The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Average Cost of Commercial Building Insurance UK (2024)

Get Commercial Property Insurance.

Powered by Alan Boswell.

Compare Quotes

- Reputation: Rated 4.8 out of 5 stars on Feefo

- Longevity: 35+ years experience

- Service: Local offices and call centres

- Efficiency: Online quotes in minutes

Get Commercial Property Insurance.

Powered by Alan Boswell.

Compare Quotes

- Reputation. Rated 4.8 out of 5 stars on Feefo

- Longevity. 35+ years experience

- Service. Local offices and call centres

- Efficiency. Online quotes in minutes

Not surprisingly, the cost of commercial building insurance is incredibly variable. For example, a small shop would clearly be less expensive to insure than a large manufacturing complex. To learn more about how much it costs to insure a commercial building, we've run the numbers on some sample rebuild costs and popular UK businesses. Here's what we found.

- Average commercial building insurance costs, by rebuild value

- Business building insurance costs, by trade

- Why is my commercial building insurance so expensive?

- How to save money on commercial building insurance costs

How Much does Commercial Building Insurance Cost?

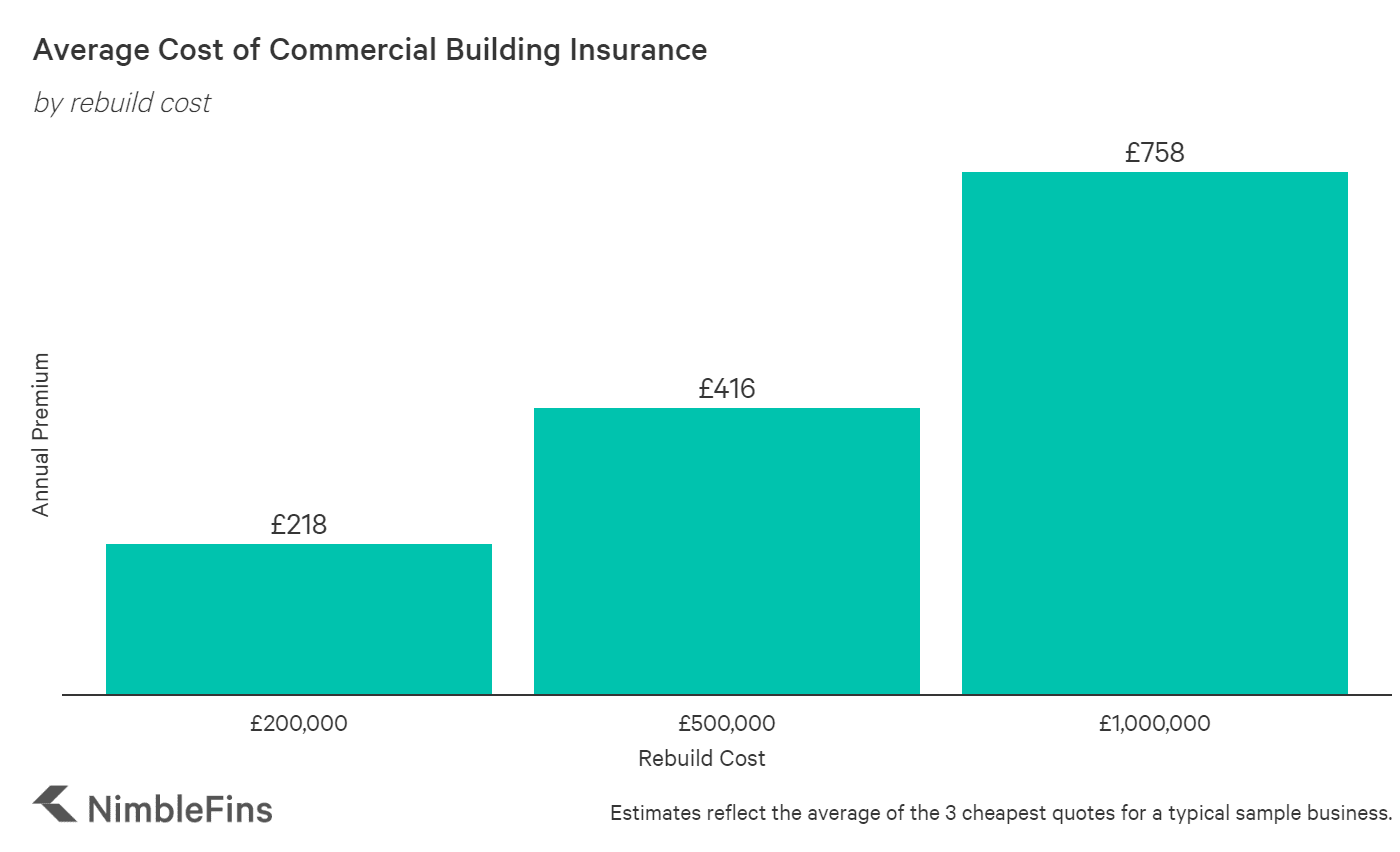

Commercial building insurance costs can be found for around £218 to insure a typical small business property in the UK with a £200,000 rebuild cost. However, properties that cost more to rebuild also cost more to insure. For example, a commercial building with a £500k rebuild cost would probably be around twice as much to insure.

Here are some sample prices to reflect different commercial property rebuild costs. While the calculations in real life will vary according to many factors, you can use this information as a rough guide to what you might need to pay.

| Commercial Building Insurance Calculator Estimates | Get Quotes | |

|---|---|---|

| £200,000 rebuild cost | £218 | Get Quotes |

| £500,000 rebuild cost | £416 | Get Quotes |

| £1,000,000 rebuild cost | £758 | Get Quotes |

The prices above reflect commercial building insurance costs, which can be useful for landlords and owner/occupiers. If you occupy your property, you'll also want to consider additional coverages, like public liability insurance, which would increase the overall cost of your business insurance. Landlords can learn more about insurance they might need here.

What type of business occupies your commercial property?

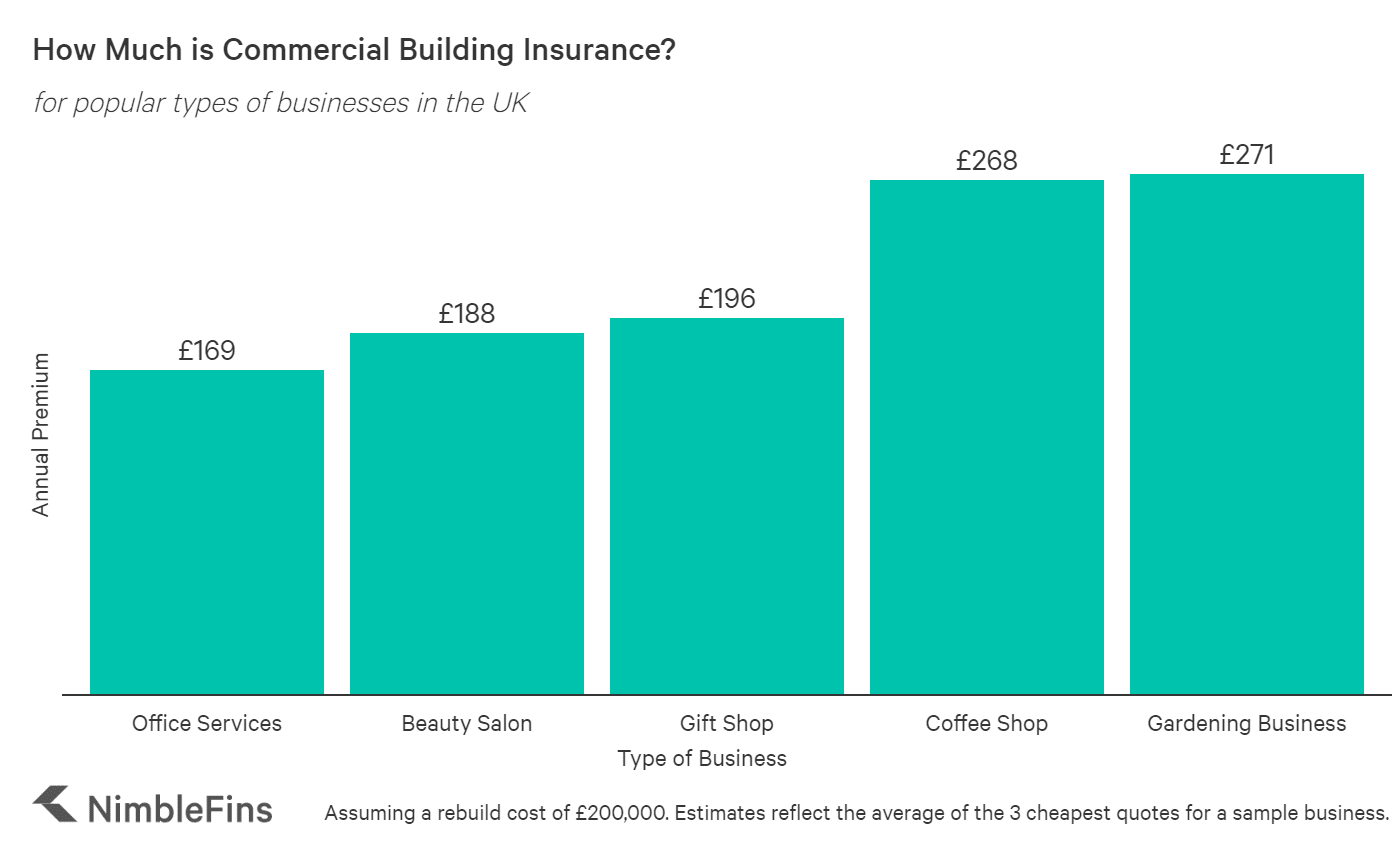

Commercial building insurance costs also depend on the type of business that occupies your property. This is because some businesses are inherently riskier than others. For example, a gift shop will have less chance of fire than a restaurant. Here are average sample quotes for some popular UK small businesses so you can see how prices vary.

| How much is small business building insurance? | Compare Quotes | |

|---|---|---|

| Office Services | £169 | Get Quotes |

| Beauty Salon | £188 | Get Quotes |

| Gift Shop | £196 | Get Quotes |

| Coffee Shop | £268 | Get Quotes |

| Gardening Business | £271 | Get Quotes |

What Affects the Cost of Commercial Building Insurance?

While rebuild cost is seen as the most obvious factor affecting the cost of a commercial building insurance quote, there are actually many factors at play. For example, an unoccupied building can cost more to insure than an occupied building—with no occupants, there's a higher risk of damage from an unnoticed flood, for instance.

An insurer takes into account dozens of details in an application to determine the potential risk—and consequently the price they'll charge for cover. Here are a few factors that can have a significant impact on your commercial building insurance quote:

- Rebuild cost

- If property is unoccupied or occupied

- Non-standard construction

- Type of occupancy (commercial only, residential only or mixed-use buildings)

- Number of properties being covered

- Add-on coverages (e.g., business interruption/rental income protection, accidental damage, cover for fixtures and fittings, tenant default, building emergency cover)

- If there are any building or renovation works in progress

- For culinary businesses: if you have a deep fat fryer

- Location

How to Save Money on Commercial Building Insurance

One of the easiest ways to save money on commercial building insurance is getting multiple quotes. In our research, we found that prices could vary as much as 1200% or more between the most expensive and the cheapest quotes.

Why do prices vary so much? Each insurer has their own pricing model, and calculates risk differently. Prices can even change with one insurer from time to time. This can occur if, for instance, an insurer decides they have enough exposure to a certain industry—at which point their prices can rise considerably.

Besides comparing the market for quotes (e.g., by using a broker or a comparison engine), there are other ways you can save on your business building insurance. Here are some ideas:

- Compare the market for a range of quotes before you buy.

- Pay annually instead of monthly to avoid interest charges that can exceed 20% APR.

- Be thoughtful about the optional extra coverages you really need.

- Keep your property well maintained to help avoid situations that can lead to a claim, which can subsequently increase your insurance premium

- Consider the excess (the amount you pay towards claims) because a higher excess can lead to a lower premium

- Secure your property well to reduce the likelihood of a burglary (e.g., using a mortice deadlock, a mortice deadlock conforming to BS3621, a key-operated multipoint lock or a rim automatic deadlatch with key-locking handle on doors and having windows either screwed shut or secured by locks with a removable key)

FAQs

Commercial building insurance protects a building used for commercial purposes (e.g., a shop, cafe, restaurant, etc.) against the financial repercussions of damage due to risks like fire, flood and theft.

Usually it's the building owners who would pay the building insurance. However a commercial tenant would need to buy their own business contents insurance. Learn about commercial contents insurance costs here.

Methodology

We sourced prices from a few large, popular commercial building insurance companies for this study. You may need to pay more or less than the figures shown above depending on the particulars of your application and the insurance company you ultimately use to insure your property.

Note: the quotes we received all reflect a minimum level of property owner liability insurance (£2 million), which acts similar to public liability cover. Why is this important? Landlords can be found liable for injury to a tenant or visitor or damage to their property. For example, someone trips on a loose floorboard on the stairs and falls, becoming seriously injured.

As a result, you could be responsible for paying compensation claims plus legal costs. You could be responsible for legal costs even if a claim is frivolous. And if you're found liable you could also have to pay the other side's legal fees. Property owner liability insurance helps protect against these financial losses.