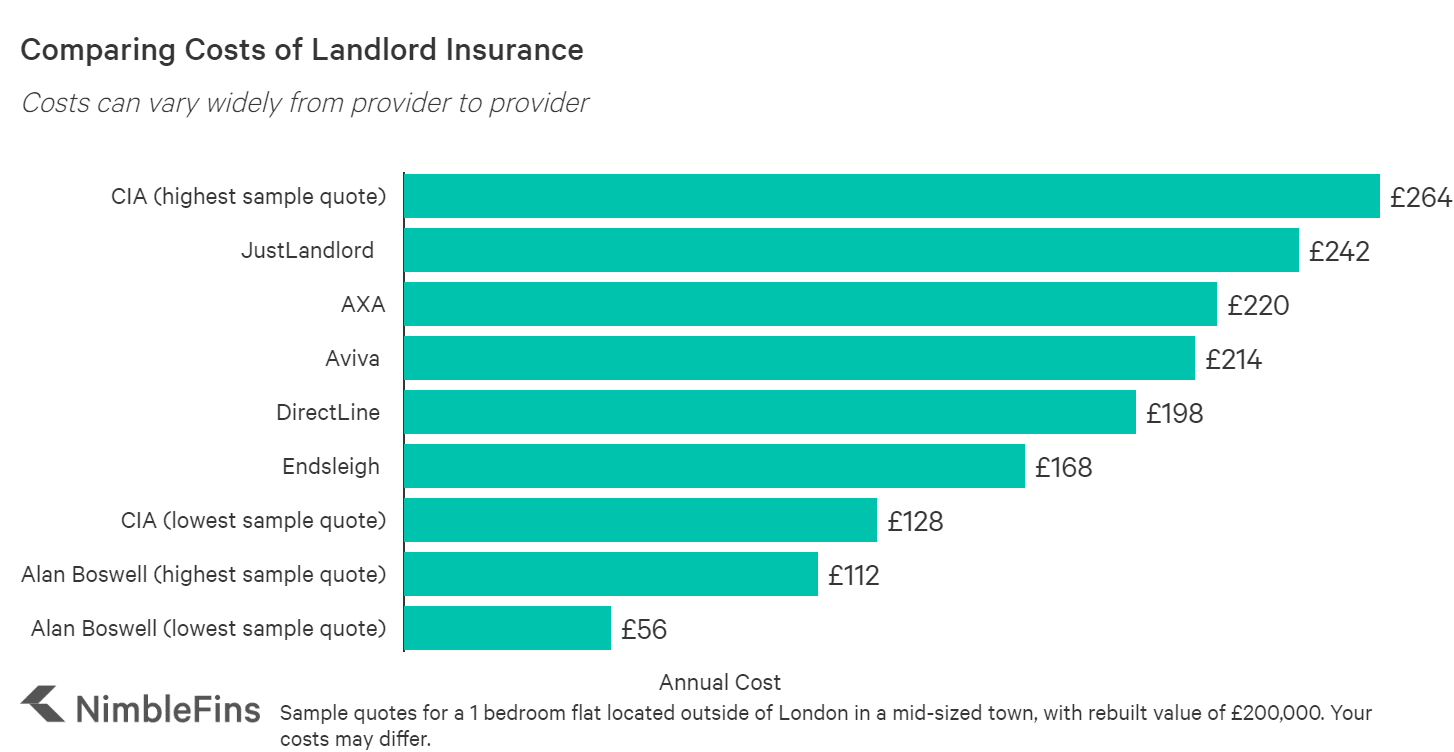

We have compiled quotes for a 1 bedroom flat located outside of London in a mid-sized town, with a rebuild value of £200,000. We found that for a no-frills policy with buildings insurance and property owners liability of £5million as standard, Endsleigh’s landlord insurance was the second cheapest provider compared to five of its leading competitors. In fact, we’ve calculated the sample quote is 16% lower than the average price of the like-for-like quotes shown below.

|

Landlord insurance quote comparison for a 1 bedroom flat (£annual) | |

|---|---|

|

CIA | £264 (highest sample quote) |

|

JustLandlord | £242 |

|

AXA | £220 |

|

Aviva | £214 |

|

DirectLine | £198 |

|

Endsleigh | £168 |

|

CIA | £128 (lowest sample quote) |

|

Alan Boswell | £112 (highest sample quote) |

|

Alan Boswell | £56 (lowest sample quote) |

Of course, these quotes are intended to be used as a guideline as they're sample quotes only, and your quotes may be higher or lower depending on your own individual circumstances.

Nevertheless, considering it is less pricy that many of its competitors, such as DirectLine and Aviva, you may be wondering if Endsleigh’s standard landlord insurance cover offers you less protection. Let’s take a look at what is and isn’t included to see if the low price is worth it.

What is/isn’t covered by Endsleigh’s Landlord insurance?

As part of their standard landlord insurance cover, Endsleigh offers a nice selection of benefits that are in line with what you would expect. Their residential landlord insurance can include cover for the following:

- The cost for repairing or rebuilding your property, including garages, outbuildings, walls, gates, fences and patios, up to £1,000,000

- Landlord contents cover from £5,000 up to £60,000 for items such as white goods and furniture

- Property owners’ liability up to £5,000,000 for bodily injury to any person by accident

- Accidental damage to property

- Employer’s liability up to £5,000,000

- Malicious damage by the tenant or their guests up to £25,000

- Loss of rent

- Up to £3,000 for alternative accommodation

- Trace and access cover

- Extended unoccupancy period, up to 120 days for student properties

- You can also choose to add useful covers to your policy, such as home emergency or landlord legal cover

Here is some more information on the different types of landlord features you might be able to arrange, in many cases as an optional add-on for an additional premium:

- Landlord liability (£5m): if you own the property outright, Aviva’s landlord insurance will cover the costs if a third party makes a claim against you for suffering sickness, injury or if their property is damaged as a result of your actions or your property

- Buildings insurance: cover will protect you against damage or loss caused by a variety of events such as fire, flood, storm, water escaping from or freezing within in-home appliances, theft, subsidence and landslides.

- Landlords contents: if any contents, such as furniture or removable appliances you provide for your tenants are damaged or lost as a result of, say, any of the above events, Endsleigh will cover the cost of repairing or replacing these. This also covers theft of gardening contents (£500 limit) and any gardening equipment stored in outbuildings (£3,000 limit).

- Loss of rental income: if your property becomes uninhabitable due to a covered event, Endsleigh will pay up to 30% of the buildings sum insured for loss of rent

- Cost of alternative tenant accommodation (£3,000 limit per claim): again, if your property becomes uninhabitable due to any of the reasons stated above Endsleigh will cover the cost of comparable alternative accommodation during the period necessary to reinstate your property to a habitable condition

- Accidental damage to glass and sanitary ware: this includes fixed bathroom fittings as well as fixed glass in windows and doors

- Underground pipes and cables cover: applies to accidental damage to drains, pipes, cables and tanks that provide services to and from your property, and for which you are legally responsible

- Replacement of locks (£1000 limit during insurance period): will cover the costs of replacing locks and keys to external doors within your property, as a result of theft or loss. Note, this cover does not apply in the event that the theft is not reported to the police or if standard/student tenants simply do not return their keys at the end of a tenancy.

- Malicious damage and theft by tenants (£25,000 limit): covers the cost to repair or replace property intentionally damaged or stolen by tenants (e.g. if a tenant purposely breaks a window).

- Landlord employers liability insurance (£5m limit): if you employ someone, by law you must have employers liability insurance (note: there are some exemptions). As owner of your property, Endsleigh's standard landlord insurance will cover compensation payments and legal costs if an employee suffers a work-related illness or accident.

- Extended unoccupancy period: the standard unoccupancy period of 90 days is extended to 120 days for student properties.

- Landlord home emergency cover: in the event of an emergency (e.g. a boiler breakdown), Endsleigh will cover the call-out costs, labour and parts required to resolve the issue. They also provide 24/7 emergency repairs and work is carried out by qualified contractors

- Landlord legal expenses (£50,000 limit): covers the cost of unexpected legal fees associated with contractual or tenant disputes. Endsleigh will provide a legal representative and cover legal costs, and this can apply to the recovery of rent arrears, repossession and costs of damage to your rented property.

- Accidental damage to contents: covers accidental damage to the contents your provide to your tenants except where this is listed as an exclusion (see exclusions section below)

Missing features

There are some features that either aren’t offered in Endsleigh’s standard residential landlord cover or aren’t available to purchase as an add on. These features are worth knowing about as they do provide that added layer of protection if something were to happen and could save you a lot of money, so going without these could be risky.

- Landlord rent guarantee: unlike loss of rental income, landlord rent guarantee insurance will cover you if a tenant is unable to make rental payments regardless of whether your property is habitable or not (e.g. if the tenant has recently lost their job). Endsleigh does not offer rent guarantee in their landlord insurance offer, so ensuring you have a stable source of income from your rental payments is incredibly important, so think carefully about whether you would be comfortable proceeding without this security.

Exclusions: What isn’t included?

As with almost any type of insurance, landlord insurance often contains some exclusions that are good to be aware of so you don’t get caught out. Endsleigh is no different, and we’ve outlined a few key ones we’ve found below. Note, the full list is much longer, so make sure to read up on the exclusions to avoid getting caught out.

- Any damage or events that you were aware of before the policy start date: a common exclusion that is often missed, so make sure you triple check when your cover officially starts!

- War and terrorism: If your property is damaged as a result of events associated with these (e.g. if, rather unfortunately, your property suffers damage from a nuclear attack) you will not be covered

- Any damage resulting from faulty design, materials or poor workmanship

- Any gradually occurring damage i.e. natural wear and tear or damage that would be expected as a result of aging

- Damage caused by frost, damp, dry-rot

- Damage to fences, gates, hedges, terraces, walls and outbuildings unless the main private dwelling of your property is damaged at the same time

Another key point to remember as a landlord of a rented property is that if your property is unoccupied for longer than the period of time outlined in your policy, any damage or losses that occur within this time will often not be covered by your insurer. Endsleigh do offer a standard unoccupancy period of 90 days (longer than many other providers) which is further extended to 120 days for student properties. Nevertheless, always read your policy wording carefully and know your rights!

How does Endsleigh Landlord Insurance Compare to Competitors?

To better understand the value of Endsleigh Landlord insurance you need to look at it in the context of other available options. We compared it to other plans in the market so you can see which may be more suitable for you.

Endsleigh Landlord Insurance vs Direct Line Landlord Insurance

Direct Line is one of the UK’s largest and most reputable insurers, earning top scores for landlord features making them one of the best landlord insurance products on the market. With over 250,000 existing landlord insurance policy holders it is certainly a popular choice and has won multiple awards to boot. Its comprehensive cover includes buildings, contents and landlord liability included as standard.

Like Endsleigh, Direct Line offer a range of optional add-ons such as malicious damage by tenants, loss of rental income and legal expenses meaning you can curate the right policy for your needs. Direct Line also offer some discounts for new and existing landlords, such as a 10% multi-property discount if you’re looking to insure 15+ properties!

Bottom Line: If you’re looking for award-winning coverage from a reputable insurer then Direct Line may be another option to consider — their extensive range of policy add-ons also gives you the freedom to tailor your policy to suit your specific needs.

Endsleigh Landlord Insurance vs Alan Boswell Landlord Insurance

One of the most affordable insurers we sampled from, Alan Boswell certainly doesn’t lack in its cover. As standard, they cover many of the ‘essentials’ including buildings, contents, landlord liability, employer's liability as well as accidental damage and malicious damage by tenants!

That being said, for landlords looking for rent guarantee, legal expenses or landlord home emergency insurance — this will come at an extra cost. However, with excellent expert and customer ratings across the board and a low sample price to boot… it’s certainly worth considering.

Bottom Line: our research found Alan Boswell to offer excellent coverage at a low price, making it one of the best landlord insurance offers we have come across. For landlords looking for a value offer that is trusted by experts and customers alike, Alan Boswell may be the landlord insurance provider for you.

Endsleigh Landlord Insurance vs LV= Landlord Insurance

One of the UK’s leading providers, LV= specializes in many different insurance areas. This multi-award winning provider receives glowing customer feedback so is certainly a firm favourite amongst experts and customers alike.

Though some customers have noted higher renewal fees and lack of rewards for loyal customers, we found LV= to be one of the cheapest providers we sampled from so it might be worth taking a look. Even with its low price LV=’s coverage certainly packs a punch — its extensive cover includes £5m landlord liability, accidental damage, malicious damage by tenants as well as loss of rental income as standard.

Bottom Line: Don’t be fooled by the low premiums, LV= is certainly another great option for price-savvy landlords looking for a value offer without compromising on cover.

How to make a claim on Endsleigh Landlord insurance

Unlike some other landlord insurers, Endsleigh work with a panel of experts which means that any policy you take out may be underwritten by any one of these providers. The process of underwriting is a funny concept, but essentially an underwriter will decides who and what to cover, and at what cost.

For this reason, you will deal directly with the insurer named on the statement of your insurance should you wish to make a claim on Endsleigh’s landlord insurance so make sure you are familiar with who this is.

You can find all the information you need on Endsleigh’s website, but we’ve listed them below as well for your reference.

- Endsleigh’s online claim centre: https://www.endsleigh.co.uk/claim-centre/

Policy numbers starting with LA1:

- Telephone number: 0345 165 0933 (24/7)

Policy numbers starting with LE1:

- Telephone number: 0345 603 8381 (Mon-Fri, 8am-6pm)

- Email: [email protected]

Policy numbers starting with LG6:

- Telephone number: 0370 900 5565 (Mon-Fri, 8am-8pm, Sat 9-5pm)

Policies underwritten by Zurich:

- Telephone number: 0800 923 4042 (Mon-Fri, 8am-8pm, Sat 9-5pm)

Policies underwritten by Aviva:

- Telephone number: 0800 012 345 (24/7)

Policies underwritten by AXA:

- Telephone number: 0330 024 6842 (Mon-Fri, 8am-8pm, Sat 9-5pm)

Before you decide to make a claim, we recommend that you read your policy wording carefully to ensure that you are indeed covered. If you are, you may be asked to provide certain details and documentation such as your policy number, photographic evidence of your loss or damage, receipts and invoices so it’s always a good idea to have these handy, or be prepared to acquire these if necessary to avoid delay.

Endsleigh landlord insurance: Discounts and savings

At the time of writing, we have been unable to locate precise offers which will save you money on Endsleigh's landlord insurance.

However, all is not lost. Typically, insurance providers will offer incentives and discounts to existing customers as well as discounts if you shop online, so be sure to double check these if you're thinking about taking out landlord insurance with Endsleigh!

FAQ’s

Sadly, yes. Regardless of whether you cancel your policy within or after your 14-day cooling off period (i.e. the first 14 days from your policy start date) you will still be charged a fee of £25.

You will also be charged a £25 fee if you wish to change details within your policy during your insurance period (e.g. if you need to change your address).