M&S Home Insurance Review

M&S Home Insurance Review

Good for

- Paying monthly

- Covering plants in the garden

- Replacement locks if keys lost

- Pairs and sets

- Help with boiler replacement

- Robust features

- No cancellation charges

Bad for

- Those wanting a cheap premium

- Underfloor heating not covered

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Important update: M&S Bank has withdrawn M&S Home Insurance from sale. If you have an existing M&S Home Insurance policy, your cover is unaffected and will remain in place until your policy end date. This review is being left up for historical purposes.

Cheap Home Insurance in Your Area

Comparison panel includes over 3 dozen UK insurance brands. Powered by QuoteZone.

In This Review

M&S Home Insurance Review: What You Need to Know

M&S Home Insurance can be a good option for those who value quality over price. Marks and Spencer plans may not for those looking for the cheapest home insurance deal but they do offer really good coverage. They may not be the cheapest, but policyholders can benefit from a host of perks not offered on some competing home insurance plans. For example:

- Contents cover will replace plants in the garden and pairs/sets

- M&S will pay to have your locks replaced in the event of lost keys

- Optional HomeServe cover will contribute £500 to boiler replacement in the event it fails and is too costly to repair

Replacement is done on a like for like basis. Premier cover is "unlimited" for contents cover, which means they'll pay the full cost of repairing or replacing the contents to the same specification with no upper limit.

Docs used to specify that you had up to 90 days away before your home was considered "unoccupied"—but now the policy wording simply refers to "the agreed number of days", so this may vary from policy to policy.

M&S Home Insurance Policies

M&S offers two levels of home insurance to choose from: Premier and Standard.

- Premier: unlimited cover for buildings and contents; includes Accidental Damage

- Standard: up to £1,000,000 for buildings and up to £100,000 for contents

What are the main differences between Standard and Premier plans?

- Limits: Higher coverage limits on Premier plans

- All Risks: Premier plans are protected on an "all risks" basis which means all loss and damage is covered unless it was explicitly excluded in the Policy Booklet. Standard plans are not "all Risks" so you are only protected against specific events listed in the Policy Booklet.

- Storm Damage: Storm damage to fences and gates is covered on Premier plans, but is excluded on Standard plans.

- Accidental Damage: Premier plans automatically include cover against events like spilled wine on the carpet to a broken shower screen to putting a foot through the floor. Standard cover provides partial Accidental Damage cover to specific items (e.g., fixed glass and sanitary fittings in the home)—but full Accidental Damage is available as an optional cover for an extra premium.

No Claims Discount No Claims Discount (NCD) protection is an option available on both plans for an added cost. You're eligible for NCD protection if you have 5 years no claims discount as calculated by M&S and you've been claim free for at least the last 3 years. With the NCD protection you can claim up to twice in five years without losing your no claims discount or affecting your premiums. You must also have an excess of at least £100 to be eligible for a NCD.

Moving House? For those moving house within the British Isles through professional movers, M&S contents cover will protect against financial loss due to accidental damage or theft during the move, including whilst in temporary storage for up to 7 days. However, personal money, jewellery, watches, items of gold or platinum, stamps and coins are not covered during household removals, so you'd be advised to watch out for those yourself.

Monthly Payments: Those who want to pay monthly can do so without financial penalty due to the 0% APR representative interest rate on monthly payments.

Optional Extras

A number of coverages are available for an extra premium so you can customise your home insurance to your needs. For more details on exclusions see below.

Personal Possessions Away From Home: You can buy OPTIONAL Away From Home cover on both Standard (up to £25,000) and Premier plans (up to £50,000) to protect against loss of or damage to items like wallets and watches when they are temporarily away from your home.

Home Emergency: Those opting for M&S's HomeServe home emergency cover get up to £1,000 per call out, which is higher than the typical £500 limit. If a part needs to be ordered to re-establish heating in the home and the part will take over 72 hours to arrive from the engineer’s first visit, M&S will deliver two electrical heaters to the property (which are yours to keep). If the main heating system is declared "beyond economical repair," M&S will contribute £500 towards a new boiler or electric heater.

Legal Expenses: Up to £50,000 of legal funding for issues such as employment disputes, medical negligence claims and consumer issues.

Accidental Damage: Accidental damage cover is included on Premier plans and can be added for an additional cost to Standard plans.

M&S Home Insurance Customer Reviews, Complaints and Ratings

Marks and Spencer doesn't have a lot of online customer reviews for us to find out what people really think once they're signed up. So instead we looked at customer reviews for their underwriter, Aviva, because ultimately that's who you'll deal with if you need to claim.

While a few years ago that stats for Aviva weren't great, they've improved since then. In fact, they have now achieved 4.1 stars out of 5 by customers on Trustpilot. However, that rating reflects many products other than M&S home insurance (e.g., Aviva car and home insurance, savings, investments, pensions, etc.). So, we read through hundreds of reviews to see if customers mentioned home insurance or even M&S specifically. Here are some positive and negative home insurance customer comments that we found:

"Easy online application after clicking through from a comparison site. Great price and good reviews."

"We dealt with M&S home insurance (Aviva underwrite their policies) for a contents claim resulting from a pipe leak... They dealt with our claim politely, promptly and fairly, and it was resolved within weeks of the event."

"Home insurance 20% increase. Aviva says we know you didn't claim. Sorry we can't be more competitive."

"Last year I thought I had roofing problem after high winds and heavy rain. I tried to open a claim with AVIVA but was unable to get through on the phone for several days... I could only get through to the emergency call out; this took over a week for some one to turn."

Additionally, M&S home insurance products have earned top marks for product features.

M&S Home Insurance Quote Comparison

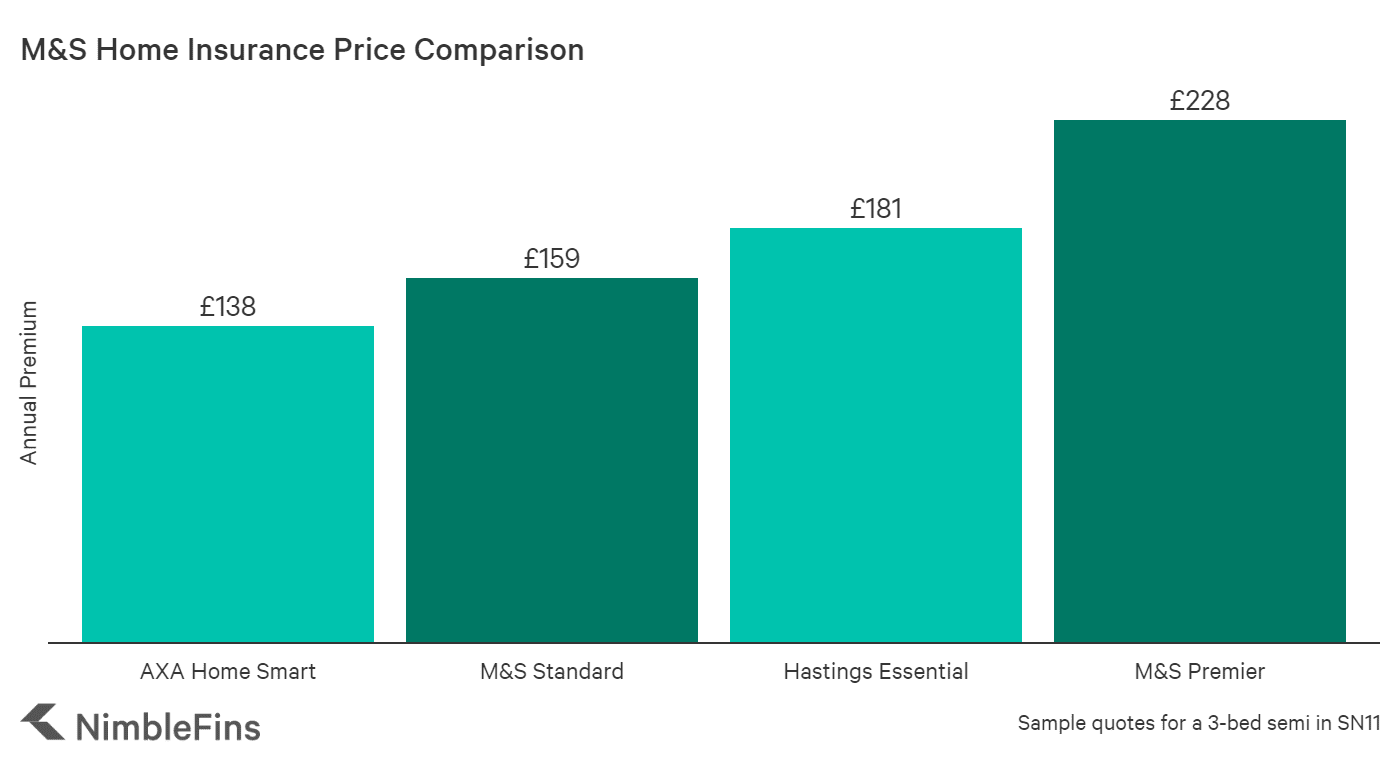

We found that Marks and Spencer Standard home insurance plans are usually competitively priced, but they won't be the cheapest on the market.

To see how M&S home insurance quotes compare to a few other popular options in the market, we quoted buildings & contents cover for a 35-year-old policyholder living in a mortgaged, 2-bedroom property in SN11 who had made no claims in the past few years. Insurance quotes can vary significantly from day to day and according to your individual details, so your quotes may reflect a large degree of variation.

Remember that the excess can affect your quote. M&S gives the option to choose a voluntary excess from £0 up to £1,000, which you pay on top of the compulsory £100 excess. A policy with a higher excess will have a lower premium, because you're committing to pay more towards any valid claims. While a lower premium is certainly enticing, be sure you're comfortable paying the excess in the event of a claim.

Cheap Home Insurance in Your Area

Comparison panel includes over 3 dozen UK insurance brands. Only one form to fill out.

M&S Home Insurance Add-On Costs

We also gathered quotes for add-on extras to see how much these might cost you. Prices might vary depending on factors like where you live—especially for accidental damage—but this can give you a rough idea of what you might be quoted from M&S for these extra coverages.

| Estimated Costs of M&S Home Insurance Extras | Standard Plans | Premier Plans |

|---|---|---|

| Accidental Damage - Contents | £20 | already included |

| Accidental Damage - Buildings | £20 | already included |

| Legal | £27.15 | £27.15 |

| Home Emergency Cover | £39.89 | £39.89 |

| Personal Belongings Away From Home (£1k) | £22 | £22 |

M&S Home Cover: Features

M&S home insurance can be extended through the addition of cover for: Away From Home/Personal Possessions, Accidental Damage (already included in Premier plans), Home Emergency, Pedal Cycle (i.e., Away From Home cover—bikes are already covered at home through Contents cover), and Family Legal. Limits for each section can be found below in the Policies section. For more complete details like full exclusions, please see the policy documents.

| M&S Home Insurance Features | Notes |

|---|---|

| Contents Away From Home |

|

| Pedal Cycle |

|

| Accidental Damage |

|

| HomeServe |

|

| Family Legal |

|

M&S Home Insurance Notable Exclusions

M&S home insurance exclusions include (but are not limited to) damage to fences, gates or hedges, loss or damage if you've been away for 60 days or more (occasional visits don't count), frost damage, damage by pets, subsidence (due to coastal or river erosion, settlement, faulty workmanship, etc.), etc.

A few exclusions stood out to us as particularly mentionable. You may want to keep them in mind if you go with M&S or as you're comparing different home insurance plans. It's always a good idea to read through the full list of exclusions in the policy documents as we've only mentioned some exclusions here and others may be more relevant to you.

- 1. Standard building cover doesn't include loss or damage caused by storm to fences and gates.

- 2. Contents cover doesn't include loss or damage during household removals to personal money, jewellery, watches, items of gold or platinum, stamps and coins.

- 3. Theft or attempted theft from a nursing home or housing while attending full time education is excluded, unless forcible and violent means are used to gain entry or exit.

- 4. Theft of unattended bicycles is excluded unless locked in a building or to an immovable object.

- 5. For policies including Away From Home cover, theft from a vehicle is only included if the items are hidden from view, all windows are closed and the boot and all doors are locked—note, the policy documents do not specify a "theft from vehicle" limit (we frequently see a £1k or £2k limit from many other insurers).

- 6. Those who leave their homes unoccupied for more than 90 days at a time won't have cover for malicious people or vandals, theft or attempted theft or water escaping from water tanks, pipes, equipment or fixed heating systems.

M&S Buildings & Contents Insurance: What's Covered?

Marks and Spencer home insurance protects against calamities such as fire, explosion, lightning, earthquake, smoke, water freezing in pipes, theft, storm, flood, escaping water and oil, subsidence (depending on cause, etc.), falling trees, branches and radio/TV aerials, etc.

| Cover benefits | Premier | Standard |

|---|---|---|

| Buildings cover | Unlimited | £1,000,000 |

| Buildings accidental damage | Included | OPTIONAL |

| Contents cover | Unlimited (inner limits apply) | £100,000 |

| Contents accidental damage | Included | OPTIONAL |

| Valuables | £50,000 | £25,000 |

| Valuables (single item limit) | £15,000 | £10,000 |

| Garden contents | Included | Up to £100,000 |

| Storm damage to gates and fences | Included | Not covered |

| Protected no claims discount | Optional | Optional |

| OPTIONAL | ||

| Contents away from home | £50,000 (£15,000 per item) | £25,000 (£10,000 per item) |

| Pedal Cycle away from home cover—worldwide cover for theft, loss or damage of your family’s bikes | £250 up to £15,000 | £250 up to £10,000 |

| Legal expenses | £50,000 | £50,000 |

| Home emergency cover | £1,000 | £1,000 |