Claims Made vs. Claims Occurring Business Insurance

Find business insurance quotes today.

Powered by QuoteZone.

Compare Quotes

- Rated 4.8 out of 5 stars on Reviews.co.uk

- Over 300,000 QuoteZone quotes completed per month

- Fill out only one form

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

As seen on

Claims Made vs. Claims Occurring

What if you carry out work while you have a valid insurance policy, but you're later sued for negligence after your insurance policy has ended—are you covered or not? It depends on whether your policy was written on a "claims made" or "claims occurring" basis. Here's what you need to know about this often overlooked but important distinction.

Table of Contents

- What is claims made insurance?

- What is occurrence insurance?

- Which is better: claims occurring or claims made policies?

- What are the limits of insurance for claims occurring policies and claims made policies?

What is a Claims Made policy?

Claims Made

You're covered only for claims made during your period of insurance.

'Claims made' insurance policies only pay out for valid claims made while the policy is still active (that is, during the policy period), and not afterwards. This is important because some risks are not discovered right away, say in the case of liability for poor professional advice, in which case claims might not be filed for years after the alleged act or decision. If a policy expires or is cancelled, you're not covered—even if the incident occurred while a policy was active.

Beyond that, to be protected with a claims made policy, you need to be insured both at the time of the alleged incident and also when a claim is made.

Example:

- A management consulting firm held professional indemnity insurance in 2024. During 2024 the firm gave acquisition advise to a client, which was followed. In 2025 the client faced a significant financial loss related to the acquisition, which they blamed on negligent professional advice by the management consulting firm. Although the professional liability policy was active at the time the advice was given, the claim would not be covered because it was made after the policy had lapsed.

What is a retroactive date in a claims-made policy?

To be protected by a policy sold on a 'claims-made' basis you need cover both when the damage occurred and when the claim is made. To ensure you're covered continuously, across years and even if you switch insurers, claims made policies can be back dated to a 'retroactive' date. This essentially means you're protected against all incidents since the retroactive date so long as your cover remains in force.

If you switch insurers for claims-made cover, your new insurer should backdate your policy to a retroactive date (say to a previous retroactive date or the date you were first covered by the first insurer) which essentially ensures you have uninterrupted insurance—even if part of the time your cover was with a different insurer. If you've had uninterrupted cover then your retroactive date will be earlier than your policy start date.

Example:

- You held a contract for professional indemnity insurance with insurer X for one year from January 2024 until December 2024, at which point you switch to a new insurer Y. Insurer Y records a retroactive date of January 2024 on your new policy, since you've had cover since then (albeit with two different insurers). So long as your policy remains valid with insurer Y, you'd be covered by insurer Y for any acts that occurred since the retroactive date of January 2024 (but not before).

What is run-off coverage on a claims-made policy?

Run-off cover is essentially a form of professional indemnity insurance for businesses no longer actively trading. It covers work done in the past when your business was active (and covered by a valid policy). Since runoff insurance doesn't cover new work, it is usually cheaper per year than an active professional liability insurance policy.

Runoff policies are often sold as packages which cover you for several years after ceasing to trade. As such they can look more costly up front, but in fact will protect you in an ongoing manner until the risk of a claim has mostly disappeared, which is reflected in the cost. You should check with your current insurer what their runoff policy terms are at renewal, as in the years leading up to your retirement you will likely need to switch to an insurer with favourable terms, as insurers don’t like to quote businesses for runoff cover unless they have held their policy for at least a year beforehand.

Run-off insurance can be critical if your line of work requires professional liability insurance and you retire, close or sell your business. If you stop trading you certainly don't want to continue paying full professional liability insurance premiums, but you still need some protection in case a client makes a claim against you later on—that's where run-off insurance comes in.

Any professional who is changing careers or retiring should consider buying a "run-off" professional liability policy. This protects you against new claims that are made after your professional indemnity insurance expires or has been cancelled. According to information from Nelsons Solicitors, new professional negligence claims can be made up to six years after the damage, so you consider a run-off policy that covers you for up to 6 years (depending on your particular risks).

Example:

- An accounting company stopped trading in 2024 and lets their professional indemnity insurance expire that year. In 2025, a client discovers that professional advice given by the company a year earlier resulted in a financial loss for the client. The client sues, but the claim would not be covered even though the advice was given in 2024 while the liability policy was active. Runoff cover, however, would cover the claim.

What is a Claims Occurring policy?

Claims Occurring

You're covered for incidents that occur during your period of insurance, even when claims are made years later and you're no longer paying for insurance.

Claims Occurring insurance protects against loss or damage that occurs during the period of insurance (which is typically 12 months long)—even if the loss does not come to light until much later, even after the policy has expired or been cancelled.

A very common type of business insurance that is written on a claims occurring basis is employers' liability insurance. It's critical for employers' liability to be claims occurring to protect against long-term health impacts, for instance of asbestos exposure, that may only be discovered years later.

In fact, there's even an organisation to help employees affected by a work-related injury or illness to find the information they need to make a claim, even years after an incident or after their employment has ended: the Employers' Liability Tracing Office.

Example:

- An employee working for your cleaning company uses hazardous chemicals supplied by your business. Years later, after your company has ceased trading, they suffer ill health effects, and blame your company. They contact the ELTO to find the insurance company that provided your business's employers' liability insurance to initiate a claim.

Which is best: claims occurring or claims made policies?

There are pros and cons to both types, and the best one for you will depend on the type of work you do and the type of risk you need to cover. And you may not have a choice in the matter, as some types of cover are usually written as claims made (e.g., professional indemnity) while others are typically written as claims occurring (e.g., employers' liability or public liability insurance).

Claims made policies are common in professional liability insurances such as professional indemnity and directors and officers insurance. One advantage of claims made policies is that they are typically cheaper than claims occurring policies, since coverage stops once the policy ends. Another advantage is that you can be covered for incidents before the start of your policy so long as the policy has a retroactive date. This concept is useful (and often implemented) if you switch insurance companies—so long as there's no gap in your cover between the policies.

Claims occurring policies are common in insurances related to physical injury or damage to other parties, such as employers' liability insurance or public liability insurance. An advantage of a claims occurring policy is that you're covered even after your policy expires so long as the incident occurred while you had an active policy. If your line of work means you could face claims in the future for work you do today, a claims occurring policy might be best for your business insurance needs.

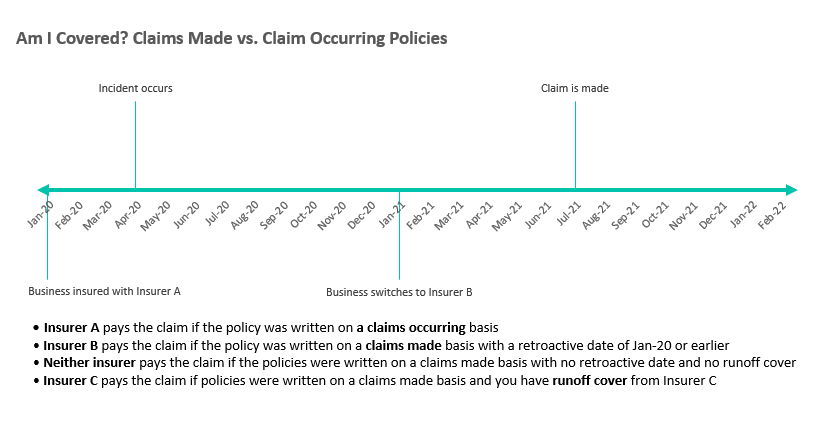

Here's a chart illustrating which of two (or three) potential insurers would cover a claim, depending on whether the policy was written as claims made or claims occurring:

Limits of insurance for claims made and claims occurring policies

Insurance policies typically have two different limits:

- Per-incident/Per-claim limit: The maximum amount that a policy will pay out for each claim.

- Aggregate limit: The maximum amount that a policy will pay out over the period of insurance.

In addition, there may be "inner limits" which essentially lower the per-incident or aggregate limit for certain types of claims. For example, a D&O policy could have lower inner limits for claims related to environmental pollution.

Claims Occurring policies typically have an aggregate limit that renews each year when you renew the policy, and claims are subtracted from the aggregate limit in the year the incident occurred. So if you have a claim this year for an incident that occurred in 2024, it's the aggregate limit from 2024 that is used up.

Example:

- Your public liability policy is "claims occurring" with a limit of £2 million. Your business is sued and must pay a settlement of £500,000. This leaves £1,500,000 of coverage for the rest of the period of insurance. When you renew next year the limit resets back to £2 million.

Claims Made policies typically have an aggregate limit that applies to all claims made in that policy year. If claims are made for incidents that occurred in prior years, any payouts would be subtracted from the aggregate limit in the year the claim is made (not the year the incident occurred).

Example:

- Your professional indemnity policy is "claims made" with a limit of £2 million and a retroactive date of 5 years prior. Your business is sued for professional negligence for work done two years ago and must pay a settlement this year of £500,000 and legal fees of £100,000, which are taken out of the current period's aggregate limit. This leaves £1,400,000 of coverage for claims made during the rest of the current period of insurance.

Final Word

Insurance policies can be written on either a claims made or claims occurring basis, and you usually don't have a choice because it depends on the type of business insurance you're buying. That said, it's still critical to understand what type of cover you have, if there are any limitations to your cover, and any risks you're exposed to. Be sure you fully understand the repercussions of your cover, and contact your insurer if you have any questions.