Compare Construction Insurance | NimbleFins Quotes & Requirements

Find construction insurance today.

Powered by QuoteZone.

Compare Quotes

- Rated 4.7 out of 5 stars on Reviews.co.uk

- Over 300,000 QuoteZone quotes completed per month

- Fill out only one form

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

As seen on

Construction Insurance UK

You never know what’s around the corner in the construction industry, and the risks you face on a daily basis can have detrimental impacts both to you and your clients. You’ll need a robust insurance policy to make sure you’re covered from every angle.

This article will cover everything you need to know about the different types of cover you might be interested in whether you run a large construction company or you're self employed. We also offer a unique insight into the costs you might expect to pay. If you’re interested to know what a quote might look like for your business, take a look at our quote form to receive no-strings-attached quotes from some of the best UK providers of builders insurance.

- What insurances are popular for construction companies?

- How much does construction insurance cost?

- Where can I get construction insurance quotes?

- Construction industry statistics

- FAQs

Homeowners looking for information on what insurance a construction company should have before starting work, as well as how doing renovation work can impact their own home insurance, can click here for more information.

Popular Types of Insurance for Constructors

The wide variety of insurances on offer to UK builders/construction companies are designed to protect your business if something goes wrong. Each type of insurance offers its own unique coverage, and this article will explain everything you need to know about each one. Here's construction insurance explained:

Public Liability Insurance

Construction public liability insurance (or just construction liability insurance) protects against claims for injury, damage or medical expenses from members of the general public. They might include (but aren’t limited to) your client, other businesses on-site, local residents or just people passing by.

Your public liability insurance will cover any compensation a court awards against your business, and any legal expenses you incur during the dispute, giving you full protection in the event of a mishap. And while not required by law, all good construction firms will hold a liability policy—and most of their clients wouldn’t hire them without one.

You’ll often find public liability packaged together with product liability, which protects you similarly for injury or damages if a claim is made after your work is completed—say, if a poorly installed carpet causes someone to trip and hurt themselves. Together, they can protect your staff and your work from any claims whether you’re on-site or the work is complete.

In terms of construction liability insurance cost, a basic £2M public liability policy for a small company will start from around £100-£110.

Public Liability Examples:

- One of your employees leaves a poorly placed toolbox in the middle of a walkway. An employee from another business trips and falls over it, hurting themselves. They’re unable to work for 2 weeks, and sue your business for their lost wages.

- While walking through a client’s home, you turn a corner with your ladder and damage their walls. They sue you for the cost of the repair.

Employers’ Liability Insurance

Employers' Liability is a legal requirement for any construction company that hires employees. Whether they’re full-time, part-time, contractors or temporary, you’ll need Employers’ Liability before you bring them on board. It protects your business from legal cases in the event that a member of staff is injured or becomes unwell as a result of having worked for you.

As of 2026, construction has officially climbed to become the 2nd most dangerous industry in the UK for non-fatal injuries, trailing only the accommodation and food service sector. According to the latest 2024/25 Health and Safety Executive (HSE) figures, the industry sees approximately 2,500 injuries per 100,000 workers—a stark reminder of the high-risk environment.

Consequently, the fines for lacking Employers’ Liability insurance remain severe, at up to £2,500 per day for every uninsured worker. With HSE enforcement focusing heavily on high-risk sectors this year, having a robust policy in place is a non-negotiable legal and financial priority.

- Employers’ Liability Example: Your employee trips and falls over an exposed piece of wiring while on-site with you. He can’t work for 3 weeks, and so sues you for his lost wages and medical expenses.

Professional Indemnity Insurance

Professional Indemnity (PI) insurance protects construction firms against claims of professional negligence, such as design errors or faulty specifications. After years of a 'hard market' following the Grenfell tragedy, 2026 marks a significant 'reset' in the sector. Insurer capacity has finally expanded, leading to more competitive rates and a gradual easing of fire safety and cladding exclusions.

However, this softer market comes with new strings attached: underwriters now demand strict compliance with the Building Safety Act 2022 and often require specific governance policies for firms using Artificial Intelligence (AI) in generative design or project modeling. If your firm provides design-and-build services, proving your 'regulatory resilience' is now the key to unlocking the best PII rates.

- Professional Indemnity Insurance Construction Example: You’ve finished an extension to a client’s house, however there’s an issue with the roof, which leaks when it rains. The client brings in another company to fix the issue, and sues you for the additional work and any water damage to their property.

Personal Accident Insurance

Especially relevant in an industry as risky as construction, personal accident coverages protect you and your employees if an injury or illness puts them out of action. They typically come under two core categories—personal accident coverages, which will generally protect you in the short-medium term (c.1-2 years), and critical illness, which offers financial support in the event you’re unlikely to return to work for the foreseeable future.

Personal accident coverage is an attractive benefit to many employees in the construction industry, who might not have their own or company coverage, so keep it in mind if you might like to attract better talent.

- Personal Accident Example: An employee of yours hurts their back while lifting a ladder, and a doctor says they can’t return to work for 2 weeks. Your insurance policy pays them 50-70% (typically) of their income for the 2 weeks.

- Critical Illness Example: You lose vision in one of your eyes due to an accident at work, and aren’t able to return in the near future. You’re paid out a one-off, lump-sum settlement to help keep you covered.

Tools and Plant Insurances

Tools and plant coverages allow you to protect your equipment wherever it is, whether on-site, in a vehicle or in your business premises. There’s a wide variety of different options available, and your insurer should be able to quickly deduce what you’ll need and what you won’t.

Some insurers may ask whether you want to include coverage for owned tools/plant, rented tools/plant or both, so consider which might work best for you.

Business Use Vehicle Insurance

If you use a personal vehicle for business purposes, such as transporting tools to a client’s site, you’re legally required to hold a form of business use vehicle insurance. If it’s your personal vehicle, then the process is fairly easy—you can contact your existing provider and tell them you’d like to upgrade, and most UK providers will be more than happy to support you—although don’t be surprised if your premium goes up.

If you use your vehicle to move expensive tools from one site to the next, you may want to consider goods in transit insurance, which will protect your tools if they’re damaged while they’re on the move. And if you have vehicles that are registered to your company’s name then you’ll need commercial vehicle insurance to keep them, and your business, insured.

Construction All Risk Insurance

Construction all-risk insurance (also referred to as ‘contractors all-risk insurance’, 'building site insurance' or 'builders contractors insurance') is a policy designed to cover all the risks you might encounter during a construction project.

These can include, but aren’t limited to:

- Public Liability

- Tools and Plant (whether hired or owned)

- Movement of machinery/Goods in Transit

- Professional Indemnity

- Employers’ Liability

- Product Liability

- Contract Works

Your insurance provider will be able to create a plan that works best for you depending on the projects you’re working on. For larger projects, you may find that both you and the property developer are named on the policy—this allows the developer to claim against the insurance for damages caused by the construction company, most relevant once they’ve left the site, and the insurance is still liable (not the constructor).

What Insurance Does a Self Employed Construction Worker Need?

Most of the coverages mentioned above can still be valuable if you’re looking for construction contractor insurance. Some of them might already be offered by your employers, even if you’re only going in as a contractor, so check with each employer before signing up to work out what you might need.

| Common Types of Construction Insurance | What it Covers | |

|---|---|---|

| 1 | Public Liability | Damages against members of the general public |

| 2 | Employers' Liability | Claims by employees for injury or illness |

| 3 | Professional Indemnity | Professional negligence |

| 4 | Tools and Equipment | If your tools are stolen or accidentally damaged |

| 5 | Personal Accident/Income Protection/Critical Illness | Income support if you’re out of work |

| 6 | Business Use Vehicle | Insures your vehicle for business purposes |

| 7 | Product Liability | Something you’ve supplied (item, project) causes damages after the event |

Do Construction Workers and Companies Need Insurance?

Almost certainly. If you’re working as an employee at a company, you should check what’s already being provided (coverage like public liability and professional indemnity should definitely be in place) but you may find that you’re responsible for covering damages to your own tools, or don’t have any personal accident cover available.

Most in the industry would probably say that public liability as an absolute must, and most clients won’t consider working with you if you don’t have an active policy when bidding for work. It’ll provide insurance during construction if a member of the general public incurs damages as a result of your work. Considering that the average settlement in 2019 was £13,500, and policies start from as low as £104 per year, it’s not worth taking the risk of working uninsured.

Professional indemnity is worth looking into for any business working on large-scale, complicated projects where mistakes can be costly, especially where you provide an expert or technical service to the project. It’ll cover the cost of compensation in the event a client thinks you’ve been professionally negligent, whether you’ve made a mistake, there was a misunderstanding or the client is simply unhappy with what you’ve done, and claims against you to pay for the redo of your work.

Employers’ liability covers you against claims made by those employed by your business and is a legal requirement if you’re hiring anybody, even if they’re only joining you for a short time (even just one afternoon!). It’ll protect your business from claims if your employee is hurt or becomes sick while working for you.

And similarly, if you’re using your vehicle to support your business, then business use vehicle coverage would be required by law to protect you against the additional risks of driving for business purposes, such as the additional mileage and often unfamiliar roads. Remember that failure to obtain the appropriate cover risks voiding your entire policy.

Tools, plant and equipment insurances will help keep your work moving forward if any of your equipment is stolen, lost or damaged outside of your control. Consider it especially if you have expensive or specialist tools that could prove difficult to replace. If you’re using your vehicle to take your equipment from A to B, a goods in transit policy can help protect the equipment in case of theft or damage in an accident.

Income protection can offer a security net for you and your employees in the event that they’re unable to work due to illness or injury. You can consider both shorter term income protection and long-term critical illness policies to create a well-rounded coverage for your company.

Finally, if you’d like a policy that takes care of most of your on-site risks during a project, consider a construction all risk policy to make sure your business ticks all the insurance boxes required before taking on a big piece of work. It can be the most convenient and well-rounded way to provide insurance for a construction site, but be sure it includes all the coverages you need for your unique situation.

Pick the combination of coverages you like the sound of to build your policy. Hopefully this answers the question of "what insurance do I need for construction?".

How much does Construction insurance cost?

Sole Trader

The most notable increase in cost for a sole trader is the additional cost of bringing on an employee. The mandatory employers' liability and additional head on the personal accident coverage adds just over £500 to the annual cost of your insurance, so if you're going to bring somebody in for a short time period consider the additional costs.

| Average Cost of Construction Insurance for a sole trader | |

|---|---|

| £2m Public Liability (PL) | £104 |

| £5m PL | £139 |

| £2M PL, £2,000 Tools (not left in van overnight) | £184 |

| £2M PL, £2,000 Tools (left in van overnight) | £203 |

| £2M PL, £10,000 Tools (left in van overnight) | £660 |

| £2M PL, Personal Accident | £211 |

| £2M PL, Personal Accident, £2,000 Tools (left in van overnight) | £309 |

| £2M PL, 1 Employee, £2,000 Tools, Personal Accident | £810 |

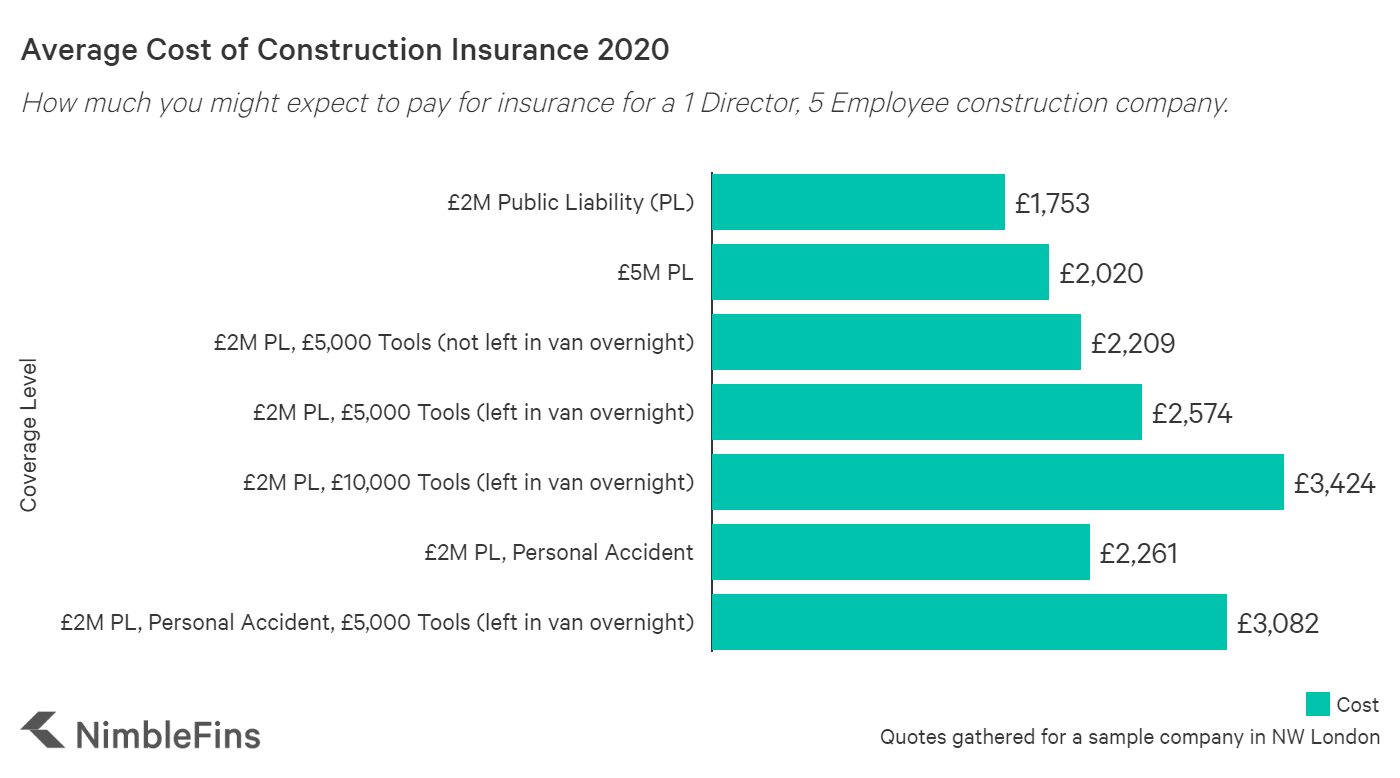

6 Person Limited Company

The price increase of moving from being a sole trader to a small limited company is driven by a number of different factors, such as the additional employers' liability, the additional heads on the Personal Accident policy and the increased chances of mistakes or damages occurring (6 people are more likely to make an error than one!).

| Average Cost of Construction Insurance for a limited company with 1 director and 5 employees, working in residential and commercial locations | |

|---|---|

| £2m Public Liability (PL) | £1,753 |

| £5m PL | £2,020 |

| £2M PL, £5,000 Tools (not left in van overnight) | £2.209 |

| £2M PL, £5,000 Tools (left in van overnight) | £2,574 |

| £2M PL, £10,000 Tools (left in van overnight) | £3,424 |

| £2M PL, Personal Accident | £2,261 |

| £2M PL, Personal Accident, £5,000 Tools (left in van overnight) | £3,082 |

11 Person Limited Company

The price increases here again represent the additional risk of having more employees and the extra employers' liability required. The risk profile of the company begins to shift, as insurers know larger companies tend to work on larger, more complicated projects, and so the additional costs do not increase linearly.

| Average Cost of Construction Insurance for a limited company with 1 director and 10 employees, working in residential and commercial locations | |

|---|---|

| £2m Public Liability (PL) | £2,943 |

| £5m PL | £3,359 |

| £2M PL, £5,000 Tools (not left in van overnight) | £3,748 |

| £2M PL, £5,000 Tools (left in van overnight) | £4,543 |

| £2M PL, £10,000 Tools (left in van overnight) | £6,274 |

| £2M PL, Personal Accident | £3,790 |

| £2M PL, Personal Accident, £5,000 Tools (left in van overnight) | £5,390 |

How can I save money on construction insurance?

- Tool storage: You’ll be able to save up to 40% (or more) on your tools coverage if you leave your tools in a secure lockup overnight.

- Experience: More experienced constructors pose less risk to insurer and so can be covered for less

- Gather Quotes: Comparing providers will help you to get the best value possible for you and your business

- Location: Some locations pose more risk than others—expect to pay more if you work near power stations, airports or harbours.

- Avoid Risk: You can expect to pay more for more risky construction work. This might look like:

- Working at heights over 10 metres

- Working at depths below 1 metre

- Using explosives or carrying out demolition work

- Disposing of dangerous items such as fumes, toxins or asbestos

- Working while suspended from cables/ropes

Where can I get Construction insurance quotes?

Compare construction insurance quotes here using a search engine powered by our partner QuoteZone—fill out a short form and quickly receive quotes from 5 providers, and easily speak to someone if you still have any more questions. Then, simply choose the package that works best for you at an affordable price to keep your business safe.

Powered by QuoteZone.

Find Construction insurance today.

Get Quotes

- Rated 4.8 out of 5 stars on Reviews.co.uk

- 300,000+ quotes completed per month

- Fill out only one form

Using an aggregator like QuoteZone can be the quickest way to compare quotes from a variety of providers. Otherwise, you could speak to a broker or go directly to an insurer you think could help.

Builders Pay and Market Statistics

Anaylsis of data from the ONS shows that the national median salary for full-time employees in the construction sector has seen robust growth due to acute skills shortages, with the UK national average reaching £39,039 (up 4.3% from the previous year).

| Region | Average Salary (2025/26) |

|---|---|

| National Average | £39,039 |

| Wales | £34,050 |

| North East | £34,800 |

| West Midlands | £35,950 |

| North West | £36,100 |

| Yorkshire and The Humber | £36,333 |

| Scotland | £37,100 |

| East Midlands | £37,210 |

| South West | £38,150 |

| East | £38,620 |

| South East | £39,850 |

| London | £42,500 |

Workplace Injury Statistics

| Industry (Main Sector) | Rate of Non-Fatal Injuries (per 100,000 employees) |

|---|---|

| Agriculture, forestry and fishing | 4,250^ |

| Accommodation and food service activities | 3,080 |

| Construction | 2,500 |

| Transportation and storage | 2,430 |

| Wholesale and retail trade; repair of motor vehicles | 2,070 |

| All-industry average | 2,070 |

^Note: Agriculture figures for 2025 are based on a 3-year average (2022/23–2024/25) as single-year reporting for this sector is often statistically volatile.

As demonstrated by the table above, workplace injuries are very common within the construction industry. This is one of the key reasons why some of the insurances mentioned above can be such a valuable asset to a business, protecting you against injury claims from your own employees (through mandatory employers’ liability) and from other third parties (through Public Liability), You can also help to protect your employees income in the event they’re hurt outside of work or due to the fault of a third party with Personal Accident/Income Protection insurances. Despite the risks involved, Payscale reports that only 3% of builders have access to any form of medical or health benefits.

FAQs

What is professional indemnity insurance in Construction?

Professional Indemnity Insurance in Construction is designed to keep you covered in the event that a client is unhappy with your work or loses money because of it. This may be due to a mistake you’ve made, because there was a failure in communication between you and the client or because they’re simply unhappy with the end result.

Professional Indemnity is a popular insurance in many industries, so if you’d like to know more about it, and if it might be appropriate for your business, read our article covering PII.

What does 'course of construction' insurance cover?

Course of construction insurance (sometimes referred to as 'building work insurance') is designed to protect property developers and constructors from the accidents that can occur on a construction project. This could include:

- Fire

- Flood

- Storms

- Vandalism

- Theft

- Subsidence or collapse

You may also see it referred to as 'contract works' and it may be included in a 'construction all risk' policy.

What insurance does a self employed construction worker need?

All of the insurances above are still relevant to those working as a self-employed contractor. However, many larger companies will already be covered by public liability/all risks policies, so check with your employer before getting on-site what they are and aren’t covered for.

If you’re going to be working on smaller projects or by yourself, then you might need your own public liability insurance. If you’re going to bring anyone else onboard, then employers’ liability is a legal must-have, and similarly if you’re going to be using your vehicle to help your business (such as moving tools from one site to the next) then you’ll need to upgrade to a business use vehicle insurance, so talk to your vehicle insurance company.

How can I claim on my construction insurance?

Claiming on construction insurance isn’t more difficult than claiming on other policies you may have in the past. As with any claim, make sure you’ve gathered as much information, data and photography to support your claim as possible, and try to report it to your insurer as quickly after the event as possible.

In 2026, the claims process is increasingly digital-first. Most insurers now require evidence to be submitted through dedicated mobile apps or portals, which use AI to instantly triage your claim. Your insurer will typically require:

- Time-stamped metadata: Ensuring the 'when' and 'where' are automatically verified via your photo files.

- Detailed Incident Log: A digital record of exactly what happened, often uploaded via voice-to-text features in the insurer’s app.

- Dashcam/CCTV footage: Increasingly mandatory for site accidents or vehicle-related disputes.

- Immediate Notification: Essential for 'claims-made' policies (like Professional Indemnity), where you must report any circumstance that might lead to a claim as soon as you become aware of it.

- Digital Damage Analysis: High-resolution photos used by insurers for automated repair cost estimations.

If you’re worried someone may make a claim against you wrongfully, getting these details yourself can help strengthen any case you make and could protect any no claims bonus you have.

What is construction all risk Insurance?

It’s simply designed to cover a lot of the risks you might face while on a large, complex and potentially busy construction site. Our definition here goes into more detail. It typically includes Contract Works or Course of Construction insurance, as well as other coverages like public liability.

Site insurance is a form of building construction insurance designed to protect a site that is currently being worked on. It typically contains many of the features you'd expect from a regular construction insurance policy, such as public liability and tools & equipment cover, but is often targeted more at smaller site changes (such as extensions and renovations) and for anybody who doesn't want a policy they feel is targeted at an enormous building site (and the cost that might come with that).

Construction insurance brokers act as an intermediary between people who need construction insurance in the UK and onstruction insurance companies. They work with their customers to build strong, well-rounded policies, and partner with insurers to help bring in new customers.

They can be more expensive at times (as can any 'middleman' service) but provide their value in the advice and guidance they're able to offer, bringing you insights into what similar companies opted for insurance-wise and what is/isn't recommended.

This depends on the type of work that you do. If you simply follow the blueprints and guidelines provided to you (and thus don't provide your own opinion or designs) then PI insurance might not apply to your work.

If you do provide guidance, design/draw blueprints or make recommendations on appropriate materials or build changes, then professional indemnity insurance could help cover costs of certain claims of professional negligence.

Whoever is responsible for the building site would typically hold a construction insurance policy. If you're a contractor, you should be told ahead of time whether you would need your own insurances or whether you'd be covered by those of the team responsible for the site. As a general rule with insurance, it's always better to be safe than sorry.

Design and build insurance typically covers the most common risks anyone working in the D&B category might face. While there is no such thing as a 'standard' policy, a good design and build policy might include professional indemnity, public liability and employers' liability. You may be offered additional coverage for cyber security or plant/Tools.

Like any other insurance, really—if you need to make a claim, gather as much information as you can, and report it to your insurer at the earliest possible opportunity.

This depends entirely on the company and clients hiring you and the work you do, but certainly consider professional indemnity, employers' liability and public liability insurance for building work as a base. It might be necessary to have other coverages, such as tools/plant, but these would vary from project to project, so make sure you're clear before bidding.

Quotes were gathered using a sample contractors and businesses. Neither ever worked:

- suspended (from a harness or rope etc.)

- underground by a depth of more than 1m

- demolishing buildings

Quotes for the sole trader were collected using a sample profile of a male builder with no previous experience working as a builder. Living in NW London, has no prior claims or convictions against him.

Quotes for our limited company were gathered using a 1 director business that brought in contractors for less than 50 days of work per year. Their director had 1-2 years experience in the construction industry.