Block of Flats Insurance: FAQs, Costs, Quotes

Compare block of flats insurance quotes.

Powered by QuoteZone.

Compare Quotes

- Rated 4.8 out of 5 stars on Reviews.co.uk

- Over 300,000 QuoteZone quotes completed per month

- Fill out one form online to get started

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

As seen on

Block of Flats Insurance UK

Whether you're insuring a small or large block of flats, or even more than one block of flats, you'll certainly compare quotes for buildings insurance to be sure you're getting the best cover for your needs—and at a cheap enough cost. But what cover do you really need? And what's the best way to compare quotes? Let's go over the basics.

What Insurance Do You Really Need for a Block of Flats?

There are a few main types of insurance coverage that a block of flats usually needs—for starters, buildings cover and third party liability. But you might want other coverages like contents cover and legal expenses, which can be a key component of landlord insurance to help with non-paying tenants, for instance. Let's run through the list to explain what each type covers to help you decide what coverage your block of flat needs.

| Popular Types of Block of Flats Insurance & What They Cover | ||

|---|---|---|

| Buildings Insurance | Covers damage or loss to the structure of your building (e.g., walls, roof, communal pipes, electrics and fixed flooring, some outbuildings or garages, etc.) due to events such as fire, flood or theft. Accidental damage can be included, too. | |

| Third Party Liability | If a tenant or visitor is injured in the block of flats (e.g., a loose railing results in an elderly person falling on the stairs), or their property is damaged, then third party liability insurance covers legal costs and compensation payments you're required to pay. | |

| Contents Insurance | Protects fixtures and fittings against damage, loss or theft. You can add accidental damage, too. Typically it's the carpets, window coverings, and other fixtures and fittings that are covered (e.g., fitted kitchens, bathrooms, appliances, etc.) If you rent out furnished or partially furnished flats, you can get cover for the furniture as well. | |

| Legal Expenses | Covers access to a legal team and legal defence costs in certain situations like employment disputes, HMRC tax enquiries, failed health & safety inspections, debt recovery, property protection and more—most relevant for landlords perhaps is that a policy should also cover evictions (e.g., in the case of non payment). | |

| Home Emergency | Can cover emergencies like burst pipes, floods, pest control, heating & hot water, electrics, home security, drains, and more (depending on the level of cover you buy). | |

| Rent Guarantee | For landlords, this covers lost rental income if a tenant defaults (usually for up to six to 12 months), also called tenant default insurance. | |

| Loss of Rental Income | Also for landlords, this covers lost rental income if your tenants are forced to move out because your property becomes uninhabitable due to a peril such as fire or flood. | |

Here are some examples of how these insurances can protect a block of flats, as well as the tenants and the property owner/s. This can give you an idea of how the different coverages work in the real world:

Block of Flats Insurance Examples

- Block of Flats Buildings Insurance Example: A flood causes damage to communal walls, doors, and floors in the ground floor of your block of flats. Buildings cover should cover the cost of repairs.

- Landlord Contents Insurance Example: A fire in your residential rented block of flats results in damage to blinds, lighting, kitchens (including appliances) and carpets in a number of flats. Contents insurance should pay to replace these damaged items (as well as furniture if you rent out the flats on a furnished or partially furnished basis).

- Public Liability Insurance Example: A tenant of (or visitor to) your block of flats slips on a recently mopped tile floor in the building's entryway. They seriously injure themselves and blame you for negligence due to insufficient 'wet floor' signage.

- Loss of Rental Income: A fire in your block of flats mean the tenants have to move out whilst repairs are undertaken. Loss of rental income insurance can cover what it says on the tin—the lost rental income while your property is uninhabitable.

- Legal Expenses: A tenant stops paying their rent, and the building owner needs professional legal advise to understand your options and next steps.

- Home Emergency Example: A leak in a top floor flat needs to be attended to quickly, before the water runs down and damages the flat below. Home emergency cover can send out a repairman to fix the problem.

- Employers’ Liability: If you have any employees working in your block of flats, say a part-time maintenance person, you'll need employers' liability insurance—it's required by law.

FAQs

Block of flats insurance at it's basic offers protection for the building and against third party liability. It's the freeholder's responsibility to buy insurance for their block of flats, whether the landlord leases or rents out the flats. It could apply to properties used by large commercial tenants, blocks of purpose-built rented residential flats, or even houses converted into flats.

While terms will vary from policy to policy, it's common for block of flats building insurance to cover the building for serious events like fire, flood and theft that result in damage to the structure of the property, such as the exterior walls, roof, floors & walls in communal areas, etc. Outbuildings and garages may also be covered (but check the policy wording). You can also get accidental damage coverage but this will increase the premium.

In a building composed of leasehold flats, it's usually the case that the freeholder arranges and buys the building insurance; then the leaseholders essentially cover the insurance premiums as part of their annual service charge. In cases where leaseholders also own part of the freehold they may need to arrange their own building insurance, which they can potentially buy individually or together via block of flats insurance (this can be cheaper than buying individual cover). It's best to check the terms of your lease to find out who is responsible in your building. See MoneyHelper for more information.

Yes, blocks of flats should certainly consider emergency repair cover. In fact, it's a landlord's legal responsibility to provide heat and hot water and to arrange for repairs if these should fail—so any block of flats are certainly wise to have this cover. It might not be needed if, for instance, you already have a maintenance staff on standby to take care of issues that arise, however.

In most cases you can buy block of flats insurance without having your property inspected; the exception to this is if your property has a history of subsidence that you want to cover.

Yes, blocks of flats should certainly have insurance to protect against events like fire, flood and theft, liability claims, and more. While it might not be required by law, holding certain insurances are likely to be a requirement of any mortgage on the property or of the leasehold agreement/any tenant agreements. At the very least, a block of flats will usually have building and third party liability insurance.

How Much Does it Cost to Insure a Block of Flats?

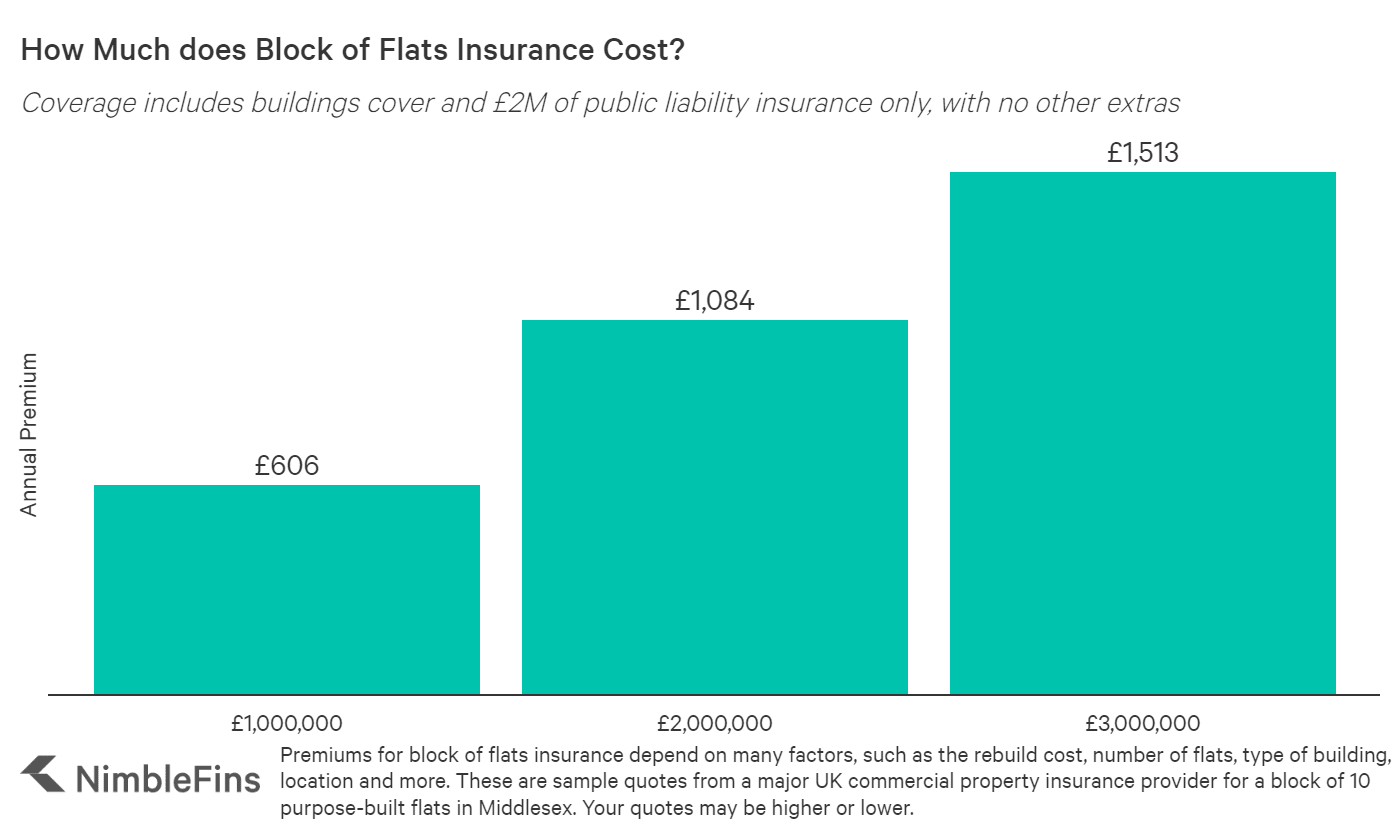

The cost to insurance a block of flats ranges from a few hundred pounds a year to many thousands—the cost of block of flats insurance depends on factors like the number of flats, the rebuild cost of the building, the types of extra coverage you need, etc. To give you a rough idea of the costs involved, we ran a few sample scenarios through a top UK property insurer's pricing engine. Here's what we found.

Block of Flats Insurance Costs by Rebuild

The cost to rebuild your block of flats, for instance if it were to burn down in a fire, determines how much you'll pay for buildings insurance. Insurance premiums and property rebuild costs have seen significant increases in recent years. For example, a block of 10 purpose-built flats with a rebuild cost of £1,000,000 would cost around £1,065 to insure (buildings and £2M public liability only) with a popular UK property insurer; and premiums rise roughly in line with rebuild costs. So a block with 2x the rebuild cost is roughly 1.8x as much to insure.

| Sample Costs for Block of Flats Buildings Insurance | Premium |

|---|---|

| £1,000,00 rebuild cost | £1,065 |

| £2,000,00 rebuild cost | £1,900+ |

| £3,000,00 rebuild cost | £2,650+ |

Your costs could be significantly higher or lower, depending on the details of your building and claims history. Premiums for purpose-built blocks have risen by approximately 75% since 2020. Because larger blocks (over £2 million rebuild value) are subject to more complex risk assessments, we strongly recommend requesting a bespoke quote to ensure your specific building features and location are accurately priced.

Add On Insurance Costs for a Block of Flats

As mentioned, the figures above only reflect buildings and third party liability. What if you want to add extras like legal expenses or damage/theft by tenants? We ran the figures to get a ballpark idea.

Optional extras for blocks of flats are now often priced per policy or per unit. Typical add-on costs include:

| Sample Add On Insurance Costs for a Block of Flats | |

|---|---|

| Legal Expenses | £46 per unit/policy |

| Landlord Emergency Cover | £171 per unit/policy |

| Rent Guarantee/Tenant Default | £133 (based on £50k cover) |

| Accidental Damage | £143 |

Where can I get quotes for block of flats insurance?

Compare block of flats insurance quotes here—after filling out a short form you'll hear back from up to five insurance providers. You'll have the chance to talk on the phone if you have questions that you want to discuss, which many people find handy since each block of flats is a bit different. Then choose the cover that offers the best price and features for your needs.

Block of Flats Insurance Providers and Brokers

If you get a compare block of flats insurance quotes here (powered by 4.8 star rated QuoteZone), you will be connected with up to five suitable companies to get a quote. Here is the list of commercial property insurance providers in the QuoteZone panel:

- 1st Choice

- Allied Wessex Dental Insurance

- Arthur J Gallagher & Co.

- Be Wiser

- BP Insurance Brokers

- Brady Insurance

- Compare Insurance

- Coversure Harborne

- Crosby Insurance Brokers

- Edison Ives Insurance

- Export and General

- Gallagher Insurance

- Greenwood Moreland

- GSI Insurance

- Insurance Protector

- Konsileo

- Nova Insurance

- Plan Insurance

- QCIS

- SJL Insurance

- The Retail Mutual

- TL Dallas (NI)

- UKinsuranceNET

Methodology

To determine the costs of insurance for our sample block of flats, we gathered sample quotes from a major UK commercial property insurer. The property contains 10 flats and is a purpose-built structure, located in Middlesex. Quotes for your building may be much higher, or lower.