A Tool to Reduce Debt: What is a Balance Transfer?

A balance transfer can help you manage existing credit card debt by moving outstanding credit card balances from one or more "expensive" credit cards (i.e., cards charging higher interest rates) to a "cheaper" credit card (i.e., a balance transfer credit card with a 0% promotional period). Doing so enables you to save money on interest payments and consequently pay down debt faster.

Used carefully, a balance transfer may be useful for those who cannot pay down their current credit card debt right away and are paying high interest charges on their existing card balances. Credit card interest rates can be 19.9%, 29.9%, 39.9% or more, making it very difficult to clear existing debt because a significant amount of your payments goes towards interest charges. Moving these debts to a 0% interest balance transfer card can be a very useful tool for getting your credit card balances paid down quicker.

How Can I Pay Down Debt Faster with a Balance Transfer Card?

Balances transferred to a 0% interest card should clear faster because 100% of your payments go towards reducing your outstanding balance; none of your monthly payments will be lost to interest charges during the 0% interest period on your balance transfer card. On an interest-bearing credit card, on the other hand, a lot of your hard-earned money goes towards interest charges.

How Much Can I Save on a Balance Transfer?

Let’s say you’ve racked up a £2,500 balance on a credit card charging 29.9% interest. You would like to pay this off, and can manage £100 monthly payments towards this effort. On your current interest-charging card, a whopping £60 of your next £100 monthly payment goes to interest charges! Overall, it would take you 44 months to clear your debt and you'd spend £1,483 on interest charges, which is more than half again of your original debt.

Instead, if your balance were sitting on a 0% interest balance transfer card, your whole £100 payment would go directly to reduce your balance. In this way, you'd clear your debt sooner and save money on interest payments along the way.

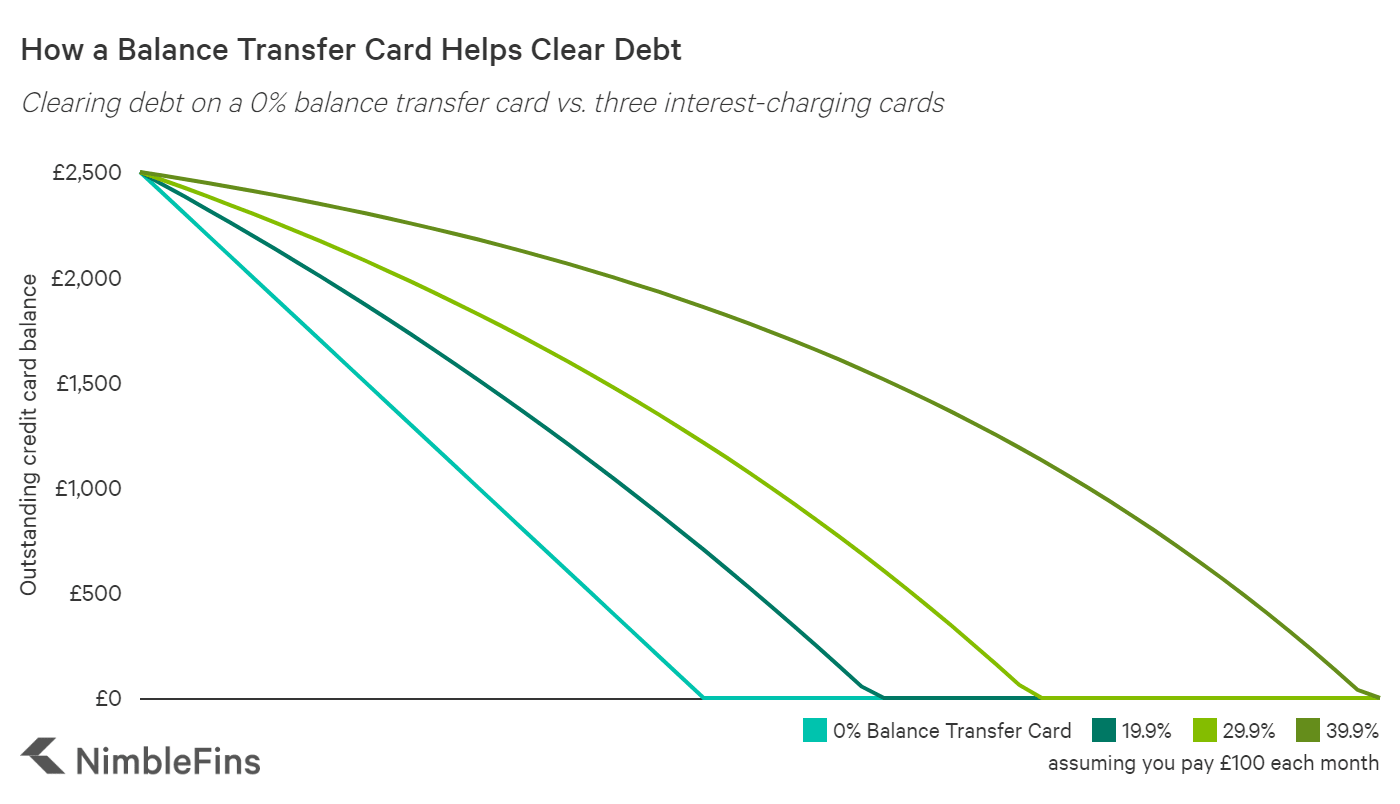

The higher your current interest rate, the more advantageous a balance transfer. The following chart shows how the balance will reduce over time on four cards: 0% (the balance transfer card) vs. 19.5%, 29.9% and 39.9% cards. In all three cases, we assumed £100 monthly payments, so by 25 months you have paid £2,500 to the bank.

What is the status of your debt situation? On the 0% balance transfer card your debt is entirely paid off (yeah!). On the 19.9% card you still have a £790 of outstanding debt. On the 29.9% card you are left with a whopping £1,280 remaining. This is the power of a balance transfer.

Features of a Balance Transfer Offer: Fee, Transfer Window and Promotional Period

Balance transfer offers are characterized by three primary features, which you need to understand in order to choose the best balance transfer offer for you:

- The fee (charged once per balance transfer)

- The transfer window

- The promotional period (i.e., months) of 0% interest

What Is a Balance Transfer Fee?

- Balance transfer fees are charged once per transfer and are calculated as 0% to 5% of the transferred amount.

A balance transfer credit card charges a fee when you move existing debts from another card. This fee is typically around 3% to 3.5% of the transferred amount for longer promotional periods, with a minimum fee that may apply (e.g. £3 or £5 minimum). The shortest balance transfers might not have a balance transfer fee (e.g. a 0% fee). Typically, the balance transfer fee is higher when the 0% period is longer. This fee structure makes sense—a longer 0% period implies you need longer to pay down your debt, which is riskier for the bank. They charge a higher fee as compensation.

The Transfer Window

- The balance transfer window is the time (usually 60 to 90 days) you have to transfer balances to get the 0% promotional rate.

In order to get the 0% rate on balance transfers, you need to transfer balances onto your new balance transfer card within a certain time frame. This is typically 90 days, but some companies (e.g., Virgin Money) have a shorter 60-day window. Balances transferred after the promotional period may incur interest at the standard APR, which can lead to higher costs if not managed carefully. Plus they might be charged a higher balance transfer fee.

What is the Promotional Period?

- The promotional period is the number of months you get a discounted interest rate of 0% interest on balances transferred within the initial transfer window.

Be Aware

A balance transfer can significantly help manage debt if used responsibly; however, it’s crucial to understand the terms and conditions to avoid potential pitfalls. For starters, balance transfer offers only apply to balances transferred within an initial "window" in order to receive the 0% introductory rate and a potentially lower transfer fee. On most credit cards, this window is 60 days or 90 days. Transfer a balance after this window has closed and you'll be on the hook for the stated APR, which can easily be 19% or much more.

Second, if you are late on even a single monthly payment (0% doesn't mean £0 monthly payments!) your intro 0% rate may be revoked and, just like if you miss the intro transfer window, you'll be charged the stated, ongoing interest rate from then on. That puts you back in the same situation you were in before, paying interest charges each month on your balances.

What is a 0% Interest Period on a Balance Transfer?

The 0% rate on balance transfers refers to the 0% promotional interest rate on newly-transferred balances. During this "intro" period you will pay no interest charges. This doesn’t mean you won’t pay anything at all, however—you still make monthly payments, but these monthly payments will go directly towards reducing your outstanding debt, helping you to clear your debts sooner.

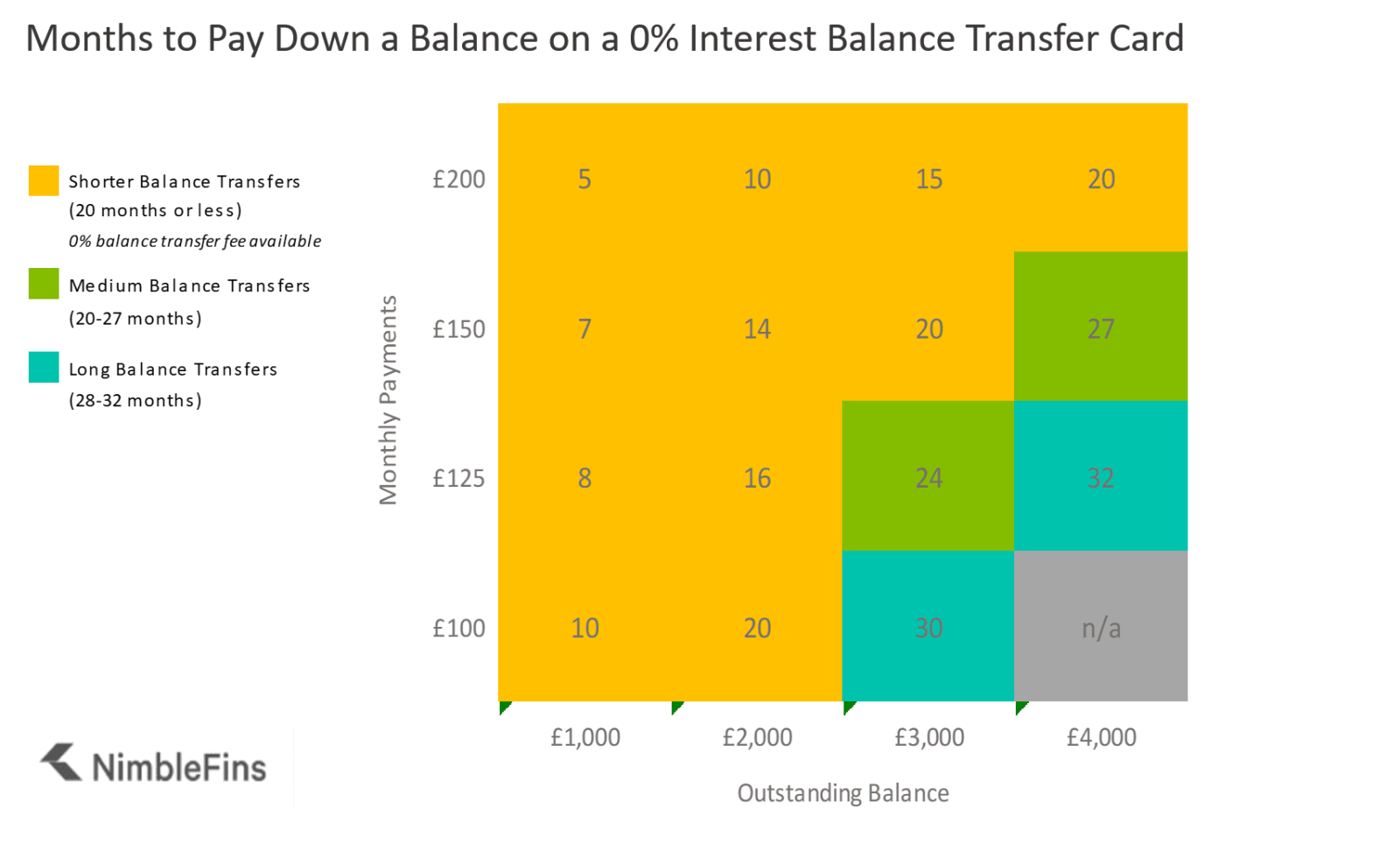

Balance transfer offers as fall into one of three buckets—short, medium, and long—each with defining characteristics. The standout feature of short balance transfers (e.g., 12 to 20 months) is that they typically charge no transfer fee. Long balance transfers offer the longest 0% period, today around 30 months, and charge higher fees up to 3% to 3.5%. Medium balance transfers fall somewhere in between.

What's the Best Balance Transfer Card for Me?

The right balance transfer card for you depends primarily on how long you need to pay down your debt. If you'll need close to 30 months to pay down your debt, you'll need one of the longest balance transfer cards in the UK market—for this you're likely to pay a balance transfer fee of around 3%.

If you only need a year or so to pay down your existing balances, then you can find a balance transfer card that charges a 0% balance transfer fee for the time you require. The chart below can help you decide the time needed to pay down your debt, given your starting balance and the size of the monthly payments you can handle.

Basically, you'll want to find a card that has the shortest 0% promotional period that's suitable for your needs, because then you'll probably pay a lower transfer fee.

How To Transfer a Credit Card Balance

Once you have your new balance transfer credit card, transferring the balance is quite easy. While each bank will have a slightly different process, it generally works as follows:

- 1) Log into your new online account (the bank will instruct you how to set this up)

- 2) Click on the link to transfer a balance

- 3) Enter the amount you want to transfer

- 4) Enter the details of the credit card from which you are moving your balance

- 5) Check and hit submit!