Chrome Credit Card by Vanquis: A Good Credit Builder Card for You?

Chrome Credit Card by Vanquis: A Good Credit Builder Card for You?

Good for

- Start with a manageable credit limit of £500 up to £1,500

- You could build your credit limit up to £4,000 over time subject to good account management

- Stay in control of your account with online servicing, a mobile app, SMS and email alerts

Bad for

- Carrying a balance month-to-month

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Note: The Chrome card by Vanquis is no longer accepting new applications, but existing cardholders should be able to continue to use their cards for a while. Vanquis has consolidated their cards under the Vanquis brand. You can read more about that on their website, here.

The Chrome Credit Card by Vanquis is a credit builder card with a relatively low APR. In fact, the Chrome's interest rate is lower than most other credit builder cards. But how does it compare to other options on the market? Read our review to find out.

Chrome Credit Card Review

The Chrome Credit Card by Vanquis can be a great tool for those who are new to credit or have had some problems in the past and now want to build or rebuild their credit rating. By showing you can manage a credit card sensibly (e.g., paying on time and staying under the credit limit), a cardholder's credit score should improve over time.

The Chrome card offers features such as Contactless (for transactions up to £30) and 24/7 full service online banking, plus the eVanquis apps for iPhone and Android let you access your account at all times from your phone or tablet. Customers report that this feature helps them stay on top of their credit limit and payments.

The Chrome is the lowest APR card on offer by Vanquis, charging a representative variable APR of 42.9%—around 10% lower than the Vanquis Classic Visa and a touch lower than the Aquis. However, as a credit builder card the interest is still high enough to rack up significant interest charges should you carry a balance from month to month. Therefore, it's best to pay off as much of the balance as possible each month.

As a new customer you'll start with an "easy-to-manage" credit limit between £500 and £1,500 (this has increased recently—the minimum credit limit used to start at £250. By showing good account management you could get a credit limit increase after your 5th statement and every 5 months after that, up to a maximum limit of £4,000.

You can apply to the Vanquis Chrome via mobile, tablet or PC by clicking the "Apply Now" button below. You'll get a response from the pre-application eligibility check in 60 seconds—this is a soft check only so will not harm your credit score.

Vanquis Chrome Credit Card

Top Tips for Using a Vanquis Chrome Credit Card

- ALWAYS pay before the due date (whether you're paying the minimum amount due, the entire balance, or somewhere in between).

- ALWAYS stay under your credit limit.

- Even though the Chrome's APR is relatively low for a credit builder card, it's still advisable to pay off your entire balance each month (or as much as possible). By doing so, you can avoid paying high interest charges on any balance that's carried from month to month.

Vanquis Customer Reviews

Is Vanquis any good? We scoured online reviews and found that existing customers rate Vanquis very highly. In fact, Vanquis has a remarkable 4.5/5 Trustscore on Trustpilot, reflecting feedback from more than 24,500 customers—and 83% of reviewers said Vanquis was "Excellent." Many customers remarked on the usefulness of the app in managing their account (e.g., tracking spending, paying on time, staying under the credit limit, etc.)

Here are some real quotes from existing customers to give you an idea of the typical customer experience:

"Easy app to use and check when payments are due are simple... easy to apply and receive the card."

"Best card I’ve ever had, lovely friendly staff, I lost my job and went over my limit and they where great about it xxxxx"

"Easy to see what you’ve spent and how much credit you have remaining. Also easy to pay balance."

"I find Vanquis very easy way to purchase items and keep check on my spending also I am improving my credit rating would recommend to anyone."

"... it is teaching me... how to budget my finances and stop the urge to go on a shopping spree... a massive issue in the past. Thank you so much Vanquis you have done such a positive thing for me and I am sure have done so for many many others."

"Vanquis is helping me rebuild my credit rating!"

"Due to Vanquis APP not working correctly I... got charged a late fee and full interest..."

"Interest rates are outrageous. I pay their ridiculous interest every month on time, plus I pay in alot of money voluntarily every month, and they charge you like there is no tomorrow...."

We find negative reviews can be really helpful, as they can help cardholders figure out how to get the most of out their cards. For instance, it seems that the App glitches sometimes so we'd recommend paying a few days early to give yourself a time buffer if this happens to you (they recommend paying 3 working days in advance anyway to give time for the payment to process).

Also, Vanquis does charge higher interest rates because they accept people with worse credit histories—these cards are best used by paying off your full balance each month (or as much as you possibly can) and working to rebuild your credit history. They're not good for carrying a balance due to the high interest rates.

Chrome Credit Card Benefits & Features

| Chrome Credit Card Features | |

|---|---|

| Initial Credit Limit | Between £500 and £1,500 |

| Credit Limit Increases | Subject to good account management (e.g., by staying within your credit limit and making at least your minimum payment on time), you may be eligible for credit limit increases every fifth month up to £4,000 |

| Transaction Fees | Non-sterling transaction fees of 2.99% |

| Cash Withdrawal Fee | 3% or £3, whichever is greater |

| Annual Fee | £0 |

| APR |

|

Chrome Interest Rate (APR): At least 51% of applicants will receive the representative Chrome purchase APR of 42.9%. The other 49% of applicants may receive a higher interest rate, anywhere from 42.9% even up to 59.9%. You don't want to be carrying a balance from month to month with those interest rates! Cash rates are typically higher, but with Chrome seem to be in line with the purchases rates, starting at 29.5% variable APR.

Chrome Credit Limits and Credit Increase: Your credit limit on a Chrome credit card will fall between £250 and £1,200, depending on your financial situation and credit history. With good account management like paying on time and staying within your limit, the credit limit on your account may increase over time—specifically, you may qualify for an increase after your 5th statement and then further increases every 5 months up to a maximum of £4,000.

While some cardholders find a higher credit limit can be useful for purchasing power and a possibly improving their credit score, a higher credit limit is not always desirable. For example, if you're on a strict budget and would rather not have the temptation of a higher limit you can reject the increase or even request that Vanquis lower your limit. Vanquis might deny a request to lower your limit, however, if they believe that you would exceed a lower credit limit. Exceeding the credit limit would result in default fees and may harm your credit score, potentially making it more difficult to get credit in the future.

Withdrawing Cash with a Chrome Credit Card: You can withdraw cash with the Chrome card for a 3% (£3 min) fee per transaction. Getting foreign cash from an ATM abroad incurs a further 2.99% non-sterling fee (more on that below). Withdrawing cash using a credit card is expensive and we don't generally recommend it for three reasons:

- Cash interest rates are higher than purchase rates

- Interest on cash withdrawals is charged immediately (there is no grace period)

- Each cash withdrawal incurs a fee of 3% of the transaction (minimum £3)

Using Chrome Abroad: The Chrome card can be used abroad, with transactions incurring a 2.99% non-sterling fee when you withdraw foreign cash from an ATM, paying for a restaurant or hotel in a local currency, etc. This fee is typical on all but special travel cards.

In addition to the non-sterling FX fee, any foreign cash withdrawals from an ATM abroad would incur an additional 3% (£3 minimum) cash withdrawal fee—this cash fee is charged in addition to the 2.99% non-sterling fee. Not only do you incur these fees but interest is charged immediately on cash withdrawals—generally speaking, using a credit card is an expensive way to get travel cash.

| Type of Non-Sterling Transaction Abroad | Fees |

|---|---|

| Foreign Cash Withdrawals | 3% (£3 min) + 2.99% |

| Foreign Credit Card Transactions (e.g., purchases, paying for a meal at a restaurant, etc.) | 2.99% |

Minimum Monthly Payments: To give you a general idea of what to expect to pay each month, the minimum monthly payment is calculated as the highest of:

- 1. the total of any interest we have charged since the date of your last statement; and any default fees we have charged; and depending on your APR, 2.5% of the remainder of the balance you owe on your account as at the statement date; or

- 2. £10

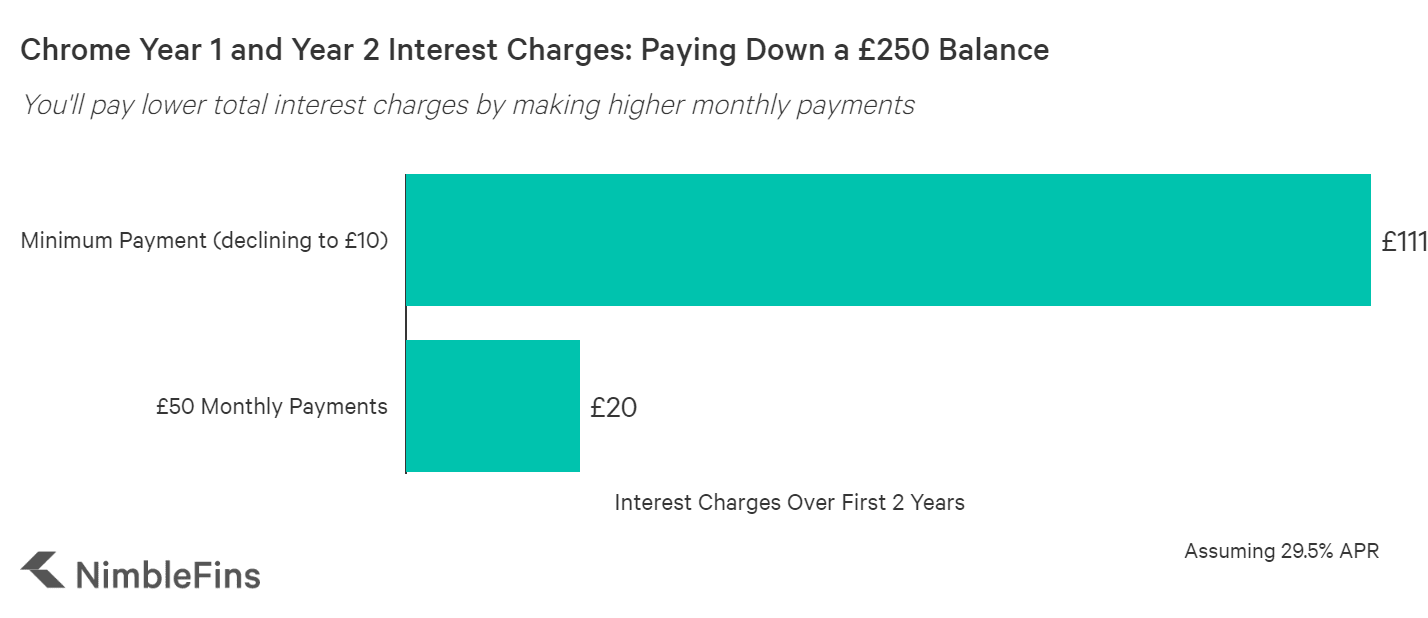

If you don't make any more purchases on your card, the minimum monthly payment will drop over time (as the balance falls) until it hits the £10 minimum payment floor. As we discussed in our article Here's How the Minimum Payment Floor on Your Credit Card Could Cost You Hundreds of Pounds, paying only the minimum payment floor can prove quite costly over the long term in terms of interest charges. In fact, in the example below, a cardholder paying only the minimum amount each month would delay paying off their debt by nearly 5 years and incur around £150 more in total interest charges over the years, versus a cardholder who consistently pays £50 per month.

Cost of Borrowing with Chrome

| Illustrative example: For a purchase of £250 on your credit card | ||

|---|---|---|

| Monthly Payment | Minimum Payment each month (£10) | £50 each month |

| Without taking into account any introductory rates, how much interest will you be charged in the first year? | £64 | £20 |

| How much interest will you be charged in the second year? | £47 | £0 |

| How long would it take to clear the balance? | 5 years, 3 months | 7 months |

The above example assumes the following: The transaction takes place on 1st January and you make no further transactions. Your statement is produced on the 1st of each month and you always make the payment each month on the 15th. Your statement is produced 31 days after you make the purchase.

Bottom Line: If you are new to credit or had some problems in the past, you may still be eligible for Vanquis's lowest APR credit card. Get the most out of the card by always paying on time and staying within the credit limit to try to improve your credit history. And pay as much as you possibly can each month to limit interest charges.

FAQs

How does the Chrome Credit Card Compare to Other Credit Cards?

To better understand the value of the Chrome Credit Card you need to look at it in the context of other available options. We compared this card to other rewards cards so you can see which may be more suitable for you.

Chrome vs Vanquis Classic Credit Card

Vanquis's Classic credit card, the Classic, will consider applicants with no credit history, poor credit history or are unemployed. Initial credit limits might be lower and the Classic has a higher representative APR of 42.9%. Potential applicants can use the pre-application eligibility checker to see their likelihood of being accepted before they apply (useful to help avoid an unnecessary hard credit check and a rejected application).

Quick Takeaway: You're likely to pay a higher interest rate with the Vanquis Classic, but you may be more likely to be accepted by the Classic if you have a worse credit rating. It may be worth trying the pre-application check with the Vanquis Classic if you're not sure.

Chrome vs Marbles Credit Card

The Marbles card is a credit builder card for those with a very limited credit history, or poor credit. Even individuals with CCJs or bankruptcy in their past will be considered. The Marbles card representative APR is 34.9%.

Quick Takeaway: The Marbles card has a higher representative APR, but on either card we'd recommend paying off the full balance each month if you can.

Chrome vs Aqua Classic Credit Card

Aqua's most popular card, the Classic, will consider those with poor credit, including the self-employed, people who've paid late in the past and those with low income. Initial credit limits run between £250 and £1,200, with a representative APR of 39.9%. Responsible management of your account (i.e., making payments on time and staying within the credit limit) can lead to credit limit increases, which can in turn improve your credit rating.

Quick Takeaway: The Aqua Classic might charge a slightly higher APR.