Average Cost of Landlord Insurance (2024)

Compare landlord insurance.

Powered by Alan Boswell Group.

Get Quotes

- Reputation. 4.9 out of 5 stars on feefo

- Longevity. 35+ years experience

- Service. Local offices and call centres

- Efficiency. Online quotes in minutes

- Reputation. 4.9/5 stars

- Longevity. 35+ years experience

- Efficiency. Online quotes in minutes

The cost of landlord insurance starts from an average price of around £170 for no-frills, buildings-only cover for a typical UK property with a £200,000 rebuild cost, according to NimbleFins research.

To find out how much your landlord insurance will cost get quotes from Alan Boswell Group, a broker that provides online quotes (and telephone service if needed for questions or more niche situations) from a variety of insurance providers. Or read more in our landlord insurance guide.

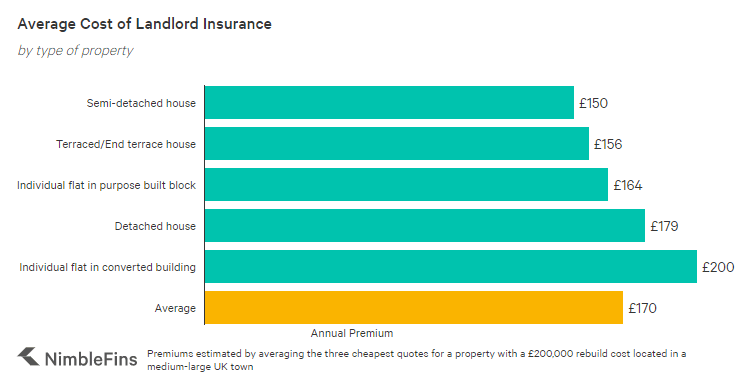

How Much Does Landlord Insurance Cost?

We calculated that the average cost of landlord building insurance is £170 in the UK. This is based on a rebuild value of £200,000, which is the average cost to rebuild a house in the UK. As you can see in the figures below, the type of structure (e.g., terraced house, converted flat, purpose built, etc.) has an impact on landlord insurance costs, with semi-detached houses typically costing the least to insure (assuming the same rebuild cost across all property types).

Compare landlord insurance.

Powered by Alan Boswell Group.

Get Quotes

- Reputation. 4.9 out of 5 stars on feefo

- Longevity. 35+ years experience

- Service. Local offices and call centres

- Efficiency. Online quotes in minutes

- Reputation. 4.9/5 stars

- Longevity. 35+ years experience

- Efficiency. Online quotes in minutes

Prices can vary according to factors like the rebuild value, type of property, the year the property was built as well as optional extras. We ran the numbers on some sample rental properties to learn more about landlord insurance costs in the UK. Here's what we found.

| Landlord Insurance Cost Calculations | Annual Premium |

|---|---|

| Semi-detached house | £150 |

| Terraced/End terrace house | £156 |

| Individual flat in purpose built block | £164 |

| Detached house | £179 |

| Individual flat in converted building | £200 |

| Average | £170 |

What if you let out commercial property?

What about landlords who rent out commercial properties? Prices will vary depending on the type of business that is using your property.

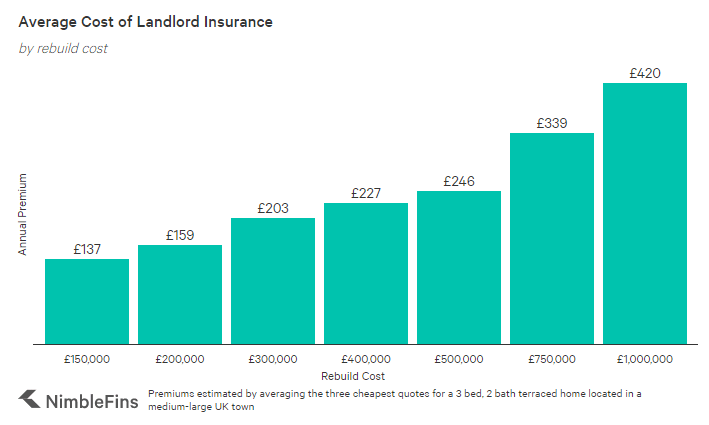

How much is landlord insurance for different rebuild costs?

Another factor affecting a landlord's insurance premiums is the rebuild cost of the building. Properties that cost more to rebuild also cost more to insure, because the insurance company could face larger losses in the event of a claim.

To show how rebuild costs affect landlord insurance rates, we've gathered quotes for a typical 3 bed, 2 bath terraced property according to different rebuild costs (e.g., sum insured). Landlord insurance quotes ranged from £137 for a £150,000 rebuild cost up to £420 for a property with a £1,000,000 rebuild cost. While you may pay more or less, the calculations show how rebuild cost affects landlord insurance costs.

Note: rebuild cost is simply the amount of money required to rebuild a building if, say, it is damaged beyond repair in a fire. The rebuild cost differs from the property value, which will be higher and reflect a local area's real estate prices as well as the size and value of the land.

| Landlord Insurance Costs, based on Rebuild Cost | Annual Premium |

|---|---|

| £150,000 | £137 |

| £200,000 | £159 |

| £300,000 | £203 |

| £400,000 | £227 |

| £500,000 | £246 |

| £750,000 | £339 |

| £1,000,000 | £420 |

The prices above reflect commercial building insurance costs, which can be useful for landlords and owner/occupiers. If you occupy your property, you'll also want to consider additional coverages, like public liability insurance, which would increase the overall cost of your business insurance.

How much is landlord insurance for homes of different ages?

It may not be a surprise, but older properties cost more to insure. In fact, we found that a property built in the 19th century would cost around 19% more than a building constructed in the 21st century. This is due to a variety of factors, such as older buildings costing more to make right in the event of damage or because newer properties might have better safety standards (e.g., security, fire standards, etc.)

| Landlord Insurance Costs, by Year Built | Estimated Annual Premium |

|---|---|

| Before 1850 | £167 |

| 1850 - 1899 | £166 |

| 1900 - 1920 | £159 |

| 1921 - 1944 | £159 |

| 1945 - 1979 | £156 |

| 1980 - 1989 | £146 |

| 1990 - 2000 | £143 |

| After 2000 | £141 |

How much are extra coverages for a landlord?

In addition to no-frills building insurance, a landlord might want to add extra coverages such as accidental damage, contents cover, legal expenses and home emergency cover. While the costs will vary depending on the exact coverage provided, value of the property, etc. we've gathered sample quotes to give you an idea of premiums for these extra coverages to help you budget and spot a good deal when you see one.

| Optional Extra Coverages for Landlords | Annual Premium |

|---|---|

| Accidental damage (building only) | £299 |

| Legal expenses (£50k of cover) | £40 |

| Tenant default/Rent guarantee (£12k to £50k of total cover) | £46 to £100+ |

| Home emergency (boiler, heating, electric) | £144 |

| Landlord's contents (£5k of cover) | £290 |

| Landlord's contents (£10k of cover) | £303 |

| Landlord's contents (£20k of cover) | £321 |

Add-on coverages like contents and rent guarantee insurance (which covers lost rental income if your tenant stops paying and can cover eviction costs as well) are dependent upon the amount of cover you need; home emergency cover costs will vary depending on the level of cover provided (e.g., heating only, heating & electrics, etc.).

What Affects the Cost of Landlord Insurance?

While rebuild cost is seen as the most obvious factor affecting the cost of a commercial building insurance quote, there are actually many factors at play. For example, an insurer might charge more to cover a home that is rented to many unrelated adults (a house share)—particularly if 3 or more adults share a property.

An insurer takes into account dozens of details in an application to determine the potential risk—and consequently the price they'll charge for cover. Here are a few factors that can have a significant impact on your commercial building insurance quote:

- Rebuild cost

- Year built

- If property is unoccupied or occupied

- Construction materials

- Type of occupancy (commercial only, residential only or mixed-use buildings)

- Type of building (e.g., purpose built, listed property, etc.)

- Type of tenants (e.g., employed, student, house shares, housing associations, Local Authorities, etc.)

- Number of properties being covered

- Add-on coverages (e.g., accidental damage, cover for fixtures and fittings, tenant default, rental protection, home emergency cover)

- If there are any building or renovation works in progress

- Location

What to look out for: When buying a landlord insurance policy, it's a good idea to have property owners' liability insurance in place—this provides financial protection if you're found liable for injury to a tenant or visitor or damage to their property. For example, if someone trips on a loose bit of carpet and falls they could sue you for negligence. Even if a claim is frivolous you might incur legal expenses defending the claim. And if you are found liable, you might need to pay compensation. Liability insurance can cover these costs.

What Checks Should You Carry Out?

Your insurance company is likely to ask what types of checks you've carried out on your prospective tenants, for instance:

- Background and identity checks

- Independent references

- Credit checks on prospective tenants or their guarantor

How Can You Save Money on Landlord Insurance?

If you're short on time, getting quotes from a broker or using a comparison engine (e.g. broker Alan Boswell or comparison engine QuoteZone) can save you precious time and money. Prices can vary tremendously from insurer to insurer, so getting multiple quotes will help ensure that you pay a market-based premium, and not more.

In our research, we found that the most expensive property insurance premiums can cost 13X as much as the cheapest quotes, or even more—for very similar cover. Why are some insurers so much more expensive? Each insurer has their own pricing model, and calculates risk differently. Prices can even change from one insurer from day to day—which is why a renewal price can be so much higher. This can occur if, for instance, an insurer decides they have enough exposure to a certain industry—at which point their prices can rise considerably.

Here are some ways to save on your business building insurance:

- Compare the market for a range of quotes before you buy

- Pay annually instead of monthly to avoid interest charges

- Discounts can sometimes be found for buying online (vs. on the phone) or purchasing all your coverage from one place

- Optional extras can be useful, but only if you need them

- Keep your property well maintained to help avoid situations that can lead to a claim, which can subsequently increase your insurance premium

- Consider the excess (the amount you pay towards claims) because a higher excess can lead to a lower premium

- Securing your property can reduce the likelihood of a burglary (e.g., using a mortice deadlock, a mortice deadlock conforming to BS3621, a key-operated multipoint lock or a rim automatic deadlatch with key-locking handle on doors and having windows either screwed shut or secured by locks with a removable key)

FAQs

Home emergency cover for a landlord typically costs around £145 a year (£12 a month) to cover boiler and central heating breakdowns, burst pipes and electrical failure. Cheaper cover can be found from around £9.50 a month if you only cover the boiler.

Yes, landlord insurance is usually more expensive than home insurance. Why? It boils down to risk. For starters, tenants are typically less inclined to take good care of a property than the owner, which can affect accidental damage coverage in particular. Another reason is that landlord insurance typically includes landlord's liability insurance, which protects against claims of accidental injury to tenants or visitors, or damage to their property.

Landlord insurance for a typical 3-bed, 2-bath property in the UK with a £200,000 rebuild cost would incur an annual premium around £170 for building-only cover—that's roughly £16 a month for landlord insurance, depending on the interest rate charged for paying monthly.

Methodology

We sourced prices from a few large, popular UK landlord insurance companies for our research. You may need to pay more or less than the figures shown above depending on the particulars of your application and the insurance company you ultimately use to insure your property.

Note: the quotes we received all reflect a minimum level of property owner liability insurance (£2 million), which will act like public liability cover. Landlords can be found liable for injury to a tenant or visitor or damage to their property. You could be responsible for paying compensation claims plus legal costs. You could be responsible for legal costs even if a claim is frivolous. And if you're found liable you could also have to pay the other side's legal fees.