Best Landlord Insurance (June 2024) | Quotes, Costs and Requirements

Find landlord insurance quotes today. Powered by Alan Boswell Group.

Compare Quotes Now

- Reputation. 4.9 out of 5 stars on feefo

- Longevity. 35+ years experience

- Service. Local offices and call centres

- Efficiency. Online quotes in minutes

Find landlord insurance quotes today. Powered by Alan Boswell Group.

Compare Quotes Now

- Reputation. 4.9 out of 5 stars on feefo

- Longevity. 35+ years experience

- Efficiency. Online quotes in minutes

Whether being a residential landlord is a side gig or your primary business, renting out property to tenants can be quite exciting—and a solid source of income. But while it's certainly popular (19% of all households rent privately), being a buy-to-let landlord can be extremely risky. To protect yourself, the right landlord insurance policy can cover (at a minimum) liability claims and repair/rebuild costs if your property is damaged by fire, flood, theft, etc. Here's what need to know, including different types of landlord cover, common exclusions and who needs it.

- Compare Landlord Insurance Quotes Online

- Which landlord insurance is the best?

- What is landlord insurance?

- What to expect when buying Landlord Insurance

- FAQs

Compare Landlord Insurance Quotes Online

Compare landlord insurance quotes online. Simply fill out a quote form with a few details by clicking the blue button below—our partner Alan Boswell sports a 4.9 out of 5 star customer rating and boasts more than 35 years of experience helping landlords find property insurance.

Find landlord insurance today.

Powered by Alan Boswell Group.

Get Quotes

- Reputation. 4.9 out of 5 stars on feefo

- Longevity. 35+ years experience

- Service. Local offices and call centres

- Efficiency. Online quotes in minutes

- Reputation. 4.9/5 stars

- Longevity. 35+ years experience

- Efficiency. Online quotes in minutes

As seen on

Note: commercial landlord insurance is a different product, as it allows for business activities on the premises.

Best Landlord Insurance Companies

NimbleFins has analysed independent customer reviews from Trustpilot and Feefo plus analysed the features on offer to rank 20 of the best landlord insurance providers in the UK. Alan Boswell Group came out on top, boasting the highest customer rating of 4.9 stars and top feature scores for their landlord insurance product. Payment Shield, Just Landlords, LV= and Allianz rounded out the top 5. If you'd like to get a quote from top-rated Alan Boswell Group, click here.

| Best Landlord Insurance Providers | Trustpilot / feefo Rating | Trustpilot / feefo # Reviews | % bad ratings | Best basic policy (100% is best) | Best with add-ons (100% is best) | Overall best policy | |

|---|---|---|---|---|---|---|---|

| 1 | Alan Boswell Group^ (Aviva) | 4.8 | 1,286 | 1% | 87% | 97% | 90% |

| 2 | Alan Boswell Group^ (Covea) | 4.8 | 1,286 | 1% | 80% | 94% | 85% |

| 3 | Allianz | 4 | 290 | 0% | 100% | 100% | 100% |

| 4 | Alan Boswell Group^ (NIG) | 4.8 | 1,286 | 1% | 77% | 90% | 82% |

| 5 | Alan Boswell Group^ (SAGIC) | 4.8 | 1,286 | 1% | 70% | 90% | 80% |

| 6 | LV= | 4.4 | 70,663 | 4% | 70% | 84% | 77% |

| 7 | AXA | 4.6 | 1,435 | 6% | 67% | 84% | 70% |

| 8 | Saga | 4.2 | 38,419 | 7% | 70% | 84% | 77% |

| 9 | Just Landlords | 4.7 | 1,116 | 2% | 53% | 71% | 66% |

| 10 | Let Alliance | 4.8 | 2,721 | 2% | 47% | 68% | 61% |

| 11 | HomeProtect | 4.2 | 16,312 | 11% | 53% | 74% | 67% |

| 12 | Direct Line | 4.5 | 5,926 | 8% | 50% | 71% | 61% |

| 13 | Payment Shield | 4.9 | 5,688 | 3% | 43% | 61% | 52% |

| 14 | Aviva | 4 | 33,875 | 15% | 47% | 65% | 59% |

| 15 | Endsleigh | 3.4 | 3,461 | 20% | 60% | 84% | 69% |

^ Note: We used Trustpilot scores where available. However for Alan Boswell and Homelet we used Feefo scores because more customers had left ratings there than at Trustpilot, and arguably the Feefo scores would be more representative due to higher reporting figures.

What is Landlord Insurance?

Landlord insurance is a package of coverages designed to protect a property that is rented out, since regular home insurance won't work for rental properties. A basic landlord insurance policy typically starts with liability insurance to protect against being sued for injury or damage to a third party (e.g., tenant injury) and landlord building insurance to protect the structure from physical perils like fire, flood and theft.

Depending on your needs, you might want your landlord insurance package to also include additional features. While not all additional features are available from all providers, here are some different types of landlord insurance coverage you can buy:

Types of Landlord Insurance

- Property owners' liability insurance: Protects you financially against liability claims for injury to a tenant or visitor, or damage to their property. Also known as "landlord liability insurance."

- Landlord building insurance: Covers the property structure against damage or destruction due to fire, explosion, flood, theft, vandalism and other risks.

- Landlord contents cover: Protects furniture or furnishings if your rental property is fully or partially furnished (and even carpets and curtains if it's unfurnished).

- Accidental damage: Covers damage due to an unexpected accident (e.g., a tap being left on, accidentally breaking a window, a nail puncturing a pipe whilst hanging a picture, etc.). Can be purchased for the building, contents or both.

- Rent guarantee: Also called tenant default insurance, this primarily covers rent if your tenant defaults (usually for up to six to 12 months). This is the landlord insurance that covers nonpayment of rent.

- Loss of rental income insurance: Covers lost rental income if your tenants are forced to move out because your property becomes uninhabitable due to a peril such as fire or flood.

- Legal expenses: Provides access to an expert legal team and covers legal defence costs in case of contract disputes, debt recovery, property protection and other circumstances related to being a landlord.

Building insurance vs landlord insurance

The main difference between landlord insurance and building insurance is that building insurance for rented properties is a component of a landlord insurance package. Regular homeowner building insurance is not sufficient for a landlord as these policies won't cover properties that are rented out. Rented properties need special building insurance for landlords.

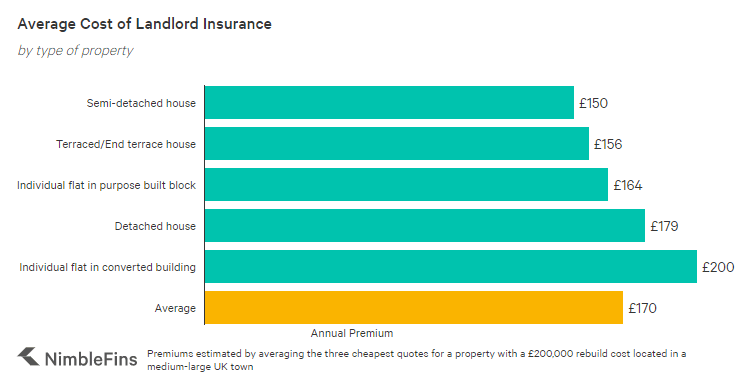

How Much Does Landlord Insurance Cost?

The average cost of basic landlord insurance, including landlord building and liability cover, starts from roughly £170 for a typical one-household UK rental property. This estimate does not include add-on features like accidental damage, contents insurance and rent guarantees, which would increase the cost of landlord insurance. And clearly the cost is higher for larger, more valuable properties, and in some higher-risk areas.

Another factor is the type of building. As you can see below, landlord insurance is different for terraced houses, converted flats, purpose built flats, detached houses, and more. According to our research, semi-detached houses typically cost the least to insure (assuming the same rebuild cost across all property types). These are rough figures estimated for a sample property; your premiums could be higher or lower.

| Landlord Insurance Cost Calculation Estimates | Annual Premium |

|---|---|

| Semi-detached house | £150 |

| Terraced/End terrace house | £156 |

| Individual flat in purpose built block | £164 |

| Detached house | £179 |

| Individual flat in converted building | £200 |

| Average | £170 |

Landlord insurance is typically more expensive than home insurance where the owner lives in the property. This is because a tenant may be less careful with a property than an owner. So accidental damage in particular can be higher for a rented property. Also, landlord insurance might include extra coverages that you wouldn't need with home insurance, such as malicious damage, rent guarantee or legal expenses.

While landlord insurance starts from roughly £170 a year for a typical rented property, prices vary from one property to the next. For example, landlord insurance for an unfurnished flat would usually be cheaper than landlord insurance for a large, furnished house—all else equal. To find out how much you should pay for your property you'll need to get landlord insurance quotes.

Building insurance for landlords costs roughly £170 a year for a typical rented property including public liability for landlords, which you should have as well.

Landlord liability insurance only will cost from around £50 a year. But many providers may be reluctant to sell landlord liability insurance only without building insurance. They are typically sold together.

What Does Landlord Insurance Cover?

Landlord insurance can cover damage to your building, furniture and furnishing, non payment by tenants, and liability. It depends on the specific coverages you buy. Let's look at some examples to see how the different options can work for you.

Landlord Insurance Examples

Here are some examples showing situations where buy to let insurance can benefit a landlord:

- Building cover example: A fire in a residential rental causes major fire, smoke and water damage to your property.

- Building cover example: Freezing temperatures cause a pipe to burst, resulting in a flood that damages the floors of a rental property.

- Building cover example: During an attempted theft, burglars cause severe damage while trying to access the property.

- Property owner liability cover example: A visitor to one of your properties trips on piece of loose carpet, injuring themselves.

- Rent guarantee example: Your tenant losses their job and is unable to pay their rent; and they refuse to leave your property.

- Accidental damage example: A tenant accidentally leaves the bath running when they get an emergency phone call and need to leave home, resulting in flooding.

- Contents insurance example: A fire causes smoke damage in your buy-to-let flat, requiring you to replace the sofa, mattresses, carpets and drapes.

Below we explain the landlord insurance coverage options in more detail with in-depth definitions.

Landlord Building Insurance

Building insurance for a rented property includes, at a minimum, the cost to replace or repair damage to your physical building and things permanently attached to it. Here are items commonly covered by the "building" portion of landlord insurance cover:

- Building

- Permanent fixtures and fittings (e.g., baths, fitted kitchens, wooden or tile flooring, etc.)

- Walls

- Gates

- Fences

- Yards

- Car parks

- Pavements

- Piping

- Ducting

- Cables

- Wires

Building insurance for a landlord might also include "alternative accommodation" coverage—this pays for alternative housing for your tenants if your rental property becomes uninhabitable due to physical damage like fire, flood, explosion or vandalism. If you don't have alternative accommodation cover, you're more likely to want loss of income insurance.

You might want contents insurance even if your properties are let out on an unfurnished basis. Why? Curtains and carpets typically aren't covered by building insurance—but they would be covered by contents insurance.

Risks

What risks does landlord building cover typically protect against? Policies may be written on an "all risk" or "certain risks" basis. An "all risks" policy does what it says and covers all risks, except those specifically excluded by the terms. On the other hand, a "certain risks" policy will specify the perils that are covered—it won't cover risks not spelled out in the policy wording.

Most landlord policies in the UK are written on a "certain risks" basis. While terms and conditions vary by insurer, it's common for the following types of scenarios to be covered by a landlord insurance policy in the UK—subject to conditions, of course:

- Civil commotion

- Earthquake

- Escape of water

- Explosion

- Fire

- Flood

- Lightning

- Malicious damage

- Riot

- Robbery

- Storm

- Theft

Landlord Liability

Property owners' liability protects a landlord if they're sued for causing injury or damage to a third party. If a tenant or someone visiting your property is injured and they claim the building owner is to blame, you could be sued for negligence. A good landlord insurance policy will include landlord liability cover. It may be included for free along with your building cover, but some insurers might require you to pay an extra premium for it. Either way it protects against injury and property damage claims made by third parties (essentially public liability insurance for a rental property). Read more in our full landlord public liability insurance guide.

Landlord Contents Insurance

Building contents insurance for landlords is for protecting household items owned by a landlord such as furniture and furnishings against loss or damage due to fire, theft, flood or other perils. It won't protect against damage like spills, however, unless accidental damage coverage is included.

If you let your properties out on a furnished or partially furnished basis, landlord contents insurance will be more important. That said, even landlords renting out property on an unfurnished basis might want to buy contents insurance, because it also covers carpets and curtains.

Accidental Damage

Accidental damage cover can be added onto contents insurance, building insurance, or both to cover accidents that result in physical property damage. Depending on the insurer and the tier of contents or building cover you buy, accidental damage protection might be included or else it could be sold as an add-on feature to your contents or building cover. It protects against accidental events like:

- Contents accidental damage example: A glass of red wine spilled on a carpet or sofa

- Building accidental damage example: Damage to a door frame when a tenant moves out

- Building accidental damage example: A tenant's child accidentally kicks a ball through a window

Rent Guarantee Insurance

Also called tenant default insurance, rent guarantee insurance covers rental income not received if your tenant stops paying. This could happen if your tenant loses their job or faces other financial difficulties, for example. With average private rents in the UK sitting around £868 a month, the typical landlord has a lot to lose if their tenant can't pay.

Rent guarantee insurance should also cover the costs of eviction if you need to go down that path. Not sure if this will affect you? Read about UK eviction statistics here.

Note: During unprecedented coronavirus times, some insurers have stopped selling rent guarantee insurance. And some landlords with existing rent guarantee policies are finding difficulty claiming.

Loss of Rental Income Cover

If an insured building is damaged and as a result you cannot rent out the property, rental income insurance protects you against the loss of income you experience as a result.

It can also cover the cost of re letting the property and legal fees you incur in trying to avoid or limit the loss of income (e.g., if your property was awaiting sale and you need to cancel the sale due to the damage). Read about the differences between rent guarantee and loss of rental income insurance here.

Legal Expenses Cover

Legal costs insurance provides both access to a legal team and money to pay these experts if you have a contract dispute or need help with debt recovery, among other issues. Property owner legal expenses cover can protect landlords dealing with eviction of a tenant who has defaulted, for instance.

As always, be sure to read the fine print of any insurance contracts before you sign up to be sure you understand what is covered—and what isn't. While we've discussed what is typically covered for landlords in the UK, features, coverages and exclusions can vary from insurer to insurer.

Landlord building and contents insurance frequently will cover malicious damage by burglars, vandals and other people not legally allowed to be on your property. However, policies are less likely to cover malicious damage by tenants. This is sometimes available as an optional add on for which you must pay an extra premium. Read more in our article about malicious damage cover for landlords.

Do I Need Landlord Insurance?

Landlord insurance is not a legal requirement for buy-to-let property owners in the UK, but it can protect a landlord's valuable property asset against fire, flood, theft, attempted theft damage and other perils. Or protect themselves against a liability claim (e.g., if someone is injured at the property). Or protect against a tenant who can't pay rent.

While insurance is not one of the legal landlord requirements, going without cover can be risky. For example, building repair or rebuild costs can reach into the tens or hundreds of thousands of pounds, depending on the damage and underlaying value of your building.

And if you have a mortgage and need the rental income to cover your monthly mortgage payments, then add-ons like tenant default/rent guarantee (e.g., if your tenant doesn't pay) and rental income cover (e.g., if your building is damaged and you cannot rent it out) can be helpful to avoid mortgage default in case of disaster for some landlords.

If you have a mortgage on your property, it's likely that the terms of the mortgage will require you to have a landlord insurance policy in place anyway before you rent to any tenants.

Landlords can benefit from contents insurance, even for an unfurnished property. This is because carpets, curtains and white goods like the refrigerator and washing machine are covered by contents insurance, not building insurance. When deciding if you need contents insurance as a landlord, take into account the cost of these items as well as any furniture or furnishings that you stand to lose if, for instance, there is a fire or flood at your rented property.

A landlord can get a specific form of public liability insurance called property owners' liability or landlord liability insurance. It will protect against personal injury, illness or property damage to a third party that is caused by or linked to a property—injury, illness or damage for which the owner of a property may be liable. It covers both legal defence costs and any compensatory damage the owner is found liable to pay.

Landlord insurance may be required if you have a mortgage on the property, as most mortgages will require that you have suitable landlord insurance in place. Landlord insurance is not required by law but it is usually recommended to cover disasters like fire, flood or personal injury at the property that could leave a property owner exposed to significant financial loss.

What to expect when buying Landlord Insurance

Before calling a provider

Before you call an insurer or broker, think about the possible losses you would want to cover Landlord insurance usually contains public liability and buildings insurance, but it can have your contents, accidental damage, rent guarantee, loss of income, or legal expenses covers added on.

Most landlords are looking at the bottom line when buying insurance, but some of these add-ons can save you thousands in legal fees or lost rent for only a few pounds extra each year – damages or evictions are seldom cheap.

Once you know what kind of risks you want to cover, you will need to determine the rebuild cost of your property. Rebuild is not the same as market value – a rebuild cost should take into account the cost of knocking down any leftover structures after a disaster and building the structure again entirely from scratch.

It’s best to start looking for insurance at least 30-45 days before renewal/start date to make sure you have time to answer insurer queries and review your quote documentation.

During a quote

Be prepared to answer questions about the property history in terms of security, flooding, subsidence, and previous losses. Underwriters will want to know if the property is occupied or not, and whether it is being used for business purposes. Houses with multiple occupants (HMO’s ) are typically hard to insure and cost more – the risks tend to be that much greater.

Brokers can sometimes obtain competitive terms with property portfolios by splitting the properties by use or location – you may be offered two or more quotes with a combined value of less than an all-in-one policy. Be aware that the cost difference may be offset by the additional effort of multiple policies.

After receiving a quote

Once you have your quote, make sure to review it thoroughly - you will need to look through all terms, conditions, clauses and exclusions and contact your insurer or broker to discuss each to make sure you understand what you are being covered for exactly and what is expected of you.

At this stage you can take your proposal form and quote to other insurers/brokers to see if there are better or cheaper options to be had. Be aware that most brokers use the same providers for their landlord insurance – you are best picking a broker you feel offers you a higher level of service.

During the life of your policy

Whichever insurer you choose, make sure to update them to changes in your property occupancy or usage as these happen. This makes sure you have appropriate cover throughout the life of your policy. Lastly, it will ensure you maintain a good relationship with your provider – no insurer likes scrambling to rewrite a completely changed policy at the last minute!

If you're having trouble getting landlord insurance, read about what this might mean and what to do here.

FAQs

At a minimum, landlord insurance would typically cover the rented building against named damages like fire, flood and vandalism, as well as your liability to third parties as a property owner. It can also cover contents, accidental damage, rent guarantees (if your tenant stops paying), loss of rental income (if your property is damaged and can't be rented out) and legal expenses cover. Landlord insurance is largely customisable, depending on what specific coverages you need. That said, some insurers offer a landlord insurance package that includes certain elements of cover.

Landlord insurance can include an element of building insurance coverage; but landlord insurance is different from homeowners' building insurance. If you have regular home building insurance and you decide to rent out your property, your existing building insurance policy will probably not cover you going forward. You'll need to contact your insurer to ask about switching to a landlord policy, or you can find landlord insurance quotes here.

No, landlord insurance does not usually cover tenants' belongings. Your tenant will need to take out their own contents insurance.

When deciding if they need contents insurance, landlords should first consider the value of the furniture and furnishings they own and use in their rental property. Be sure to include the value of carpets and curtains, as these are considered part of contents cover (not buildings). Next, see how much contents insurance will cost you. Contents cover typically costs in the range of £300 a year, but will depend on factors like the amount of cover you need.

Landlord insurance might cover non payment of rent IF your package includes rent guarantee insurance. You'll typically need to pay extra for this coverage, the cost of which will depend on the amount you charge for rent each month.

No, landlord insurance does not typically cover vacancy (e.g., if you're unable to find renters). That said, if you have loss of rental income insurance and your property is vacant because it's temporarily uninhabitable due to physical damage like fire then you might be covered for a period of lost rent.

No, you wouldn't need both a landlord policy and a separate homeowners' building policy. If you decide to rent out your property you'll need to switch to a landlord building insurance policy. You might be able to amend an existing building policy to cover your rental activities; but if your existing building insurance policy won't cover renting out the property then you'd cancel that and buy a separate landlord building policy. If renters aren't allowed on your existing policy, it won't do any good to keep paying for it.

No, landlord insurance is not compulsory or required by law. However, while landlord insurance is not a legal requirement, if you have a mortgage then you are probably required to have a suitable policy in place, or else you'd break the terms of your agreement.

No, landlord insurance is not compulsory or required by law. However, if you have a mortgage then you are probably required to have a suitable policy in place, or else you'd break the terms of your agreement.

It depends on the situation and the tenancy agreement, but generally speaking you would take the cost of repairs for accidental damage out of the tenant deposit; that said, accidental damage cover on your landlord's insurance policy can be used if the damage will cost more to repair than the deposit or if you don't want to take from the deposit.

If you have ACCIDENTAL DAMAGE cover as part of your landlord's insurance policy, this will cover many types of tenant damage. Not all landlord insurance policies include accidental damage cover, and you may need to pay extra to add it. You can get accidental damage for either contents (e.g., the furniture in a furnished property) or the building or both.

However, you might not want to claim on your landlord insurance to cover tenant damage, even if you are covered. Why? When you claim, your premium might go up the next year (and in subsequent years).

As a result, for small damages it might be better to take the cost to make repairs out of the tenant’s deposit instead of claiming from your insurance. However, if you don't want to take from the deposit (e.g., you might want to save the deposit for other issues that arise later) or if the damage costs a lot to repair (e.g., more than the deposit) then you might decide to claim the cost from your landlord insurance.

Many insurance companies will supply a discount when insuring multiple buy to let properties, so be sure to ask your landlord insurance broker or provider if they can offer a discount to you.

A landlord can use landlord insurance to protect against damage to their rental property and liability claims at the very least—these can be catastrophic and lead to significant losses without the right insurance in place.

The landlord pays for building insurance on a rented property, because it's owned by the landlord. The landlord might also pay for contents cover to protect furnishings, window coverings, carpets, etc. But the tenant should buy their own contents insurance to cover their belongings, from furniture to clothing.

To claim on your landlord insurance policy, you'll need to call their claims number, which can be found online or in your policy documents. Once you explain the claim situation, they will instruct you on how to limit any damage and of the next steps. Remember you may have an excess to pay; you can ask about this when you call.

No, you'll need special house insurance for a letting property. Regular homeowners insurance will not typically cover the property if it has been let out to renters.

Many companies sell landlord insurance, such as Direct Line and Aviva, plus you can compare quotes using a search engine like Compare the Market or our partner QuoteZone.

We've found that Alan Boswell, Payment Shield, Just Landlords, Direct Line, Paragon Advance and LV= offer some of the best customer ratings and features in the UK. Customer ratings give an indication of price and service while a study of features indicates the quality of the product. See how these companies compare here.

Methodology

To create the list of the best landlord insurance companies in the UK, we first scoured independent review sources to find companies that had earned at least 3.4 stars from customer reviews. We also dug into policy wordings to find details on product offerings. For landlord insurance, we considered factors like landlord liability, loss of rent, key damage, trace and access, accidental damage, theft by tenants, and more. We have a score for a company's basic policies, that reflects what's included as standard without any additional premiums for extra coverages. We also have a separate score for premium policies, which reflects policies where all of the extra coverages available. The final policy score is an average of the two.

We then ranked them according to a combination of the policy scores and the customer review scores.

There may be other companies that can provide an excellent product and service which did not make this list.

Compare Landlord Insurance

If you want to compare residential landlord insurance online, fill out a quote form by clicking the blue button below—our partner Alan Boswell will analyse your details to connect you with suitable buy to let building insurance providers.

Find landlord insurance today.

Powered by Alan Boswell Group.

Get Quotes

- Reputation. 4.9 out of 5 stars on feefo

- Longevity. 35+ years experience

- Service. Local offices and call centres

- Efficiency. Online quotes in minutes

- Reputation. 4.9/5 stars

- Longevity. 35+ years experience

- Efficiency. Online quotes in minutes