What is Credit Card APR?

The Annual Percentage Rate (APR) is basically the interest rate you pay to a bank to borrow their money. It's common knowledge that a lower APR is better, but we often don't understand exactly how APR is calculated. This guide will take you through the basics and nuances of a credit card APR and how APR can affect you and your finances—particularly important if you're struggling with household debt.

- Overview: APR applies to purchases, balance transfers, money transfers, and cash withdrawals. We’ll explain how these differ, when they apply, and provide you with a rough idea of what typical interest rates are.

- APR and Your Credit Card Bill: APR impacts both your outstanding balances and how your payments are allocated to your bill.

- How to Lower Your APR: We'll explain how to refinance your existing credit card debt with a lower APR or find a lower APR for future purchases.

- APR vs. Interest Rate: We'll show you how your interest charges are calculated based on your APR and provide a few examples.

Credit Card APR Basics

A credit card APR is a representation of the interest rate on your credit card. But how exactly does the APR translate into your interest charges? APR is an annualized figure, but credit card interest isn't charged just once a year—credit card interest charges are calculated daily. We will explain how to convert APR into an effective interest rate (which is what you actually pay) below. If you take a look at the summary box of a credit card, you may see a number of different APRs. These different rates apply to different ways in which you use your card:

Purchase APR. The Standard Purchase APR will be applied to all purchases you make with your credit card (some cards charge a Promotional Purchases rate of 0% during an introductory period). This is the interest rate we tend to think of first when looking at credit cards.

Balance Transfer APR. If you moved or transferred an existing balance from an old card onto a new balance transfer credit card, it will be charged this APR. Good balance transfer cards charge a 0% interest rate on balances transferred during a promotional period. For balances remaining after this promotional period is over, in most cases, the balance transfer APR of a card is the same as the Purchase APR.

Cash Advance APR. If you use your credit card to get cash (e.g., an ATM withdrawal, etc.), you will be charged this interest rate. Cash Advance APRs tend to be higher than purchase/balance transfer APRs. Cash advances can be surprisingly expensive because, on most cards, there is no grace period. In other words, daily interest charges start accumulating immediately from the day you withdraw the money. This means you will have interest charges on cash advances even if you pay your full balance before your next due date.

APR Grace Period

Banks will grant credit card users an interest-free period, commonly known as a “grace period”, a time during which they can pay off their balances without getting charged interest. How long is a grace period? Well, that depends. The grace period is really the time between your purchases and your next due date, so it will vary based on the timing of your purchases within your billing cycle. On many cards this grace period will be a maximum of around 50 days, averaging around 25 days for most purchases. If you can pay off your entire balance during the grace period, you will get to skip paying interest on that balance. For this reason we encourage credit card users to always pay off their balances by each due date.

What Determines Credit Card APR?

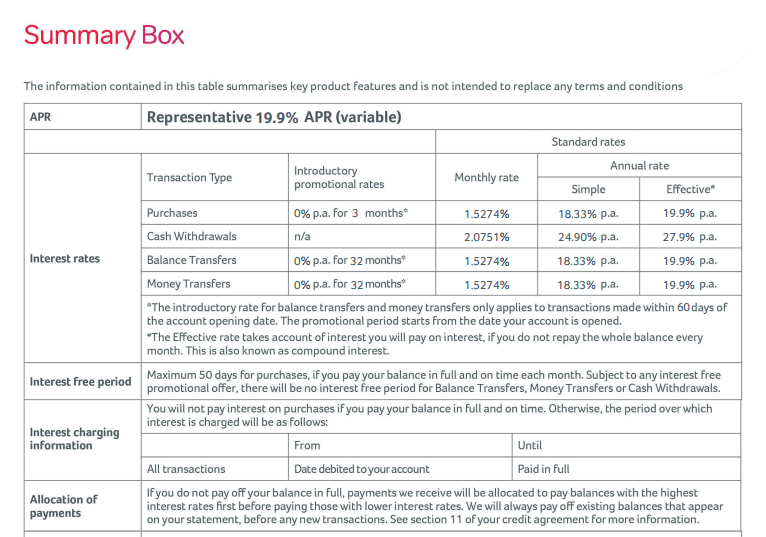

Credit card APR is based entirely on what your bank calls "credit worthiness"—in other words, your credit score. In most Summary Boxes you will see a list of several different APRs—sometimes up to five or six! The different APRs represent the range of interest rates you may be charged, depending on your score. Generally, higher credit scores correspond with lower APRs. If a credit card has a stated representative APR, then at least 51% of accepted applications will get that APR rate. Other customers may get a higher rate based on their individual financial situation. Here you can see a sample Summary Box that illustrates the different APRs. As you can see, this card comes with an APR of 19.9% on purchases, balance transfers, and money transfers, and a higher APR of 27.9% on cash withdrawals.

What is an Average Credit Card APR?

Credit card APRs can vary significantly across different issuers, brands, and credit card types. Some credit cards are designed specifically to have low interest rates, while those aimed at individuals with poor credit tend to have higher APRs. The table below shows average representative APRs by type, according to our database of the most popular cards. As you can see, there is a real cost to those late payments and other debt issues that may result in you being limited to poor credit cards.

As of February 2026, the general market average interest rate has risen to 24.66%, the highest level in over 30 years. Current category averages include:

| Card Type | Average |

|---|---|

| Average Interest Rate | 24.7% |

| Credit Builder (Poor Credit) Cards | 36.2% |

| Airline Rewards Cards | 28.2% |

| Student Credit Cards | 18.9% |

| Cashback/Retail Cards | ~31.4% |

| No Foreign Transaction Fee Cards | ~27.5% |

While these figures show representative APRs, it's important to note that some people (e.g. those with weaker credit scores) will pay even more. For example, the representative APR on the Aqua Classis card is 39.9%—meaning, at least 50% of cardholders will pay 39.9% or less, but the other 49% of cardholders might a higher rate.

How Does APR Affect Your Bill?

APR affects your bill because it determines how much interest will accumulate over time. Additionally, the APR will affect which parts of your balance any payments will go towards. That is, when you pay the bank, will that payment reduce your purchases balance, your balance transfer balance, or your cash withdrawal balance? The bank uses payments to reduce balances in a certain order. The good news is that payments are applied to balances associated with the highest interest rates first, meaning the most expensive "debt" is eliminated first.

For example, imagine you have a £1000 purchases balance and a £200 cash withdrawal balance, which are being charged interest at 20% and 30%, respectively. If you make a £250 payment, that payment is allocated accordingly: £200 to the £200 outstanding cash balance and the remaining £50 to the £1000 purchases balance. Following this payment, you are left with a £950 purchases balance only, accruing at a 20% interest rate.

How Can You Lower Your Credit Card APR?

Finding a way to pay a lower APR can save you hundreds or even thousands in interest payments. Those who are unable to pay off their full balances every month can rack up significant interest charges over time on a high APR card. One way to lower your APR is to consolidate your credit card debt, moving your existing balances over to a 0% intro APR balance transfer credit card. These cards are designed to help you pay back your existing debts sooner. So long as your balance is paid back during the 0% interest period, you're essentially eliminating all interest charges. The market for 0% balance transfer credit cards has tightened significantly; as of 2026, the best balance transfer credit cards offer up to 38 months of 0% APR (offered by TSB), with other major lenders like Barclaycard and Tesco Bank offering up to 36 months. On most balance transfer cards you will pay a fee to transfer any balances (but this could be a 0% fee for a card with a shorter interest-free period); generally speaking, the longer the 0% intro period, the higher this transfer fee.

Executing a balance transfer to a good 0% card will usually leave you better off financially, despite any transfer fees. Those that don't want to open a new card just for balance transfers can try another strategy for lowering their APR. Some credit cards will lower your APR if you show responsible management of your debts, that is by paying the minimum monthly payment on time and staying within the credit limit. It doesn't hurt to call your card company and ask if this is a possibility.

If you're more concerned with the APR on your future purchases, you might look for a 0% purchase card, the longest of which currently lasts 25 months (offered by providers such as M&S Bank, Lloyds, and TSB). This is a reduction from previous years when 30-month offers were more common. These "purchases cards" waive interest during a promotional period, the longest of which currently lasts 30 months. If you're interested in a card to lower the APR on your purchases, take a look through our article on the best 0% purchases cards.

How to Calculate your Credit Card Interest Charges

Understanding the implications of APR on your interest charges isn't intuitive. Knowing your credit card charges 18.9% interest, for example, doesn’t give you an immediate understanding of how much interest you'll pay on your next month’s bill. In this section, we will work through an example of how to determine your credit card interest charges from your APR.

Let's start with the assumption that you have a £2,000 outstanding balance, and your APR is 18.9%. What will your interest charges be on your next statement? Remember that interest is charged daily, so your interest charges are a function of the balance each day. The first step is to calculate your interest charge on one day. But what interest rate do you use for just one day, since APR is an annualized figure? For one day only, we need the Daily Periodic Rate (DPR), which is simply the APR divided by the number of days in a year, or 365. DPR = APR / 365. Therefore, our interest charge on any given day is:

Daily Interest Charge = Daily Balance x (APR / 365)

In our example, the daily interest charge would be £2,000 x (18.9% / 365) = £1.04. If you carried that £2,000 balance for 30 days, you Monthly Interest Charge would simply be the Daily Interest Charge x Days in Billing Cycle, or £1.04 x 30 = £31.20. However, this example is a bit simplistic, since our daily balance changes as we make purchases throughout the month. In order to calculate monthly interest charges, financial institutions will use different methods that employ terms such as "average daily balance" or "adjusted balance" to reflect ever-changing balances. Average daily balance, the most common, is calculated by simply adding up the daily balances over each day in the billing cycle and then dividing that sum by the number of days in the billing cycle. Our formula for the monthly interest charge becomes:

Monthly Interest Charge = Average Daily Balance x (APR / 365) x Days in Billing Cycle

which we can expand, using the definition of Average Daily Balance to be:

Monthly Interest Charge = (Sum of Daily Balances)/Days in Billing Cycle) x (APR / 365) x Days in Billing Cycle

You'll notice that we have Days in Billing Cycle in both the numerator and denominator, which means they cancel out of the formula leaving:

Monthly Interest Charge = Sum of Daily Balances x (APR / 365)

Keep in mind that you may have different APRs across different parts of your bill (e.g., purchases, balance transfers, etc.). The formula may be developed further, taking into account these various APRs.

Total Monthly Interest Charges = ∑ Sum of Daily Balances_n x (APR_n / 365), where n represents each APR and its corresponding balance

In plain English, this means that the bank calculates a separate interest charge for each section of your balance (e.g., purchases, balance transfers, etc.), using the respective balances and APRs. Then they add up each of those individual interest charges to arrive at your total monthly interest charge. Expanding the earlier example, let's say you have an average daily purchases balance for the month of £2,000 and an average daily transfer balance for the month of £1,000, carrying APRs of 18.9% and 20.9%, respectively. Your monthly interest charge would be: (£60,000 x 18.9% / 365) + (£30,000 x 20.9% / 365) = £31.07 + £17.18 = £48.25.