Picking the Best Balance Transfer Credit Card

Before you head to a comparison site for a balance transfer, learn how to spot a good deal (for you) when you see one—because individual factors like your outstanding credit card debt and the amount you can repay each month will determine which offer is best suited for your needs.

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

-

Picking

The Best Balance Transfer for You -

Balance Transfer Calculator

Months to Pay Down Debt -

Examples

Different Scenarios -

Watch Out

Balance Transfer Fine Print

Balance transfer comparison tables can be quite confusing, so it helps to first figure out which type of offer best suits your financial situation before you dive into the melee. Balance transfers are a bit like the Goldilocks story—the best for one person might be suboptimal for next person.

What is a Balance Transfer credit card?

A balance transfer is a specialist type of credit card that allows you to shift existing credit card debt to it.

Importantly, balance transfer cards come with an interest-free period. This means any debt you shift across won’t attract interest for the duration of the 0%. As a result, all of your repayments during the 0% period will go towards cutting your debt, as opposed to servicing interest. This gives you the power to become debt-free sooner.

Put simply, if you’re paying interest on a credit card, a balance transfer can be your golden ticket to cutting what you owe. Not only that but if you use a balance transfer correctly—by fully repaying your balance before the end of the 0% period—you can clear your debts without having to pay any interest whatsoever.

Do note that 0% balance transfer credit cards aren’t all the same. While some cards offer exceptionally long 0% periods, they often come with a one-off fee. This fee is usually a percentage of the amount of debt you wish to shift. However, some cards come without a fee, though 0% periods on fee-free cards are often much shorter than the longest deals.

What are the top Balance Transfer credit cards?

| Card | 0% length, up to | Transfer fee | Rep APR (after 0% ends) |

|---|---|---|---|

| TSB | 38 mths | 3.49% | 24.9% |

| Barclaycard | 36 mths | 3.15% | 24.9% |

| MBNA | 36 mths | 2.99% | 24.9% |

| NatWest | 36 mths | 3.10% | 24.9% |

| RBS | 36 mths | 3.10% | 24.9% |

| Ulster Bank | 36 mths | 3.10% | 24.9% |

| Virgin Money | 36 mths | 3.4% | 24.9% |

| Tesco Bank | 36 mths | 3.45% | 24.9% |

| Halifax | 35 mths | 2.49% (min £5) | 24.9% |

| Lloyds Bank | 35 mths | 2.49% | 24.9% |

| Santander | 34 mths | 3.15% (min £5) | 24.9% |

| HSBC | 35 mths | 3.19% (min £5) | 24.9% |

Poorer credit scorers may be offered shorter periods at 0% plus a higher rep APR.

Top balance transfer no fee cards

If you’re confident you can clear your credit card debt within a shorter period that the longest deals above, you may be better off opting for a fee-free balance transfer card. Here’s a pick of the best cards.

| Card | 0% length, up to | Transfer fee | Rep APR (after 0% ends) |

|---|---|---|---|

| Barclaycard | 14 mths | None | 24.9% |

| Santander | 12 mths | None | 24.9% |

| Virgin Money | 12 mths | None | 24.9% |

| NatWest | 11 mths | None | 24.9% |

| RBS | 11 mths | None | 24.9% |

| Ulster Bank | 11 mths | None | 24.9% |

Poorer credit scorers may be offered shorter periods at 0% plus a higher rep APR.

How to Choose a Balance Transfer for You

Finding the best balance transfer offer is about figuring out how many months you need to clear your debt, then choosing a suitable 0% promotion with the lowest fee. (Shorter 0% promotional periods generally charge a lower balance transfer fee). So, to pick the right card for you, follow these three simple steps:

- 1. Decide how long you need to pay down your debt in months, as balance transfers are marketed in months not years (e.g., 18 months)

- 2. Find balance transfer offers with a similar 0% APR period (e.g., 18 to 20 months)

- 3. Of those, choose an offer with the lowest balance transfer fee (but keep in mind other factors as well)

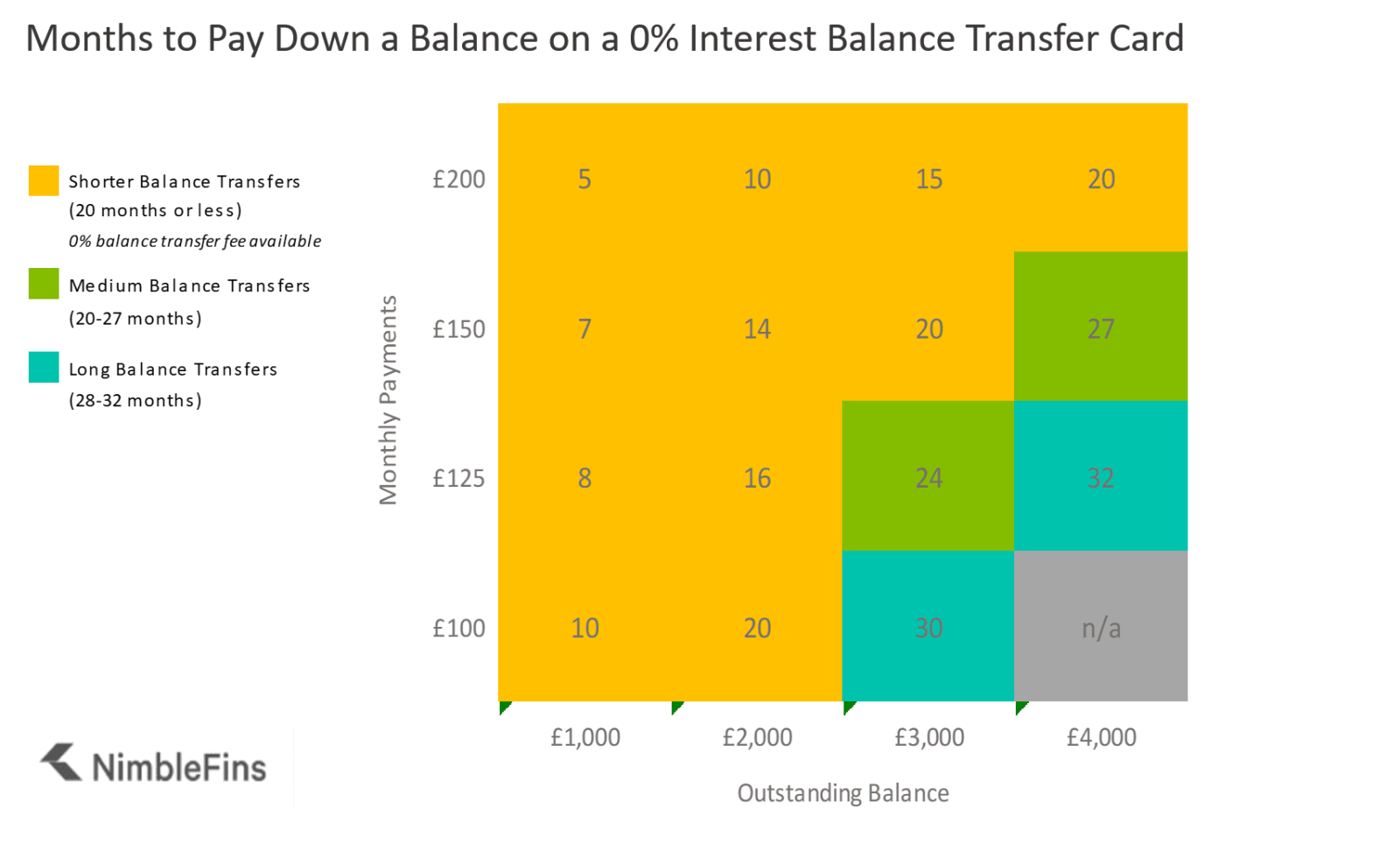

How Long of a Balance Transfer do You Need?

Choosing the right balance transfer card will depend on how long you need in order to clear your existing debt. To figure this out, use the table below which shows the months needed to pay down debt on a 0% interest card, by starting balance and monthly payment. For example, someone with a £2,000 outstanding debt who can pay £100 per month would be debt free in 20 months (£2,000 divided by £100 = 20 months).

| Months to Clear Debt on 0% Balance Transfer Card | £1,000 Balance | £2,000 Balance | £3,000 Balance | £4,000 Balance |

|---|---|---|---|---|

| £200 monthly payments | 5 | 10 | 15 | 20 |

| £150 monthly payments | 7 | 14 | 20 | 27 |

| £125 monthly payments | 8 | 16 | 24 | 32 |

| £100 monthly payments | 10 | 20 | 30 | 40 |

Balance Transfer Credit Card Calculator

How many months will it take to pay down your balance at 0%? Enter your starting balance and the amount you'll be able to pay per month (enter both as positive numbers, e.g. £3,000 and £150). Hit the yellow lightning run button to see how many months it would take to pay down the balance (assuming you maintain the 0% interest rate).

Credit Card Debt Payoff Calculator

Time to pay down credit card debt at 0%

Narrowing Down the Field

Once you have a feel for how long it will take you to pay your balance down to £0, look for a suitable balance transfer offer with a relatively low balance transfer fee. The balance transfer fee is a percentage of the transferred balance—balance transfer fees typically range from 0% to 3.5%. In most cases shorter balance transfer offers charge lower fees; longer balance transfer offers charge higher fees.

It makes sense that credit cards charge a higher fee for a longer 0% promotion, because the provider is essentially taking on risk for a longer period of time. However, pricing can be inconsistent from company to company, so it’s worth comparing options.

There is No Best

Actually, there is no "best" balance transfer card—it all depends on your financial situation. For example, someone who can pay off their debt within a shorter time frame (e.g., 12 months or less) may secure a no fee offer (i.e., a 0% transfer fee). On the other hand, someone needing more than 2 years to repay their outstanding debt may end up paying a fee (e.g., 1.5% - 3%) for the additional time.

We've heard it recommended on other websites to take a no-fee balance transfer (even if the 0% APR period isn't long enough for you) with the argument that you could always move the remaining balance to another 0% card at the end of the first card's 0% period—and so on. There are certainly risks to this method, however.

For example, if your credit profile has changed, or the risk appetite in the market, you might not find a new credit card willing to lend to you. Also, every time you apply for a new credit card this action is marked on your credit file. While this can impact your future creditworthiness, it usually isn’t a big deal unless you apply for lots of cards in a short space of time.

However, if you wish to reduce the impact on your credit score, and assess your chances of acceptance for any particular card before you apply, you may wish to use a balance transfer eligibility calculator. It’s also worth looking out for cards that offer ‘pre-approval’. That’s because if you’re pre-approved for a card, you’ll definitely be accepted when you apply, so there’s no risk of facing a rejection. If you're pre-approved for a card you'll also get the advertised length, even if the card is an 'up to'.

Balance Transfer Credit Card Offers

While the balance transfer market changes constantly, there are a few consistent players that seem to offer relatively competitive combinations of 0% APR period and fees. Amongst these are Halifax, Virgin, Santander and Sainsbury's. Keep an eye out for offers from these companies, although there may be better offers available in the marketplace. Below we highlight some different balance transfer scenarios.

Examples of How To Choose the Best Balance Transfer Credit Card for You

Balance transfer offers are defined by two key features: the fee and the interest-free period (or duration).

The balance transfer fee is a charge, usually calculated as a % of the balance you are transferring. This fee can range from 0% (e.g., "no fee") to 3.5%, or more and is payable once the balance is initially transferred. Do note that in order to pay the headline (low) fee, you'll usually have to transfer your balance within a set period after you get accepted for a card. This period is usually a few days, though it can vary from card to card.

The interest-free period is the number of 0% months you get on your transferred balance. This means you won’t have to pay interest on your credit card debt during this period. This gives you time to pay down the outstanding amount via the form of monthly payments.

The size of the fee is typically related to the interest-free period. Usually, the longer the interest-free period, the higher the fee. You can find shorter-duration cards, with interest-free periods up to 20 months or so, that charge no fee at all.

Best Balance Transfer: You don’t want to pay a fee

Those who can pay off their debt within 1 - 1.5 years can find offers in the market that don't charge a balance transfer fee at all (so long as you make the transfer within the initial window, usually 30-60 days). Choosing a no-fee balance transfer offer means you can pay back your debt without paying any fees or interest charges at all—all of your payments will go directly towards paying down your outstanding balance, leaving you debt-free sooner.

Best Balance Transfer: You need as much time as possible to pay down your debt

If you need a bit more time to slowly pay off your credit card debts, there are balance transfer cards that won't charge interest for up to 30 months or so. This has come down from 2017/18 when the longest balance transfers were up to 43 months. Balance transfer cards offering the longest durations charge a one-off fee when you transfer the balance, which is typically around 3%.

Best Balance Transfer: You want a balance transfer card for new purchases, too

If you have transferred a balance that is now sitting on a balance transfer card, once you're past the 0% on purchases intro period (if there is one), avoid putting new purchases on this same credit card. Doing so will subject your new purchases to unnecessary interest charges.

The fine print in the Interest section in the Summary Box of most credit cards advises that new purchases will remain interest free IF you pay the full balance in full each month. This balance includes the amount of any transfers.

So even if you intend to pay off new purchases every month to avoid paying interest on them, if your card still has some of your transferred balance, you will be charged interest on new purchases from their transaction date until the date you pay them off. There's no "grace period." For this reason, save yourself money by putting new purchases on a card that you haven't used for a balance transfer.

If you want to learn more, read our article What is a Balance Transfer.

Balance Transfers: What to Look Out For

There are a few circumstances in which you can lose your 0% promotional interest rate or your promotional transfer fee—in either case it will cost you.

- Transfer the balance within the initial window (often 30-60 days) to be eligible for the 0% promotional interest rate

- Pay on time each month AND stay within your credit limit to keep your 0% promotional interest rate

- Weaker credit scores may get a shorter interest-free period (e.g., 12 months instead of 20 months). Check this detail on any card before you apply—these cards are marketed with a 0% APR up to a certain number of months

In almost all cases by exceeding your credit limit or not paying at least the minimum monthly payment on time, you will lose the 0% APR intro period. If that happens, you will be charged interest at the stated balance transfer rate, which is usually well in excess of 19.9% APR. (You can read more about typical APRs in our article Average Credit Card Interest Rate (APR).)

Also, your balance MUST be transferred within a specified window—typically 60 or 90 days—or you'll pay a higher transfer fee and the stated interest rate (typically 19.9% or more). Also, it's important to be aware that, depending on your circumstances, you may be offered a shorter promotional period and/or higher representative APR.

Regardless of the card you choose in the end, remember to always stay within your credit limit and pay at least the minimum monthly payment on time, or you'll lose the 0% APR intro rate.

How a Credit Card Balance Transfer can be Beneficial

Balance transfer credit cards can help consumers manage their credit card debt, by moving an outstanding balance from one or more interest-charging credit cards to a 0% interest card. Balance transfer credit cards can have a positive impact on your financial situation in two ways:

- No interest charges: Save money by not paying any interest charges on your outstanding balance during the 0% promotional period.

- Become debt free sooner: Generally speaking, the whole of your monthly payment will be applied to pay down your balance, allowing you to become debt free sooner.

Making Monthly Payments on a Balance Transfer Card

You are still required to pay (at least) your monthly minimum payment every month. In other words, "0% balance transfer deal" doesn't mean you have nothing to pay each month, it just means that you don’t have to pay any interest during the interest-free period. In fact, you must make at least the minimum monthly payment on time or you'll lose your 0% promotional rate! The easiest way to avoid falling foul of this rule is to set up an automatic direct debit.

TOP TIP: Let's clarify one thing here—while you’re only required to make at least the minimum monthly payment to keep the 0% period alive, in order to clear your balance within the interest-free period, it’s likely your monthly payment will have to be a lot more than the minimum. How much should you pay each month? Figure this out by dividing the transferred balance by the number of months you pay 0%.

Let's work through an example of the average UK cardholder with a balance of £1,500 on a credit card that is charging you 19.9%. If you can secure a 0% balance transfer offer for 15 months, then you should ideally pay £100+ a month to clear your balance during the promotional period

How To do a balance transfer?

Once you have been accepted for a new balance transfer credit card, transferring your balance is quite easy. While each bank will have a slightly different process, it generally works like this:

- 1) Log into your online account (the bank will instruct you how to set this up)

- 2) Click on the link to transfer a balance

- 3) Enter the amount you want to transfer

- 4) Enter the details of the credit card from which you are moving your balance

- 5) Check and hit submit!

FAQs

Help With Debt

If you're worried about paying back your debts, it can be a good idea to get in touch with one of the many debt charities in the UK. They can help you plan the best way to pay back your debts and may suggest options that are better for you than a balance transfer credit card. Here are a few to get you started: