The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

What is DJ Insurance?

Building up a solid reputation as a DJ can take years, but whether you're just starting out or you have a successful following already, you'll certainly need business insurance. Having the right insurance in place can help protect against financial disaster if, for instance, a member of the public is injured during one of your gigs and they blame you. Here's what you need to know about DJ insurance to protect you, your equipment and your business.

What Kind of Insurance Does a DJ Need?

While insurance needs vary from situation to situation, here are some of the more common types of insurance coverages that a DJ might need—including some examples to show you when insurance can help.

1. Public Liability insurance protects you financially if you accidentally injure a member of the public or damage their property. With respect to these types of situations, public liability insurance primarily covers two things: legal expenses and compensation claims. Public liability insurance is frequently available with £1 million, £2 million, £5 million and £10 million of cover.

- Bodily Injury Example: A member of the audience trips on a cord, falling and badly breaking their wrist. They sue you for lost wages because they're unable to work for 6 weeks.

- Property Damage Example: You accidentally damage the venue walls when carrying in your equipment. The venue sues you for the repair costs.

2. Employers' Liability insurance is required by law if you have anybody working for you (with few exceptions). It protects against compensation claims by current or former employees if they fall ill or are injured because of work.

- Employers' Liability Example: An employee falls off the stage and damages their knee, needing surgery and time off work as a result. The NHS claims for the medical expenses and your employee makes a claim for negligence.

3. Equipment Cover can protect against accidental damage, loss or theft of valuable DJ equipment, such as monitor speakers, mixer, turntables, headphones, vinyl records and even a laptop. Not only is DJ equipment expensive to replace, but being without can mean lost revenues. Equipment cover can protect your equipment at home, in transit or at a venue. Having this insurance in place can keep you spinning.

4. Personal Accident insurance can provide a financial benefit to make up for lost wages or even cover medical expenses for you and/or employees in case of an accidental serious injury—or compensation for accidental death. The benefit can be weekly or in a lump sum, depending on the seriousness of the injury.

- Personal Accident Example: If an employee slips and falls while working, hurting their back, personal accident insurance can pay them a weekly amount as a benefit while they're off work due to the injury.

In addition, a DJ might need commercial vehicle insurance, business interruption insurance, cover for playing abroad or other business insurance coverages.

How do I Find the Best DJ Insurance for Me?

When choosing a disc jockey insurance policy, there are a few things to keep in mind. First, make sure you can get the specific cover that you need for your situation (e.g., public liability, equipment, etc.). Second, check the financial strength of an underwriter, which you can do by looking at Fitch, Standard & Poor's, A.M. Best and Lloyd's. Third, read customer reviews online—e.g., Trustpilot and reviews.io. Finally, check quotes from multiple sources (e.g., via a comparison site) because quotes can really vary from company to company.

- Look for customisable cover

- Check the financial strength of the insurance underwriter

- Read customer reviews

- Check prices in the marketplace

How Much is Public Liability Insurance for a DJ?

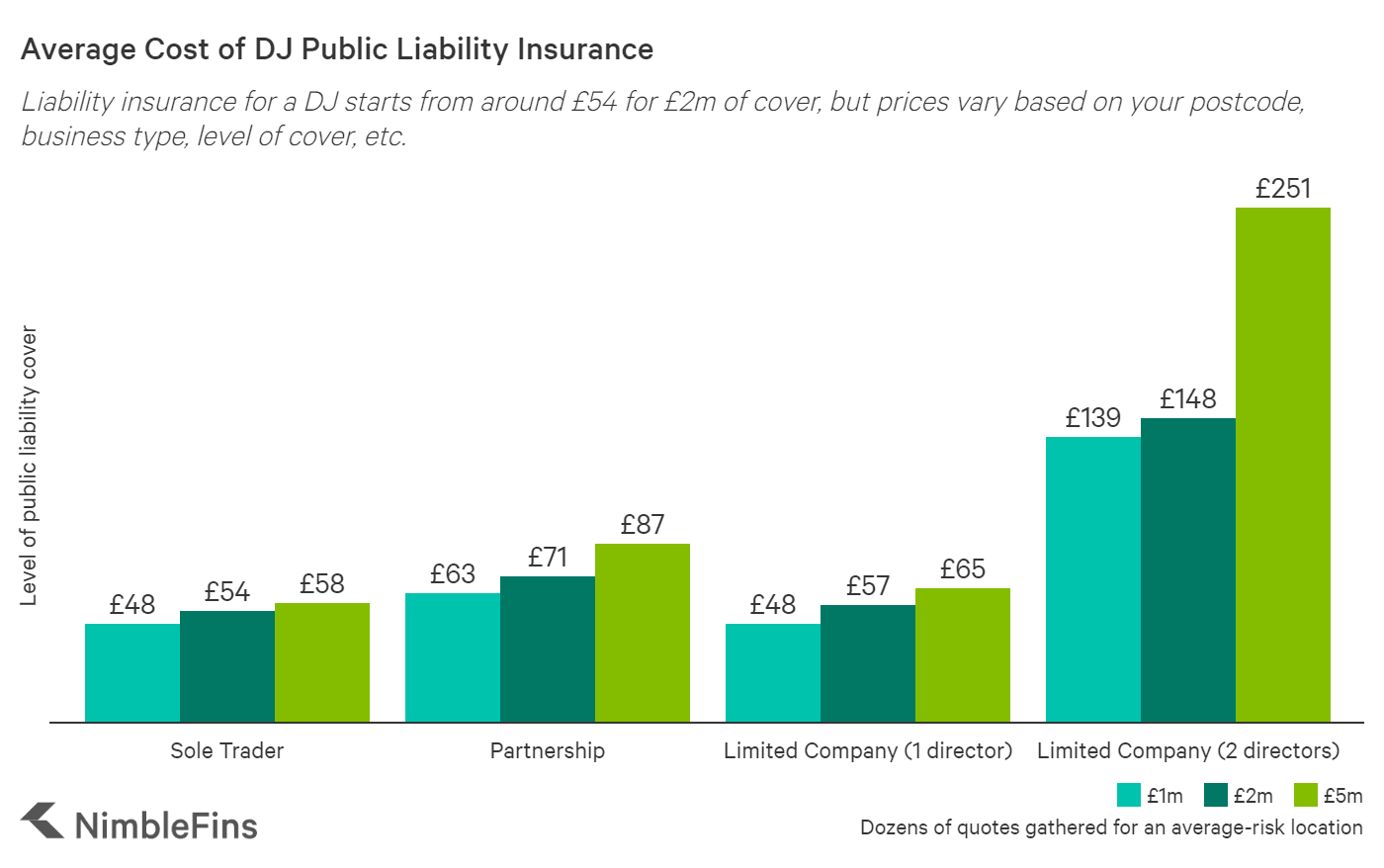

The average cost of public liability insurance for a DJ starts from around £54 a year for a self-employed sole trader with £2 million of cover. The premium increases with cover level, but additional amounts of cover typically cost very little compared to the initial million of cover. For instance, while £2m of cover would cost around £54, more than doubling the cover to £5m could cost as little as £4 extra.

| Average Cost of DJ Public Liability Insurance | £1m cover | £2m cover | £5m cover |

|---|---|---|---|

| Sole Trader | £48 | £54 | £58 |

| Partnership | £63 | £71 | £87 |

| Limited Liability Company (1 director) | £48 | £57 | £65 |

| Limited Liability Company (2 directors) | £139 | £148 | £251 |

Cost of Employers' Liability for a DJ

Adding additional coverages will increase the premium you pay. For example, if you hire any employees, you'll need to make sure they're insured as well with employers' liability insurance—it's required by law. How much does employers' liability insurance cost? In our sample study we found that adding employers' liability insurance for 1 employee would increase a self-employed DJ's business premium by £135 (bringing the total premium to £188 for £2m of public liability plus employers' liability cover).

Of course, these are just sample quotes to give you a general idea of prices; your premiums might vary significantly depending on your situation and the details of your application.

FAQs

Public liability insurance may not be a legal requirement for a DJ, but it may be required by certain venues—in fact, you may need to show proof of your DJ public liability insurance before you can perform. Even when it's not required by a contract, liability insurance is essential to have whenever you're working with or near members of the public.

The average cost of DJ public liability insurance is around £54 for a sole trader (e.g., if you're self employed), but prices vary depending on where you live, your business structure, the amount of cover, etc.

A DJ needs insurance to protect financially against situations like injury to a member of the public (see public liability insurance); theft of, loss of or damage to their expensive DJ equipment; injury to an employee (see employers' liability insurance); etc.

If you need DJ insurance, it's wise to check a few comparison sites to get an idea of prices, and also some of the specialist providers of liability and equipment cover for DJs in the UK marketplace.

DJ Statistics

According to the latest 2026 market data from Payscale and industry benchmarks, the average DJ in the UK now earns £30.12 an hour, with pay generally ranging from £14.50 to £61.00 an hour depending on experience and event type. Over the course of a year, DJs in the UK typically earn between £22,400 and £102,000. Based on our 2026 quote analysis, a standard £5 million public liability policy for a mobile DJ now costs approximately £88 per year.

Therefore, a typical self-employed DJ would only need to work for roughly 2.9 hours to pay for their annual cover—making public liability insurance an exceptionally cost-effective way to protect your business.