Courier Insurance: Quotes, Costs, Requirements (June 2024)

Want courier insurance? We can help.

Get ANNUAL courier insurance quotes for your car, motorbike or van.

Get annual quotes

Get SHORT TERM courier insurance quotes for your van.

Get short-term quotes

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

As seen on

Courier insurance is a form of Hire and Reward legally required for a car, van, motorcycle or bike used to carry other people’s goods and items in return for payment. If you use your vehicle to move something from A to B as a job, courier insurance can ensure you’re protected—and driving legally.

This article will help you understand courier insurance costs (which are noticeably higher than regular vehicle insurance premiums!), compare different types of courier insurance (courier van insurance vs courier car insurance, for example) and help you get the best quote possible for courier driver insurance.

Do you need Courier Insurance?

Simply put, vehicles used to move goods, materials or passengers from A to B must be covered by special courier vehicle insurance. The type of insurance needed, and the amount required, will depend on what the vehicle is being used for. This is one of the first questions people ask when they're thinking about becoming a courier.

If you’re working as an independent courier then it’ll be very important to confirm you’re covered to protect yourself against unexpected costs. At an absolute minimum, at couriers would be legally required to be covered by third party single vehicle courier insurance—regular vehicle insurance won't provide cover for courier work, so if you're going to be working independently then make sure look into courier delivery insurance before undertaking any work.

However, if you’ll be working through another company (think Deliveroo, Uber, or perhaps even a local furniture moving service), then it’s important to work out what you’re covered for and what you’re not.

These firms might provide a form of free coverage for "off-vehicle" accidents causing injury or damage to third parties while you're at work (in the form of public liability), but sometimes not for the courier themselves, and rarely for your vehicle, so if you want to ensure you/your vehicle are fully protected you’ll need a separate courier insurance policy. Each individual firm will have its own coverages, so make sure you know what you’re protected for—and which insurance you need to buy yourself.

What are the top Courier Insurance providers?

| Courier Insurance Providers | Popularity (monthly search volume) | Trustpilot Rating | Trustpilot # Reviews | Compare Courier Quotes |

|---|---|---|---|---|

| Academy Insurance Services Inc | 2,590 | 4.7 | 579 | Compare |

| Business Choice Direct | 1,390 | 4.7 | 1,595 | Compare |

| One Answer Insurance | 2,410 | 4.7 | 1,666 | Compare |

| Insurance Revolution | 5,190 | 4.5 | 677 | Compare |

| Inshur | 21,730 | 4.4 | 6,422 | Compare |

| Zego | 68,930 | 4.4 | 9,474 | Compare |

| County Insurance | 1,300 | 3.3 | 18 | Compare |

| Broadsure Direct | 440 | 2.9 | 2 | Compare |

| Coversure | 7,090 | 2.5 | 53 | Compare |

Compare Courier Insurance

It can take some legwork to find a cheap courier insurance policy, so using a search engine can be a time-efficient way to find the best courier insurance companies, whether you're looking for cheap delivery car insurance, cheap van insurance companies or other forms of cheap hire and reward insurance.

Want courier insurance? We can help.

Get ANNUAL courier insurance quotes for your car, motorbike or van.

Get annual quotes

Get SHORT TERM courier insurance quotes for your van.

Get short-term quotes

Also remember that pay-as-you-go courier insurance (like that offered by Zego) can be another option if you're only working as a courier part time or temporarily. But those working full-time as a courier might find an annual policy to work out cheaper in the long run.

Types of Coverage

Similar to what you might find with car insurance, there are three levels of cover you can buy to protect the vehicle you use for courier services.

Third-party-only

Third-party-only is the minimum level of coverage required legally to drive your vehicle. It will cover damages to another driver’s vehicle or property, but will not cover your vehicle at all.

- Example: An accident occurs involving you and another vehicle that you're at fault for—TPO covers damages to the other vehicle but not for yours.

Third-party, fire and theft

TPFT provides all the benefits of T-P-O, but with added protection for damages caused by fire or theft. You still are not covered for damages to your own vehicle caused by an on-road accident, whether yourself or another driver was at fault.

- Example: Your car is stolen from the street at night.

Comprehensive

Provides all of the benefits of the above, but with the additional benefit of covering you and your vehicle as well as any involved third parties.

- Example: Your car is damaged when you slide off the road in slippery conditions.

In the table below, you can see what coverage each policy offers you through insurance provider AXA, as an example. Our research indicated this was fairly standard across a number of courier insurance companies. When you compare courier insurance quotes, be on the lookout for the features in the list that you might need.

| What's covered? | Third Party | Third Party, Fire and Theft | Comprehensive | |

|---|---|---|---|---|

| Injury to other people or damage to their vehicles or property | ✓ | ✓ | ✓ | |

| Accident recovery cover | ✓ | ✓ | ✓ | |

| 93 days’ EU travel | ✓ | ✓ | ✓ | |

| Continued cover while your van is getting serviced or repaired | ✓ | ✓ | ✓ | |

| Minimum cover to legally tow a trailer | ✓ | ✓ | ✓ | |

| Loss or damage to your van caused by fire or theft | ✓ | ✓ | ||

| Built-in music, navigation and entertainment equipment | ✓ | ✓ | ||

| Loss or theft of your keys (up to £500) | ✓ | ✓ | ||

| Guaranteed courtesy van if your van is stolen or damaged | ✓ | ✓ | ||

| Loss or damage to your van | ✓ | |||

| Broken windows and windscreens | ✓ | |||

| Personal injury to the driver of your van (up to £5000) | ✓ | |||

| Medical expenses (up to £250) | ✓ | |||

| Personal belongings (up to £250) | ✓ | |||

| Cover if you put the wrong fuel in your van | ✓ |

Types of Courier Insurance

Courier Van Insurance

Courier van insurance covers vans used to carry goods or materials in return for payment. Courier van insurances are, generally, designed to protect most types of light haulage work, from couriers to furniture removal. Most policies offer the three levels of cover mentioned above: TPO, TPFT and comprehensive. And interestingly, comprehensive courier van insurance can be cheaper than TPO or TPFT, despite offering the highest level of protection. Courier van insurance costs typically start from around £2,000 per year.

Courier Car Insurance

Similarly to courier van insurance, cars used for courier services (now a more popular prospect than ever with the rise of tech companies offering paid courier work for small, easy-to-carry deliveries such as food/takeaway or individual packages) require a specific insurance policy. Your standard car insurance policy is unlikely to cover courier activities, and many service providers will require proof of insurance before allowing you to take jobs. Costs have really risen in this category, with many people now being quoted £4,000 per year.

Bicycle and Motorbike Insurance

Those wishing to use a bicycle/motorbike for work purposes will also want to consider policies to help protect themselves against any damages. Most courier ‘app’ companies will provide you with basic on-the-job coverage for injury/public liability (with some even offering sick pay or a one-off payment for paternity/maternity!) but won’t cover the vehicle at all.

Food Courier Insurance

Different food delivery services offer different levels of protection when you sign-up to work for them. As a minimum standard, most will provide third-party-only vehicle insurance and a level of public liability insurance. You can find out more about popular food courier services, and the food delivery driver insurance offered, here:

(Optional) Goods in Transit Insurance

The insurances mentioned above will cover your vehicle while it is in use for paid courier services, however some courier van insurances won’t cover the value of your goods in transit, so it’s worth checking to see if that is covered, if you need it. There can be specific exclusions on high value goods such as fine art or jewellery, so check before you buy if you know you’ll be working with these types of goods.

- Example: you’re carrying a set of expensive mirrors, some of which are damaged while driving. Your client wants you to pay for their replacement.

(Non-courier specific) Public Liability Insurance

Public liability insurance is one of the most common types of business insurance, bought to protect a business financially from the litigation costs and compensation payments that can follow certain types of accidents that cause injury to third parties or damage to their property.

- Example: while carrying a large item, your vision is impaired and you walk into a member of the public, knocking them over and causing a minor injury.

(Non-courier specific) Employers Liability Insurance

Employers liability insurance covers compensation payments to your current and former employees if they are injured at work or become ill due to their work for your business. In addition, employers liability insurance would cover legal fees associated with defending an employee liability claim.

- Example: one of your employees trips and falls while making a delivery, and believes insufficient equipment was at fault.

Optional Extras

When carrying out your courier insurance comparison, you might be interested in these other features, which may be sold as optional extras.

Breakdown/Accident Recovery

Some providers offer this as an optional extra, some offer it within comprehensive packages, so make sure to double check before buying. Provides you either with the help you need to get your van back on the road, or with a back-up vehicle in case yours is taken out of action longer term.

EU/International Insurance

More relevant for haulage couriers, but if you’re transporting goods across the UK border and into Europe/internationally, this special insurance ensures you’re covered while you’re outside of the UK.

Fleet (More than one van)

As with other types of commercial fleet vehicle insurance, courier motor fleet insurance coverage is laid out similarly to those designed for individual couriers (comprehensive, TP, TPFT) but covers multiple vehicles. Primary benefits include discounts and keeping all policies from the same provider (equal levels of coverage, single renewal date).

Haulage (or Hauliers Insurance)

Haulage insurance covers you for the movement of goods across long-distances. Haulage insurance is typically more applicable for jobs that takes a number of hours to complete, and generally involves one starting and finishing point.

How much does courier insurance usually cost?

NimbleFins research shows that courier van insurance typically ranges from around £1,450 to £2,150 for comprehensive cover, while courier car insurance can cost even more. The cost for insurance packages varies depending on which type of insurance you choose. Prices vary depending on which additional extras you do/don’t require, and which provider you choose to go with.

During our research we found that many providers consider courier insurance a more “specialist” product than personal car/van insurance, so there may be extra steps before you’re set-up properly and covered.

Our guide to the cost of Courier insurance goes into a lot more detail, so if you'd like to know more about the specifics (as well as some tips to save!) then have a read.

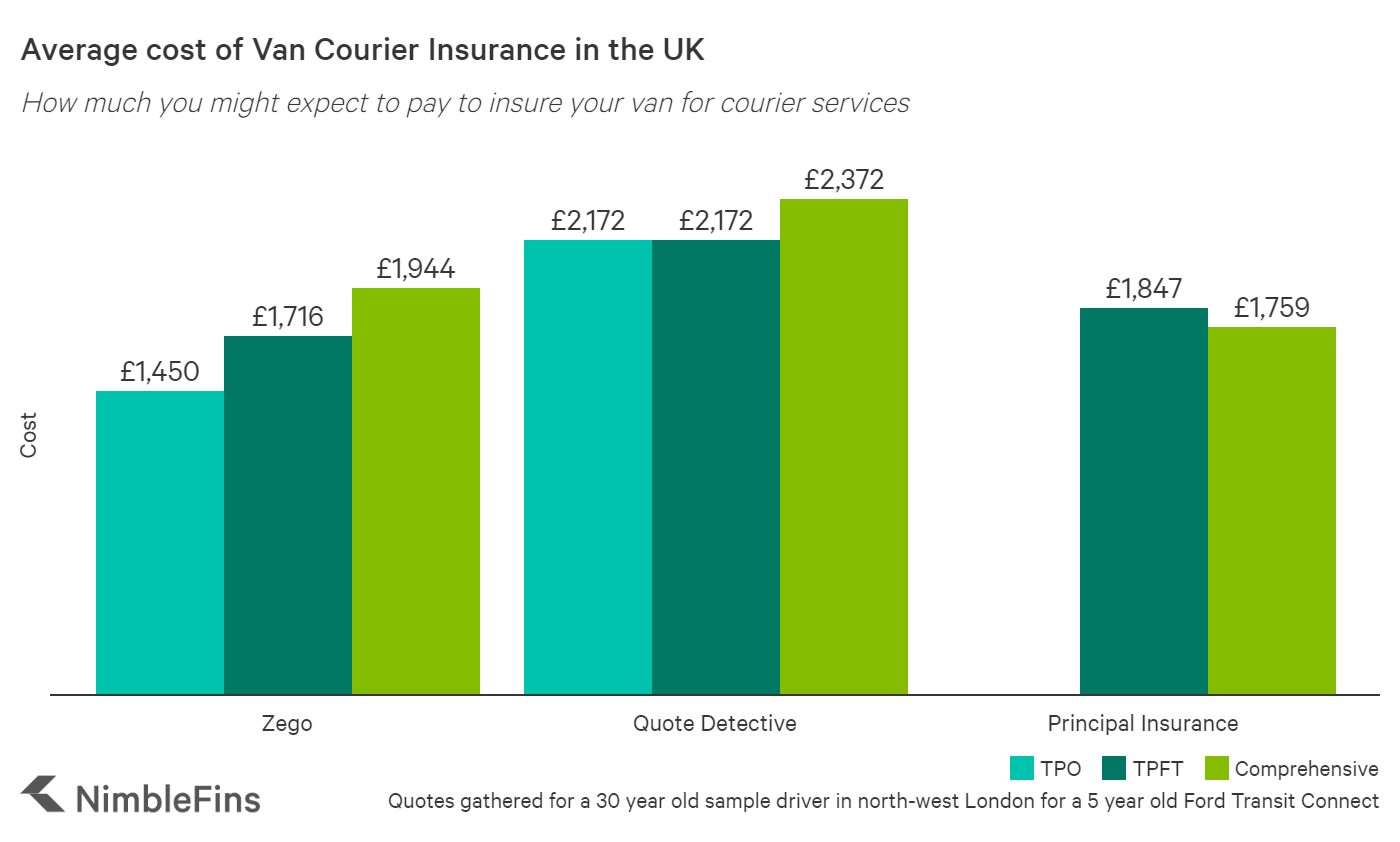

Below is a visual summary of 3 quotes we received for comprehensive, TPFT and TPO van insurances for a 5 year old Ford Transit. There are some interesting points to note.

| How Much is Van Courier Insurance in the UK? | TPO | TPFT | Comprehensive |

|---|---|---|---|

| Zego | £1,450 | £1,716 | £1,944 |

| Quote Detective | £2,172 | £2,172 | £2,372 |

| Principal Insurance | n/a | £1,847 | £1,749 |

Some providers offer TPFT as their minimum courier insurance coverage, and won’t offer a TPO policy.

Fully comprehensive coverage can, in some cases, be cheaper than less extensive policies, especially for older and historically safer drivers. A key reason for this is because young (and riskier) drivers typically search for TPO (minimum required) insurance and providers can afford to reward safer drivers for their business.

FAQ

Some level of commercial or hire and reward coverage is typically required in order to be a courier. The definitions of these vary from provider to provider, so make sure to be clear with your provider what type of work you'll be doing, and they'll be able to put together an appropriate policy for you. As courier work has become more popular, many policies will specify whether you are/aren't covered for delivery work, so look out for this as you research.

A courier working for somebody else's business (perhaps a local takeaway, an app like Deliveroo or a company like Amazon) might be covered by the business's business insurance (e.g. public liability insurance) but ask to be sure. A delivery driver operating their own vehicle would need to insure their vehicle is properly covered as mentioned above (e.g. appropriate commercial/hire and reward cover).

No—Goods in transit coverage is not a legal requirement for couriers or delivery drivers. That being said, it can be a great way to protect yourself if you regularly carry high value goods, whether they're your own or somebody else's.

Hire and reward insurance refers to a form of vehicle insurance that allows you to use your vehicle in return for payment. This, naturally, includes work such as food or parcel delivery but be sure the hire and reward policy you're considering covers the type of deliveries you'll be making (e.g. not all hire and reward policies cover food delivery).

You'll want to check with your provider for an exact definition, as each insurer defines hire and reward slightly differently. Being clear with your insurer about the type of work you'll be doing is critical to ensure you're properly insured.

It can be easier to find cheap courier van insurance if you drive a vehicle that insurers are most familiar, such as:

- Ford Transit

- Citroen Belingo

- Mercedes Sprinter

- Vauxhall Vivaro

Many methods of reducing your personal car insurance still apply to creating the cheapest courier insurance policy possible (no claims history, clean driving license, paying annually). Paying a larger policy excess (the amount you’ll pay in the event of a claim), fitting an enhanced security/monitoring system (black box, dashboard cam) and parking your vehicle closer to home/in a secure garage will all help to reduce the cost of your courier policy.

If you’re part of a larger courier company with more than one vehicle, you may also be able to sign up to a Fleet Insurance package, which will cover all vehicles under one policy at a lower rate than if you were to insure them with the same provider individually.

What to look out for in a courier insurance policy

As with most insurance policies, it’s worth making sure you know what you’re covered and not covered for. Our research found that most providers would charge extra for replacement vehicles, breakdown cover and legal cover in the case of a lawsuit, so keep these things in mind when creating a policy that works for you.

Also make sure to inform your social, domestic & leisure insurance provider (if they’re two separate policies) as soon as possible that you’ve started working as a courier, and the details of your new policy and provider, to avoid any unnecessary risk of them nullifying your policy in the case of an accident. Remember many insurers will happily add on courier/goods in transit insurance, so check with them if you’d like to keep the policy under one provider for convenience sake (but you could get a cheaper deal shopping around elsewhere!)

Common exclusions or conditions

There are many exclusions and conditions that apply to personal vehicle insurance that cross-over with courier insurance regarding security, accidents where you’re not at fault and the value of insurance that will be paid. There are some more courier specific insurance conditions to be aware of, such as trailer coverage (most policies will not cover you for damages or theft incurred to a separate trailer attached to your car or van, so you’ll need to purchase this separately).

If it’s your first time owning and driving a van, your no claims bonus/discount from your car driving history also doesn’t typically carry across, so be prepared to start a fresh no claims for your van driving.

Additional FAQ’s

All vehicle quotes were gathered for a 30-year-old male driver living in North West London, who had been driving for 5+ years with no claims or convictions against his name. In both cases, the driver had never worked as a courier previously (0 months self-employed) with no additional forms of employment.

The van used was a 1.6L 2014 Ford Transit Connect with 71,000 miles. The car used was a 1.8L 2012 Toyota Prius with 48,000 miles. Our research indicated both vehicles were popular choices for van/car couriers.

You may be finding that the insurance you require as a courier is significantly higher than your personal vehicle insurance. There are a number of reasons for this. Firstly, courier drivers tend to drive for long hours, and regularly operate on roads they’re unfamiliar with. If you’re using a van for courier services, larger vehicles also typically fall into higher insurance brackets.

Given that courier insurance is also a business insurance (as opposed to social, domestic & pleasure policies you might be used to for your personal travel), coverages like goods in transit or public liability must also be factored into potential costs.

Yes—a few insurers offer policies targeted at couriers only intending to work on a short-term basis, however be aware that many insurers will invalidate your social, domestic & pleasure policy if you’re working as a courier—even if you’ve got temporary courier insurance.

Some providers and comparison websites will take into account your no claims bonus from other/previously registered vehicles, however you can only transfer no claims gained through the same type of vehicle (as an example, 5 years of no claims on a car wouldn’t apply to your first van).

The policies can be separate, however be aware that some personal vehicle insurance providers will invalidate your policy if you haven’t clearly stated you’ll be using your vehicle for both personal and business purposes, irrespective of whether or not you were working at the time of an accident. Some providers will also not consider your insurance valid if you were being protected by a temporary insurance provider (Zego, MCE). Be sure to inform your personal car insurer of your plans and alternative insurance.

Absolutely, but it may take some work to do. Most personal vehicle insurers won't cover courier work. Alternatives would be getting a courier policy that also covers personal driving (and cancelling the existing personal insurance) or getting top up cover for the courier work. But as mentioned above, stay wary that some personal vehicle insurance providers don't like drivers getting top up cover; if you choose to use a temporary courier insurer like Zego or MCE, irrespective of when your accident occurs, they could invalidate your policy. It's critical to inform your existing insurer if you plan to do this, notifying them of your courier job, and getting their approval for your policy.

The market for vans has been popular for much longer, allowing insurers and underwriters to more accurately evaluate risks, costs and driver profiles. Van couriers are considerably more likely to collect and offload goods at designated depots, that have appropriate safety measures in place, compared to car couriers who are more likely to park outside a store/restaurant to collect food/goods. Van couriers are less likely to drive unsociable, late-night hours to collect goods or make deliveries.

Find Courier insurance today.

Powered by QuoteZone.

Get Quotes

- Rated 4.8 out of 5 stars on Reviews.co.uk

- 300,000+ quotes completed per month

- Fill out only one form

Additional Guides

NimbleFins aims to provide a full guide to anyone in the world of courier or delivery drivers. Here's some of our additional guides and research to courier service insurance that may interest you.