The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Average Cost of Home Insurance 2026

Cheap Home Insurance in Your Area

Quickly compare up to 50 UK insurance providers. Powered by QuoteZone.

We've gathered quotes from a dozen of the best UK home insurance companies and analysed the home insurance market to find out how much you might pay for combined buildings and contents insurance in 2026 depending on factors like excess and coverage.

- Average home insurance cost

- Rebuild cost calculator

- Home insurance extras cost

- How can the excess be used to lower your home insurance premium?

- How does no claims bonus affect home insurance premiums?

- Is paying monthly a good idea?

- Building insurance

- Home and contents insurance UK

- FAQs

The average costs for both for basic and more premium policies can help you decide which type of home insurance fits in your budget and whether a quote is too good to be true, or perhaps more than you need.

For information on costs of extras like family legal, accidental damage, personal belongings, bikes and home emergency, see our article on average costs of home insurance extras.

Average Home Insurance Cost

NimbleFins research showed the average cheap home insurance quote for the typical British home in 2026, with a £300,000 rebuild cost, is around £356 a year or £33 per month. This reflects the five cheapest quotes available for basic policies that include £50,000 of contents cover to protect personal possessions but no accidental damage cover, with rates adjusted for inflation in January 2026.

More robust policies with accidental damage cover, legal cover and home emergency cover cost £461 on average (an extra £100 or so per year for these additional features).

But you might pay more or less in the market today, depending on the rebuild cost of your home, the excess, your no claims bonus, the features you want in a policy and even if you have made a claim on your home insurance in the past.

Supporting NimbleFins research, the latest data from the Association of British Insurers found that the average price actually paid by homeowners for a home insurance policy covering buildings and contents in Q3 2025 was £384 (down from £407 a year earlier).

| Average Cost of Cheap Home Insurance^ (£300k rebuild) | per year | per month | |

|---|---|---|---|

| No accidental damage | £356 | £33 | |

| With accidental damage | £401 | £37 | |

| With Accidental Damage, Legal and Home Emergency | £461 | £43 |

This data could imply that adding accidental damage costs £143—but in reality it can often be added to a policy for quite a bit less. There may be other differences between the set of policies that excluded or included accidental damage, accounting for the £143 difference between the groups.

We should note that listed buildings typically cost more to insure.

The range of annual premiums in our study was quite large, ranging from under £300 per year up to £1,500 per year or more, depending on company as well as the coverage and features we selected, and other differences like excess and no claims bonus. This is why it's critical to compare prices before accepting a quote from one company.

The provider and tier can make a big difference, with quotes for premium cover from some brands costing 5X as much, or even more. Let's see how these factors affect premiums.

Rebuild Cost Calculator

A big factor that determines the cost of your home building insurance is the rebuild cost of your home.

The average cost to rebuild a house in 2026 is around £323,500 for a 1,400 square foot 3-bed home, but your rebuild cost will depend on many factors such as the size of your home and where you live.

If your home needs different or specialist building materials compared to most standard properties, or your home is a listed building your rebuild cost could be much more.

The following chart can give you an idea of how the rebuild cost can affect your premium. Prices reflect the five cheapest prices including:

- £50,000 of contents cover,

- accidental damage,

- legal,

- home emergency.

| Average Cost of Cheap Home Insurance^, by building rebuild cost | ||

|---|---|---|

| £120,000 rebuild cost | £341 | Get Quotes |

| £300,000 rebuild cost | £461 | Get Quotes |

| £500,000 rebuild cost | £468 | Get Quotes |

| £1,000,000 rebuild cost | £480 | Get Quotes |

Buildings cover alone usually costs in the region of £80 less than a combined home insurance policy with both buildings and contents cover.

Extras

Cheaper policies tend to be stripped of "extra" coverages like legal, home emergency and accidental damage, while more expensive/higher tier policies might include these features.

In many cases a higher tier policy that includes the features you want ends up cheaper than adding extras onto a cheaper policy. For example, adding all three can add over £110 to your premium.

According to our study, here's how much these features usually cost when you add them on:

| Estimated Cost of Home Insurance Add Ons | |

|---|---|

| Legal Assistance | £24 |

| Home Emergency | £41 |

| Accidental Damage (building & contents) | £48 |

| Total | £113 |

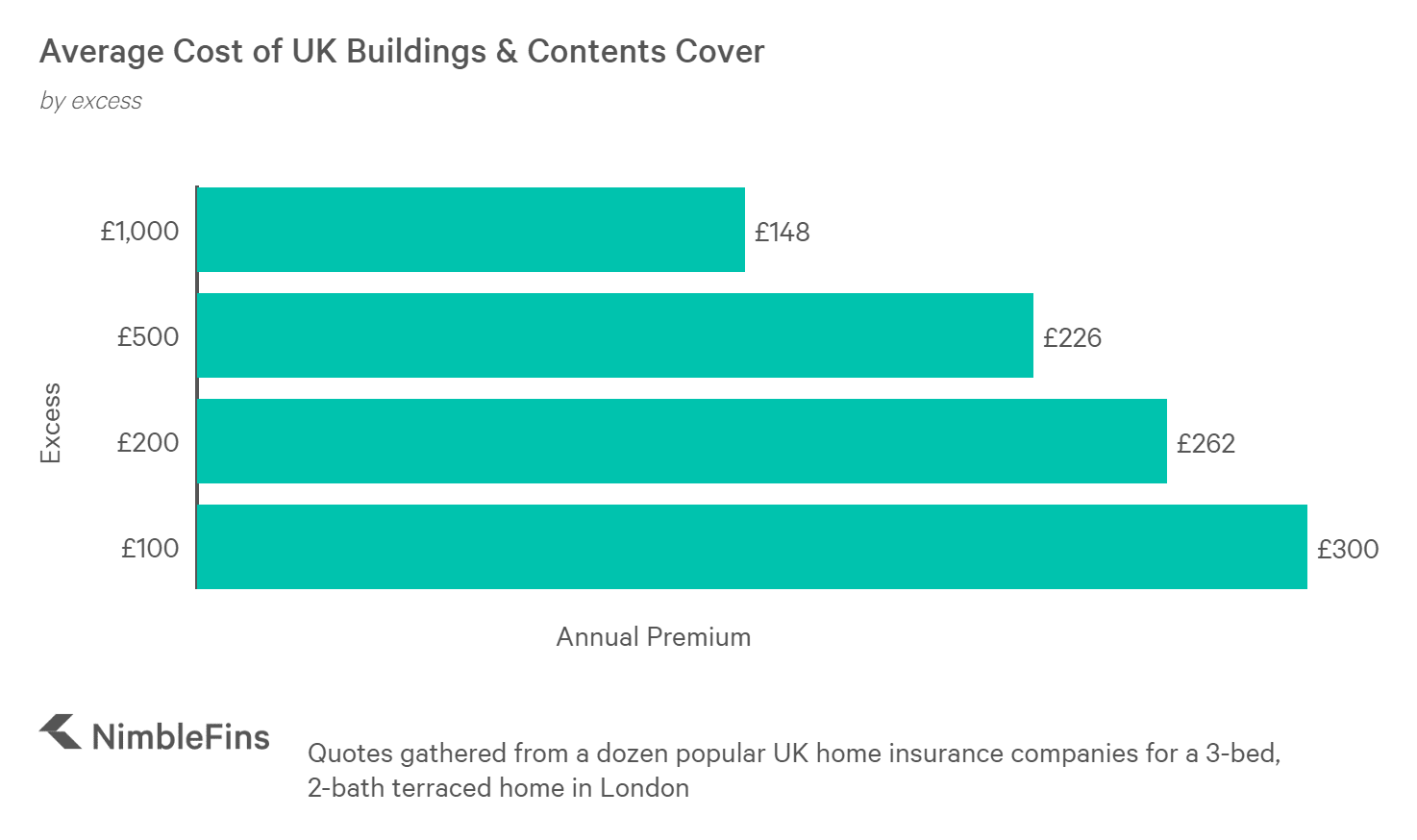

How Excess Affects Home Insurance Premiums

Like all insurance policies, your home insurance premium can often be reduced by electing to pay a higher excess, and vice versa.

The excess is the amount you pay towards any claim before the insurer pays any reimbursement. The more you are willing to pay towards a claim (the excess), the lower your insurance premium in most cases.

While you may be enticed by a higher excess/lower premium combination, carefully consider the financial impact of a higher excess. Should you ever need to claim on your policy, you'll need to be able to cover the excess.

Premiums Drop When You Pay a Higher Excess

| Average Buildings & Contents Insurance Premium by Excess | Annual Premium |

|---|---|

| £500 | £433 |

| £300 | £461 |

| £100 | £476 |

What is a Compulsory Excess?

An excess is an amount you must pay towards any claim on your home insurance, and a compulsory excess is basically the minimum excess that an insurance company requires.

A compulsory excess is non negotiable.

Not all insurers apply a compulsory excess; some have £0 compulsory excess, letting you choose the entire excess amount through your selection of voluntary excess.

Whether or not you have a compulsory excess, you can typically add a voluntary excess amount on top of the compulsory excess.

What is a Voluntary Excess?

As its name implies, the voluntary excess is an amount that you volunteer to add on top of the compulsory excess.

Selecting a voluntary excess (thereby raising the total excess) should lower the premium you pay, but keep in mind your coverage is essentially reduced if you need to claim.

You'll be required to pay both the compulsory and voluntary excess before the insurer pays their share of a claim.

How Does No Claims Bonus Affect Home Insurance Premiums?

The NimbleFins team recently ran some tests and found that someone with 0 years of no claims would pay 22% more for home insurance than someone with 5 years of no claims. On a typical home insurance policy, having 5 years of no claims translates into a savings of roughly £60 per year.

After five years, you get less and less benefit per additional year of no claims.

However, NCDs can vary significantly from company to company so your experience may be different.

| Average No Claims Discount on Cheap Home Insurance | |

|---|---|

| 3 years | -20% |

| 5 years | -22% |

| 9 years | -25% |

An interesting point is that compared to a few years ago, we've noticed that no claims discounts have increased for home insurance. This means that people who haven't made claims can save even more nowadays. Why? We think it's because claims have gotten so much more expensive, due to inflation—so insurance providers are really keen to attract people without a history of making claims.

How Much Does House Insurance Cost a Month?

In the UK, the average monthly payment for combined buildings and contents insurance in 2025 is about £35 per month. But beware—monthly payments end up costing around 9-10% more than paying upfront.

Why? Because when you pay monthly you're essentially borrowing money so you pay the premium AND an interest charge each month. For example, a £300 annual policy would cost £28.21 per month based on a 22.9% APR. Each month, you'd pay about £25 towards the premium and £3.21 in interest payments (with interest charges totalling £39 for the year).

If you have the cash, or have a 0% credit card, we recommend paying upfront to save yourself the interest payments. For more information on this topic, please read our article Should I Pay my Home Insurance Annually or Monthly?

Cheap Home Insurance in Your Area

Quickly compare up to 50 UK insurance policies. Only one form to fill out.

Building insurance

Building insurance is one component of a home insurance policy that covers the bricks and mortar of a property, but not the contents within it. It can be purchased on its own or as part of a package which also includes contents.

Because it doesn't include contents cover it can be cheaper, and does cover a few things inside the property too, such as fitted bathrooms and kitchen cupboards.

Renters don’t need building insurance, it is the property owner’s responsibility as they own the structure of the house.

If you are applying, or already have a mortgage, you will usually need building insurance as a minimum as part of the terms of the loan.

Building insurance basically protects the investment into a property, meaning if it was destroyed an insurance provider would pay the cost of rebuilding it. However, it's important to ensure you have calculated an accurate rebuild cost, which we covered earlier in this guide.

Home insurance vs building insurance

Home insurance can cover contents insurance, building insurance, or both. Home insurance is used to explain the overall policy while building insurance is just one specific element, which can be purchased on its own or as part of a combined home insurance policy.

Building insurance simply covers anything permanently fixed to the property, but a comprehensive home insurance policy could also cover the contents inside and include other features such as emergency assistance and bike protection.

What does building insurance cover?

Building insurance covers anything permanently attached to the house, such as brick walls, windows, doors, fences, drains, the roof, as well as fitted furniture such as cupboards, fitted bathrooms, wooden flooring and fitted wardrobes.

The best way to determine whether something is covered under building insurance or contents is to think about if you were moving house. Anything that can be reasonably moved to another property, is considered contents, while anything fixed such as a fitted (but not freestanding) fridge, or fireplace is considered part of the building. Interestingly carpets are usually considered contents, but laminate or wooden flooring is part of the building.

Leaks and damp walls and floors also fall under building insurance, as does subsidence and some roof repairs.

However, it is always worth checking policy documents before you take out cover, as sometimes there are restrictions in how much an insurer will pay out for subsidence. If you've already made a subsidence claim, you might find it more difficult to get subsidence included in your cover, or have to pay a higher price.

Read more about what building insurance covers and what building insurance doesn’t cover in our comprehensive guide.

Does building insurance cover roof repairs?

Roof repairs fall under building insurance, but providers may not pay out for all roof damage. Each provider will have their own policy explaining which causes of damage qualify for support. If your roof is new (under 10 years old) you'll usually stand a better chance of getting a full payout.

It could be a good idea to keep records of maintenance you've done to your roof through the years to prove you've looked after it, as insurers could reject a claim if they think the roof could have survived the incident if it had been kept in better condition.

You'll need to provide your insurance company with a quote for the repair work and it could help your case if you get a full report from the contractor. Some insurance companies need quotes from more than one roofer, so it may be best to contact your provider before arranging inspections.

What is the average cost of building insurance?

The average premium paid for a buildings-only insurance policy is around £329 heading into 2025, up around 15% from the year before. Standalone contents cover costs an additional £138 or so—making combined buildings and contents policies much better value for money.

The cost of building insurance is dependent on a number of factors such as the rebuild cost, the percentage of flat roof on your home, what materials your home is made of, and your previous claims history.

Your location will have an impact, as this can impact the rebuild cost and insurers will also take into consideration crime levels in your neighbourhood.

And the size of your home will also affect the premium (e.g. larger homes cost more to rebuild after a fire, all else equal).

What does building insurance cover in flats?

Building insurance in flats covers the same things as building insurance on a home - anything permanently attached to the flat such as walls, windows, doors, driveways, drains and pipes. The difference is who pays for it.

If you own the freehold to the flat, it is your responsibility to pay for the building insurance.

If you only own the leasehold to the flat, you may not need to purchase building insurance, although this does depend on some factors.

If you pay ground rent or property maintenance to the freehold owner, it's more likely they are responsible for the building insurance. Check this with them.

Sometimes you can be a leasehold owner but do not pay a property management fee, and it may not be clear if you are covered or not. Land Registry documents will tell you who owns the freehold, so you can get in touch with them and ask if they pay for building insurance. If they do not, it is probably worth you buying this yourself so your part of the block of flats is covered.

If you are a tenant of a leasehold or freehold flat, it is the landlord's responsibility to provide, or check the status of, building insurance. This is the case with a tenant in any type of property - a landlord has responsibility for insurance of the property itself and any contents they own. But it is the tenant's duty to sort out any contents insurance they want, if they feel they need it.

Building insurance quote

If you're interested in getting a building insurance quote, click here where you can enter your details and get quotes from up to 50 providers. The process only takes a few minutes of your time and you're likely to know all the necessary details off the top of your head.

In our experience, the only bits that might need extra time and double checking are confirming the month and year you purchased the property, the types of locks on your external doors (don't worry, there is a door lock guide with pictures in the quote form!) and the percentage of flat roof (if you have one).

Note: the percentage of flat roof is worth confirming—we recently redid our building insurance and guessed we have 30% flat roof but when we confirmed on the floor plans, found it was only 11%! Not only could getting it wrong impact your premium, but a wrong guess could invalidate your insurance. Luckily you won't need the exact percentage, just a range.

Once you have entered your details, you're likely to get dozens of quotes. From there, you can easily compare the premium and excess (the amount you pay towards a claim), plus compare across features like legal expenses, accidental damage (to buildings and/or contents) and home emergency cover.

These may be included as standard, available for an additional premium or not available.

To learn more about or purchase a specific policy, you simply click to go to the provider's site. The details you entered initially will be transferred over to the provider, simplifying the buying process.

Home and contents insurance UK

Contents insurance is an element of home insurance which you may or may not need depending on your circumstances. Many people choose to have contents insurance for the property they live in as it protects their valuables which could include expensive electronics or jewellery. Both home owners and renters can benefit from contents insurance.

Contents insurance for renters

Tenants renting a property need their own contents insurance policy to protect their belongings. A landlord's contents insurance will only cover their own items, and they won't be able to claim for your items.

Some tenants decide not to get contents insurance and that is their own decision - there are no rules stating they must have it. Read our guide: What home insurance do I need if I rent? for more information.

Landlords may also decide to include contents insurance in their policy if they are letting their property out fully or partly furnished. (But to reiterate, this only covers the landlord's contents, not the renter's.)

Sometimes there are a number of expensive white goods in a property that is rented out, but it is a personal choice whether the landlord chooses to protect them. Sometimes they may feel if an item broke or was damaged it wouldn't be worth paying the excess and potentially increased premiums to claim on the insurance.

What does contents insurance cover?

Contents insurance covers most moveable items inside a property which have been damaged or destroyed from fire, theft, smoke or flood.

You can also have accidental loss/damage, legal, home emergency and extra valuables such as bikes, included in a policy. Sometimes these must be bought as add-ons.

FAQs

Methodology

Unless otherwise noted, the sample cost estimates provided in this article reflect the average of the 5 cheapest buildings & contents insurance quotes gathered from a dozen popular UK home insurance providers for a 3-bed, 2-bath terraced home in Surrey with a £300,000 rebuild cost and £300 excess with 9+ years of no claims. Homes are protected by a 5 lever mortice deadlock conforming to BS 3621 on the front door, but no alarm. Where the rebuild value was £120k or £300k, we assumed contents worth £50,000; for higher rebuild costs we assumed £100,000 of contents. Annual to monthly payments were calculated using an 21% APR. Rates were adjusted for home insurance inflation in January 2026.

Read more: