What is a 0% Purchases Card?

A 0% purchases card is a credit card that doesn't charge any interest on your new spending during a promotional period that can last from 1 month up to 25 months or more. As of early 2026, the market has stabilized, with several top providers extending offers back toward the two-year mark.

0% purchases cards can be useful for spreading the cost of purchases over the length of this intro period without incurring interest charges—but you still must make monthly payments on a 0 purchases card! NimbleFins explains how this works and how you can save money below.

Table of Contents

- How a 0% Purchases Card Works

- How Much Can a 0% Purchases Card Save Me?

- Dual Purchase and Balance Transfer Card

How a 0% Purchases Card Works

With a 0% purchases card, you aren't charged interest on new purchases for the duration of the promotional period. Once the promotional period is over, the credit card provider will start charging your standard interest rate on any remaining balances.

What are the Best 0 Purchases Credit Cards?

Promotional periods on 0% purchases cards last anywhere from one month up to 25 or 26 months in 2026. Although the market is constantly changing, promotional periods have extended a bit for 0% purchases cards in the past few years. Lenders like TSB, M&S Bank, and Lloyds Bank currently lead the market with some of the longest offers.

Losing Your 0 Interest Promotional Rate

You can lose your 0% rate and be moved back onto your stated purchases interest rate if you:

- Make a late payment

- Don't pay at least the minimum amount

- Exceed your credit limit

Going over your credit limit or failing to pay the minimum amount on time each month usually means you lose all promotional offers and the credit card will start charging your balances at the stated interest rate.

When applying for a new purchases card, be sure to check not just the promotional period (i.e., months of 0% interest) but also the standard interest rate, as they can be high and quite variable. To give you an idea of the range of interest rates you might find on some UK 0 interest purchase cards, see the selection of ranges below:

| Purchases Rates on 0 Interest Credit Cards | Minimum Purchases Interest Rate (variable) | Maximum Purchases Interest Rate (variable) |

|---|---|---|

| Halifax Purchase and Balance Transfer | 24.9% | 34.9% |

| Marbles | 39.9% | 64.9% |

| Sainsbury's Purchases | 24.9% | 34.9% |

Do You Make Monthly Payments on a 0 Interest Card?

Yes, you still make monthly payments during a 0% interest promotional period. During this period, your minimum payments will usually be around 1% of the balance (plus any default charges or monthly/annual fees)—there may be a minimum £ payment such as £5, or the full balance if that balance is less than £25.

The good news is that none of your payments during the promotional period on a purchases card are lost to interest charges, but instead go directly towards reducing your outstanding balance.

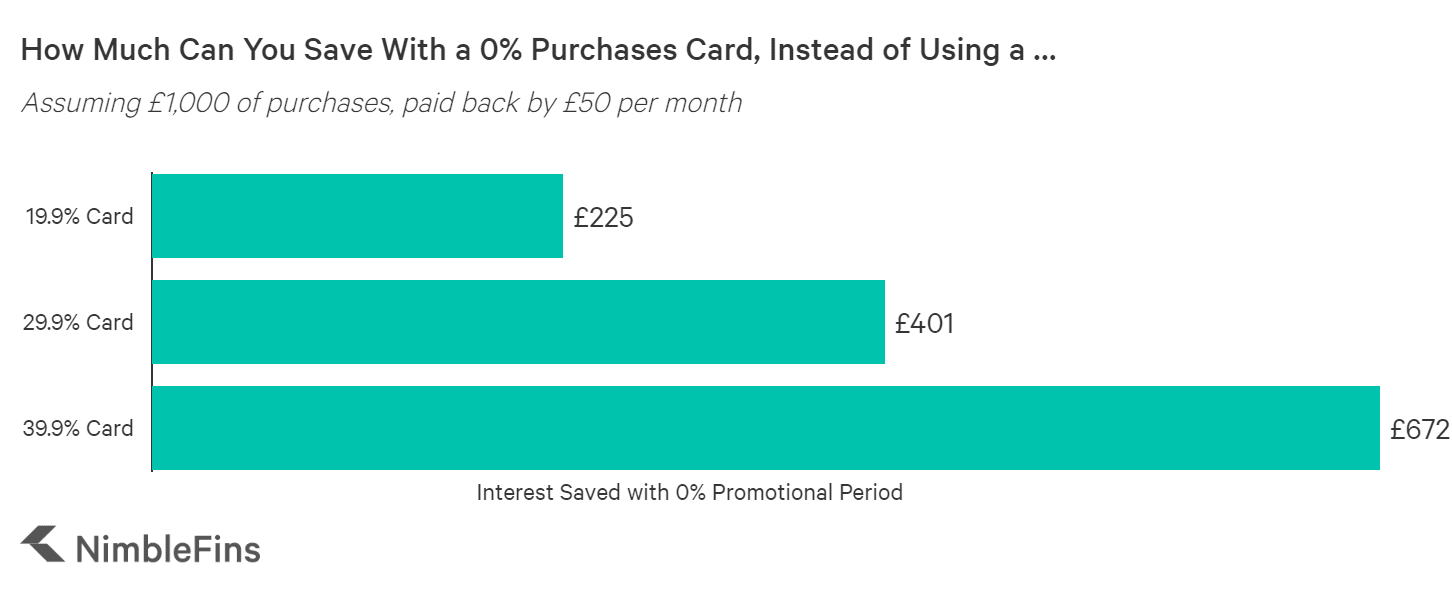

How Much Can a 0% Purchases Card Save Me?

A 0% interest credit card can save cardholders a significant amount of money in avoided interest payments. Let's look at an example. Say you spend £1,000 on charges related to house renovations that you would prefer to pay off slowly over one year—maybe you just don't have extra cash in hand right now, but you can afford £50 payments each month.

Your options are charging this £1,000 in renovation costs to your existing 19.9% credit card (which is close to the average UK credit card interest rate) OR opening a new 0% purchases card.

OPTION 1—24.9% card: Charge £1,000 to a 24.9% card (the current average UK credit card interest rate for 2026), paying back £50 per month (more than the minimum payment)—this will cost you £294 in interest charges and take 26 months to pay down the balance.

OPTION 2—0% purchases card: Charge £1,000 to a 0% card with a promotional period lasting at least 25 months, paying back £50 per month (more than the minimum payment)—this will cost you £0 in interest charges and take 20 months to pay down the balance.

In this example, a 0% purchases card not only saves £294 in interest charges (a whopping 29.4% of the original amount) but you would be debt free 6 months sooner. Make sure you understand how your outstanding balance, the size of your monthly payments, and the length of the promotional period affect the outcome. Ideally, you have paid down your balances by the end of the promotional period.

In the example above, paying £50 per month on a £1,000 balance would leave you debt free in 20 months. Here's the math: £1,000 ÷ £50 per month = 20 months. In this case, look for a 0% purchases card with a promotional period lasting at least 20 months. The savings you can make on a purchases card are even more pronounced the higher the interest rate on your current credit card, as you can see in the chart below.

Purchases Cards with Balance Transfers

Purchase cards sometimes offer balance transfer capability as an added feature for those need help managing existing debt—but cards with both purchases and balance transfers tend to have higher balance transfer fees than you'd find on a card whose primary focus is balance transfers.

Cards with long 0% interest periods for both purchases and balance transfers are often referred to as "dual" or "all around" offers.

If you want one card for everything, it's important to understand how the balance transfer fees are affected. Putting a balance transfer on a long purchases card is more expensive than putting a balance transfer on a short purchases card. Choosing the best card for you will depend on your individual financial situation.