Aqua Advance Credit Card Review: A Credit-Builder Card with No Foreign Transaction Fees?

Aqua Advance Credit Card Review: A Credit-Builder Card with No Foreign Transaction Fees?

Good for

- Using abroad

- Rebuilding one's credit rating

- The chance to lower your interest rate

Bad for

- Those wanting to pay a low interest rate

- Individuals needing to carry a balance from month to month

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Note: The Aqua Advance is no longer available to new applicants. We are keeping this review up for historical purposes.

The Aqua Advance is a credit builder card with two stand-out features: no FX fees on transactions made overseas and the opportunity to potentially lower your interest rate from 34.9% to 19.9% (variable). Is this a good card for you? Read our review to see how it compares to other options.

Aqua Advance Credit Card Review

The Aqua Advance Credit Card is a solid credit builder card for those trying to improve their credit rating through good behaviour, and who need a card to use abroad. One solid feature is that your interest rate might go down each year for three years. (They used to say it could drop by up to 5% a year for three years, potentially getting to as low as 19.9%, but they have removed this language from their website.) Having your interest rate drop on credit card is very helpful for your credit score. How do you make that happen?

- Stay within your credit limit

- Pay at least the minimum payment on time

As with all credit cards (and credit-builder cards in particular because the have higher interest rates), try to pay off as much of the balance as you can each month—ideally the whole amount outstanding—to avoid falling deeper into debt.

Can you use the Advance on Holiday?

As a travel card, there are no fees on purchases made abroad. So it's fine to use this card for paying in hotels, restaurants, bars and shops when you're on holiday.

But cash withdrawals abroad are expensive as they are subject to higher-than-average interest and this interest starts to accumulate immediately—there's no grace period like you get on purchases. Plus the card charges a 5% cash withdrawal fee (minimum £4) at home and abroad (this has recently risen from 3%/£3 minimum).

Bottom Line: The Aqua Advance is a great option for those with weaker credit histories who want the chance to improve their credit rating and need a card to use when travelling abroad that doesn't charge FX fees.

Aqua Advance Benefits & Features

| Aqua Advance Card Features | |

|---|---|

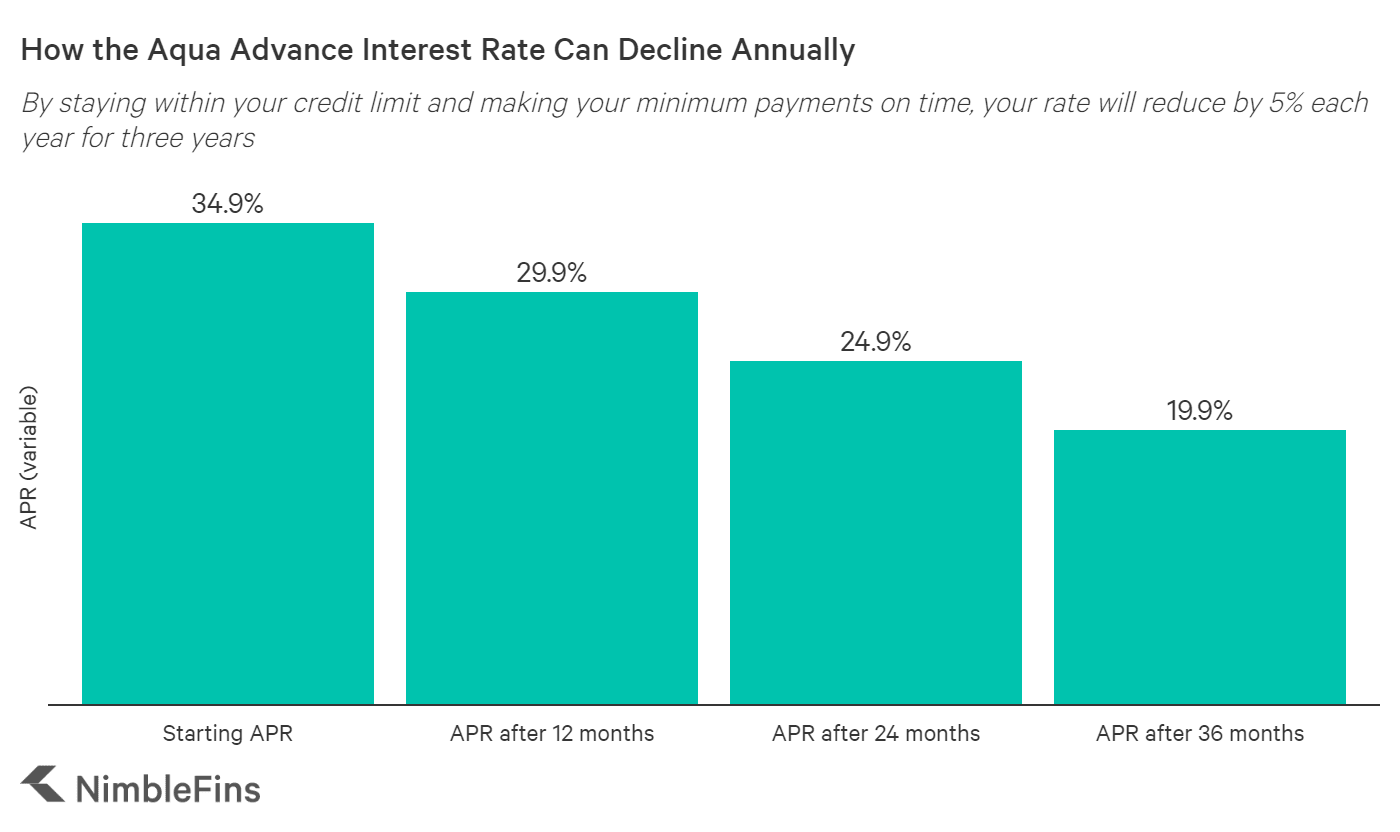

| Decreasing Interest Rate | By staying within your credit limit and making your minimum payment on time, your interest rate should reduce by 5% each year for three years. Those starting with an APR of 34.9% can reduce the rate by 5% every 12 months until the rate is down to 19.9% APR. |

| Transaction Fees | No non-sterling transaction fees on purchases or cash withdrawals made abroad (but foreign ATM withdrawals will still incur a Cash Withdrawal Fee, which is charged regardless of currency) |

| Cash Withdrawal Fee | 5% fee at home and abroad (£4 minimum) |

| Initial Credit Limit as low as | £250 to £1,200 |

| Text Reminders to help you |

|

| Annual Fee | £0 |

| APR |

|

Using the Aqua Advance Abroad: The Aqua Advance can work as a travel card also, as it doesn’t charge a fee for purchases made abroad. However, between the 5% cash withdrawal fee and the interest rate on cash of 44.9% APR, this card can cost more than average for ATM withdrawals, whether at home or abroad.

Who may be Eligible for an Aqua Card? As credit builder cards, Aqua cards are targeted at those with weaker credit histories. Below we've organized some detail regarding who Aqua will consider, and who they won’t, from their website. Falling into one category or another is by no means a guarantee of whether or not you’ll be accepted, just an indication of your odds. As part of the application process you can use their eligibility checker to give you further guidance. If you've had a CCJ in the past 12 months, Aqua will probably reject you. Aqua will consider you if you've/you're:

- a homemaker, student, on a low income or work part-time

- been refused credit in the past

- never had a credit card

- recently moved to the UK

- recently moved house and not on the electoral roll

- rebuilding credit rating

Aqua Advance Interest Rates: As a credit builder card, interest rates are higher than average, starting at 34.9% APR for purchases. But rates can be 44.9%, 49.9%, 54.9% or even 59.9% (largely depending on your credit history)! However, cardholders can improve their situation through "good behaviour". By staying within your credit limit and paying at least your monthly minimum on time, it is possible for the interest rate to drop—they previously advertised a drop of 5% a year, but now they don't specify the amount. Where possible, set up a direct debit to pay off your card on time every month. The chart below assumes a 5% decrease in interest rate per year.

FAQs

The starting Aqua Advance credit card limit is between £250 and £1,200, depending on your credit history.

The Aqua Advance is a credit-builder card that has two interesting features: a structured plan to lower your interest rate (possibly by 5% each year) and no FX fees on non-sterling transaction.

Cardholders can use their Aqua credit card to withdraw cash from an ATM, but it's expensive to do so. For starters, the interest rate on cash withdrawals is around 10 percentage points higher than the purchase rate (check your terms to find your cash rate) AND there is no interest free period on cash transactions which means interest charges on ATM withdrawals start building up immediately. On top of that, each cash withdrawal is charged 5% of the transaction (minimum £4).

How does the Aqua Advance Credit Card Compare to Other Credit Cards?

In order to decide if the Aqua Advance credit card is for you, it’s best to compare it against the closest competitors.

Aqua Advance Card vs Halifax Clarity Credit Card

The Halifax Clarity Credit Card is a very good card for travel use. Not only does it charge no fees on cash withdrawals and purchases made abroad in the local currency, but it also imposes a lower interest rate on cash withdrawals. This can be important because interest is charged immediately from the date of a cash withdrawal.

Quick Takeaway: Those with better credit ratings will probably be better off with the Halifax Clarity card, as it won't charge a fee on your ATM withdrawals and sports lower interest rates.

Aqua Advance Card vs Santander World Elite Mastercard

The Santander World Elite Mastercard is a decent travel card in that it doesn't charge a fee for non-sterling transactions made abroad (cash withdrawals are still charged 3%, minimum £3 per transaction). However, there's a £15 per month account fee, which seems high if all you're looking for is no-fee foreign transactions. The card does also offer access to over 1000 airport lounges and over 1 million Wi-Fi hotspots worldwide, plus a 24/7 concierge service and cashback on everyday spend.

Quick Takeaway: The Santander World Elite Mastercard might be good for spending abroad and access to airport lounges and hotspots when travelling, but it doesn't come cheap with a £15 per month account fee (translating into a variable APR of 49.8% APR).