Compare Public Liability Insurance Quotes (June 2024) | NimbleFins

-

Compare public liability insurance.

Powered by QuoteZone.Get Quotes

- Rated 4.8 out of 5 stars on Reviews.co.uk

- 300,000+ quotes completed per month

- Fill out only one form

Compare public liability insurance.

Powered by QuoteZone.Get Quotes

- Rated 4.8 out of 5 stars on Reviews.co.uk

- 300,000+ quotes completed per month

- Fill out only one form

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Whether you're self employed, running a small business or organising an event, you need to consider public liability (PL) insurance, which covers you if a member of the public claims you've cause injury or property damage. Between legal fees and settlement payments, compensation claims can cost tens of thousands of pounds or much more—potentially causing financial ruin if you're not insured. Here's what you need to know about public liability insurance, one of the most common types of business liability insurance.

- Public Liability Insurance Quotes

- NimbleFins Compares the Best Public Liability Insurance Companies

- How much does Public Liability Insurance cost?

- What is Public Liability Insurance?

- Common exclusions

- What to expect when buying Public and Products Liability Insurance

- Where can I get Public Liability Insurance quotes?

- FAQs

Compare Public Liability Insurance Quotes

Compare public liability quotes by sharing a few details about you and your business, and you'll be connected with up to 5 insurance providers. You’ll have a chance to build a policy to fit your needs specifically, and ask any questions you might have before signing up.

Compare public liability quotes.

Powered by QuoteZone.

Get Quotes

- Rated 4.8 out of 5 stars on Reviews.co.uk

- 300,000+ quotes completed per month

- Fill out only one form

In addition you can compare prices before you buy by getting quotes for public liability insurance online with another search engine such as Simply Business, or find a BIBA broker using their search tool, or use a direct insurer like Direct Line, AXA or Hiscox.

Before you sign on the dotted line, be sure that an insurer is qualified to offer insurance by checking the Financial Services Register, which is maintained by the Financial Conduct Authority.

Quick Public Liability Facts

What does public liability insurance cover mean?

Public liability insurance covers situations where a member of the public (e.g., customer, passer-by, etc.) claims your business has caused personal injury or property damage. It's frequently available with £1M, £2M, £5M and £10M of cover.

How much does public liability insurance cost?

According to NimbleFins research, the average cost of public liability insurance for small businesses in the UK is around £120 per year. However, public liability insurance costs can vary widely from one business to the next depending on the risk profile, so to compare prices for your business fill out a quote form here.

Who needs public liability insurance?

Any type of business with exposure to members of the public or their property might need public liability insurance, including:

- Sole traders

- Partnerships

- Companies

- Charities

- Events

Is public liability insurance required?

- Public liability insurance is not a legal requirement, but it might be required by your clients and partners—even when not 'required' it can be important when work involves exposure to members of the public.

Get public liability quotes.

Powered by QuoteZone.

Get Quotes

- Rated 4.8 out of 5 stars on Reviews.co.uk

- 300,000+ quotes completed per month

- Fill out only one form

Below we rank the best public liability insurance companies for businesses, explain the different risks faced by businesses, and how to protect yourself with a PL policy. Check out the examples of how public liability works, see our poll to learn how much PL cover our readers typically go for, and for quick takeaways see the grey boxes. To find out how much people typically pay for public liability insurance go to the average cost section and when you're ready to get quotes yourself, click here where you'll fill out a short form and can get a call back to help with any questions.

Compare Top Public Liability Insurance Companies

| Best Public Liability Insurance Providers | NimbleFins Rating (out of 5)^^^ | Popularity (monthly search volume) | Trustpilot / feefo Rating | % bad ratings | Trustpilot / feefo # Reviews | Compare Quotes |

|---|---|---|---|---|---|---|

| AXA | 3.9 | 4840 | 4.6 | 6% | 1,435 | Compare |

| Direct Line | 3.3 | 8040 | 4.5 | 8% | 5,926 | Compare |

| Hiscox | 2.9 | 2690 | 4.7 | 5% | 910 | Compare |

| Ageas | 2.6 | 80 | 4 | 13% | 15,564 | Compare |

| Aviva | 2.5 | 4190 | 4 | 15% | 33,875 | Compare |

| Optima UW by Ageas^^ | 2.3 | 190 | 4 | 13% | 15,564 | Compare |

| Covea | 2.2 | 40 | 3.6 | 32% | 1,763 | Compare |

| Lexicon UW by Covea | 2.2 | 60 | 3.6 | 32% | 1,763 | Compare |

| Chiswell UW by HDI Global specialty^ | 2.1 | 0 | 4.3 | 16% | 4,068 | Compare |

| Elements Insurance UW by Covea^^ | 2.0 | 20 | 3.6 | 32% | 1,763 | Compare |

| Markel | 1.9 | 90 | 4.1 | 14% | 149 | Compare |

- ^ Trustpilot ratings reflect Simply Business because there are no online customer reviews for Chiswell or HDI Global.

- ^^ Trustpilot ratings reflect the underwriter.

- ^^^ To see how we calculated our rating, see our methodology section.

According to NimbleFins research and comparison, the best public liability insurance company in the UK is AXA, followed by Directline and Hiscox. To compare the best public liability insurance companies, NimbleFins dug deep into policy wordings, tested quotes for several different types of businesses and compared customer ratings for a dozen providers. Here they are, ranked from best to worst. Read more about how we calculated this ranking in our methodology section at the end.

Top-ranked AXA stood out for covering the widest range of professions and coverage limits, although their prices were a touch more expensive than some broker-provided policies. Discount codes for AXA are often readily available through browser add-ons such as Honey, and AXA themselves will often notify you of available discounts at checkout, so whilst their base prices can seem high AXA wins out for breadth of covers available and pricing flexibility. If you call in you may get a discounted quote as well, all of which added together makes AXA our top choice.

Direct Line and Hiscox, two direct insurers, rounded out the top 3 providers for public liability insurance for small businesses. Both have comprehensive offerings but offer them for less professions. Honorable mentions go to Aviva, for having some useful policy features and Markel, for being the easiest company to obtain a quote through.

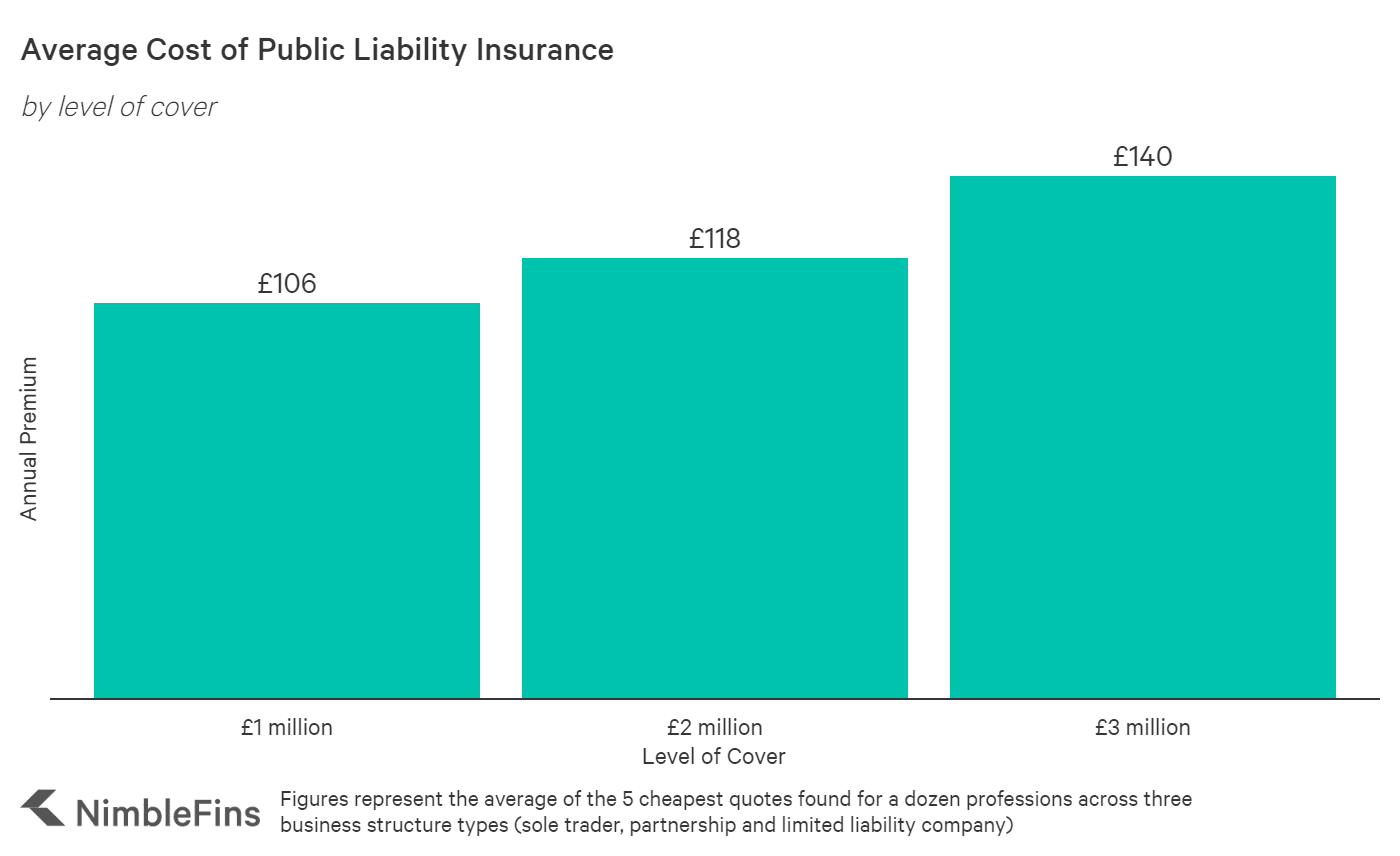

How Much does Public Liability Insurance Cost?

According to NimbleFins research of dozens of types of businesses and occupations, the average cost of public liability insurance for small businesses in the UK is £118 a year or £14.30 a month.

However, as Public Liability is priced based on the specific risks of your business, rates for your business may be lower or significantly higher than this average. For example, liability insurance for a limited company can be more than self-employed public liability insurance.

When quoting a Public Liability insurance product, an underwriter will take into account many factors, including:

- Level of cover

- Size of your business

- Line of work

- Location

- Number of employees

- Business structure (e.g., sole trader, partnership or limited liability company)

- Number of directors or partners

- Claims history

- Additional coverages

Businesses that face higher risks will pay higher premiums than businesses viewed as lower risk, all else equal. For example, a builder will likely pay higher premiums than a photographer. Insurance underwriters perform their own internal risk calculations and so you may receive very different quotes from different insurance companies, even if the cover is equivalent between companies.

In fact, quotes could have more to do with an insurer's internal risk management than with your business specifically. For example, if an insurer decides they have written too many Public Liability insurance policies for contractors lately, their risk appetite for writing new contractor liability policies may be quite low. As a result that company's quotes for new contractor liability policies could be much higher than the rest of the market.

Considering all of this, it is always worth comparing how different insurers will price Public Liability cover for your business—whether you are renewing or buying your first policy for a new small business.

Public Liability Insurance Discounts and Promotion Codes

Promotion: Save 15% to 25% by paying upfront instead of monthly with many insurers.

What is Public Liability Insurance?

Public liability (PL) insurance protects businesses against claims made by third parties if personal injury or property damage occurs on the business premises or while working off-site. PL insurance is the most common type of business insurance for a reason. Most businesses face some exposure to third party liability risk and public liability insurance can protect a business financially from the litigation costs and compensation payments that can follow certain types of accidents. If your business unintentionally causes bodily injury or property damage to a third party, public liability can cover:

- Legal costs

- Compensation payments

- Medical bills

- Repair costs

If a client, customer, vendor or member of the public is accidentally injured or their property damaged by your business (this includes damage resulting from actions by you or an employee, as well as from your product if product liability is a component of your cover), then Public Liability insurance can help protect your business if it is brought to court. The number of public liability claims in the UK topped 70,000 in 2019/20, making PL insurance a critical risk management tool for tens of thousands of businesses each year.

Example:

- You own a small gift shop that sells locally-produced, handmade artisan products. To keep up with a weekend rush you decide to restock your shelves with some of your most popular items. A customer trips over a box you left in an aisle and falls. He injures his shoulder which prevents him from working and decides to sue your shop for damages. Your Public Liability policy will cover any legal costs and settlement claims up to your coverage limits.

Do I Need Public Liability insurance?

Public Liability insurance is not a legal requirement. In terms of the law, it's voluntary—but in most cases public liability insurance is still critical for many businesses. Ask yourself this question: Does my business (including you or your employees) have any in-person exposure to third parties like customers, clients, vendors, suppliers, cleaners, landlords or other members of the public—or their property? If so, public liability insurance can cover legal expenses and compensation in case of accidental injury or damage.

Public liability cover is important for any business that interacts with members of the public or their property. Any contact with a third party can lead to a potential accident, exposing a business to the risk of financial loss. Businesses that have the greatest need for Public Liability insurance are those who have the most contact with the public, for instance pubs, cafes, restaurants, shops, salons and builders or tradesman—but any business with third party exposure should have public liability coverage.

Additionally, Public Liability insurance may be required by some trade organisations or customer contracts. For example:

- The Association of Plumbing & Heatings Contractors Limited (APHC) has minimum insurance requirements if you want to become a licensed member

- A commercial property development project might require electricians working on the project to have a minimum amount of Public Liability cover—e.g., Barratt Homes requires subcontractors to supply proof of insurance with a minimum of £5,000,000 of public liability (in addition to employers' liability and professional indemnity, as needed)

- A wedding caterer will be required to have Public Liability cover in place to work in a self-catering venue

What Does Public Liability Insurance Cover?

Public liability insurance covers compensation payments and associated legal costs for three types of accidental damage that could be caused by your business:

- Bodily injury

- Property damage

- Wrongful arrest

If your business is sued over these types of third-party damages, your Public Liability insurance underwriter can cover legal defense costs as well as compensation payments. Note: you won't be covered for claims resulting from the work that you're doing. That is, if work you're carrying out directly causes damage this is not usually covered. So, for example, if a carpet cleaner uses a fluid on the carpet that discolours it, public liability insurance would NOT typically cover a claim to replace the client's carpet. But if the carpet cleaner accidentally broke an expensive mirror while carrying the carpet cleaning equipment into the house, this should be.

Public liability is third-party insurance that covers damage to members of the public (e.g., your customers or passersby)—it does not cover damage to you, your employees or your business. To protect against injury or illness to employees you'll need employers' liability insurance, which is actual a legal requirement. To learn about the differences between public liability and employers' liability insurance, read our article about it here.

Property Damage

Public Liability insurance covers damages if your business (including you or one of your employees) causes property damage to someone else's property.

Examples:

- You have a plumbing business that installs the sink in a domestic kitchen renovation. Unfortunately, a fault in a seal means the kitchen floods and damages the wooden floors and surrounding cabinets.

- You run a small cleaning business. While an employee is cleaning someone's home, a valuable vase is accidentally knocked over and broken.

However, Public Liability insurance does not cover damage to your business's property—it is a third-party cover so just covers property not associated with your business. (Damage to your business would be covered by commercial contents or buildings insurance).

Example:

- You own a takeaway restaurant, and a fire starts in the deep fryer. The fire spreads to a neighboring salon, damaging their storeroom. Your Public Liability Insurance would cover damage to the salon's property (e.g., the building and contents), but would not cover damage to your business.

Bodily Injury

Public Liability insurance covers your business if a third party (e.g., a customer or vendor, but not an employee) suffers a bodily injury resulting from your business operations or whilst on your business premises. Your underwriter will cover costs to investigate and defend a claim (e.g., solicitor fees, court costs, etc.) as well as any compensation payments and medical fees.

Examples:

- You own a dog walking company. One of the dogs in your care jumps on an elderly person in the park, knocking them down and causing them to break a hip.

- You run a bouncy castle business. One of the anchors holding a bouncy castle to the ground fails and the inflatable tips, injuring some of the children inside.

It's important to understand that bodily injury on a Public Liability insurance policy does not cover you or your staff. If you or an employee are injured at work, a combination of Employers' Liability and Personal Accident/Personal Injury insurance can offer protection.

Product Liability

Product Liability insurance covers legal fees and compensation payments that you're legally liable to pay if a product your business has supplied (e.g., manufactured, distributed or sold) results in injury or damage to a third party. This coverage applies to incidents that occur away from your business premises; and in fact claims can be brought up to 3 years after a product is used.

Product Liability insurance is often sold as a part of a Public Liability policy, but it may be offered as a separate, extra coverage that a business buys on top of their Public Liability insurance. It is rarely sold on its own without Public Liability.

Examples:

- You are a market trader who makes and sells homemade curry sauces at fairs. After selling your famous Jalfrezi at a fair one day, people fall ill and blame you for food poisoning.

- You manufacture handmade shoes. The heel on a pair of your high heels snaps off, causing a woman to fall and injure herself.

Non-Physical Damages

In addition to bodily injury and property damage coverages, Public Liability insurance also typically covers awards of damages for several non-physical injuries. These coverages will be specifically defined in your Public Liability insurance policy wording. Non-physical types of claims cover the unintentional results of intentional actions (vs. the bodily injury and property damage clauses of a Public Liability policy that cover negligence accidents, or unintentional actions).

Examples:

- Wrongful arrest: A clothing shop accuses a customer of shoplifting and calls the police, who subsequently arrest the customer. After reviewing the CCTV footage, it becomes clear that the customer did not shoplift, and was wrongfully arrested. The customer sues the shop.

- Wrongful eviction: A tenant is forced to leave their home by a landlord who has not followed proper legal procedures, such as getting a court order and using bailiffs to execute the eviction. The tenant sues the landlord for illegal eviction.

Legal Fees

If your company is sued for damages that are covered by your Public Liability insurance, the policy will cover the costs of your legal defense, including solicitors fees (e.g., to investigate or defend a claim against your company), court costs, etc.

Public liability cover for legal fees and expenses may be subject to a separate limit that is in addition to the injury and damages limit. For example, a Public Liability policy might have a £5 million limit for compensation amounts owed and a separate £100,000 limit for legal expenses incurred defending a claim.

Examples:

- You hold a Public Liability Insurance policy with £2 million of liability cover, plus £100,000 of legal defense cover. Your business is sued for bodily injury and found liable for a judgment of £500,000. Your legal defense team incurred £75,000 of expenses while defending your business. Your Public Liability Insurance underwriter would pay for the £575,000 in compensation and legal costs.

Medical

Public Liability insurance also covers your business financially if the NHS claims for expenses they incur such as hospital treatment and/or an ambulance call out.

What is Not Covered by Public Liability Insurance?

There are many common exclusions to Public Liability insurance you should be aware of. Each insurance provider will have their own set of terms, but here are a few common exclusions that you'll find on most public liability policies:

Public liability insurance will not cover:

- Damage or injury to works in progress or due to faulty workmanship. If damage occurs to a client's property that is a work in progress or as a result of faulty workmanship, this is typically excluded.

- Your business property and contents. Public Liability insurance only covers damage to the property of third parties. To cover your business premises and contents, you need commercial property insurance (building and/or contents, as appropriate).

- Design and advice. If you give or deliver advice, instructions or designs, these are not covered by public liability insurance; instead you need professional indemnity insurance (may also be referred to as professional liability insurance). If you are a professional, read about the differences between public liability and professional indemnity here.

- Employee injuries. Public Liability insurance only covers bodily injuries to third parties. To cover employees who are seriously injured or even killed by a workplace accident, you should buy Personal Accident insurance. Also, employers' liability is required by law if you have anyone working for you.

- Road traffic accidents. Your commercial auto insurance will cover motor vehicle claims related to your business.

- Damage caused intentionally. Any injury or damage that was caused intentionally is excluded.

- Crimes: Fines, penalties or compensation payments levied by a criminal court are not covered.

- Recalls and defects: Public Liability insurance won't cover the cost to remedy defects in a product, for instance via a product recall. However, product recall can be added to some products liability insurances, which can be wrapped up with public liability insurance. If you need it you’re best talking to a broker to obtain the proper coverage. It will not be cheap, though.

How Much Public Liability Insurance do I Need?

Small businesses in the UK commonly take out £1 million to £5 million of public liability insurance. However, the level of Public Liability insurance cover you need depends on your business structure and the line of work you do—in particular, how physically risky it it. For instance, a construction business will have a greater need for Public Liability cover than, say, a maths tutor. When deciding what amount of Public Liability cover is right for your business, consider the type of work you do and the size of possible compensation claims.

How Much Public Liability Insurance Should I Buy?

The amount of public liability insurance coverage you need is something you need to decide on your own—you won't find any insurance agents or brokers who will advise you regarding how much to buy. That said, they may be able to ask you the right questions to help you arrive at an answer.

It may be useful to know that it's frequently sold with £1 million, £2 million and £5 million of cover, but you can buy more or less. Ultimately it depends on the risks your business faces, the size of your business, and other factors.

If you have an idea of how much you'll purchase, we'd love to know what you're thinking. Please let us and our other readers know in the poll below!

What to expect when buying Public and Products Liability Insurance

Before calling a provider

Before you approach an insurer or broker, think about the areas of greatest concern for public liability claims – the things your business does which could cause injury to the public or damage to their property. Remember that ‘the public’ includes visiting representatives of other businesses, including subcontractors, tradesmen and businesses which occupy the same space as yours.

There are a range of activities and businesses with public or products liability risks to consider:

- Shops, offices and other commercial properties - slips, trips and falls over wires, products and stairwells

- Building and industrial sites - injury to trespassers or visitors, falling building materials, holes, exposed wires and falls from height

- Sole traders and freelancers - visits to client sites where you could cause an accident or injury, use of client equipment you might damage by accident

- Manufacturers, practitioners and producers - injury or illness caused to consumers of your product or services, such as bad food or injuries caused whilst giving a haircut or beauty treatment

Consider which of the above apply to your business, and be prepared to discuss your activities with insurers, including turnover amounts generated by different activities, the height and depth of your work, the number of employees or clients you have and the nature of any special treatments, products or services you provide. If you, your premises or your products have any certifications or safety features, be prepared to explain and provide evidence of these.

It’s best to start looking for insurance at least 30-45 days before renewal/start date to make sure you have time to answer insurer queries and review your quote documentation.

During a quote

Your insurer or broker will ask you for details as above and you may need to complete a proposal form – this is your signed statement as to the activities of your business, and it’s important that you complete this neatly and thoroughly – a messy or incomplete proposal form can prejudice insurers against you. If in doubt, call your provider to clarify details.

Be prepared to answer questions about the way you work, and to explain why you or your business does things a certain way. Underwriters may propose exclusions or conditions to any potential insurance policy - this is normal and you should be prepared to consider changing the way you work, and the cost of this compared to any savings you might make on your policy.

Depending on underwriter/insurer queries, you may need to arrange follow-up calls to provide further information. Quotes can take anywhere from an hour to a few weeks to finalise.

After receiving a quote

Once you have your quote, make sure to review it thoroughly - you will need to look through all terms, conditions, clauses and exclusions and contact your insurer or broker to discuss each to make sure you understand what you are being covered for exactly and what is expected of you.

At this stage you can take your proposal form and quote to other insurers/brokers to see if there are better or cheaper options to be had.

Be aware that many brokers use exactly the same insurers. You can request that your current broker disclose which insurers they have approached. Make new brokers aware of this so they can approach different insurers – this makes sure no ground is re-trod and your company doesn’t get a bad reputation for flooding the market with quote requests each year – insurers tend to stop quoting if they suspect this is the case.

During the life of your policy

Whichever insurer you choose, make sure to update them to changes in activities, income or contractual terms as soon as you know of them. This makes sure you have appropriate cover throughout the life of your policy but in the case of changes to your business, reduced risk or turnover it can also mean discounts. Lastly, it will ensure you maintain a good relationship with your provider – no insurer likes scrambling to rewrite a completely changed policy at the last minute!

FAQs

The limit on an insurance policy is the maximum amount that an underwriter will pay in claims. Your Public Liability policy may have separate limits "for any one occurrence" and "during any one period of insurance". A "per occurrence" limit is the maximum that an insurer will pay for a single claim, while the per period of insurance limit is the maximum they will pay for the policy year, regardless of the number of claims. Although other amount may be available, the most common limits in the UK Public Liability insurance market are:

- £1 million

- £2 million

- £5 million

- £10 million

Yes and no—it depends on the type of claim. Bodily injury claims typically have no excess. However property damage claims frequently have an excess which can range from £100 up to £750 or more. Some categories of claims might have separate excesses, for instance damage due to water damage.

There is no "general" liability insurance product in the UK. To provide a wide range of liability coverage, you can buy Public Liability, Product Liability (which is sometimes included in Public Liability policies) and/or Employers' Liability insurance.

There is no difference between public liability and third party insurance; the terms are interchangeable however 'public liability' is the broadly accepted name.

Yes—while public liability cover protects against injury or damage claims from third parties like customers or visitors, employers' liability covers injury or illness claims from a business's employees.

Sole traders who mix with members of the public in a business capacity can get sole trader public liability insurance to cover situations where a third party is injured or their property damaged accidentally. It can be especially important for sole traders who don't have the protection of a company.

Self-employed people who mix with members of the public in a business capacity can get self employed public liability insurance, which can be especially important as anyone who is self employed doesn't have the protection of a company.

Public liability insurance can provide a financial benefit if a business is blamed for causing accidental injury or property damage to a third party.

Yes, an individual can get public liability insurance. In fact, public liability insurance is commonly considered to be quite important for individuals working in a sole trader capacity as they don't have the protection of a company.

Public liability insurance is calculated based on a business's industry and line of work, their turnover, previous claims history, the limit of insurance, the excess, and many other factors.

Public liability insurance is not a legal requirement like employers' liability, however it may be required for certain business contracts and is generally advisable in cases where business and members of the public mix.

Yes, you can usually pay public liability insurance monthly—but when you consider the relatively low cost of a policy and that monthly payments often incur finance charges, it might make more financial sense to pay upfront.

Yes, you can cancel public liability insurance. However, it is likely that you will have to pay a cancellation charge which can be in the range of £50. If you've paid upfront, you may or may not be entitled to a partial refund.

To compare public liability insurance deals, start by looking at the premiums, limits of insurance (e.g., £2M, £5M, etc.) and the excess. You may also want to check customer ratings of the provider online.

To claim against public liability insurance you'll need to contact your broker or insurer to initiate the process. Also check your policy wording to understand the conditions you must follow to ensure a successful claim.

In Summary

Public Liability insurance can help protect you and your business financially if a member of the public sues you after accidental injury or property damage due to your negligence. It is widely purchased by a wide spectrum of businesses from tradesmen to cleaners to shops. As compensation claims can run into the thousands or millions of pounds, most business owners look to include public liability as a critical component of their business insurance package.

Public Liability Insurance Requirements by Occupation

To learn more about the specific insurance needs for your industry or profession, visit our main business insurance landing page which includes a list of articles about insurance for different professions. We are currently building our library of profession-specific business insurance pages. If we haven't yet written about your profession, please let us know in the comments section below and we'll get on it!

Panel

The panel of public liability insurance providers you can access through us is powered by QuoteZone and includes a wide range of businesses from big names such as Towergate to smaller brokers. Click here to start the quote process, and the comparison engine will select up to five insurance providers from the panel to share your quote details with; they may call you to discuss your quote at which point you can ask any questions you have that we have not answered here.

- A-Plan

- Be Wiser

- Brady Insurance

- Broadsure Insurance

- Business Choice Direct

- Compare Insurance

- Coversure Insurance

- Custodian

- GSI Insurance

- Inspire Insurance

- Insync Insurance

- Konsileo

- Nova Insurance

- Plan Insurance

- Pol-Plan Insurance

- Professional Liability Brokers

- Rainbow Connected

- Rhino Trade Insurance

- SJL Insurance

- Tapoly

- Towergate Insurance

- Yellow Jersey Cycle Insurance

Methodology

We use a points-based system where a provider gets a final score based on number of policy features offered x average review (expressed as a percentage), where multiple reviews exist on different platforms we weight by number of reviewers and recombine at the end to get a final percentage, so a bad review from one reviewer on one site doesn't skew the numbers (their review will be worth 1/800th of the review score given by 800 people on another site, for example). Once we have final scores for each occupation, we take that score and table it for a visual expression of insurer features and flexibility, before applying a separate methodology to rank across all insurers tested.

We also included a 'no quote' penalty in the final score, for insurers that wouldn't quote for any of the professions/businesses we tested (administration services, sports coach for kids, builder working at less than 10m height and a gift shop). That means for every unavailable policy an insurer has, they lose 1/5th of their final score, with the number in this column representing a true combination of all factors we're comparing.

Here is a quick recap of the business profile we used in our testing: 5+ years experience, no financial problems, £50,000 turnover, vanilla/low risk activities, no international work, ltd company, one director and one employee (20k wages, no PAYE details) doing manual work (where relevant, i.e. no manual work for a clerical business), retroactive cover requested, low risk option always chosen.

To obtain quotes from each insurer we went directly to their site, but where insurers do not quote directly we made use of online comparison and brokerage sites to produce quotes. Please note that brokered policies can differ from broker to broker, despite being underwritten by the same company, so you should always read through policy wordings and make sure you understand exactly what is being covered when purchasing any insurance policy.

Here are the results:

Public Liability Insurance Comparison (scores out of 5)

| Rank | Insurer | Limits Available | PL Pricing | EL Pricing | Excess Levels | Policy Features | Customer Ratings | Range of Professions | Final score/5 |

|---|---|---|---|---|---|---|---|---|---|

| 1 | AXA | 5.0 | 3.5 | 2.5 | 2.8 | 5.0 | 4.3 | 5.0 | 3.9 |

| 2 | DirectLine | 5.0 | 4.0 | 4.3 | 3.3 | 5.0 | 4.5 | 3.8 | 3.3 |

| 3 | Hiscox | 4.4 | 3.7 | 4.0 | 2.5 | 5.0 | 3.6 | 3.8 | 2.9 |

| 4 | Ageas | 3.3 | 3.7 | 2.3 | 5.0 | 1.7 | 4.6 | 3.8 | 2.6 |

| 5 | Aviva | 2.8 | 3.7 | 2.7 | 2.5 | 5.0 | 3.3 | 3.8 | 2.5 |

| 6 | Optima UW by Ageas | 2.8 | 3.7 | 2.3 | 3.8 | 1.7 | 4.4 | 3.8 | 2.3 |

| 7 | Covea | 3.3 | 3.7 | 2.0 | 3.8 | 1.7 | 3.6 | 3.8 | 2.2 |

| 8 | Lexicon UW by Covea | 3.3 | 3.7 | 2.3 | 2.5 | 1.7 | 4.4 | 3.8 | 2.2 |

| 9 | Chiswell UW by HDI Global specialty | 5.0 | 2.7 | 2.0 | 1.3 | 1.7 | 4.4 | 3.8 | 2.1 |

| 10 | Elements Insurance UW by Covea | 2.8 | 3.7 | 2.0 | 1.3 | 1.7 | 4.4 | 3.8 | 2.0 |

| 11 | Markel | 3.3 | 4.5 | 4.0 | 2.5 | 5.0 | 3.9 | 2.5 | 1.9 |

| 12 | Churchill UW by U K insurance Ltd | 4.2 | 4.5 | 2.5 | 2.5 | 1.7 | 4.3 | 2.5 | 1.6 |

| 13 | NIG uw by U K insurance ltd | 3.3 | 4.0 | 2.0 | 2.5 | 1.7 | 3.9 | 2.5 | 1.5 |

| 14 | Zurich | 1.7 | 2.5 | 1.0 | 2.5 | 1.7 | 4.6 | 2.5 | 1.2 |

| 15 | AIG uw by AIG | 3.3 | 4.0 | 3.0 | 1.3 | 1.7 | 4.3 | 1.3 | 0.7 |