Capital One Classic Credit Card Review: The Credit-Builder Card for You?

Capital One Classic Credit Card Review: The Credit-Builder Card for You?

Good for

- Checking eligibility before you apply

- Those with past CCJs or defaults

- Receiving free text/email alerts and a mobile app

Bad for

- Those with no UK credit history

- Those looking for a low interest rate

- Carrying a balance from month to month

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

The Classic credit card is Capital One’s most popular UK card and is designed for those trying to improve their credit rating. This credit-builder card is a solid offering from a solid company, but is it right for you? Read this review to learn about pros and cons and alternative cards in the UK market.

Capital One Classic Credit Card Review

The Capital One Classic credit card is a solid, all-around credit-builder card that's even open to those with CCJs or defaults in the past.

The Classic is a basic card, without any rewards or perks, aimed at providing credit to those with marks on their credit history. Once you have the card, paying on time and staying within your credit limit should improve your credit history. It can take months to see an improvement in your credit rating, so a bit of patience is required, too!

The Classic is Capital One's most popular card with over 4 million people accepted.

The mobile app and text/email alerts to help you manage your finances—staying on top of payment due dates and under the credit limit are key factors for someone rebuilding their credit history.

Who is eligible for the Capital One Card?

Will you be accepted for the Capital One Classic card? Applicants can use the QuickCheck tool to perform a soft credit check, which won’t leave a mark on you credit record for other lenders to see and will tell you if you’ll be approved before you apply. Please know that this is not a guarantee that you'll be accepted, just an indication. For example, if identity or fraud checks throw up any red flags, you may be rejected even if QuickCheck indicated you could get a card.

As a credit-builder card, Capital One will consider people with an imperfect credit history. A number of stipulations on their website indicate who is more or less likely to be accepted. Capital One is...

| More likely to accept you if you... | Not likely to accept you if you... |

|---|---|

| Are at least 18 | Haven’t had credit in the UK before |

| Have shown a history of managing credit (even with CCJs or defaults in the past) | Have declared bankruptcy in the past 12 months |

| Are on the electoral roll at your current address |

Bottom Line: The Capital One Classic card is a really good option for those with a spotty credit history who need a credit card. The QuickCheck eligibility checker is a great feature to know if you'll be approved before you apply, plus the mobile app and alerts help you stay on top of your account.

Capital One Classic Benefits & Features

| Capital One Classic Credit Card Features | |

|---|---|

| Credit Limit | £200 to £1,500 |

| Credit Limit Increases | Cardholders may be eligible for up to two credit limit increases a year |

| Free Mobile App | Highly rated in the App Store |

| Text/Email Alerts | To help you stay on top of your account |

| Eligibility Checker | To see your odds of being accepted |

| Non-sterling Transaction Fee | 2.75% |

| Cash Fee | 3.0% (minimum £3) |

| Annual Fee | £0 |

| Late and Failure to Pay Default Sum | £12 |

| APR | 34.9% variable APR on purchases, cash withdrawals, balance transfers and money transfers |

Pre-eligibility check

Checking your odds of acceptance before you submit an application is important because applying and getting denied can be damaging to your credit rating. Technically speaking, other lenders won’t see if you’ve been denied, but they will see the hard credit search. And too many hard credit searches can be a red flag to potential lenders.

Those with poor credit are wise to avoid repeated hard searches resulting from multiple application denials. (It’s fine to have a hard search IF you are accepted and get your credit card.) Capital One stand by their QuickCheck answer, unless certain information pops up in fraud prevention databases or they can’t verify your identity. Being registered on the electoral roll will really help with the id verification process.

Mobile App

Capital One's free mobile app for iPhone or Android can keep you on top of your account. Using a 6-digit passcode to log in, you're able to:

- View your current balance

- Check your credit limit (and how much you have left to spend)

- View latest transactions

- Check payment information (e.g., when and how much to pay next)

- Make a payment to your Capital One card

Text/Email Alerts: Capital One will set you up with free SMS/text or email alerts to let you know when your balance is near your credit limit, you've gone over your credit limit or payment details, such as when your Direct Debit will be taken, when a payment is due or if you've missed a payment.

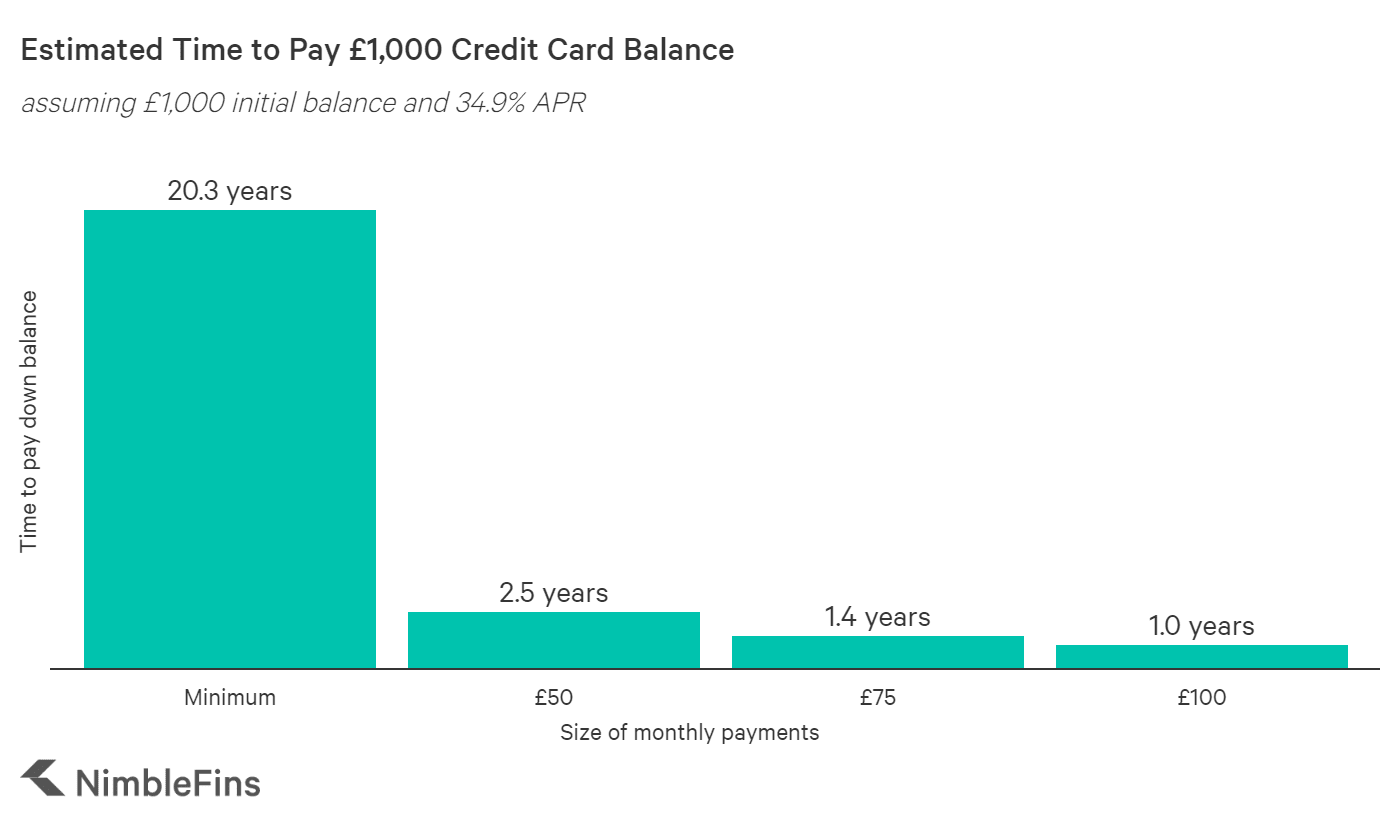

Capital One Classic Credit Card Monthly Payments

Most people know the importance of making an on-time payment each month, in order to maintain or improve their credit rating. There's another very important consideration to keep in mind when it comes to your monthly payments—the size of your payment. Will you pay the minimum amount only, or more?

By paying only the minimum payment, you are extending the time to be debt free and increasing the amount of interest charges you will pay in total over the life of your credit card debt. Instead of paying the minimum amount only, paying a higher amount—really as much as you can afford—will reduce your total interest charges as you pay down the balance.

The following chart illustrates for a £1,000 outstanding credit card balance, charged at 34.9% APR, how total interest charges are reduced with higher and higher monthly payments. Note, we have calculated the minimum payment as 1% of that month's outstanding balance plus any interest charges for the month.

Minimum monthly payments can be very costly in the long run, because the absolute pound value of the payment drops over time (because it is calculated as a percentage), extending the time you pay interest. You can see the repercussions of a falling minimum payment in the following chart. By paying only the minimum each month, cardholders won't pay back the debt for 20 years!

How does the Capital One Classic Card Compare to Other Credit Cards?

To better understand the value of the Capital One Classic Credit Card you need to look at it in the context of other available options. We compared this card to other rewards cards so you can see which may be more suitable for you.

Capital One Classic Credit Card vs Vanquis Classic Card

The Vanquis Credit Card is another popular UK credit builder card. Applicants with no credit history, poor credit history or are unemployed are all considered. Initial credit limits are lower, between £150 and £1,000, with a representative APR of 39.9%. Potential applicants can use the pre-application eligibility checker to see their likelihood of being accepted before they apply (useful to help avoid an unnecessary hard credit check and a rejected application).

Quick Takeaway: The Vanquis representative APR is around 5 percentage points higher. (It's best if you can pay off your entire balance on time each month to avoid interest charges, which can be significant on any credit builder card, anyway.) If you're not eligible for the Capital One card due to bad credit, it may be worth trying the pre-application check with the Vanquis Classic.

Capital One Classic Credit Card vs Marbles Card

The Marbles credit card is also designed for those with bad credit who want to rebuild their credit rating. Initial credit limits are a touch higher, between £250 and £1,200, with a representative APR of 34.9% that could drop by 5% over two years if you make at least your minimum payment on time every month.

Quick Takeaway: In terms of initial credit limit and APR, these cards are really pretty similar. The Marbles card has the advantage of their stated price promise, which will see your interest rate drop by 5% over two years if you use the card the right way. But the Capital One card states they consider credit limits rises as standard over your first two years. Which is more important to you?

Capital One Classic Credit Card vs Barclaycard Forward

The Barclaycard Forward credit card is also designed for those working on your credit history if you’re new to credit cards or want to improve your credit rating. Initial credit limits may be lower, and can start as low as £50. But the representative APR of 29.5% may be lowered by up to 5% over two years (3% in the first year and 2% in the second year).

Quick Takeaway: You may get a lower credit limit with the Barclaycard, but get the benefit to you and your credit record of having your interest rate drop in each of the first two years—if you use the card the right way (that is, you make at least your minimum payments on time).