Top Cheap Home Insurance Companies UK

Compare quotes from up to 50 home insurance providers. Powered by QuoteZone.

- Save up to £241*

- Buy online or by phone

- 4.8 out of 5 stars on Reviews.co.uk**

Get Quotes

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

No single insurance provider is the cheapest or best for everyone, but some home insurance companies stand out for the best combination of good customer reviews, features and cheap quotes. We've assembled a list of reputable, cheaper home insurance providers by analysing data from over 50 UK brands. Read about some that stood out to us, and why.

- Compare house insurance quotes

- Home Insurance: What to Look For and Who Each Provider Might Suit

- Average home insurance cost

- Questions about buying home insurance

Compare House Insurance Quotes

Compare cheap home insurance quotes quickly and easily from over 50 trusted providers, many of which have a range of deals. Can we be your cheapest quote? Save up to £241*. For you. For better finances.

Compare quotes from up to 50 home insurance providers. Powered by QuoteZone.

- Save up to £241*

- Buy online or by phone

- 4.8 out of 5 stars on Reviews.co.uk**

Get Quotes

Home Insurance: What to Look For and Who Each Provider Might Suit

There are dozens of reputable home insurance providers in the UK, and the right one depends on your property, your priorities and how much of your cover you want built in versus added as optional extras. The providers below have been selected based on features, independent ratings and customer feedback. No provider is right for everyone—use these summaries to narrow your shortlist, then compare quotes before buying.

One note on ownership: in July 2025 Aviva completed its acquisition of Direct Line Group, making Direct Line, Churchill and Green Flag part of the Aviva family. Both brands continue to trade independently, but they are now ultimately owned and underwritten by the same group.

Consider LV= If: You Want Strong All-Round Cover With High Customer Satisfaction

LV= consistently scores well across both independent product ratings and customer reviews. It holds a 4.7 out of 5 rating on Feefo from verified customers (correct as of January 2026), and its policies carry Defaqto 5-star ratings. Three tiers are available: Essentials, Home and Home Plus. The key differentiator between tiers is what's included as standard versus as an add-on. Extended accidental damage, personal belongings away from home and bicycle cover are all included on Home Plus, or can be added to the lower tiers individually. If you work from home, business equipment cover is included as standard across all tiers (up to £5,000 on Essentials, £15,000 on Home, and up to your contents limit on Home Plus). Buildings rebuild cover goes up to £500,000 on Essentials, £1 million on Home, and unlimited on Home Plus. LV= renews at a price equal to or cheaper than an equivalent new customer quote, which is worth knowing.

LV= may suit you if:

- You want a well-rated all-rounder with strong independent customer satisfaction scores

- You work from home and want business equipment covered as standard

- You want flexible tiers so you only pay for the extras you need

- You want unlimited rebuild cover (available on Home Plus)

It may be less suitable if:

- You own a listed building (LV= does not cover listed or preservation order properties)

- You want the very highest customer satisfaction scores—see NFU Mutual below

Also worth considering: NFU Mutual NFU Mutual was named Which? Recommended Provider for 2025 and achieved the highest customer satisfaction score (81%) in Which?'s survey of 35 home insurance providers. Its policies hold a Defaqto 5-Star Rating and it charges no interest for monthly payments—a rarity. The trade-off is that NFU Mutual is not available on comparison sites; you have to contact them directly or through a local agency. For buyers willing to go direct, it's the standout option on claims and service quality.

Consider Aviva If: You Want a Large Insurer With Flexible Policies and Online Claims

Aviva is the UK's largest insurance group and its Signature home insurance policy is Defaqto 5-star rated. In the most recent Which? analysis (September 2025), the Signature policy qualified as a Which? Best Buy for buildings cover, scoring 74%, and came third in the country for contents cover at 79%. Aviva's customer score from the same survey was 72%. Three policies are available: Online (comparison sites), Premium (comparison sites) and Signature (direct only). Limited accidental damage is included as standard; full accidental damage can be added. No interest is charged on monthly payments for Online and Signature policies. Claims can be made online, 24/7. Aviva also now owns Direct Line and Churchill (since July 2025), making it the UK's largest home insurer by market presence.

Aviva may suit you if:

- You want a large, financially secure insurer with a wide range of policy options

- You want no interest charged on monthly payments (Online and Signature policies)

- You want a Which? Best Buy buildings policy

- You value 24/7 online claims management

It may be less suitable if:

- You want full accidental damage included without paying extra (only limited cover is included as standard)

- You want the strongest possible claims satisfaction scores

Also worth considering: Halifax Halifax was named Defaqto Home Insurer of the Year 2025. Its Silver policy is in the upper half of Which?'s policy scoring table and notably includes full accidental damage cover as standard—something only around a quarter of policies do. No interest is charged for paying monthly. Customer satisfaction scores are lower than Aviva's, but the product breadth and accidental damage inclusion make it worth a quote if that feature matters to you.

Consider Direct Line If: You Want Higher-Tier Cover With More Included as Standard

Direct Line has been selling home insurance since 1985 and remains one of the UK's most-used providers, now operating as part of the Aviva Group since July 2025. It is not available on comparison sites. Three tiers of cover are offered: Home Insurance (standard), Home Insurance Plus and SELECT Premier. The top two tiers include personal possessions, accidental damage, home emergency and family legal protection as standard—features that typically require separate add-on payments elsewhere. This makes it easier to get comprehensive, all-in cover without having to build it yourself.

Churchill, also now part of the Aviva Group, offers similar tiered cover through comparison sites. Its Home Plus policy includes accidental damage, personal possessions, home emergency and family legal protection as standard. If you prefer to buy via a comparison site rather than direct, Churchill is the sister-brand route to functionally similar cover.

Direct Line may suit you if:

- You want comprehensive cover with key features built in rather than priced as extras

- You don't mind buying direct rather than through a comparison site

- You want a long-established, widely-recognised provider

It may be less suitable if:

- You want to compare prices quickly across multiple providers on a comparison site (Direct Line is not available there—try Churchill as a comparison-site equivalent)

Consider John Lewis If: You Want Premium Features Including Cyber Cover

John Lewis home insurance has improved significantly following a change of underwriter from RSA to Great Lakes Insurance, bringing higher coverage limits, no charge for paying monthly and some features not commonly found in standard policies, including cyber cover. The ability to mix and match tiers independently across buildings and contents is also distinctive—you can take a higher buildings tier while keeping contents at a lower level, rather than being forced into a single combined tier. John Lewis scored the highest Fairer Finance customer experience rating in our top providers list.

John Lewis may suit you if:

- You want cyber cover included as part of your home insurance

- You want the flexibility to choose different tiers for buildings and contents independently

- You want no monthly surcharge for paying in instalments

- You value high customer experience ratings

It may be less suitable if:

- You want the widest possible comparison across many insurers (John Lewis is available on some comparison sites but not all)

Consider Tesco If: You Want a Straightforward Which?-Recommended Policy

Tesco Bank was named a Which? Recommended Provider for home insurance in 2025, one of only two providers to receive this status (alongside NFU Mutual). Tesco underwrites its own home insurance through Tesco Underwriting Ltd (with separate underwriters for home emergency and family legal cover). Three clear tiers are available. The Which? recommendation reflects both policy quality and customer satisfaction scores, making it one of the more reliably validated options in the mainstream market.

Tesco may suit you if:

- You want a Which?-endorsed policy with independently verified customer satisfaction

- You want a simple, clearly structured set of tiers without lots of configuration

- You already bank or shop with Tesco and prefer to consolidate providers

It may be less suitable if:

- You have a non-standard property or complex insurance needs (a specialist provider may be better suited)

Consider Swinton If: You Want a Broker With Multiple Underwriters and Strong Reviews

Swinton is a UK insurance broker (not an underwriter) that has operated since 1957 and searches a panel of leading insurers including AXA, Covea and Highway. This means the underlying underwriter and policy terms can vary. Swinton holds a 4.4 out of 5 Trustpilot rating, with 70% of reviewers scoring it 5 stars, and its Premier policy is Defaqto 5-star rated. As a broker, Swinton can be found on comparison sites and may suit buyers who want to access multiple underwriters through a single trusted intermediary.

Swinton may suit you if:

- You want to access quotes from multiple underwriters through one broker

- You value strong Trustpilot ratings and a long-established name

- You want a Premier-level policy with Defaqto 5-star cover

It may be less suitable if:

- You want a consistent, directly underwritten policy where the insurer you buy from is the insurer you deal with at claim time

- You want to verify exactly who your underwriter is before buying

Consider esure If: You Want Solid Features at a Competitive Price

esure reliably offers a good range of features for the price and is one of the larger UK home insurance brands. Coverage features are generally strong relative to the price point. Customer satisfaction scores are lower than some competitors listed here, so esure is better suited to buyers who are primarily comparing on value and features rather than prioritising claims experience above all else.

esure may suit you if:

- You want a solid set of features without paying a premium price

- You're comfortable comparing on features and price via comparison sites

It may be less suitable if:

- Claims experience and customer service are your primary decision criteria

Consider HomeProtect If: Your Property Is Non-Standard

For properties that mainstream insurers struggle with—including non-standard construction (flat roofs, timber frames, listed buildings, thatched roofs), properties that are sometimes unoccupied, or homes where someone runs a business from the premises—a specialist provider is usually a better starting point than a standard comparison site search.

HomeProtect is one of the better-known UK specialists in this space. Policies are underwritten by AXA and Legal and General, the buildings cover is Defaqto 5-star rated, legal expenses cover and home emergency cover are included as standard, and alternative accommodation cover goes up to £30,000. 74% of new HomeProtect customers reported saving money when they switched (survey of 1,281 buyers, November–December 2025).

Also worth considering for specialist needs: Intelligent Insurance, which specialises in non-standard and complex properties including listed buildings, thatched properties and those with a history of subsidence or flooding. Its policies are Defaqto 5-star rated and it operates on a personalised, phone-based quoting model rather than through comparison sites.

How To Pick a Good Buildings & Contents Insurance Plan

Homeowners insurance is meant to protect what is probably your largest asset, so carefully consider what your insurance policy covers—and what it doesn't cover. While you may be tempted to choose a policy with a higher excess or with fewer features to save money on your premium, remember that paying more for a plan with extended coverage may save you money in the end.

If you’re concerned that you’re paying too much for home insurance, you should check prices through a comparison site like our partner QuoteZone to get an idea of what other insurance companies would charge in your area. Many insurance companies have similar limits across basic or premium plans, so switching insurance companies won’t necessarily cause you to lose coverage.

In general, be sure that the limits are high enough to cover the full value of your contents and the rebuild cost on your house (you can use BCIS's rebuild cost calculator) to help you figure out the cost to rebuild your home, say in the case of fire). Premium plans cost more, but they often include extra coverages without you needing to pay an additional premiums. Some features that you may want to look out for include:

Public liability: Covers you for the costs of being sued due to an incident at your home.

Alternative accommodation: Covers the cost of staying elsewhere (e.g., hotel, rented house, etc.) while your house is being repaired if it's rendered uninhabitable following a major incident (e.g., fire, flood, etc.).

Empty property: Cover is limited or removed if you leave your home unoccupied for too long (e.g., for a long holiday or work assignment); always check the number of days you can leave your property empty before it is considered "empty."

Home Emergency: An emergency number you can call to fix emergency damage, such as a burst pipe or unsecured door.

Accidental damage cover: Cover for accidents that damage your contents at home and/or your house (e.g., stepping through a loft floor or spilling wine on the carpet).

Legal expenses cover: Cover for personal legal expenses related to issues such as employment disputes, bodily injury claims, etc.

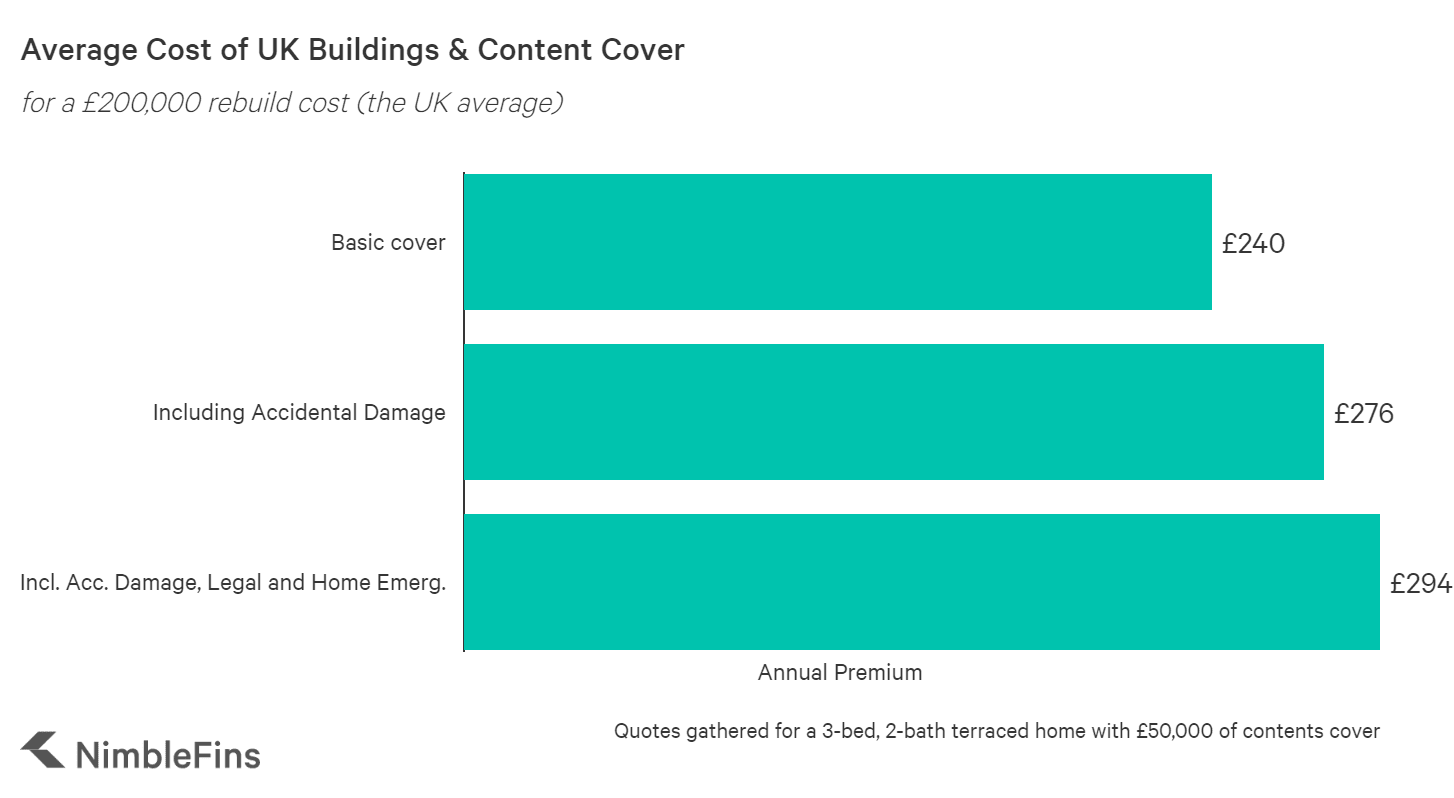

Average Cost of Home Insurance

Most people pay around £300 for combined buildings and contents home insurance, but the annual cost of buildings & contents insurance for a 3-bed, 2-bath semi-detached house ranges from £123 up to £900 or more, so it's critical to comparison shop for a home policy before you buy.

Policies towards the top of the range typically offered higher coverage levels—for instance, higher valuables cover and unlimited buildings cover as well as the inclusion of accidental damage, away-from-home cover, home emergency cover and legal cover (features which sometimes cost extra).

Another factor that might determine your cost of home buildings insurance is the rebuild cost of your home—the average cost to rebuild a house is around £200,000 for a 1,400 square foot 3-bed home, but your rebuild cost will depend on many factors such as the size of your home and where you live.

Questions About Buying Home Insurance

Methodology

In order to come up with a list of top picks for best cheap home insurance in the UK market, we first scoured quotes from a number of comparison sites and direct insurers to find companies that offered good value for money for our sample profile. Then we ranked brands on their TrustPilot customer ratings, Fairer Finance scores and our view of their products to find which of the cheap home insurance brands are best in terms of features and customer service. The companies in the top ten all had a minimum TrustScore of 3.8, a minimum Fairer Finance score of 59% and at least one top-notch product in terms of features.

Cheap Home Insurance in Your Area

Comparison panel includes up to 50 UK home insurance providers. Powered by QuoteZone.

List of home insurance companies analysed in this study

- AA

- Admiral

- Adrian Flux

- Apricot

- Arkwright

- Aviva

- Axa

- BeWiser

- Bradford & Bingley

- British Gas

- Carole Nash

- Churchill

- computerquote

- Co-op

- dialdirect

- Direct Line

- Easy Insure

- Ecclesiastical

- esure

- Fluxdirect

- fresh home

- Frontier

- getcover.co.uk

- GoSkippy

- Halifax

- Hastings Direct

- Home Protect

- Home Quote Direct

- Homenet

- iGO4

- intelligent insurance

- John Lewis

- Legal & General

- LV

- M&S Bank

- Magnet

- More Than

- NOVA Insurance

- One Call Insurance

- One Insurance Solution

- Policy Expert

- Post Office

- Privilege

- Quote 2 Insure

- quotelinedirect

- Quotemehappy

- Quoteyourhome

- RAC

- RCIB

- Rias

- Sainsbury's Bank

- Sheilas' Wheels

- SunLife

- Swiftcover

- Swinton

- Tesco Bank

*For information on the latest saving figures, pay-less-than figures, and pay-from figures used for promotional purposes, please click here.