Vanquis Visa Classic Review: The Credit Builder Features You Need?

Vanquis Visa Classic Review: The Credit Builder Features You Need?

Good for

- Start with a credit limit between £250 and £2,500

- A friendly UK Customer Service call centre

- Online & SMS account management

- Slightly lower APR than some competing credit-builder cards

Bad for

- Carrying a balance month-to-month

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

The Vanquis Classic Credit Card is a credit-builder card that can help people with bad credit to rebuild their credit rating. By paying on time and staying under the credit limit, a cardholder's credit rating may improve over time. As a credit-builder card, Vanquis Classic interest rates are higher-than-average, but these can be avoided by paying your full balance each month.

Vanquis Classic Credit Card Review

The Vanquis Classic is a Visa card that may work well for you even if you have no credit history, poor credit history or are unemployed. As a credit-builder card, it can be used for improving your credit rating by giving you the chance to demonstrate good account management. How do you do this? By paying on time each month and staying within your credit limit. By doing so, your credit history should improve over time.

New customers start with an easy-to-manage credit limit from £250 (which can go as high as £2,500) as you can see here.

They used to say with good financial management you could get a credit limit increase after your 5th statement and every 5 months after that, but they seem to have gotten rid of that language with the higher initial credit limit range.

Applying for the Vanquis Classic Visa is pretty quick and easy—you apply via mobile, tablet or PC. Potential applicants can use Vanquis's eligibility check to see their likelihood of being accepted before submitting an application. This feature is particularly useful for those worried about their credit rating, avoiding an unnecessary hard credit check and a rejected application which could make it even harder to get credit in the future. Depending on your application details, Vanquis may be able to give you a decision within 60 seconds.

Vanquis Customer Reviews

Is Vanquis any good? We scoured online reviews and found that existing customers rate Vanquis very highly. In fact, Vanquis has a remarkable 4.3/5 Trustscore on Trustpilot, reflecting feedback from more than 40496 customers—and 82% of reviewers said Vanquis was "Excellent." In our opinion, this rating is quite high for a financial product—and we're glad to see it on a credit builder card.

Many customers remarked on the usefulness of the app in managing their account (e.g., tracking spending, paying on time, staying under the credit limit, etc.), although not all customers have a top-notch experience and the higher interest rates are a problem for those who can't pay their entire balance each month.

Here are some real quotes from existing customers to give you an idea of some customer experiences:

"From online application to approved with documents submitted and a better introductory offer than advertised within 48hrs. Easy and quick with no fuss or hassle."

"I have a credit card with Vanquis way over a year now, got a decent credit increase twice already, way more than other cards ever, no small print. I had a poor credit in the past when I applied but they but thay trusted me and I improved my credit score since then. Called customer service once regarding a balance transfer and had a nice helpful chat with a native speaker, rather than a bot. The only thing is the app, its ok however other banks offer instant balance refresh. Overall I'm happy."

"Nice people but hopeless system. I tried to set up a savings account. The optional home telephone number is not optional as you cant skip it so if you dont have a home phone go away! After filling in all the details you need to fill in your nominated bank. However, their system offers a choice of what it considers will be your nominated account name. If your nominated account name does not match their system then you are stuck and have to start sending proof and paper work off which is a complete waste of time. Hopeless. Done loads of this over the years and never had this problem."

"Easy app to use and check when payments are due are simple... easy to apply and receive the card."

"Best card I’ve ever had, lovely friendly staff, I lost my job and went over my limit and they where great about it xxxxx"

"Good experience and user friendly app and help to manage the day to day expenses."

"I find Vanquis very easy way to purchase items and keep check on my spending also I am improving my credit rating would recommend to anyone."

"... it is teaching me... how to budget my finances and stop the urge to go on a shopping spree... a massive issue in the past. Thank you so much Vanquis you have done such a positive thing for me and I am sure have done so for many many others."

"Vanquis is helping me rebuild my credit rating!"

"The app is absolutely terrible!! I’m so tired of it resetting and then having to faff around in order to set my card up again and pay my balance. Online process isn’t that great either. The whole process is so clunky and takes days for payments to clear. As a result I’ve switched over to a new card today. Will be settling and closing."

"Interest rates are outrageous. I pay their ridiculous interest every month on time, plus I pay in alot of money voluntarily every month, and they charge you like there is no tomorrow...."

"The app was great until the past week or so, now often offline and Payit has stopped working. I emailed them and didn't get a reply."

"The app STILL doesn’t work with iOS 16! Just launches and immediately quits! Rubbish, and no reason given."

We find negative reviews can be really helpful, as they can help cardholders figure out how to get the most of out their cards. For instance, it seems that the App glitches sometimes so we'd recommend paying a few days early to give yourself a time buffer if this happens to you (they recommend paying 3 working days in advance anyway to give time for the payment to process).

Also, Vanquis does charge higher interest rates because they accept people with worse credit histories—these cards are best used by paying off your full balance each month (or as much as you possibly can) and working to rebuild your credit history. They're not good for carrying a balance due to the high interest rates.

Vanquis Classic Benefits & Features

| Vanquis Classic Credit Card Features | |

|---|---|

| Credit Limit | Between £250 and £2,500 |

| Credit Limit Increases | You may be eligible for credit limit increases |

| Transaction Fees | Non-sterling transaction fees of 2.99% |

| Cash Withdrawal Fee | 3% or £3, whichever is greater |

| Annual Fee | £0 |

| APR |

|

Vanquis Interest Rate (APR): The stated Vanquis Classic purchase APR is 42.9%. At least 51% of applicants will receive this rate or better. The other 49% of applicants may receive a higher interest rate, anywhere from 42.9%. Cash rates are typically higher, starting at 37.9% variable APR.

Vanquis Credit Limits and Credit Increase: Vanquis credit limits fall between £250 and £2,500, depending on your financial situation and credit history.

While some cardholders find a higher credit limit can be useful for purchasing power and a possible improvement to their credit score, a higher credit limit may not be in your best interest, depending on your individual financial situation. For instance, if you're on a strict budget and would rather not have the temptation of a higher limit you can reject the increase or request that Vanquis lower your limit. Remember that if you exceed your credit limit, then your credit score would be harmed and you'd incur default fees.

Vanquis Cash Limits: Withdrawing cash using a credit card is expensive and we don't generally recommend it for three reasons:

- Cash interest rates are higher than purchase rates

- Interest on cash withdrawals is charged immediately (there is no grace period)

- Each cash withdrawal incurs a fee of 3% of the transaction or £3, whichever is greater

Using Vanquis Abroad: The Vanquis Visa can be used abroad. Each time you do so, you'll pay a 2.99% non-sterling fee on all foreign transactions such as taking foreign cash from an ATM or paying for a restaurant or hotel in a local currency. This fee is typical on all but special travel cards.

In addition to the non-sterling FX fee, any foreign cash withdrawals from an ATM abroad would incur an additional 3% (£3 minimum) cash withdrawal fee—this cash fee is charged in addition to the 2.99% non-sterling fee. Not only do you incur these fees but as interest is charged immediately on cash withdrawals, using a credit card is generally an expensive way to get travel cash.

| Type of Non-Sterling Transaction Abroad | Fees |

|---|---|

| Foreign Cash Withdrawals | 3% (£3 min) + 2.99% |

| Foreign Credit Card Transactions (i.e., purchases) | 2.99% |

What's the Minimum Monthly Payment on a Vanquis credit card? To give you a general idea of what to expect to pay each month, the Minimum Repayment is calculated as the highest of:

- 1. Depending on your APR, one of 3.5%, 4.5% or 5% of the balance owing on your Account as at the statement date and any amount by which your Account is in arrears; or

- 2. Any interest/minimum finance charge, default charges and any account maintenance fees added to your Account since your last statement plus any arrears due on your Account plus 2.3% of the remaining balance; or

- 3. £5.

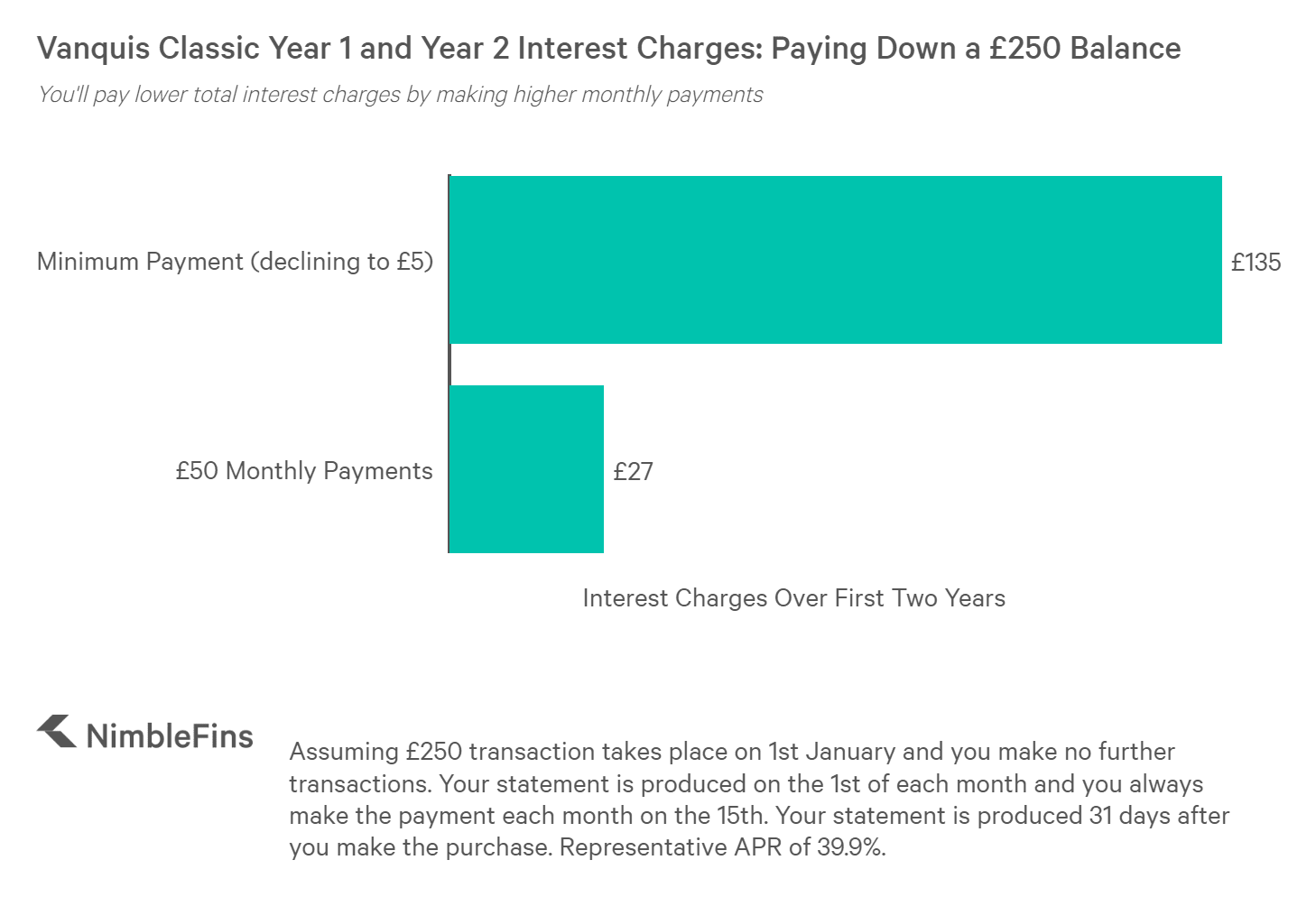

If you don't make additional purchases on your card, the minimum monthly payment will drop over time (as the balance falls) until it hits the £5 minimum payment floor. As we discussed in our article Here's How the Minimum Payment Floor on Your Credit Card Could Cost You Hundreds of Pounds, paying only the £5 minimum payment floor can prove quite costly over the long term in terms of interest charges. In fact, in the example below, a cardholder paying only the minimum each month would delay paying off their £250 debt by over 5 years, and incur over £150 more in total interest charges over time, versus a cardholder who consistently pays £50 per month.

Cost of Borrowing with Vanquis Classic

The above example assumes the following: The transaction takes place on 1st January and you make no further transactions. Your statement is produced on the 1st of each month and you always make the payment each month on the 15th. Your statement is produced 31 days after you make the purchase.

Bottom Line: Even if you're unemployed, have a bad credit history or have no UK credit history, you may be able to get a credit card with Vanquis. In fact, if you need a credit card but are concerned that you won't be eligible, Vanquis may be one of your best chances of getting a card. Just remember to always pay on time and pay as much as possible each month!