Best Aqua Credit Cards

Aqua specializes in credit cards for people with bad credit. We've analyzed Aqua's two cards and discuss the pros and cons of each, including fees and interest rates, to help you figure out which card may be best for you. Choosing the right card will depend on your individual situation.

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

-

Best Aqua Card for Poor Credit or First Card

Aqua Classic -

Learning

FAQs

Aqua Credit Cards Review

In analyzing Aqua's credit cards, we considered features such as interest rates, rewards, foreign transaction fees and credit limits. The best card for you will depend on your own needs and circumstances. Note: recently Aqua has introduced a pre-eligibility check, so you can see your odds of being accepted before you apply—without hurting your credit record.

Aqua used to offer a wider range of cards including Aqua Advance, which was good for using abroad due to low fees, and Aqua Rewards, which paid cash rewards on spending. But those two cards are no longer being offered. What remains in the Aqua Classic.

Best Basic Aqua Card for Bad Credit or Low Income: Aqua Classic

- Purchase Rate (variable)

- 39.9%

- 0% on Purchases for up to

- n/a

- 0% on Balance Transfers for up to

- n/a

- Initial Balance Transfer Fee

- 3%

- FX Fee

- 2.95%

- Cash Fee

- 3% (min £3)

The Classic Credit Card is apparently Aqua's most popular card and will consider those with poor credit, including the self-employed, individuals who've had trouble with late payments in the past and those with a low income. Initial credit limits run between £250 and £1,500. This increased upper limit allows for slightly more flexibility for those looking to manage their credit utilization ratio while rebuilding their score. Responsible management of your account (i.e., making payments on time and staying within the credit limit) can lead to credit limit increases, which can in turn improve your credit rating—especially once the credit limit reaches £1,000.

- Credit limit may increase with "good behavior"

- No annual fee

- Eligibility Checker

- Free text alerts

- Higher-than-average interest rates from 39.9% variable APR

- Cash APR From 37.45% to 59.94% variable

- 2.95% foreign transaction fees

FAQs

Voluntarily Decreasing an Aqua Credit Card Limit

Sometimes, cardholders prefer to decrease their credit limit—perhaps to avoid accumulating an unmanageable amount of personal debt. In this case, you may request a lower credit limit by calling 0333 220 2691. You may be charged for this call, as it is an 03 number that is charged at a standard national rate. Please check what it will cost from your mobile or land-line provider before calling. Aqua lines are open from 8am-9pm Monday to Friday, 9am-5pm Saturday and 10am-6pm Sunday.

Aqua Credit Card Payments

You can make payments to Aqua via:

- Direct Debit

- Online

- Post

- GIRO

- Standing Order

- Telephone Banking Service

You can find more information on a particular Aqua payment method here.

Aqua Credit Card Payment—How Much Should You Pay?

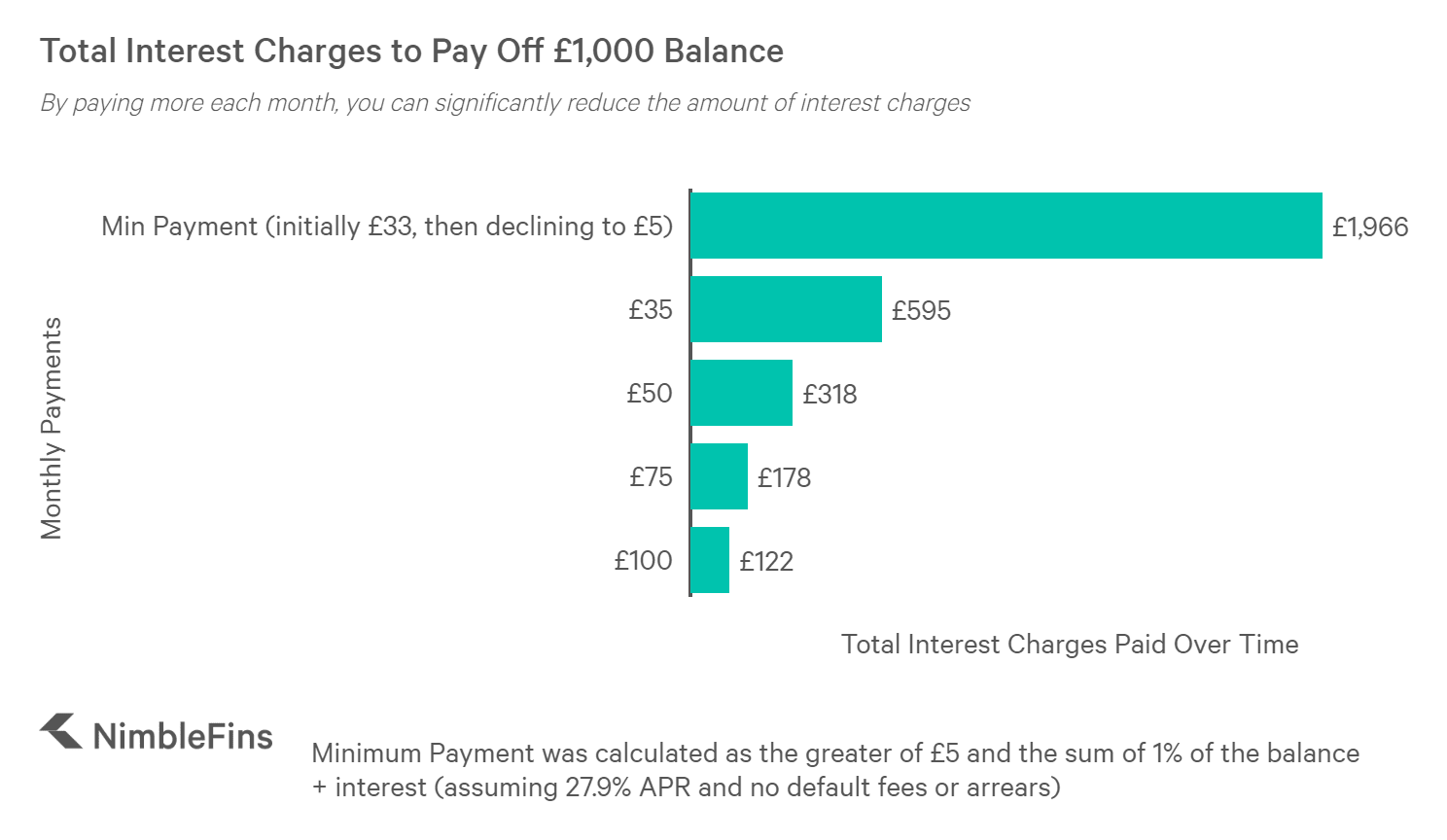

While you are probably aware that making at least the minimum monthly payment is important for a good credit rating and to avoid fees and charges, it's also important to understand why you may want to pay more than the minimum amount due each month.

Basically, by paying only the minimum amount you will extend the time to become debt free and also pay more in interest charges. By paying a larger amount each month, you can become debt free sooner and also reduce to total interest paid over the life of the debt. Paying as much of your outstanding balance as you can afford each month is generally a good strategy.

Top Tip: Pay as much as you can each month.

The chart below shows how making larger monthly payments equates to lower total interest charges over the life of a debt. Notice how only paying the minimum amount due each month results in interest charges about 6X times larger than maintaining a constant £50 payment.

Be aware that, as a credit-builder company, Aqua's interest rates are higher than average, as you can see in the following chart. Try to pay down your full balance each month to avoid interest charges.

Summary of Best Aqua Cards

| Best For... | Card | Purchase APR (variable) | Quick Overview |

|---|---|---|---|

| Travel | Aqua Advance | 34.9% | No longer available |

| Bad Credit | Aqua Classic | 35.9% |

|

Comparing Aqua Credit Cards to Other Similar Cards

Since brands like Chrome and Aquis have been consolidated and are no longer accepting new applications, readers should consider active alternatives. For rebuilding credit, the Vanquis Classic Credit Card is a primary competitor with a Representative 42.9% APR. Alternatively, the Capital One Classic offers a slightly lower Representative 34.9% APR. Both remain viable options for those who may not qualify for the Aqua Classic.