The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Average Cost of Handyman Insurance (2026)

Get Handyman Insurance

Powered by QuoteZone

Compare Quotes

- Rated 4.8 out of 5 stars on Reviews.co.uk

- Over 300,000 quotes completed per month

- Fill out only one form

The average cost of self-employed handyman insurance starts from around £9 a month or £75 a year in the UK, but certain factors can greatly increase the cost. For example, adding extras like tool cover or personal injury insurance or hiring any employees will bump up the cost of business insurance. Whether you're starting a new business or are an established handyman, here's what you need to know about costs for handyman insurance to be well informed about pricing in the UK market.

Not sure which insurance coverages you need as a handyman?

Read our in-depth guide to handyman insurance requirements here.

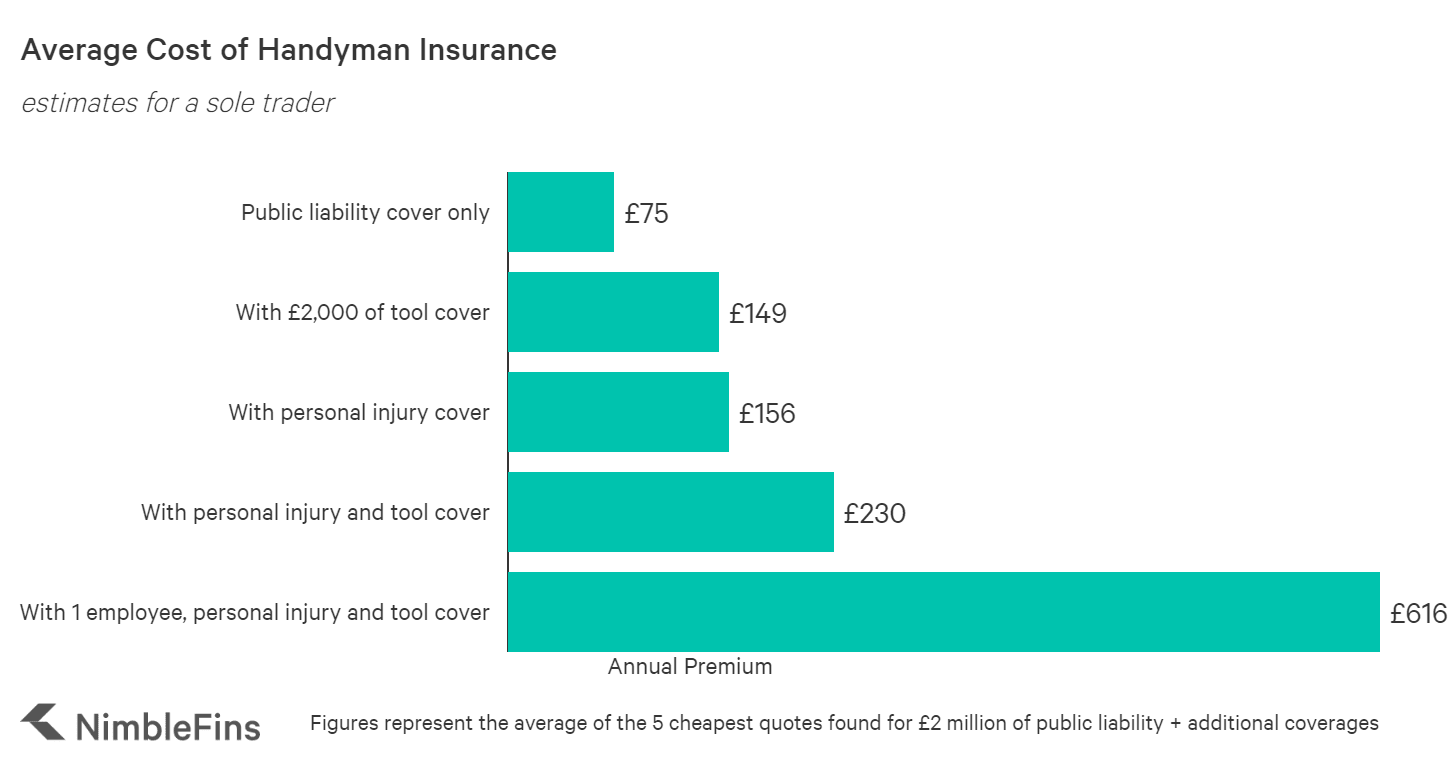

Average Cost of Handyman Insurance

The average cost of public liability insurance is £75 to provide £2 million of cover for a self-employed handyman working alone (which is higher than the average cost of sole trader public liability insurance in the UK). However, the cost of handyman insurance can rise by up to 10X if you add extra coverages or hire any employees.

For example, handyman cover with £2 million of public liability, £2,000 of tool cover and personal injury all-in costs around £230 a year. Hire 1 permanent employee and this rate will rise to over £600 (if anyone is working for you, you're required by law to hold employers' liability insurance, which is costly).

| Starting cost of handyman insurance (per year) | |

|---|---|

| Public liability cover only (£2 million) | £75 |

| Public liability with £2,000 of tool cover | £149 |

| Public liability with personal injury cover | £156 |

| Public liability with personal injury and tool cover | £230 |

| Public liability with 1 employee, personal injury and tool cover | £616 |

Given that a handyman can earn more than £20 to £30 an hour, paying for the bare minimum public liability only costs a few hours of work—it's well worth it.

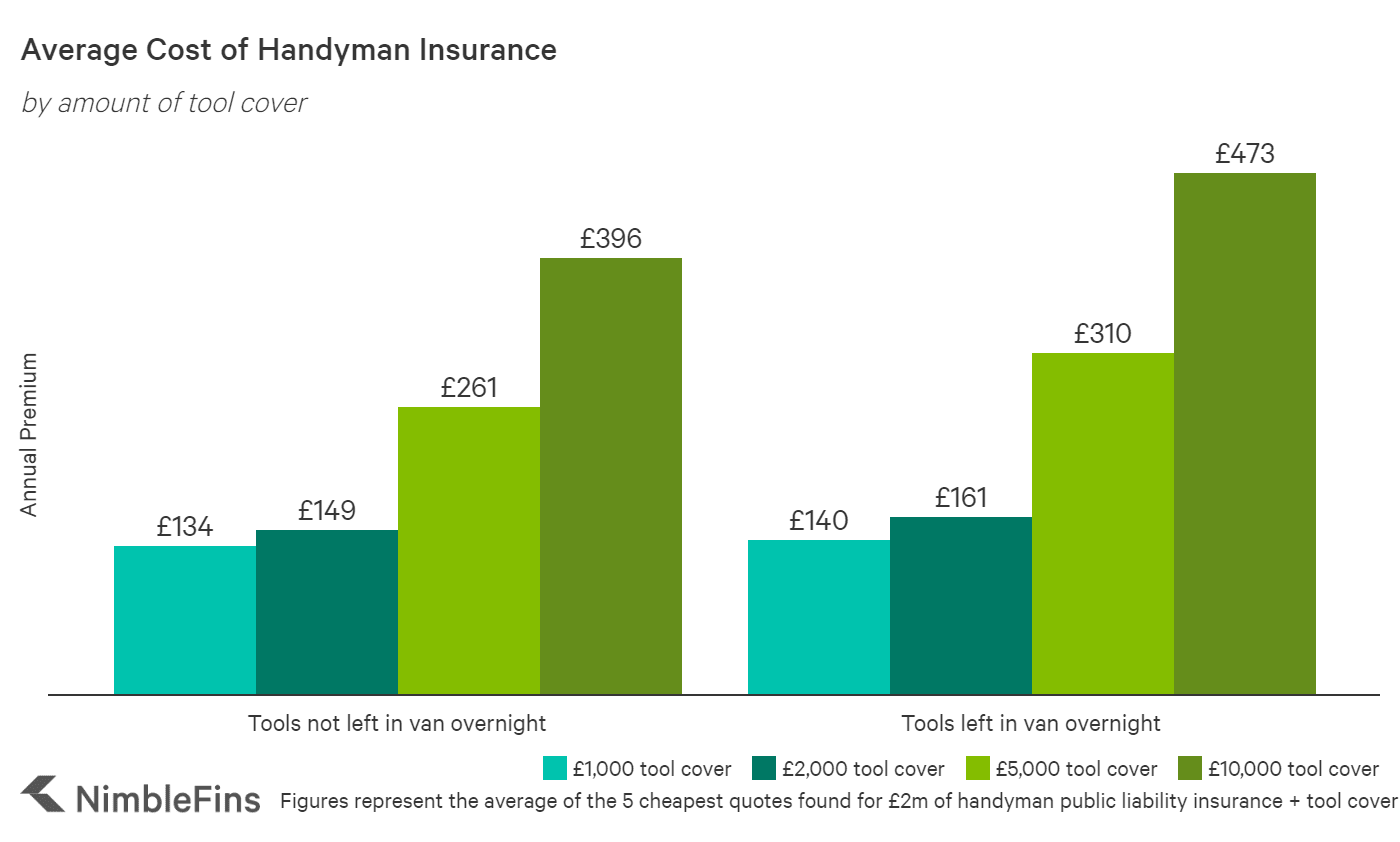

How does tool cover affect handyman insurance costs?

Tools can cost thousands of pounds to replace if they're lost, stolen or accidentally damaged, which is why many handymen opt for some amount of tools cover. The higher the level of tools cover, the higher the additional premium—however, each additional £1,000 of tool cover gets cheaper to add.

For example, the data in our study showed that the first £1,000 of tool cover adds around £60 (or £65 if you leave them in a van overnight) to the cost of a £2m public liability policy. The next £1,000 of tool cover would add another £15 - £20 to your premium, and so forth. The following graph shows the cost of £2m public liability and tool cover, for various levels of tool cover.

How does personal injury cover affect handyman insurance costs?

Our recent test of the market showed that adding personal injury cover to your handyman insurance would typically add around £80 to your premium.

For example, the data showed that for a sole trader with £2 million of public liability insurance, adding personal injury would increase their all-in premium from around £75 to £155, an increase of £80.

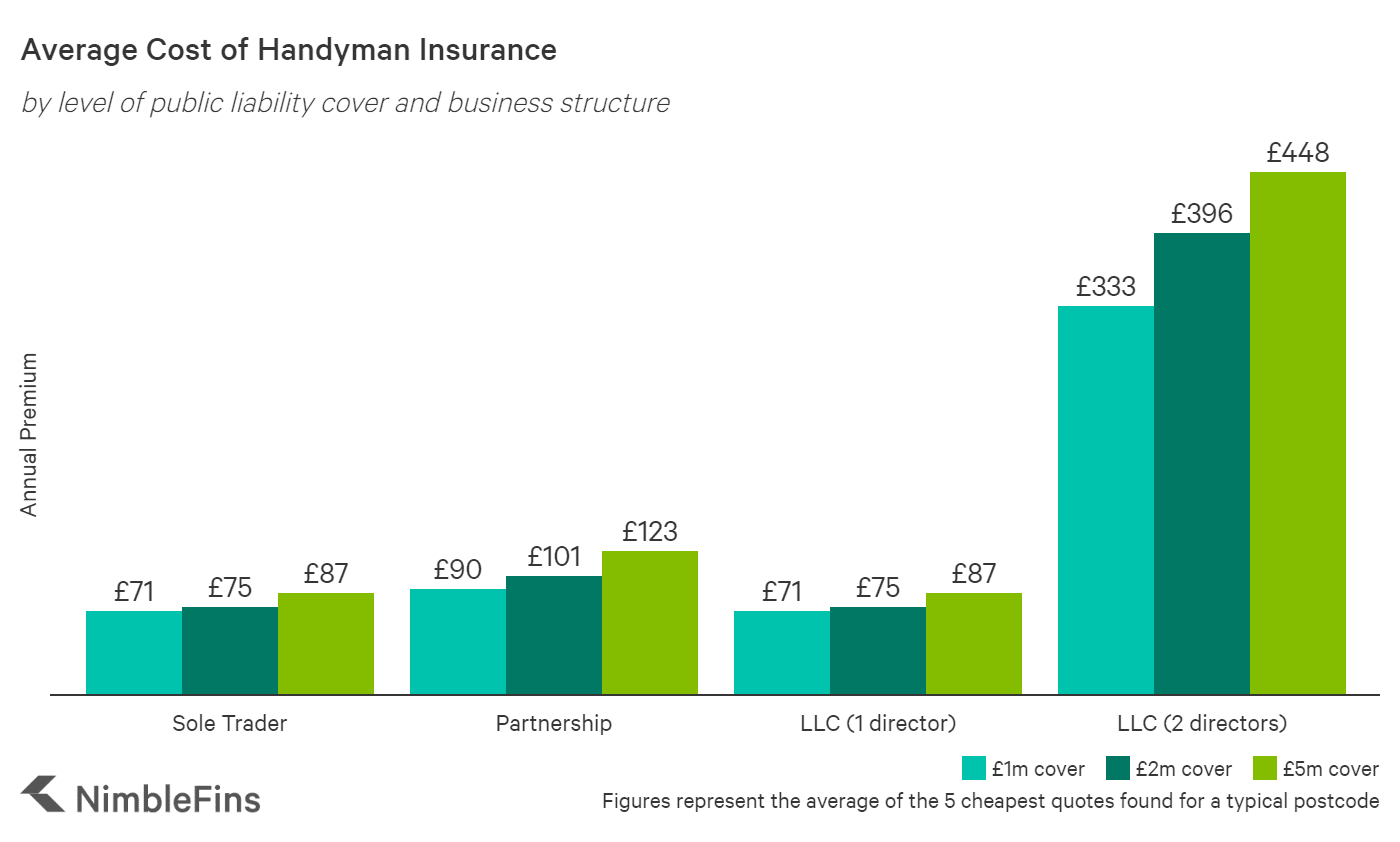

How does coverage level affect handyman insurance costs?

Another factor that has an impact on the cost of your handyman business insurance is the level of cover. The higher the cover limits, the higher the rate. However, additional cover typically costs less per £1 million of cover than you pay for the first £1M of cover.

For example, a sole trader would pay on average £71 for the first £1 million of public liability handyman insurance, but just £4 for the next million pounds of cover. In the chart below you can see how handyman insurance costs increase with coverage levels and across different business structures.

Your business structure also plays a role here, with additional coverage costing more for certain types of businesses. In particular, an LLC with 2 directors will have the largest rate jump for higher levels of cover, as you can see in the chart above.

How does hiring employees affect handyman insurance costs?

When you hire an employee, you're required by law to have employers' liability cover in place—even if they're family, they're paid in cash and/or they work on a part-time basis. Employers' liability can be costly, increasing your basic insurance costs by up to 5X or more.

For example, our study showed that it would cost around £272 to add employers' liability insurance to self-employed handyman's insurance coverage. But this can vary significantly from one insurer to the next.

Other factors that influence your handyman insurance rate

Many additional factors can have a bearing on the cost of handyman business insurance. For instance, where you live and work can impact prices by 20% or more.

In addition to extras like employers' liability, personal injury and tool cover, some businesses require or opt for additional coverages like legal, stock and business and office equipment insurance—which further add to your rate.

How to Save Money on Handyman Insurance

There are a few ways to try to save money on your handyman business insurance. First, be sure to compare quotes from more than one source, because rates can vary greatly from firm to firm. For example, in our study the range of quotes for a self-employed handyman with £2M of public liability cover ranged from £68 to £179, a difference of 162%. Using a comparison site can help in this regard, saving you time as well as money.

Second, insurance firms may let you choose a higher excess to essentially give you a discount on your handyman insurance—but a higher excess is not necessarily a good idea. The premium reduction is often quite small compared to the additional excess you'd need to pay in the event of a covered claim.

Third, perhaps the simplest way to save money on handyman insurance is paying annually (upfront) for the whole year. This can save you around 12.5% on your handyman business insurance costs each year.

Methodology

We started by gathering dozens of quotes for public liability handyman insurance to find out what a typical handyman might pay for cover. We then varied quotes by different factors like the types of additional cover, employees, etc.

Please note that insurance quotes can vary noticeably depending on the situation. As a result, your business insurance premium might be significantly higher or lower than the rates mentioned here. Use this information just as a rough guide to help you learn more about handyman insurance costs and how different factors can affect insurance premiums in general.