Workshop Insurance: What Do I Really Need?

Find workshop insurance quotes today.

Powered by QuoteZone.

Compare Quotes

- Rated 4.8 out of 5 stars on Reviews.co.uk

- Over 300,000 QuoteZone quotes completed per month

- Fill out only one form

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

As seen on

Workshop Insurance Wiki

Workshops contain expensive tools and equipment and can be dangerous places—especially if you have visitors—so it's critical to get the right insurance to protect yourself against disasters such as theft or injury. Read our in-depth guide to learn about the different types of cover you might need, as well as typical costs. For quick definitions of each type of cover, see the blue boxes below and use the examples to see how the right insurance coverage can work for you and your workshop.

To find out how much you'll need to pay for insurance for your workshop, fill out a quote form where you'll fill in some basic information then receive quotes from up to 5 insurance providers. You can ask questions if you have them, then pick out the best policy for your budget and needs.

Popular Types of Insurance for a Workshop

If you have a workshop you should learn about a few key types of insurance to decide if they apply to your situation or not—public liability, employers' liability and contents/tools/equipment cover. There are some other add-on extras you might want as well such as personal injury. Let's run through the list to explain what each type covers to help you decide if you need it or not.

| Common Types of Workshop Insurance & What They Cover | ||

|---|---|---|

| 1. | Public Liability | Covers if a visitor or other third party is injured while at your workshop |

| 2. | Product liability | Covers if someone is injured or falls ill due to a product you design or sell (often combined with public liability) |

| 3. | Employers' Liability | Protects against related liability claims if an employee is injured or falls ill due to work |

| 4. | Workshop Contents | Protects the contents of your workshop (can include tools and equipment) against loss, damage or theft |

| 5. | Stock | Covers raw materials, works in progress or finished goods for sale |

| 7. | Personal Accident | Personal accident insurances can provide money if you or an employee are off work due to a job-related injury or illness |

| 8. | Business Interruption | Can reimburse you against lost revenues and pay for temporary workshop space in the event of physical damage preventing you working, such as flood or fire (but not usually situations like coronavirus) |

| 9. | Commercial Buildings | If you own your workshop premises, buildings insurance can cover damage or loss due to events such as fire, flood or theft |

Here are some examples of how these insurances can protect a workshop:

Workshop Insurance Examples

- Public Liability: A customer visiting your workshop trips over a toolbox left on the ground and is injured. Public liability insurance covers your legal defense fees and any compensation you're required to pay to the customer to compensate them for damages.

- Employers’ Liability: (If you're a professional and have hired anyone) An employee suffers from a back injury while carrying timber and blames your business for supplying poor equipment. They sue for damages. Employers' liability insurance covers your legal defense fees and compensation you're required to pay to your employee as the result of a lawsuit against you.

- Workshop Contents & Tools Example: A fire in your workshop results in the loss of all furniture (e.g., work tables), fixtures (e.g, lights), tools and equipment. Workshop contents insurance pays to replace the lost equipment, fixtures and fittings. (Repairs to the premise's structure—e.g., pipes, floors, walls, electrics, etc.—would fall under the buildings insurance.)

- Buildings: The same fire damages key structures of your building, requiring work to replace the plumbing, electrics, floors, windows, etc. This repair work could be covered by a buildings insurance policy on your workshop.

- Business Interruption Example: A severe storm damages the roof of your workshop, making it unsafe to inhabit until repairs are made. Business interruption insurance can cover lost revenues over this period of time, and/or fund an alternative work space.

FAQs

Yes, you should probably have insurance for your workshop, although the type of coverages you need will depend on whether your workshop is a 'hobby shop' or your business premises—a hobbyist might only need buildings and contents cover, while a business might also need employers' liability (if you hire anyone), public liability (if any customers or other members of the public visit your workshop or you work at your client's premises), etc. Click here to learn more.

Depending on your policy, some home insurance will cover garages or outbuildings, but there is typically a theft from outbuildings limit of £2,500, although some policies impose a £1,000 limit, either of which will be insufficient to cover expensive tools for a well-stocked workshop. Contact your home insurance to ask if they'll cover your home workshop, but in all likelihood you'll need a separate workshop insurance policy.

With so many factors affecting the cost of insurance, it's hard to say which are making the difference for you. The value of your tools and equipment certainly plays a part, as does the type of building structure that houses your workshop and the security of it. For example, the cost of workshop insurance essentially triples if you add £2,500 stock, £5,000 tools and £10,000 plant machinery to your public liability cover.

Save money on workshop insurance is similar to saving money on any type of insurance. Here are some examples of factors that can lower your workshop insurance premiums:

- No previous claims/convictions

- Lower levels of cover

- Strong security in your workshop (e.g., alarms and 5-lever mortice deadlocks)

- Compare quotes in the market before you buy

If your workshop is based at home, you might need separate buildings/contents insurance beyond what your home insurance will cover—call your home insurer first to ask what they will cover. A proper workshop policy can usually cover your tools and equipment at much higher levels than you'd get from home insurance. And if you have visitors to your workshop then strongly consider public liability insurance.

It's critical that you keep a record of your tools and their value. Ideally, you've kept all your purchase receipts. It's also a good idea to take high-resolution photos of your workshop and all of your tools and equipment (with identifying labels or other details clearly displayed) in case you need proof of the value of your tools in a claim situation.

Which Types of Insurance do Workshops Need Most?

There are a few main types of insurance that any workshop should consider buying. For starters, property insurance for your building (if you own it), tools, equipment and machinery can protect against perils like fire, floor, theft and more. You can also get cover for your stock, including raw materials, works in progress and finished goods. If you have visitors from any third parties like customers then a suitable public liability insurance is critical for protecting against liability claims of accidental injury or damage while visitors are on site.

If you hire anyone to assist in your workshop, employers' liability insurance is a legal requirement —even if your staff is temporary, part time or paid in cash. Employers' liability insurance (EL) premiums have risen significantly over the last few years due to increased claims inflation. Business interruption insurance can help keep your business alive if your workshop is physically damaged by fire or flood, by reimbursing you for some lost turnover or helping to secure an alternative workspace.

You may also want personal accident cover to provide a financial buffer if you're injured when working. During the quote process you'll typically be able to add on these extras if you want them.

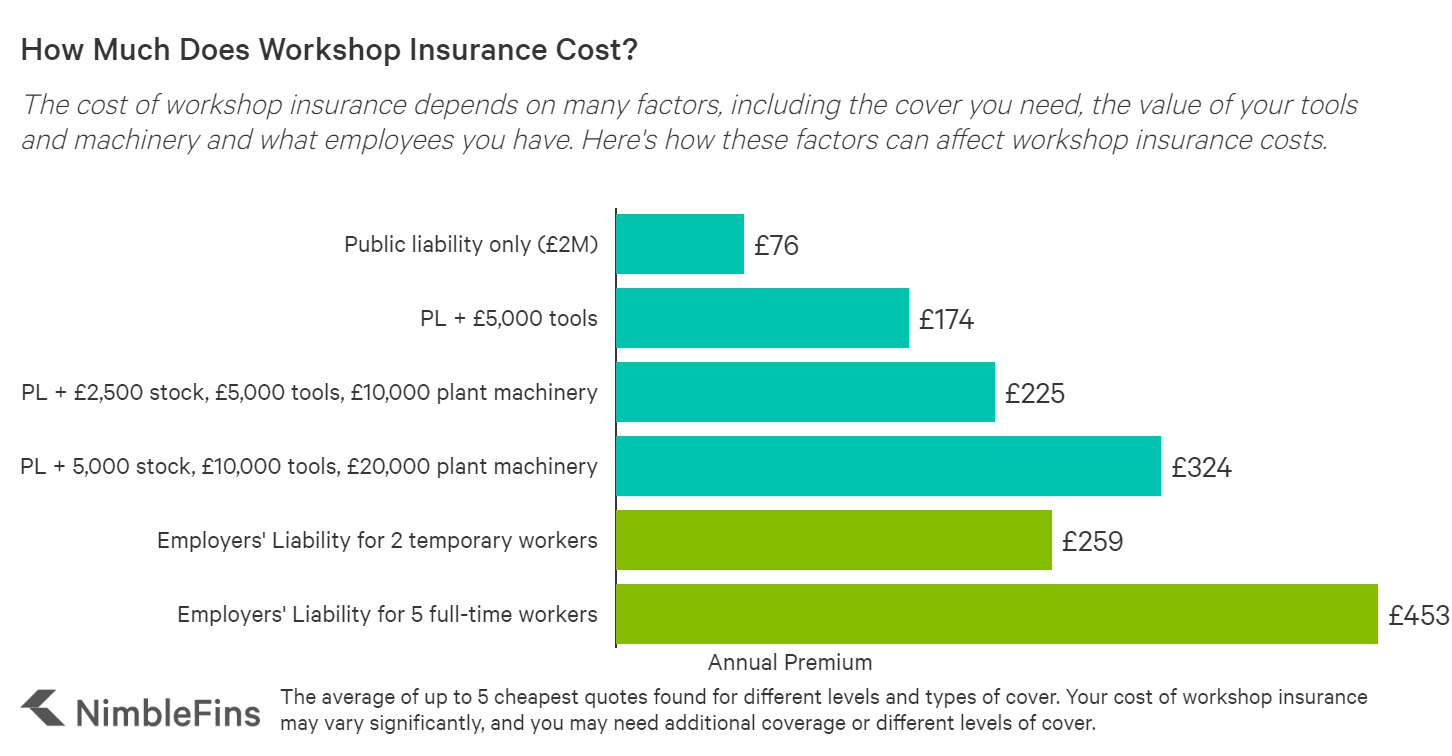

How Much Does Workshop Insurance Cost?

The average starting cost of workshop insurance in the UK has risen in the 2026 market. For a self-employed tradesperson, Public Liability alone now typically starts from £104 to £115 per year. Once you add Tools cover (approximately £69 to £100 for £5,000 of coverage) and protection for stock or plant machinery, a comprehensive combined policy is likely to start at over £325 per year for most workshops. If you hire any workers to help you'll need to add employers' liability which can easily double the cost of your workshop insurance, depending on the number of employees and how much they work for you.

In short, costs vary significantly from business to business, depending on factors like the type of work you do, the amount of tool, equipment and machinery you're covering (whether you own it or it's hired), the type and level of coverage you want, the number of people you employ, etc. To give you a rough idea of how costs can vary, we've run some sample quotes to insure a typical workshop in the UK. Here's what we found.

| How Much Does Workshop Insurance Cost? | Estimated Sample Costs |

|---|---|

| £2M public liability | Annual Premium |

| Public liability only (£2M) | £115 |

| PL + £5,000 tools | £215 |

| PL + £2,500 stock, £5,000 tools, £10,000 plant machinery | £275 |

| PL + 5,000 stock, £10,000 tools, £20,000 plant machinery | £375 |

| Employers' Liability for 5 full-time workers | £753 |

We also took a quick look comparing insurance for plant machinery owned vs. hired. By hiring in your machinery instead of owning it, you could save around £35 a year in plant insurance (assuming the value of the machinery you own/hire is at most £10,000).

Where can I get quotes for workshop insurance?

Compare workshop insurance quotes here—after filling out a short form you'll receive quotes from up to five insurance providers. You'll have the chance to talk on the phone if you have questions that you want to discuss. Then choose the cover that offers the best price and features for your needs.

More Information on Types of Workshop Insurance

If you want to better understand what the primary types of workshop insurance typically cover, see the definitions below.

Public Liability Insurance

Public Liability Insurance (PL) is an important cover for workshops if you have any visitors, such as customers. PL insurance protects against claims that you're responsible for any accidental injury or property damage on site by members of the public and, if you're sued, can cover the cost of your legal expenses as well as any compensation you're found liable to pay.

While not required by law, workshops that allow visitors will find that public liability is certainly worth the cost—consider that AXA previously reported an average public liability settlement of £13,500, but modern legal and medical costs mean major claims can easily reach six figures.

Employers’ Liability Insurance

Employers' Liability Insurance (EL) is a legal requirement for your UK workshop if you have any employees, even temporary or part-time staff. EL protects you against any injury and illness claims made by workers and can cover both your legal defense fees as well as any compensation you're found liable to pay them. With non-fatal workplace injuries topping 650,000 a year in the UK, this cover is not only required by law, it's essential given the physical nature of workshop tasks. According to the 2024/25 HSE statistics, roughly 59,219 of these injuries were serious enough to be reported by employers under RIDDOR.

Workshop Contents & Tools Insurance

Most workshops will want Tools Insurance to protect financially against the loss, damage or theft of valuable tools—property cover can be expanded to include plant machinery, stock, and other workshop contents like fixtures and fittings.

In addition, workshops owners might want to consider other types of business insurance such as personal accident cover, business equipment (e.g., computers), legal expenses, and more. When you're getting quotes, you'll typically be able to add on these extras if you need them.

Workshop Insurance Companies

If you get quotes through our partner QuoteZone (click here to get started), you'll fill out a short form then get quotes back from up to five of the following insurance providers.

- 1st Choice

- Allied Wessex Dental Insurance

- Arthur J Gallagher & Co.

- Be Wiser

- BP Insurance Brokers

- Brady Insurance

- Compare Insurance

- Coversure Harborne

- Crosby Insurance Brokers

- Edison Ives Insurance

- Export and General

- Gallagher Insurance

- Greenwood Moreland

- GSI Insurance

- Insurance Protector

- Konsileo

- Nova Insurance

- Plan Insurance

- QCIS

- Quote Four Ltd

- SJL Insurance

- The Retail Mutual

- UKinsuranceNET

Methodology

Quotes were gathered for a sample workshop in the South of England. No fewer than the four cheapest quotes were averaged to give us our results. Our sample profile had no prior convictions and had never been denied insurance. Your costs may be higher or lower depending on the difference in variables your risk profile is measured by.