Self Employed Insurance: What Do I Really Need?

Find self-employed insurance today.

Powered by QuoteZone.

Compare Quotes Now

- Rated 4.8 out of 5 stars on Reviews.co.uk

- Over 300,000 quotes completed per month

- Fill out only one form

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

As seen on

What is Self Employed Insurance?

If you're self employed, you really need to consider to consider buying business insurance. Not having the right cover in place could lead to significant financial problems. Why? When you're not employed and protected by a company's cover, you are directly exposed to certain risks—like being sued.

Below we explain the different risks faced by the self employed, and how to protect yourself with different types of insurance. Check out the examples of how they work and for quick definitions see the blue boxes. To find out how much people typically pay for self employed insurance go to the average cost section and when you're ready to get no-obligation quotes yourself, click here where you'll fill out a short form and can request a call back if you still have questions.

- What are popular types of self employed insurance?

- Where can I get self employed insurance quotes?

- FAQs

- Self-employed statistics

What are Popular Types of Self Employed Insurance?

While each situation is unique, there are a few types of business insurance consistently popular with self-employed people in the UK. Below we explain what each one generally covers, and provide some real-life examples to help you decide what types of cover you need given your individual circumstances. If you still have questions, fill out a quote form where you can request a call back on the phone.

Self Employed Public Liability Insurance

Public liability insurance is critical if you are self employed and you have in-person contact with members of the public, such as customers, clients, a landlord or other people. Why? If a third party is accidentally injured, or their property is damaged, and they blame you, you could be facing an accidental injury or damage lawsuit.

Even if you've done nothing wrong, public liability insurance can be helpful because it will give you access to a legal team to support your defence. It covers both legal expenses to defend you and your business and compensation claims if you're found liable. How much public liability insurance do you need if you're self employed? It's a personal decision but, for reference, public liability insurance is commonly sold with £1 million, £2 million, £5 million and £10 million of cover in the UK. Get quotes here.

- Bodily Injury Example: A member of the public slips and falls on a freshly mopped floor in your design office, blaming you.

- Bodily Injury Example: A client trips on materials you left on the floor, falling and breaking their wrist. They sue you for negligence.

- Property Damage Example: A fire in your catering premises that damages a shop next door to you. That business sues you for damages.

- Property Damage Example: When bringing heavy equipment into a client's property, a freelance massage and beauty therapist accidentally damages a client's property. (IF you're a self employed freelancer, see our article What Insurance does a Freelancer Really Need?

Learn more in our article on Why Public Liability Insurance is So Important if You're Self Employed.

Product Liability Insurance

Product liability insurance protects against claims that your business's goods or products have caused bodily injury or property damage. If you design, make and/or sell a product, or if you fix things, you might need this cover. In addition to product designers and manufacturers, tradespeople like builders, plumbers and electricians should consider product liability insurance, plus those selling on ebay, Etsy, Amazon, etc.

- Product Liability Example: A member of the public falls ill after eating food and blames you for food poisoning.

- Product Liability Example: A dog has an allergic reaction to the materials used in the dog toy you make and sell.

Professional Indemnity Insurance for Self Employed

Professional Indemnity (PI) insurance protects you if you're self employed and you sell your expertise, which could be in the form of advice or professional services. PI insurance covers client claims of financial loss due to advice or service given as part of your self employed work being negligent (for example, you've made a mistake or error in your work); it will cover your legal defence fees as well as any compensation you need to pay.

Depending on the work you do, some clients might contractually require that you hold PI insurance. Self-employed professions that might need PI insurance include, but are not limited to:

- Accountant

- Architect

- Consultant

- Contractor

- Designer

- Engineer

- Gardener

- Lawyer

- Photographer

- Solicitor

- Surveyor

- Videographer

- Web developer

- Wedding planner

- Professional Indemnity Example: A designer works on a high-end renovation for a client's home. Mid-way through construction, the client claims that your design is not able to be completed within budget and sues you for their financial loss.

Note: Self-employed hairstylists, beauty therapists and massage therapists should look into a product very similar to professional liability insurance called "treatment cover", which covers injuries to your customers or clients that occur during or due to your work.

Employers' Liability Insurance

Self employed doesn't necessarily mean you work alone. If your business expands and you hire employees, you'll need to buy employers' liability insurance (EL) coverage—it's required by law even for casual or temporary workers. There are a few exceptions, of course, when you don't need cover.

EL insurance can feel expensive compared to other types of business insurance but it protects against compensation claims by current or former employees if they fall ill or are injured because of their work for you. It covers both legal fees in defending yourself from a claim and any compensation you're required to pay.

- Employers' Liability Example: An employee injured their back at work. They blame you for faulty training and sue you for negligence.

Contents, Equipment and Stock Cover

Contents insurance covers accidental damage, loss or theft of valuable equipment, furniture & furnishings, computers and other business items that can be expensive to replace. Having contents cover not only provides financial protection for the value of these goods, it also helps get you working again if you do face a disaster like fire, flood or theft. Whether you rent your premises or own them, contents cover can be a critical component of insurance for someone who's self employed.

Those holding valuable stock can pay an extra premium for stock insurance, which is typically offered as an extra, add-on insurance coverage. Stock cover provides financial protection if your stock is lost, stolen or damaged. As with everything there are exclusions, for instance frozen food isn't usually covered (but sometimes you can pay extra for this if you need it), nor is general deterioration of stock.

- Contents and Stock Insurance Example: Your premises are broken into, and your laptop and other business equipment are stolen.

Business Use Car Insurance

Declaring business use on your personal car insurance is critical if your self-employed work involves driving between multiple work locations or visiting clients. If you use your car in these ways but have only disclosed social, domestic, pleasure driving and/or commuting, your insurance could be deemed invalid and you'd essentially be driving uninsured. Most, but not all, insurers will let you expand your coverage to include business use.

There are three classes of business use. Class 1 covers driving away from your regular place of business, for instance to multiple work sites or to visit clients. Class 1 can cover spouses as long as they're driving for your business. Class 2 would cover a named driver such as an employee or co-worker. Class 3 ("commercial travelling") is far less commonly used and for the type of driving done by travelling salespeople.

Note: There are circumstances in which "business use" is not sufficient and you need a "commercial" vehicle insurance policy instead. For instance if you get paid to deliver goods you'd need courier insurance and if you get paid to transport people then you need a form of taxi insurance.

- Business Use Car Insurance Example: You have an at-fault accident while driving your personal car to visit clients. Luckily, you are insured because you had previously declared and paid for business use on your car insurance policy.

Legal Expenses and Tax Investigation Insurance

Business legal expenses insurance (LEI) covers situations that you can face if you're self employed, like tax enquiries, debt recovery and contract disputes, providing access to an expert legal team and paying your legal defence costs in certain situations up to the policy limit for situations such as:

- Employment disputes

- HMRC tax enquiries

- Failed health & safety inspections

- Contract disputes

- Debt recovery

- Property protection

- Identity theft

- and more

- Legal Expenses Insurance Example: You have a dispute with a client that ends in them not paying you for your work. You need legal assistance to pursue a claim against them.

IT and Cyber insurance

If you process payment card information or store sensitive customer information such as names, addresses, banking information then it's a good idea to consider cyber insurance. Cyber insurance covers losses related to hacking, data breaches, viruses and other cyber crimes, covering direct costs incurred by your business and also claims from third parties that were harmed by an attack on your systems.

- Cyber Insurance Example: You open an email attachment that contains a virus, allowing hackers to gain access to client information and your business files. Cyber insurance pays for experts to deal with the situation, including paying a ransom, credit score monitoring for affected customers, etc.

Personal Accident Insurance

If you have a work-related accident that leaves you unable to work, personal accident insurance can help you pay your bills while you're off work. This type of cover pays out a benefit as a weekly amount or a lump sum payment to help with lost self-employed income. You can learn more about other types of personal insurance from the MoneyHelper.

- Personal Accident example: You trip while carrying a large box into your business premises, falling and seriously breaking your leg. You're unable to work for 6 weeks while you heal, and the personal accident insurance pays a weekly benefit over this time.

Other Types of self employed insurance

Self employed people might also want other types of business insurance such as business interruption cover in case your business premises are physically damaged in a fire, flood or storm leaving you unable to work (but business interruption insurance doesn't usually cover lost revenues due to situations such as the coronavirus lockdown).

Is Self Employed Insurance Required?

A self employed person can absolutely find themselves in a situation in which they're sued or face another type of financial loss that can be mitigated from the right insurance coverage.

Even if a liability claim is unfounded and you've done nothing wrong, if someone sues you, you still need to defend yourself, which can cost thousands of pounds. If you are found liable, then you'll have to make a compensation payment which can reach into the tens or hundreds of thousands of pounds or even more.

When you need public liability insurance: One of the most common types of self-employed liability insurance is public liability insurance, which protects against claims of accidental injury or damage made by third parties. Public liability insurance is usually needed if you have in-person exposure to clients or other members of the public. Read more in our article on the subject: Do You Need Public Liability Insurance if You're Self Employed?

When you need professional insurance: If you give advice or offer a service (e.g., a self-employed garden designer or architect) then professional indemnity insurance can protect against claims made by clients that you haven't done your job properly.

When you need employers' liability insurance: If you hire any employees, you're required by law to hold employers' liability insurance in most cases, even if you're self employed.

When you need to declare "business use" on your car insurance: You will need to declare business use on your car insurance if your self-employed work involves driving to clients or visiting multiple work locations. (People paid to make deliveries or transport passengers need a form of Who needs commercial vehicle insurance?).

Common Types of Self Employed Jobs

- Accountant

- Barber

- Chef

- Creative

- Engineer

- Graphic Designer

- Instructor

- Makeup artist

- Photographer

- Videographer

- Architect

- Beauty therapist

- Consultant

- Designer

- Florist

- Hair stylist

- Interpretor

- Masseuse

- Solicitor

- Web developer

- Artist

- Cameraman

- Contractor

- Dog grooming

- Gardener

- Healthcare professional

- Lawyer

- Personal trainer

- Surveyor

- Wedding planner

How Much is Insurance if you're Self Employed?

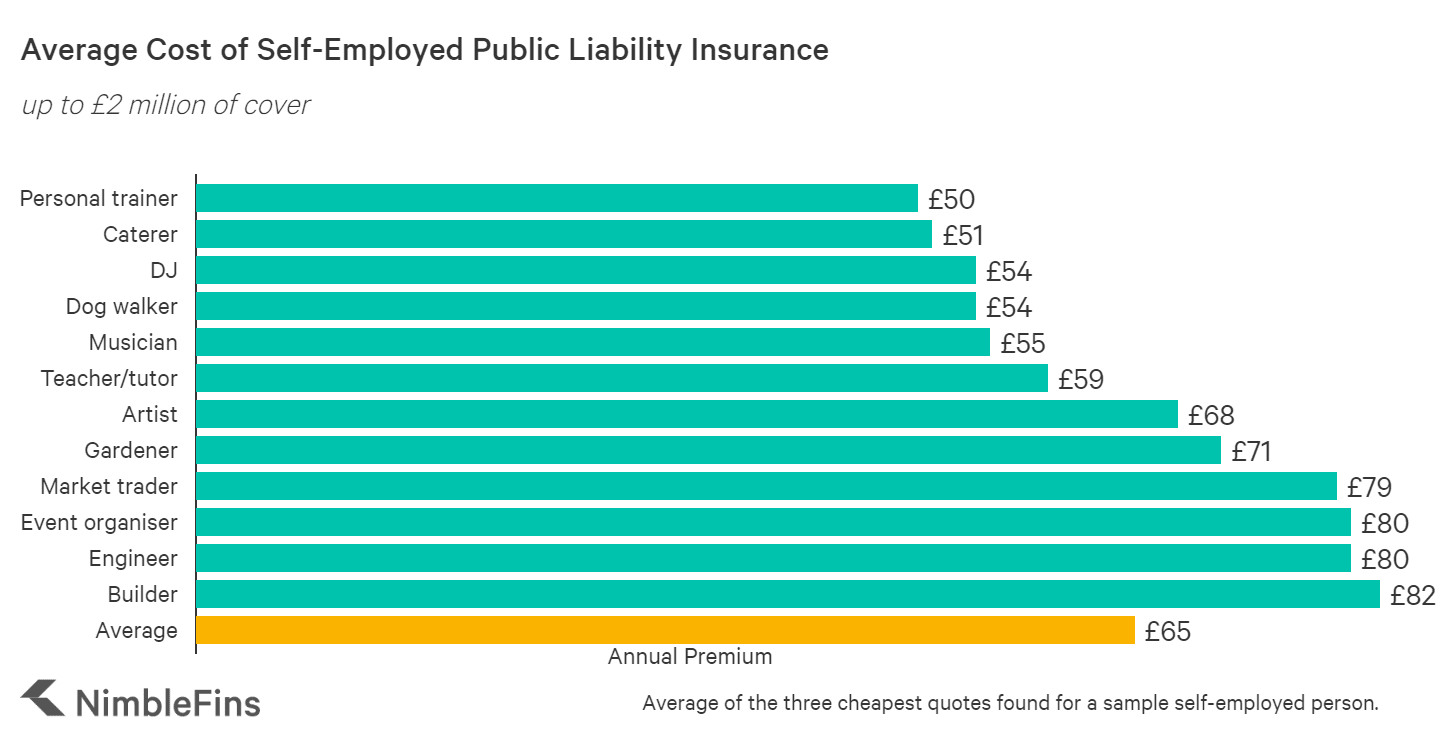

Basic public liability insurance if you're self employed costs from £50 - £60 a year for less-risky professions like cleaners, dog walkers, photographers, teachers, tutors, caterers, musicians, DJs, and more. Riskier professions like engineers, gardeners and builders will pay more. In the table below you can see typical public liability insurance costs for a sample self-employed person.

If you give advice or a service you might need professional indemnity insurance, which starts from around £80 a year. If you need to declare business use on your car, expect your premiums to go up as well. Add-ons will increase your insurance costs.

Where can I get self employed insurance quotes?

Compare self employed insurance quotes here—after filling out a short form you'll receive quotes from a number of self employed business insurance providers. You can even request a call back if you still have questions that you want to discuss. Then choose the cover that offers the best price and features for your needs.

FAQs

Yes, self employed people need their own insurance. The types of insurance you need if you're self employed depend on the work you do and other factors. Read about different professions and self employed insurance needs here.

A self employed painter probably needs public/product liability insurance because they have contact with clients and other third parties. A self employed painter who hires any employees needs employers' liability insurance. They might also want add-ons such as equipment cover, personal accident cover and/or professional indemnity cover to protect against claims a client has faced a financial loss because you've made a mistake in your work/given poor advice.

A self employed hairdresser typically needs public and product liability insurance, treatment cover and employers' liability insurance if they employ anyone. Others types of cover needed could include property/contents insurance and be sure your car is covered for business use if you drive to clients or multiple work locations!

A self employed gardener typically needs public and product liability insurance to protect against accidental injury or damage claims made by clients or other third parties. Plus they'll need employers' liability insurance if they employ anyone. Others types of cover needed could include equipment cover or personal accident insurance, and be sure to tell your car insurance company as you will need to make changes to your cover (e.g., declaring business use at a minimum).

A self employed carpenter typically needs public and product liability insurance to protect against accidental injury or damage claims made by clients or other third parties. Plus they'll need employers' liability insurance if they employ anyone. Others types of cover needed could include equipment cover or personal accident insurance, and be sure to tell your car insurance company as you will need to make changes to your cover (e.g., declaring business use at a minimum).

As of early 2026, the average cost of public liability insurance for self-employed individuals has risen to approximately £145 per year. This increase reflects the rising costs of legal defense and medical care, which impact settlement values. While low-risk professions like tutors or life coaches can still find cover for under £100, riskier trades such as construction or tree surgery typically face premiums starting at £250 to £450. Premiums can still vary by 5X or more depending on the specific nature of your work and the level of cover you choose.

You can get quotes for self employed insurance by filling out the form here—public liability, product liability, professional indemnity, employers' liability and more. If you're not sure what you need, you'll be able to talk with someone after you submit the form.

Yes—if you drive your car to multiple work locations or visit clients then you'll need to disclose business use to your car insurance provider or get a new plan that covers this. Read more about business use car insurance here or click to get quotes.

You can claim certain self employed business insurances such as public liability, product liability, professional indemnity, employers' liability—but not "benefit" coverages such as personal accident insurance.

Self Employed Statistics

According to the latest 2026 data from the Office for National Statistics (ONS), there are now approximately 4.27 million private sector businesses in the UK that do not employ anyone other than the owners. The construction industry remains the dominant sector for self-employment, accounting for roughly 16% of all UK businesses. Modern shifts in the workforce have also seen a surge in professional, scientific, and technical services, which now represent one of the fastest-growing categories of self-employed individuals.

| Self Employment Statistics UK | |

|---|---|

| Construction | 925,000 |

| Professional, scientific & technical activities | 760,000 |

| Wholesale, retail & repair of motor vehicles | 480,000 |

| Administrative & support services | 410 000 |

| Total self-employed | 4,272,535 |

The most common self-employed profession is also one of the most expensive to insure—due to dangers of the job, construction insurance premiums are relatively high.

Since the significant 2020 dip, the self-employment landscape has undergone a 'structural correction.' While the total number of self-employed workers has not yet returned to the 5 million peak seen in late 2019, 2025 and 2026 have shown a steady recovery. The market has shifted away from casual 'gig economy' roles toward more specialized, professional sole proprietorships. As of early 2026, the number of non-employing businesses has increased by roughly 200,000 year-on-year, driven by a post-pandemic desire for workplace flexibility and the growth of digital-first 'side hustles' transitioning into full-time ventures.