Welders Insurance | Quotes, Costs and Requirements

Find Welder insurance quotes.

Powered by QuoteZone.

Compare Quotes

- Rated 4.8 out of 5 stars on Reviews.co.uk

- Over 300,000 QuoteZone quotes completed per month

- Fill out only one form

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

As seen on

Because welding is a tricky business, a well-rounded insurance for welders policy is vital to ensure you, your customers and your employees (if you have any) are financially protected against an accident or other disaster. This guide to welder insurance will explain everything you need to know about the coverages on offer, such as public liability insurance for welders, and give you a breakdown of the typical welder insurance costs.

- What insurances do welders buy?

- Where can I get welder insurance quotes?

- How much do welders in the UK earn?

If you only have a few minutes

What can welder insurance cover?

- Public liability

- Product liability

- Employers' liability

- Professional indemnity

- Commercial Property

- Tools and equipment

- Personal injury

- and more

How much does welder insurance cost?

Welder public liability insurance can cost around £250 a year; fill out a quote form here to compare prices.

Who might need welder insurance?

- Self-employed welder

- Owner of a welding business

Is welder insurance required?

- Welder insurance is not a legal requirement, but it might be required by your clients and partners. Given the dangerous nature of the trade, welder insurance is critical for protecting you and your business financially against disaster.

What Insurance Does a Welder Need?

While public liability is the core component of cover, there are many types of insurance for welders; and many insurers will bundle these together to create a comprehensive policy that works well for various types of welding businesses. Buying all insurance coverages from one provider can simplify renewals and claims processes.

However, it may be cheaper to take out different components of cover from different providers. A broker can be useful for arranging different components of cover from different insurance companies, but many insurers offer comprehensive tradesman policies that welding businesses and self-employed welders can take advantage of.

| Common Types of Welders Insurance & What They Cover | ||

|---|---|---|

| 1. | Public Liability | Safeguards a business if third parties suffer damages or injury and blame the welding business |

| 2. | Product Liability | Often sold with public liability, product liability protects against damages or injuries due to the work product or a product sold (e.g. MIG guns) |

| 3. | Employers' Liability | Protects a business if an employee is injured or becomes unwell due to their work |

| 4. | Personal Accident | Covers financially if a welder is unable to work due to illness or injury (usually work-related, but some policies cover any illness or injury that gets in the way of work) |

| 5. | Business Use/Commercial Vehicle | Insures a personal vehicle or work vehicle for the additional risks of driving for business purposes (e.g. additional mileage) |

| 6. | Tools | Can insure welding tools if they’re stolen/accidentally damaged or lost |

These types of insurance can apply to self-employed welders and those running a larger welding company.

Welders Insurance Examples

- Public Liability: While a welder is working in somebody's home, the client trips and falls over a wire the welder left out. The client is injured and can’t work for a month. They sue the welding business for their lost wages.

- Product Liability: A welding gun sold by a welding business malfunctions and causes significant damage. The third parties sues for the damage and repair costs.

- Employers’ Liability: An employee burns themselves while welding and blames the inadequate safety equipment provided by their employer. They can’t work for 6 weeks, and sue the business to cover the damages.

- Personal Accident: A welder has a minor fall and can’t work for 2 weeks. Personal Accident helps cover lost earnings so the welder can pay their personal bills.

- Business Use Vehicle: A welder is involved in an accident while driving to a client site, damaging their van and another vehicle. Comprehensive Business Use Vehicle coverage pays for the repairs to both vehicles.

- Tools and Equipment: A welder's tools are stolen from a secure building site. Tools insurance pays for the cost of an equivalent replacement.

FAQs

Yes, due to the nature of their work welders absolutely need some form of coverage. While it isn’t a legal requirement, most clients won’t engage a welder if they don’t have a valid form of public liability.

A welder with any employees, contractors or part-time staff (even if they only work for one day!) must hold employers’ liability insurance—it's required by law. And a welder driving their vehicle for business purposes must hold a valid form of commercial vehicle insurance or 'business use' vehicle insurance. Driving without it is illegal. (A personal vehicle that is insured for social, domestic, and pleasure (SD&P) is not insured to visit client sites or other business use. Using a vehicle for the purposes when it's not insured properly risks the SD&P insurer voiding the policy if an accident does occur. Read more here.)

General liability insurance is a business insurance that protects a business for claims of injury, illness or damages. It is mostly a term used in the United States. In the UK this type of cover is more commonly known as 'business liability insurance', and typically comprises public liability and product liability.

Ways of saving money on other insurances, such as car or home coverages, also apply to welders insurance. These could include:

- Gathering multiple quotes to compare

- Lower levels of protection

- Working away from big cities, airports etc.

- No previous claims, convictions or bankruptcies

- More years of experience

There are a couple of more welder-specific things you can avoid to lower your costs too:

- Oxyacetylene welding

- Working at heights above 10m, or while suspended by ropes/harnesses.

What insurances do you need to be a welder?

Due to the amount of risk involved in welding work, most good welders hold public liability (and accompanying product liability) coverage at the absolute minimum. It’s unsurprising given the dangerous tools welders use, and the financial costs of not being protected—the average compensation awarded for a Public Liability claim in 2019 was £13,500.

A welding business that hires anybody must hold a form of employers’ liability, even to protect workers only employed for a short time. And vehicles used by a welding business must be covered by a commercial vehicle insurance policy—personal vehicles used to travel between work sites can be covered by a SD&P policy instead, so long as the policy also covers business use. This may cost more as it protects against the additional risks of business mileage (e.g. unfamiliar roads, driving during peak traffic).

Protecting expensive equipment with a welding tools policy is advisable to replace valuable tools and equipment quickly if they're stolen or damaged in a covered event like a fire. Consider the impact on a client if something goes missing and a replacement can't be sourced quickly. And as there’s a risk of tools getting damaged in transport, have a look into goods in transit policies.

If you’re concerned about how you might fare financially if you were unable to work due to injury or illness, have a look into relevant Personal Accident coverages to make sure you’re safe if something does go wrong.

Yes, self-employed welders need insurance. You generally need the same types of welder insurance whether you're a self-employed sole trader or you run a welding company. (Although a larger business is more likely to need employers' liability insurance than a sole trader, and coverage levels might vary on other types of cover.) If you're employed by someone else they should provide your insurance; but check to be sure.

How much does welding business insurance cost?

The average cost for basic welding business insurance with £2M of Public Liability is roughly £250 per year in the UK. However, premiums will depend on the business size, previous claims history, types of coverage needed and other factors. Below are some sample business insurance costs across different levels of coverage for a sample sole trader welder. Your costs will surely vary from these, but they can give you a general idea of potential costs.

Welding public liability costs considerably more than the average cost of public liability insurance in the UK. Given the risks welders are exposed to, this is fairly unsurprising—most would agree a welder is more likely to be involved in a costly accident than a domestic cleaner, for example.

| Average Cost of Welders Insurance for a sole trader | |

|---|---|

| £2m Public Liability (PL) | £264 |

| £5m PL | £338 |

| £2M PL, £2,000 Tools (not left in van overnight) | £386 |

| £2M PL, £2,000 Tools (left in van overnight) | £418 |

| £2M PL, £5,000 Tools (left in van overnight) | £555 |

| £2M PL, Personal Accident | £370 |

| £2M PL, Personal Accident, £2,000 Tools (left in van overnight) | £524 |

| £2M PL, 1 Employee, £2,000 Tools, Personal Accident | £1189 |

Where Can I Get Quotes?

Compare welder insurance quotes here. Fill out a short form for us and we'll connect you with some of the UK's leading welding insurance companies to help you get the best deal possible.

More Information on Types of Welders Insurance

Public Liability Insurance

Public Liability Insurance for welders helps keep you covered if a third party (client, other supplier, general public) is injured or incurs financial damages as a result of the work you’re doing. It’ll cover you for any legal costs you expend during the process, and any compensation awarded against you (up to the agreed limit of your policy, usually £1M, £2M, £5M or £10M).

Employers' Liability Insurance

Employers' Liability Insurance is required if you employ any staff. It’ll cover you against any claims employees make if they believe you’re at fault for an injury or illness they’ve had while working for you.

It’ll cover your legal costs and any compensation awarded to the employee, and you’ll need to have it even if the employee is only working for you for a short time, they’re being paid cash in hand or even if they’re a family friend.

Tools Insurance

Tools and Equipment coverage will protect your tools if they’re stolen or accidentally lost/damaged. It can help keep your projects ticking when something goes wrong by paying for a replacement/equivalent tool. It's especially useful if you have any expensive or specialist tools that you wouldn't be able to replace immediately if something did go wrong.

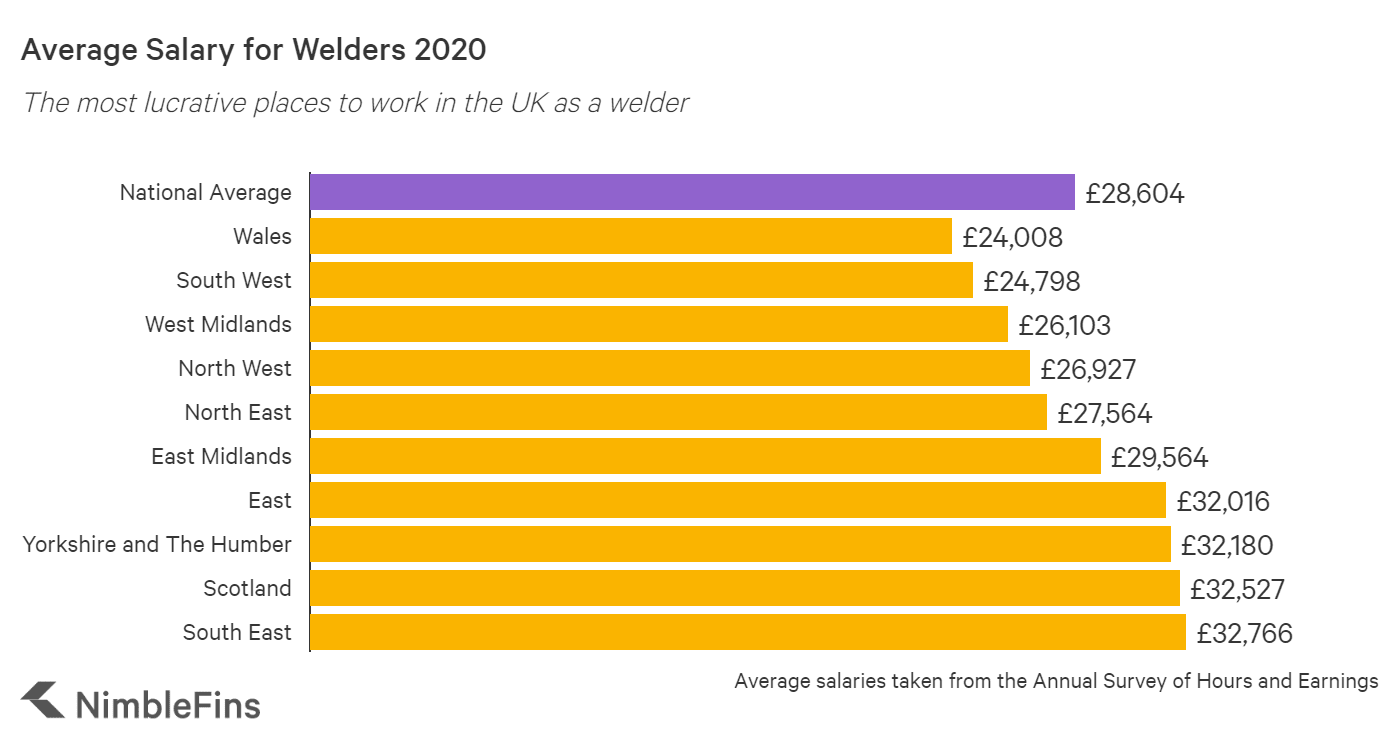

Welder Salary Information

The average salary for a welder in the UK is £28,604 per year. This varies from as low as £24,008 in Wales all the way up to £32,766 in South East (although the Annual Survey for Hours and Earnings doesn't cover London, which often tops trade salary rankings). An aging workforce offers ample opportunities for any budding welders—YouthEmployment estimates that while the demand for welders may reduce by 10% in the next 10 years, nearly 50% of the workforce will be coming to retirement age over the period.

| Region | Average Salary |

|---|---|

| Wales | £24,008 |

| South West | £24,798 |

| West Midlands | £26,103 |

| North West | £26,927 |

| North East | £27,564 |

| National Average | £28,604 |

| East Midlands | £29,564 |

| East | £32,016 |

| Yorkshire and The Humber | £32,180 |

| Scotland | £32,527 |

| South East | £32,766 |

You'll be glad to hear that welding also ranks as one of the UK's most lucrative trades for self-employed tradespeople—check out our article on the topic if you might like to know more about how strong the prospects are for welders compared to other trades.

Quotes were gathered for a sample welder in NW London with no previous welding experience. No fewer than the two cheapest quotes were averaged to generate our results. You may find your costs higher or lower depending on the variables insurers measure your risk profile by.

Salary information was taken from the Annual Survey of Hours and Earnings.