Window Cleaner Insurance: What Do I Really Need?

Find window cleaner quotes today.

Powered by QuoteZone.

Compare Quotes

- Rated 4.7 out of 5 stars on Reviews.co.uk

- Over 300,000 QuoteZone quotes completed per month

- Fill out only one form

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

As seen on

What is Window Cleaning Insurance?

Window cleaning can be a risky business—so it's critical to get the right insurance in place to protect you and your business from certain financial disasters. This is true whether you're working as a contractor, running your own business or working for somebody else’s.

This article will tell you everything you need to know about window cleaning insurance, from types of cover, costs and who needs to buy it. If you still have questions, fill out a quote form and an insurance provider call you back on the phone.

Types of Insurance for a Window Cleaner

While working as a window cleaner, it’s important to keep yourself, your employees and other third parties (other window cleaners/contractors, members of the public/clients) protected. There are a number of different insurances available that you’ll want to be aware of.

Public Liability Insurance

Public Liability insurance for a window cleaner keeps you covered financially if a third party (e.g., client, member of the public, workers from other companies) is injured or incurs damages to their property or equipment while you’re working. It covers both the cost of the damages and your legal expenses up to the value of your policy (in the UK these are typically £1 million, £2 million, £5 million or £10 million).

Public Liability isn’t a legal requirement, but it is often a contractual one; most commercial clients and many residential customers will require proof of cover before you start. Reflecting the latest 2025/2026 data from the Association of British Insurers (ABI), the average settlement for a public liability claim has likely risen to approximately £16,200^. With legal costs and medical inflation increasing, a single accident—such as a falling bucket or a trip over a hose—could be financially devastating without the right protection.

- Injury Example: While putting your equipment away in your van, a member of the public trips over a ladder you’ve left on a public walkway. They’re unable to work for 2 weeks, so sue you for their lost wages.

- Property Damage Example: While moving your equipment into your client’s home, you damage the front entrance. They sue you for the value of the damage.

Employers’ Liability Insurance

Employers' Liability insurance is a legal requirement for any business that has employees, irrespective of whether they are full-time or part-time. It covers you in the event that somebody is injured or becomes unwell as a result of their work for you, and sues you for damages as a result. Employers’ Liability will cover you both for the cost of any settlement and your legal defence.

Given the risks window cleaners expose themselves to on a daily basis (e.g., heights, solvents), it’s important to make sure you’re covered against any potential risks for an appropriate amount.

- Employers’ Liability Example: A temporary employee you’ve hired to help with a large piece of work trips over a piece of equipment left on the floor. They say your company is at fault and claims compensation.

Professional Indemnity Insurance

Professional Indemnity insurance protects you in the event that a client is unhappy with the work you’ve completed. Irrespective of whether it was due to a mistake your company made, a misunderstanding with the client, or perhaps they’re just not satisfied with the work, professional indemnity will cover your legal cost and any compensation required.

- Professional Indemnity Example: After completing a piece of work, your client is dissatisfied with the cleanliness of the window and sues you for the value of your work and the cost of the reclean.

Business Van Insurance

If you own a van that you use for work purposes, such as carrying your tools and equipment from client to client, you’ll require a form of business van insurance. It will cover your vehicle for the additional wear and tear that comes with the additional mileage of using it for work purposes, and will include your social, domestic & pleasure coverage within it, so you’re covered at all times.

Business van insurance works similarly to your traditional car/van insurance, so consider what providers do and don’t include as standard, and think about which optional extras (breakdown cover, windscreen cover etc.) might make sense for you.

- Business Van Insurance Example: while travelling to a client’s property, you’re involved in an accident. Your comprehensive business van insurance covers the damage and repair cost to your vehicle (you can read more about the different levels of vehicle cover here)

Tools/Equipment Insurance

Tools and equipment cover can be valuable for any business using expensive tools for their work. Your insurance policy can cover you for the cost of these tools, allowing you to get back to work as quickly and efficiently as possible, avoiding any potential issues with your client over timeliness.

While signing up for your tools insurance, you’ll need to tell your provider whether or not you intend to keep the tools in a van overnight. Keeping them inside your van, and not in a secure location, can increase the cost of your policy, as they’re more liable to be stolen.

Income Protection and Critical Illness Insurance

These insurances are designed to protect you in the event that you’re unable to work due to illness or injury. Income Protection insurance will cover you if you’re not able to work as the result of a short-term injury/illness, and Critical Illness insurance will pay out a one-off sum if you can’t work because of a long-term/critical illness or injury.

- Income Protection Insurance Example: while out on a cycle ride with your family, you fall and are hurt, and are unable to work for a month. Your income protection coverage pays you for the month you’re not working (Which? estimates this is typically 50-70% of your monthly income

Do Window Cleaners Need Insurance?

Yes, most window cleaners require some level of insurance to cover themselves against potential risks. And while some insurances aren’t legally required, you should consider the costs of a claim being made against your company, or your tools being damaged/stolen. Claims against businesses for injury, illnesses or issues with the work aren’t cheap, so consider whether you’re comfortable operating with the risk of a potential claim against you and your business.

As a minimum legal requirement, you’ll require employers’ liability if you’ve hired any employees, irrespective of the agreement—whether it’s a one-off engagement, they’re a family friend, or they’re being paid cash-in-hand. If you’re not covered with employers’ liability then it’s illegal to hire any members of staff.

If you’re using your personal vehicle for business purposes, make sure you’ve upgraded your social, domestic & personal policy into a business use vehicle insurance. If you’re using your vehicle for business purposes (even if the accident occurs while you’re driving for personal reasons), and you fail to inform your insurer, you risk voiding your coverage and driving uninsured.

Many clients won’t engage you if you don’t have public liability insurance to make sure that they, their property, and other members of the public are protected in the event of any damages or accidents. And if you’re working on larger/corporate projects, you should consider a form of professional indemnity in case of an error or if the client is unhappy with the work. If it’s an expensive project, you could be liable both to return the fee from the client and cover the cost of the work being redone.

Tools and equipment cover will insure you for the value of your tools up to a certain value (typically in sets of £1,000—so £1,000, £2,000, £3,000 etc.) in the event that they’re damaged or stolen. It’s especially worth considering if you have expensive, difficult to replace tools that could delay the completion of work and impact your relationship with the client.

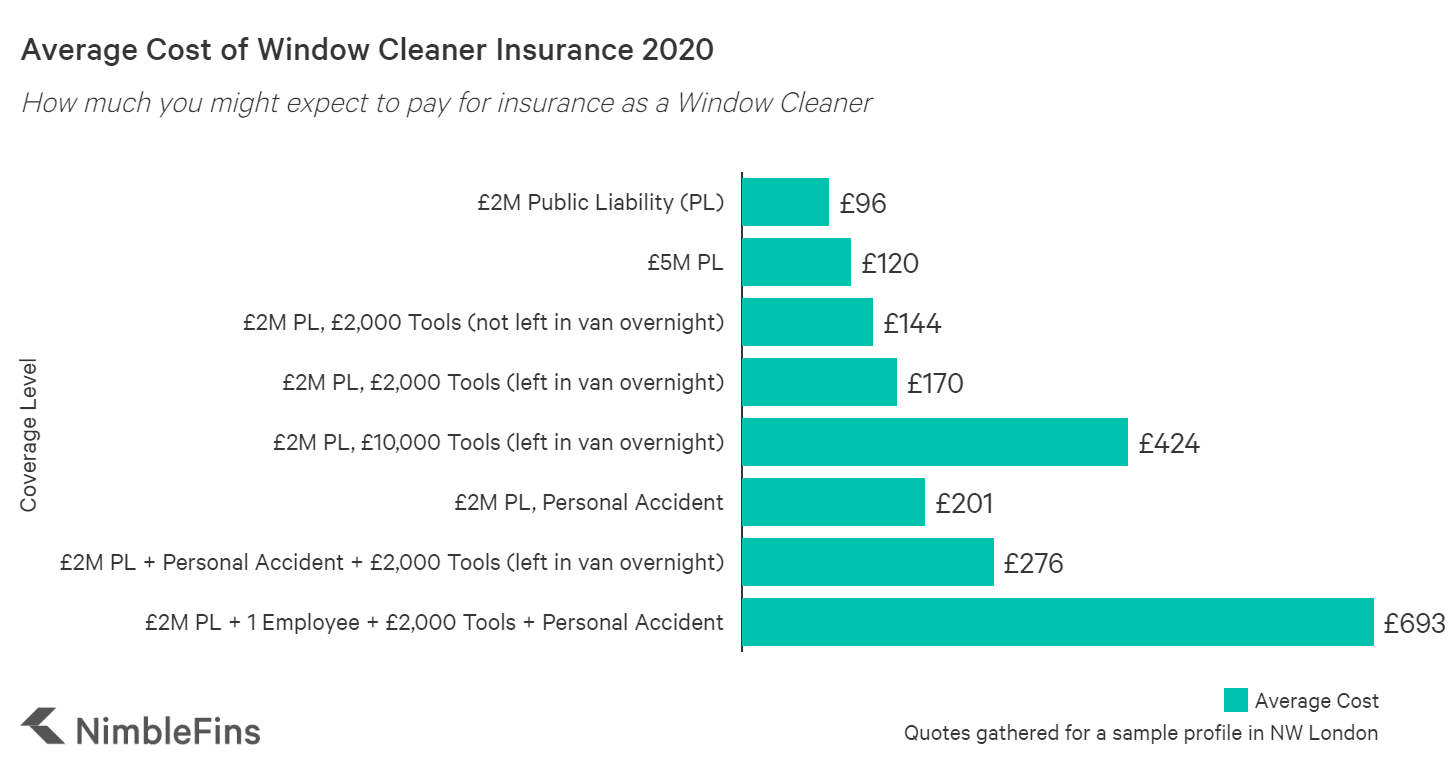

What Are The Typical Insurance Costs for a Window Cleaner?

Below is a breakdown of the average cost of quotes we received from providers to highlight how much you can expect to pay, and the cost difference of adding additional coverage/higher values of protection.

| Average Cost of Window Cleaner Insurance | |

|---|---|

| £2m Public Liability (PL) | £108 |

| £5m PL | £135 |

| £2M PL, £2,000 Tools (not left in van overnight) | £162 |

| £2M PL, £2,000 Tools (left in van overnight) | £194 |

| £2M PL, £10,000 Tools (left in van overnight) | £475 |

| £2M PL, Personal Accident | £225 |

| £2M PL, Personal Accident, £2,000 Tools (left in van overnight) | £312 |

| £2M PL + 1 Employee + £2,000 Tools + Personal Accident | £785 |

Why does hiring an employee add so much cost?

Adding employees increases the cost of personal accident cover if you provide it, because having more people increases the odds of an accident occurring. In addition,you also have to add employers’ liability into your insurance package if you hire anyone.

How much is public liability insurance for a window cleaner?

A window cleaner starting their business in 2026 can expect to pay from around £108 for annual public liability insurance. While you may find lower rates with high experience or by choosing a higher excess, paying monthly will usually increase the total cost due to interest. This £108 baseline remains higher than the current 2026 UK median cost for public liability insurance (which sits at approximately £92), reflecting the inherent risks of working at height and the potential for water or chemical damage to third-party property.

Why is public liability more expensive for window cleaners?

Many professions don’t require you to work with solvents, equipment or heights. The work window cleaners do is considerably more risky than being sat behind a desk all day and so you’ll need to be protected appropriately!

How can I save money on my window cleaner insurance?

As mentioned above, traditional methods such as more years of experience and storing your tools in a lockup overnight (not in your vehicle) will reduce your costs. You may also find it cost-effective to take out different policies from different providers, but keep in mind you’ll have a few different points of contact, which can get confusing.

You’ll naturally save money on your insurance if you’ve never had a policy rejected or had any criminal convictions.

You can also expect your insurance to cost more if you work at any of the following locations, due to the obvious increased risk of working on them, so keep this in mind when considering where you’re taking your work:

- power stations

- nuclear installations

- oil, gas or petrochemical works

- airports, aircraft, etc.

- watercraft, docks, harbours

- railroads

- medical facilities

Where can I get window cleaner insurance quotes?

Compare window cleaner insurance quotes here—after filling out a short form you'll receive quotes from up to five insurance providers. You'll have the chance to talk on the phone if you have questions that you want to discuss. Then choose the cover that offers the best price and features for your needs.

Window Cleaner Current Industry Earnings (March 2026)

- Salary per annum: £25,000 to £32,000 (Employed); up to £40,000+ (Self-Employed)

- Pay per hour (Median): £12.71 (Aligned with the 2026 National Living Wage)

- Typical hours per week - 37-40

Quotes were gathered for a window cleaner looking to get into the industry for the first time. Our sample profile lived in the outskirts of London, and wasn’t covered for some of the more dangerous locations mentioned above. No fewer than the three cheapest quotes were averaged to give us our results. Our sample profile had no prior convictions and had never been denied insurance. In 2026 rates were adjusted upwards to reflect current market conditions.

Your costs may be higher or lower depending on the difference in variables your risk profile is measured by.

^The £16,200 average claims figure is a projected industry benchmark for 2026, derived from the 17th Edition of the Judicial College Guidelines (JCG) combined with current ABI (Association of British Insurers) claims data.