Best Cash Back Credit Cards

We've analyzed dozens of credit cards, in order to find the best cashback cards for giving you money back on your purchases. Selecting the best card for you will depend on your individual budget and spending patterns, there are many good options available. To learn more about cashback rewards, please see our Cashback vs. Miles vs. Points: What’s the Difference? guide.

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

-

Comparing

Summary of the Best Cashback Credit Cards -

Best Cashback Credit Cards Overall & No Fee

American Express Platinum Cashback Cards -

Cashback Credit Card for Groceries

Amex Nectar

-

Learning

How Does a Cashback Rewards Credit Card Work? -

Choosing

How To Pick the Best Cashback Card for You -

Methodology

Methodology

According to our analysis of the market, the following cards stand out as objectively the best for certain purposes. The best card for you will depend on your individual situation and spending patterns. Please use the information in this guide to learn about differences between products and help you narrow down your choices.

Cashback Credit Card Comparison

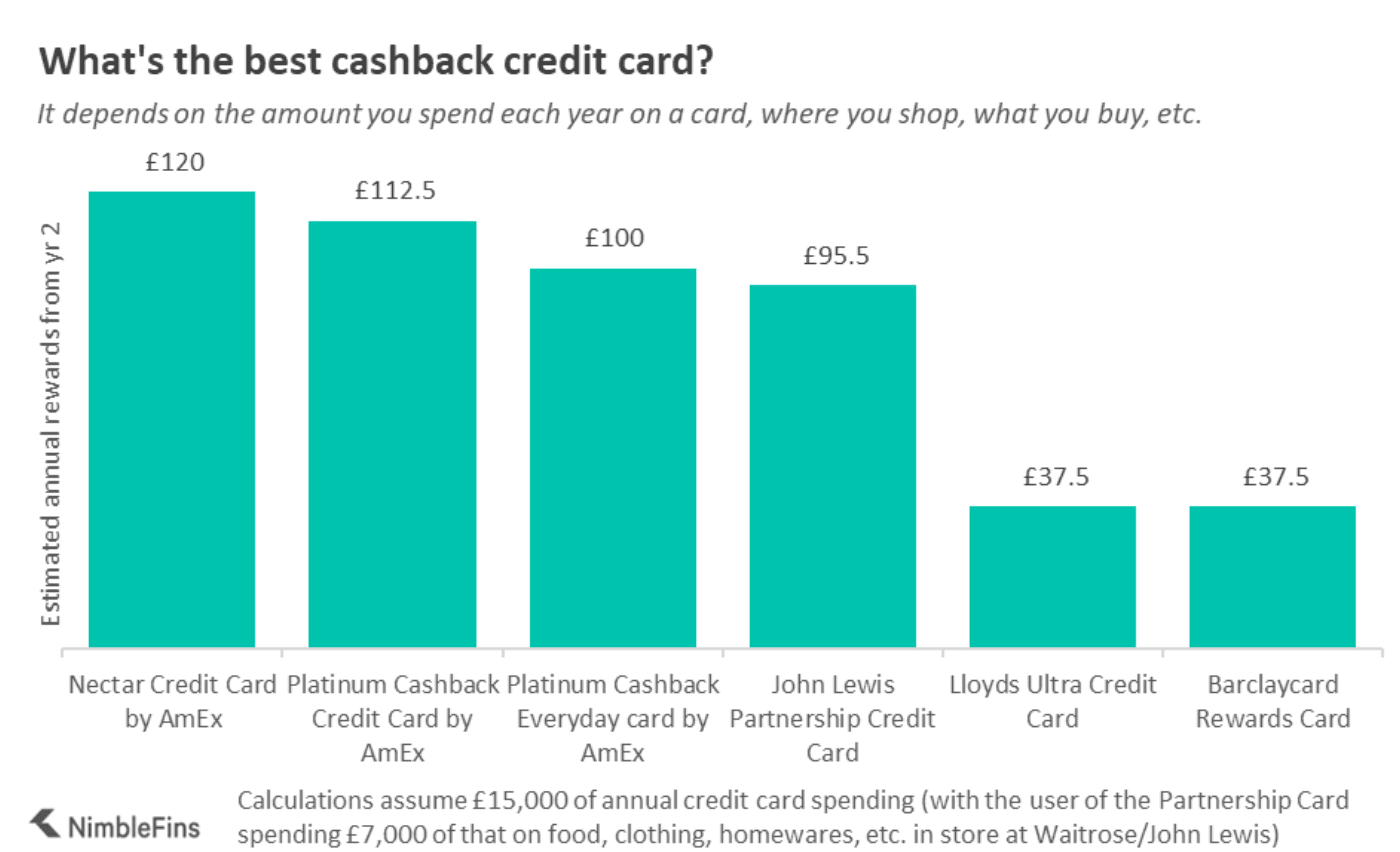

To compare cashback credit cards, NimbleFins analysed six cash back (or equivalent) credit cards and calculated the cashback rewards the average UK consumer charging £15,000 per year could earn on each card.

The card with the highest ongoing rewards rate is the Nectar Credit Card by American Express, which returned an estimated 0.8% on ongoing rewards (~£120 per year).

The next highest-rewarding cards are the Platinum Cashback Credit Card by American Express and Platinum Cashback Everyday card by American Express cards, that returned 0.75% (£112.5 per year) and 0.67% (£100 per year), respectively.

While the rewards rate is a touch higher on the Nectar card, when it comes to true cashback, the Amex Platinum Cashback and Platinum Cashback Everyday cards have a distinct edge over the Amex Nectar Card: universal flexibility. Rather than locking your rewards into a specific loyalty scheme like Nectar points—which limits your spending to partners like Sainsbury's or Argos—the Platinum cards pay your rewards directly as an annual statement credit. It’s actual money knocked off your credit card bill, giving you total freedom over how and where you spend your savings. You need to consider the different features of each card, and how they may benefit you personally to determine which one is "best" for you.

Here is a summary of the rewards and estimated rewards outcomes for the six cards we assessed:

| Cash Back Rewards Credit Cards | Initial rewards | Ongoing rewards | Annual Fee | Estimated ongoing rewards after year 1 for £15,000^ of annual spend (reflects annual fee) | ||

|---|---|---|---|---|---|---|

| the math | the rate | the rewards | ||||

| Nectar Credit Card by American Express | 20,000 Nectar points when spend £2,000 in the first 3 mos | Earn 2 Nectar points/£1 spent (£1 min); Earn 1 Nectar point/£1 spent at warehouse retailers | £30, waived first year | (2 x 0.005 x 15000-30)/15000 | 0.8% | £120.0 |

| Platinum Cashback Credit Card by American Express | 5% for the first three months (up to £125 cashback) | 0.75% cashback for first £10k of purchases; 1.25% cashback on purchases beyond £10k, except 0.5% at warehouse retailers | £25 | (0.0075 x 10000+0.0125 x 5000-25)/15000 | 0.75% | £112.5 |

| Platinum Cashback Everyday card by American Express | 5% for the first five months (up to £100 cashback) | 0.5% cashback for the first £10k of purchases; 1% cashback on purchases beyond £10k, except 0.5% at warehouse retailers (i.e., Costco) | n/a | (0.005 x 10000+0.01 x 5000)/15000 | 0.67% | £100.0 |

| John Lewis Partnership Credit Card | n/a | 1.25% in store; 0.1% out of store | n/a | (7000 x 0.0125 + (15000-7000) x 0.001)/15000 | 0.64% | £95.5 |

| Lloyds Ultra Credit Card | 1% cashback on all card purchases in first year | 0.25% cashback | n/a | 0.25% | 0.25% | £37.5 |

| Barclaycard Rewards Card | 0.25% cashback | 0.25% cashback | n/a | 0.25% | 0.25% | £37.5 |

^Note: Actual rewards rates on some of the cards will vary based on the amount you spend each year on the credit card. Also, American Express cards are accepted by a smaller proportion of retailers, which could impact actual rewards rates.

Please see the methodology section for more information, including why we picked annual spending of £15,000 for our calculations.

Best Overall & No Fee Cashback Credit Cards

In our opinion, the following cards offer the best cashback rewards in their respective categories. We have modeled their features to estimate annual rewards, based on potential UK household credit card charges of around £15,000 a year (£1,250 per month). Our calculations incorporate all relevant annual fees, rewards rates, bonuses, etc. Actual results will vary depending on how you use a card. And as with all rewards cards, it's important to pay back the full balance each month in order to take best advantage of the rewards.

Overall Cashback: Platinum Cashback Card from American Express

The Platinum Cashback Card by American Express is one of our favourite overall cashback cards not only for the great rewards across all categories but also because it pays out rewards as statement credits. Over the long-term, the card earns 0.75% or 1.25%, depending on your level of spending. You can also take advantage of the welcome offer of 5% for the first three months (up to £125 cashback). Despite the relatively modest £25 annual fee, we have calculated the Platinum Cashback card can earn the average UK household charging £1,250 to their card (and paying back in full each month) around £112.5 per year in cashback rewards. Since the rewards are given as statement credits, the rewards on this card are generally simple to use and flexible compared to many others in the market.

Note the 34.6% representative variable APR (29.1% variable purchase APR).

Cashback is not earned on cash advances, balance transfers, travellers' cheques, FX transactions, interest, any spending above your credit limit, charges for returned payments, late payment or referral charges and finance charges.

- 0.75% cashback rate on purchases up to £10,000 per year

- 1.25% cashback rate on purchases over £10,001 per year

- 5% intro cashback rate up to £125 reward

- Amex not accepted everywhere

Best Cashback Card with No Annual Fee: Platinum Cashback Everyday Card from American Express

The Platinum Cashback Everyday card from American Express is a great cashback card option to consider for those who expect to spend less than £10,000 a year on the card. While it sports lower cashback rates than our top overall pick and its sister card, the Platinum Cashback card, the lack of annual fee likely makes it better value for smaller spenders. (In contrast, the paid card could deliver higher cashback rewards for larger spenders.)

The Platinum Cashback Everyday card offers long-term cashback rates of 0.5% to 1%. As cashback comes in the form of statement credits, the card is a solid contender for those desiring a simple rewards card.

Note there is a £3,000 minimum spend requirement per card year to earn any rewards on this card!

Note the 29.1% representative variable APR.

Cashback is not earned on cash advances, balance transfers, travellers' cheques, FX transactions, interest, any spending beyond your credit limit, charges for returned payments, late payment or referral charges and finance charges.

- 0.5% cashback rate on purchases up to £10,000 per year

- 1% cashback rate on purchases over £10,001 per year

- 5% intro cashback rate up to £125 reward, in first five months

- No annual fee

- Amex not accepted everywhere

Best Store Cashback Cards for Food (Groceries)

If, like many people, you spend a lot of your budget on food you might benefit from a credit card that rewards extra for dining and/or grocery spending. Depending on your particular needs, one of these cards could turn out to be quite rewarding for you.

Amex Nectar Credit Card

The Nectar Credit Card is probably the most flexible grocery credit card, because unlike other grocery-related credit cards, the Nectar card gives you the same approximate 1% rewards rate on all shopping. So you can shop at any grocery store you want and also use the card for general spending and earn the same rate. Most other grocery loyalty credit cards (e.g. Tesco Clubcard or the Partnership Card) only deliver an equivalent rate on in-store spending (not out-of-store spending).

The first year with the card is the most valuable—the relatively high welcome bonus of 20,000 Nectar points (earned when you spend £2,000 in the first three months) is worth around £100, more than any other grocery welcome bonus. While you are not limited in how you earn points, you can only redeem points at one grocery chain (Sainsbury's) or other Nectar partners. Cardholders can expect to earn Nectar points worth around £120 in their second year and beyond, assuming £15,000 of annual spend which is roughly the amount that the average UK household would spend on a credit card.

Note the 35.8% representative variable APR (29.1% variable purchase APR).

- Earn 2 Nectar points for almost every £1 spent (£1 minimum), in addition to Nectar points earned through the Nectar loyalty program when shopping at Nectar partners (approx. 1% rewards rate)

- Earn 1 Nectar point for every £1 spent at warehouse retailers (approx. 0.5% rewards rate)

- Welcome offer of 20,000 Nectar points when you spend £2,000 in the first three months (worth approx. £100)

- Access to Global Assist for help when you travel abroad

- Purchase Protection will repair or replace any damaged or stolen items within 90 days of purchase

- £30 annual fee (waived first year)

- Amex not accepted everywhere

How Does Cashback Work?

Cashback is the most flexible and easiest-to-use of the rewards systems. Cashback cards return a percentage of your spending made using the card. Often, the percentage varies by spending location or category (e.g., different rates in-store vs out-of-store on branded cards).

How to Choose the Best Cashback Card for You

Choosing the best cashback credit card for you will depend on your individual needs and spending habits. In particular, when looking across the cashback cards you should keep in mind these two factors:

- where you spend your money (e.g., restaurants, a specific grocery store, petrol, etc.)

- the type of cashback you prefer (i.e., store vouchers or statement credits)

Some of the cashback credit cards listed here have no annual fee, so it is feasible to take out more than one card in order to optimize your rewards across different spending categories. Additionally, as many of the cashback cards are issued by American Express, which isn't accepted everywhere, a Mastercard or Visa cashback card may come in handy when your Amex has to stay in your wallet.

Those looking for a simple rewards program should focus on the cashback programs that deliver rewards as statement credits or store vouchers. But while statement credits might be simpler, they are not necessarily better for you. Many people love the idea of heading out to shop with a big voucher in their wallet. It all depends on your personal preferences.

Methodology

For this article, our team considered the following credit cards that offer cashback rewards on spending, where cashback is defined as statement credits or an equivalent that can be used to reduce a common cash payment (e.g. vouchers or Nectar points):

- Platinum Cashback Credit Card by American Express

- Platinum Cashback Everyday card by American Express

- John Lewis Partnership Credit Card

- Nectar Credit Card by American Express

- Lloyds Ultra Credit Card

- Barclaycard Rewards Card

- Santander Edge Credit Card

- Amazon Barclaycard

To determine the cards with the "best" rewards rates, we calculated expected rewards for a standard amount of spend in the 2nd year and beyond. (Rates in the first year can be highly variable due to waived annual fees, welcome bonuses, etc.)

The standard amount of annual spending we chose for our rewards calculations was £15,000 . Why did we pick £15,000 as the spending figure? A typical households spends the following amounts on average each year on the following categories, which add up to roughly £15,000 and which we assume could mostly be charged to a credit card and earn rewards:

- Food and non-alcoholic drinks: £3,911

- Recreation and culture: £2,068

- Restaurants and hotels: £2,501

- Household (furniture, linens, etc.): £1,980

- Clothing and footwear: £941

- Personal (e.g., toiletries, jewellery, sunglasses, etc.): £825

- Vices (e.g., alcohol, tobacco, etc.): £640

- Package holidays: £1,708

- Health: £429

For our calculations, we assumed:

- No spend at warehouse retailers (e.g. Costco)

- Value of 0.5p per Nectar point

- For the Partnership Card, an average of £7,000 of annual spend on food, clothing and housewares is purchased at John Lewis/Waitrose (achieving a higher in-store rewards rate)

^Note: Actual rewards rates on some of the cards will vary based on the amount you spend each year on the credit card. Also, American Express cards are accepted by a smaller proportion of retailers, which could impact actual rewards rates. "Warehouse retailers" include stores like Costco.