How To Tell What Business Contents Cover You Need

Find business contents insurance quotes today. Powered by QuoteZone.

- Rated 4.7 out of 5 stars on Reviews.co.uk

- Over 300,000 quotes completed per month

- Fill out only one form

Compare Quotes

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Does your business have equipment, tools, inventory, and computers? And would it be expensive to replace these items? If so, business contents insurance can provide financial protection and keep your business up and running if you're the victim of theft or a disaster like fire or flooding. Here's what you need to know about contents insurance for a business, including common exclusions and who needs it.

- What is business contents insurance?

- What does business contents insurance cover?

- Common Exclusions

- FAQs

What is Business Contents Insurance?

Business contents insurance protects your tools, stock and business equipment if they're stolen or damaged. If your business is the victim of theft, fire, flood or other disaster, contents insurance can help your business avert financial disaster and keep trading.

Contents insurance is considered a critical component of insurance coverage, because businesses often make a sizable investment into their equipment and stock. And without these items, you might not be able to trade.

Business Contents Insurance Examples: Theft and Property Damage

Business contents insurance covers your tools, stock and equipment from a wide range of perils, from fire to flood to theft. Here are real-world examples illustrating how contents insurance can benefit a business in a time of need:

- A burst water pipe damages computer equipment in an office building.

- A thief breaks into your home-based business and steals your business laptop.

- A fire in a restaurant's kitchen damages critical equipment like ovens, freezers, pots, pans and mixers.

- Flooding in a newly-renovated pub damages sofas, tables, chairs and linens.

- A builder's tools costing thousands of pounds are stolen from their storage facility.

What's Covered?

Business contents insurance protects business items that are stored on or even near your business premises, and can cover the following types of items:

Business Items Commonly Covered

- Business equipment (e.g., computers, printers, tablets, telephones, mobile phones, etc.)

- Furniture

- Goods held in trust (e.g., items sold to customers but not yet delivered)

- Inventory

- Items or tools belonging to employees or other visitors (e.g., pedal cycles, tools and personal items)

- Laundry equipment

- Tools and equipment specific to your profession (e.g., food processors in a restaurant, power tools for a contractor, etc.)

- Trade samples, brochures and promotional materials

- Valuable paper documents or billing records

However, you may need to pay extra for some types of contents cover. For example, stock insurance to protect a business's inventory is sold as an add-on feature to contents insurance, and the premium for stock cover will depend on factors like the value of your stock. And you may need to pay extra to cover your store front, glass and external signs for which you are responsible.

Perils Typically Covered

What does a business contents policy protect against? While terms and conditions vary by insurer, it's common for the following types of scenarios to be covered by a business contents insurance policy in the UK:

- Civil commotion

- Earthquake

- Explosion

- Fire

- Flood

- Lightning

- Malicious damage

- Riot

- Robbery

- Storm

- Theft

Why Do I Need Contents Insurance for my Business?

Businesses need contents insurance to help them avert financial disaster and keep trading if they're the victim of theft, fire, flood or other disaster.

Without contents insurance in place, you'll be on the hook to pay for any business items that are stolen, or lost or damaged in a fire, flood or other disaster scenario. Even if you have funds available to replace lost equipment, this could result in a significant financial loss. And if you don't have funds on hand to replace lost, stolen or damaged business items, then you could have to cease trading temporarily or even shutter your business. Contents insurance can solve for this problem.

Who Needs Business Contents Insurance?

Most businesses buy contents coverage as an integral part of their business insurance package. In fact, any business with items, stock or equipment should have contents insurance—especially if replacing those items would be financially detrimental to your business.

Do you work from home? Your home insurance probably won't cover your business stock and equipment, so you'll need to get separate business contents to cover these items. Even if you have a small business and only have one computer, business contents insurance can be useful to provide financial protection and help get you up and running ASAP after a disaster.

Common Exclusions

As with all insurance policies, contents insurance won't cover everything and each policy will be subject to terms and conditions. For example, business contents insurance policies typically won't cover frozen food (unless you pay extra for this cover) as that falls under deterioration of goods. While conditions will vary, there are some common exclusions to be aware of when it comes to contents insurance:

- Gradual deterioration or wear and tear

- Faulty design, materials or workmanship

- Dampness, dryness, mould, fungus, rot, rust, corrosion, vermin, insects, moths, etc.

- Change in temperature, colour, flavour or texture or finish

- Mechanical or electrical breakdown of contents

- There may be inner limits on wines, spirits and tobacco products (e.g., £1,000)

- Stock stored in a basement might be subject to a minimum storage distance off the floor (e.g., 15 cm)

- Theft claims if your premises were not secured according to the conditions of your policy

- Loss or damage from dishonesty or fraud by an employee or person lawfully on your premises

Repair, Replace or Cash?

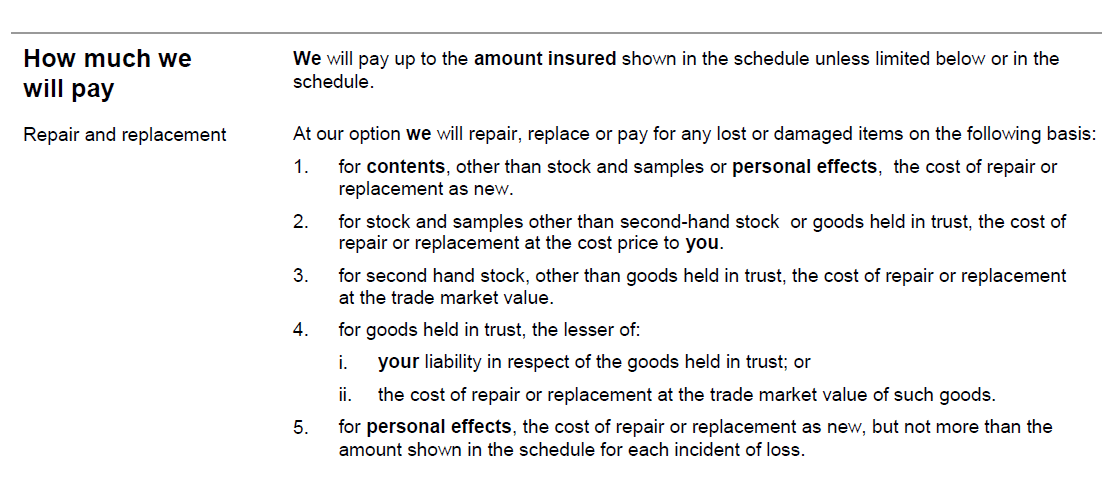

When buying a policy, look at the fine print to understand the basis your insurer will use to settle a claim—that is, an insurer can repair, replace or pay the cash value up to the amount insured in event of a claim.

- Repair

- Replace

- Pay cash

And the terms may differ depending on the types of content—that is, an insurer may calculate the basis differently for stock, samples, personal items and other content as you can see in the sample below from the policy wording for Hiscox office contents coverage.

As you can see above, Hiscox pays for most contents and personal items based on a new-for-old basis. For example, if the furniture in a business was damaged in a fire and not repairable, the policy would pay the cost to replace them as new, disregarding any depreciation. Other policies might offer old-for-old cover so it's also worth checking this detail when buying contents cover.

FAQs

Yes, contents insurance is considered to be a legitimate business expense, because it would help to keep your business running in the event of a disaster like theft, floor or fire.

No, breakdown of equipment is not covered by business contents insurance. However, many UK insurers sell equipment breakdown coverage that can provide financial protection against unexpected and sudden mechanical or electrical failure.

Some business contents policies might cover a small amount of stock (e.g., £5,000) but you usually need to pay extra for stock cover. And your premium should reflect the value of your inventory (e.g., that is, its cost to you).

The cost of business contents insurance starts from around £136 a year, but prices can vary depending on many factors unique to your business and needs.