Zego Insurance Review: great for flexibility

Zego Insurance Review: great for flexibility

Good for

- 4.6-star Trustpilot rating

- Highly flexible, reasonably priced

- Preferred insurance partner for many top delivery driver firms

- Convenience of documentation, information and customer support through app

Bad for

- 8AM-8PM customer service - not ideal for late night delivery drivers

- Potentially serious coverage issues with many SD&P providers

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Zego has a 4.2 star rating on TrustPilot, however there are some common issues you should know about before signing up. Here, we review the positives and negatives of Zego's car insurance policies.

In This Review

- Zego Car Insurance Features and Review

- Cost breakdown

- Zego reviews and ratings

- How to cancel Zego insurance

- Zego insurance contact number

- Insurance companies that allow Zego

- Zego Just Eat

- Zego taxi insurance

Zego Car Insurance Overall Review

Zego’s car insurance is highly popular with delivery drivers and couriers, and comes with a 4.2-star Trustpilot rating, but there are a number of important potential issues you should be aware of.

Zego’s courier car insurance is a fairly unique product in the UK market, targeted at delivery, courier and car hire/vehicle share drivers and businesses. It offers no strings attached hourly Pay As You Go (top-up) insurance to cover hire & reward work driving, and also 30-day and annual policies that cover both your social and your hire & reward driving.

You should be aware that Zego PAYG car insurance will only match your existing coverage level—therefore if your personal policy only covers you for third party damages (TPO), then Zego will only cover you for this as well. If you're not sure what you will or won't be covered for, you can read more in our explanation of the types of car insurance in the UK

The criteria for getting insured with Zego are not as rigorous as some other providers, some of whom avoid offering coverage to professional drivers/couriers due to the additional risks involved (covered below), and while your quote may change once they’ve conducted background checks on previous convictions and motoring history, if you meet these requirements you have a pretty good chance of being eligible for their policies:

- You have a Full UK/EU driving licence

- You have had fewer than 3 at-fault claims in the past 3 years

- You are aged between 21 and 65 years old

- You live and work in England, Scotland or Wales

- You are the registered keeper or owner of the vehicle

- Your vehicle is valued less than £30,000

- You work for one (or more) of their partnered work providers

How does Zego insurance work?

With the Zego monthly/annual plans that cover both social and delivery insurance, you’re covered any time you’re on the road working with one of their partners.

With the top-up cover, protection generally starts from the moment you log-in to your delivery app of choice and start accepting orders, and stops whenever you log-out or stop accepting deliveries. It's automatic, so you have nothing to worry about, and even if you're working with another provider that isn't partnered with Zego, turning your coverage on and off can be quickly done through their mobile app.

Before and after these times, those with Zego PAYG top-up cover are protected by their existing SD&P policy (assuming the company ishappy for you to work as a courier with Zego’s insurance—more here), so if you need to make a claim, or are involved in an accident, it’s important to remember where your claim needs to go.

When aren’t you covered?

The biggest issue for a lot of Zego PAYG customers comes from the combination of their SD&P coverage and their Zego policy. Some SD&P providers don’t accept ‘additional’ coverage for business/courier purposes, and so you risk voiding your existing SD&P coverage by working as a courier through Zego. We've put together a guide to which of the UK's largest insurers will or won't accept Zego's top-up coverage as valid, which is well worth checking out to make sure you're protected.

There are a number of reasons policy providers reserve the right to do this in their terms and conditions, but many of them will have it in writing so your hands are somewhat tied. The reasoning they do this is explained more in our FAQs.

It’s therefore very important to inform your provider before taking any courier work while protected by Zego to ensure you’re still protected, whether an accident occurs while you’re working or not.

If your SD&P provider is happy for you to use Zego while delivering, then your pay-as-you-go coverage will generally start when you begin accepting delivery requests from your application of choice (Deliveroo, JustEat, Uber etc.). Zego will then check on an hourly basis if you're still accepting requests—if you are, it will extend your coverage for another hour automatically, if you're not, then your Zego insurance will stop.

If you've opted for one of the 30 day or annual policies, then you'll always be covered whenever you're working with one of Zego's partners as they cover both social and delivery driving.

Cost Breakdown

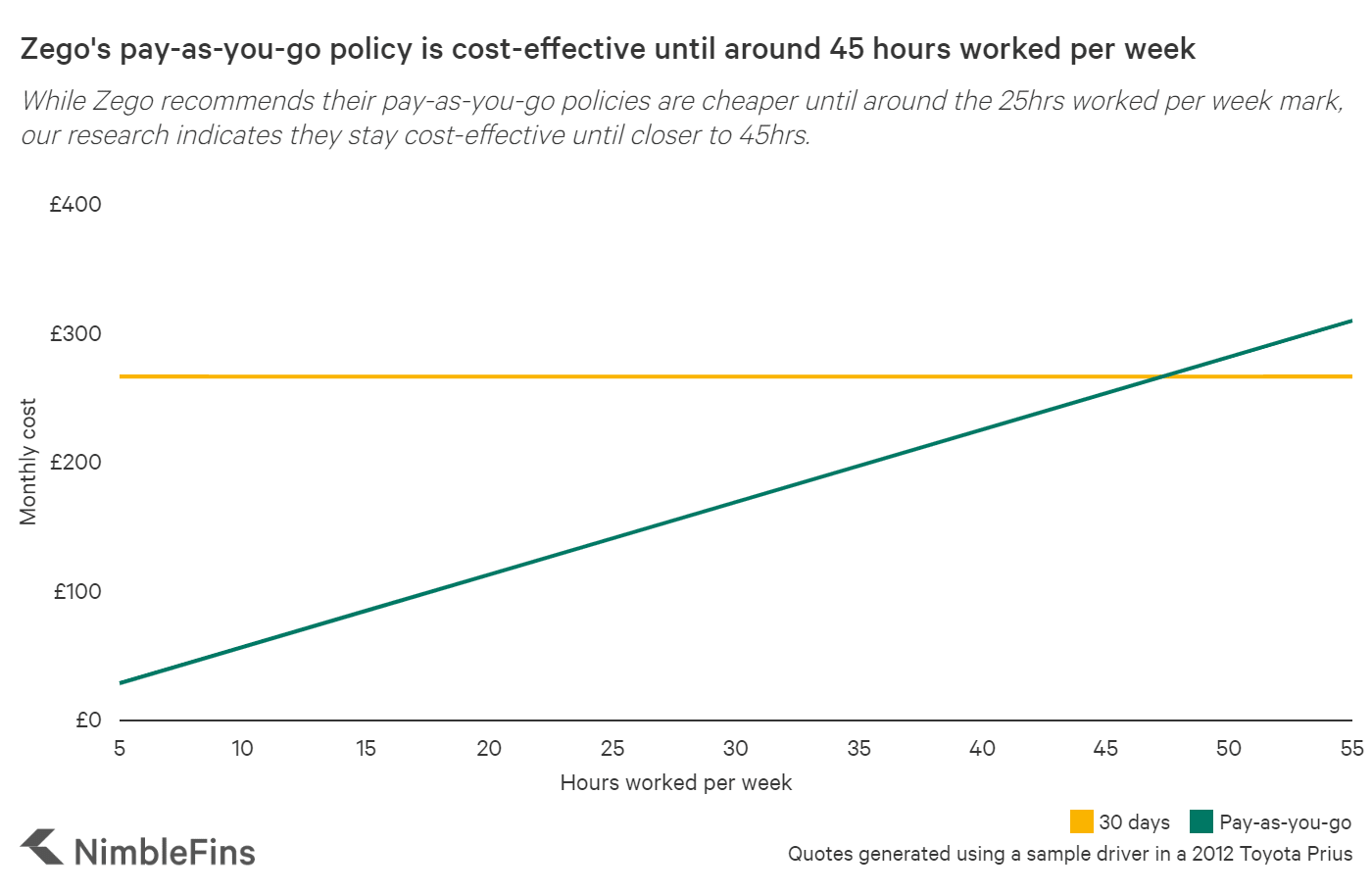

We researched Zego’s different policies against themselves and against other providers to compare what was included and what had to be purchased separately and to work-out which policy would be most cost effective for every type of driver, from part-time, less than 5 hours per week, all the way to full-time drivers working for 40+. Here's the overall breakdown of Zego's car delivery policies and estimated prices for sample drivers.

| Pay-as-you-go | 30-day | ||

|---|---|---|---|

| How does it work? | Pay only when working using your Zego balance | Pay an upfront fee at the beginning of your policy | |

| How much does it cost? | From £0.80—£3.00 per hour | From £90—£350 per policy | |

| What level of cover is provided? | Your Zego coverage will be equivalent to your existing social, domestic & pleasure car insurance policy | ||

Zego recommends its pay-as-you-go policy is more appropriate for those working less than 20 hours per week as a courier—this may be true for some of their policies, but quotes we received for a 2012 Toyota Prius (a popular car among delivery/Uber drivers) indicated that you’d actually need to work over 45 hours per week for the Prius 30-day policy to make more sense (quoted at £1.25 per hour or £266 per month)

Your own break-even point will vary depending on factors like your age, driving record and choice of vehicle. If you'd like to know which is more cost effective for you, simply divide your 30-day quote by your hourly cost to work out how many hours you'd need to work in a month for both quotes to cost the same. If you work any more than that, the 30-day plan is more effective, any less and you're better of paying hourly.

And Zego insurance for scooters and bikes should be even cheaper than the car policies.

Zego Car Insurance Reviews and Ratings

Zego has a 4.2 out of 5 star rating at Trustpilot based on 7,000+ reviews, which implies customers generally have a very positive experience while working with Zego. We should note, however, that their rating has come down from 4.6 when they had around 6,000 ratings, so people may have been having more problems recently. Most of these reviews, however, were in relation to their customer service or signing up process, and were not claims related.

Here are some examples of Trustpilot reviews. Subjects that were regularly mentioned in the 5-star reviews were the ease of signing up, quality of the mobile app and (often despite quite a long wait) excellent customer service/issue handling.

"No chat agents available. No answers to calls. Scam. No response to email. The app rated my driving 93% and yet renewal quote increased by £1000. Trying to rob me! No claims whatsoever. Much much cheaper elsewhere. They do not answer calls. Online chat is permanently UNAVAILABLE..."

"Waiting 2 hours on the phone..."

“Amazing service by Shima after waiting quite long time on the phone, she did excellent job very clear very efficient super quick.”

“..because this is simply and easy insurance. Whenever you work you pay its not fixed like other insurance..”

“Great app so far, nice and easy to navigate”

While Zego’s reviews and ratings are overwhelmingly positive (which is not the norm for insurance companies..), there are certainly some consistent topics that occur regularly in the 1 and 2-star comments. Below are some complaints that come up regularly in Zego’s one-star reviews:

“Over the past 2 weeks zego have been putting (my partner) as working when he hasn't been, he rings zego who sort out the issue for that moment but then it'll sign in again and start taking money saying he is working.”

“..however if you call around you will very quickly realize that none of the insurers will allow or sell their SDP or SDPC insurance if you mention anything about using Zego..”

“Their sales team will do all they can to missell you a policy, even if the policy isn't right for you.

The theme of the criticisms of Zego are fairly consistent—issues with slow response times from their customer service team, problems with using other providers while using Zego’s courier policies and customers feeling they’d been mis sold or not had the full story explained to them.

How to cancel Zego insurance

While you will still owe Zego for any monies outstanding when cancelling, Zego’s style of policy mean this is very rarely an issue for consumers.

Their 30-day/annual policies are non-refundable, so if you sign up for one of these policies make sure you’re fully aware what you’re signing up for, as once you pay for the coverage the money will be gone and your policy will start. Once your policy expires, you're free to either continue the coverage or stop it there, depending on your needs.

Zego’s “pay-as-you-go” coverage automatically tops up when it gets low, however if at any point you wish to close your account, Zego will happily refund you for the full amount held in your account. Section 4.74 of their terms of business states: “Any positive balance will be refunded upon account closure.”

It seems there are no administrative costs for the closing of an account either, which is a massive positive when you consider the average cost to cancel car insurance is around £55 after your 14 day cooling-off period. However, cancelling a contract with Premium Credit (for those who paid monthly) could result in a cancellation fee, but they don't list the size of this fee in their terms.

Zego insurance contact number

| Zego Car Insurance Contact Numbers | Phone Number |

|---|---|

| Customer Services | 020 3308 9800 |

| Get a quote | 020 3053 9815 |

| Claims | |

| Car Flex | 01908 302 023 |

| Car H&R | 034 5300 4006 |

| Windscreen issues | 080 0783 4695 |

| Private hire | 01908 302 023 |

Insurance Companies that allow Zego

Simply put, most of the UK's top insurers will not allow you to take out pay-as-you-go delivery or courier insurance through Zego. While we have an in-depth research piece that is well worth a read if you're not sure, the overwhelming majority of providers will not accept Zego as valid coverage, and may refuse to payout or invalidate your cover in the event of an accident.

| Insurance Company | Offer cover for delivery driving? | Accept top-up/pay-as-you-go cover as valid? |

|---|---|---|

| Admiral |

|

|

| Ageas^ |

|

|

| AXA^ |

|

|

| Aviva |

|

|

| Direct Line^ |

|

|

| esure |

|

|

| Hastings^ |

|

|

| LV |

|

|

| NF Mutual^ |

|

|

| RSA (More Than)^ |

|

|

Question marks indicate an insurer where a NimbleFins reader informed us they were refused cover as a result of Zego after the press office of the insurer informed us that they accepted Zego, or where we did not receive a formal response from the press office after speaking with a sales advisor

Zego Just Eat

Finding good JustEat insurance can be tricky. Many of the UK's top providers refuse to cover delivery drivers, and so you may consider an alternative, like the product offered by Zego. Zego's pay-as-you-go/top-up coverage has proven highly popular with many JustEat delivery drivers.

However, there are a number of issues that could come about from this, as your insurer may not allow you to be 'double insured'. You must check with them before taking out a policy with Zego, to make sure you're not going to risk invalidating your SD&P cover.

Zego Taxi Insurance

Zego's taxi/private hire insurance has proven popular with those looking to use their personal vehicles as a source of income, perhaps with the likes of Uber or Bolt. It comes in two levels - Third Party Only and Comprehensive.

It's a great option for any drivers who have found it difficult to find coverage from traditional providers (perhaps if you've made a claim in the past or are on the younger side), however can create a lot of headaches with your SD&P provider.

Make sure to check with your SD&P insurer before using your car for taxi work to make sure you don't run the risk of invalidating your cover—if they don't allow it, you'll likely need to change providers to an insurer that will.

Is Zego insurance good?

Online reviews for Zego are generally extremely positive, earning them a 4.6-star rating on Trustpilot.

However, those who get the PAYG top-up cover can run into issues if they have had to make a claim with their regular insurance provider, if they didn't allow top-up Zego coverage.

Many SD&P providers don't allow you to double up on your insurance, nor would they usually accept drivers who drive a taxi or courier vehicle. This means if you're involved in an accident while driving for personal reasons your insurer may be within their rights to refuse you coverage (and possibly invalidate your policy altogether).

Going with Zego's monthly/annual social & delivery insurance can alleviate this problem, however.

Zego insurance quotes

Click here to compare quotes from a number of providers including Zego. Otherwise, if you know what you're looking for, you can shop with them directly.

FAQs

You can get a quote from Zego directly from their website; Zego is also part of the courier and delivery driver panel run by our partner QuoteZone, which you can access here to compare prices from multiple providers.

Firstly, most providers will write in their T&C’s that you accept the risk of them voiding the policy if you change the purpose of your vehicle (from personal usage to delivery work) without informing them before doing so.

The reasoning for this is fairly simple, the price you agreed with them for your insurance was based on the mileage expectations of somebody using their vehicle for personal reasons, like drives to the shop or dropping the kids off at school. The extensive miles delivery drivers log on their vehicle leads to additional wear and tear and risk of damage, increasing the chances you’ll need to make a claim—chances that the insurance provider won’t have been able to factor into their original quote for your price.

Zego describes it’s pay-as-you-go payments as similar to an Oyster card or pay-as-you-go mobile phone. You pay a £25 deposit, which is used during your first shifts. Once the balance drops below £5, the account automatically tops up to make sure you’re always covered.

Zego's Hire & Reward delivery driver car insurance is underwritten by RSA. Claims are also handled by RSA. Their claims team is contactable at:

- [email protected]

- 034 5300 4006

There's no singular answer as to why so many of the UK's largest car insurance providers steer clear of offering policies to couriers, but it isn't hard to imagine some of the reasons why insurers might not be interested.

Many of the reasons your SD&P policy can become more and more expensive are the risks delivery drivers are most exposed to—drivers work long, unsociable hours behind the wheel, driving on roads they aren't familiar with, often parking roadside to collect food and goods from restaurants and shops and clocking up a massive annual mileage, around 3x that of the typical British driver in 2020.

You should be able to do this through your Zego app. Simply log into the account you've taken out your coverage through.

If you're on a pay-as-you-go tariff, it shouldn't be more complicated than just canceling payments. You may want to ask Zego to delete your data if you don't intend to return, and would rather not receive marketing from them.

If you're on a monthly tariff, you'll have to wait until the end of the month before your insurance is officially canceled, but after that Zego won't chase you for any outstanding payments (assuming you've gone through the process of canceling your coverage correctly!)