The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

What Insurance does a Photographer Really Need?

Insurance for photographers can help protect against a number of risks specific to the profession, from public liability or professional indemnity claims to theft of expensive photography equipment. And there are other business insurance coverages you might need as well. Here's what you need to know about photographer insurance to protect you and your business.

- What are common types of insurance a photographer needs?

- Does a photographer need insurance?

- How much is insurance for a photographer?

Types of Insurance for a Photographer

While insurance needs vary from business to business, there are a few types of insurance that photographers frequently need. We discuss them below and also provide some simple examples to help show how the different types of cover can offer protection.

1. Public Liability Insurance

Public Liability insurance for a photographer protects you financially if a member of the public (e.g., a client) is injured or their property damaged due to your work. Public liability insurance can pay for legal defence expenses and compensation claims if you're sued for injury or damage. It's common in the UK marketplace to see limits of £1 million, £2 million, £5 million or £10 million on offer.

- Bodily Injury Example: A client trips on a lighting cord and seriously breaks their arm. They are unable to work for 3 months and sue you for lost wages as a result.

- Property Damage Example: When carrying your equipment into a client's home, you accidentally knock an expensive vase off of a table in their front hall. The client sues you for the value of the vase.

2. Employers' Liability Insurance

Employers' Liability insurance is a requirement if you hire any employees, even part-time workers. If an employee becomes ill or is injured due to their work for you and sues you as a result, employers' liability insurance covers legal defence costs and claims settlements.

- Employers' Liability Example: An employee slips and falls on a wet floor in your studio, seriously injuring their back. They blame you and sue for damages.

3. Professional Indemnity Insurance

Professional Indemnity insurance can protect you from a compensation claim from a client who is unhappy with their photos and they blame your professional advice or claim negligence on your part. Perhaps there was a misunderstanding, there was a problem with your equipment or they are just not satisfied with your work. Professional indemnity insurance can cover legal defence costs and compensation settlements if the client claims a financial loss as a result.

- Professional Indemnity Example: You give advice on using certain lighting and positions to achieve what you believe is a bride's wishes, but the client is unhappy with their wedding photos, claiming you didn't deliver what was promised. They sue you for the cost of retaking the photos, which involves paying for makeup, hair and tuxedo rentals for the bride, groom and rest of the wedding party.

4. Tools/Equipment Insurance

Tools/Equipment Cover is critical for many photographers to protect their expensive cameras and other equipment in the event of damage or theft. As photography equipment is quite expensive, this cover can be very valuable in event a disaster like theft. Photography equipment is mission critical and you can't work without it.

- Tools/Equipment Cover Example: When you stop for a rest en-route to an event, your car is broken into and all of your equipment is stolen. Tool/equipment cover that includes in transit/away from home protection can reimburse you for these stolen items.

5. Personal Accident Insurance

Personal Accident insurance can provide a financial benefit to you (or an employee) if you're injured and unable to work as a result. This cover can help you cover your day-to-day household bills while you're out of work. This type of cover is a "benefit" (so not tax deductible) and would be paid either as a weekly payout in case of a temporary injury (e.g., broken arm) or a lump sum payout for a permanent disability (e.g., loss of an eye).

- Personal Accident Example: You slip and fall at work, seriously breaking your leg. You're unable to work for 6 weeks while your leg heals so you claim for the weekly benefit to keep you afloat until you can resume working again.

In addition, a photographer might need other types of cover as mentioned below.

Do Photographers Need Insurance?

Yes, most photographers generally do need business insurance. While needs might change whether you specialise in fashion photography, landscape photography, wildlife photography, sports photography, event photography, wedding photography, pet photography, real estate photography, or other types, many professional photographers look into public liability insurance, professional indemnity, equipment cover and employer's liability to protect any employees at the very least.

Public liability insurance is critical for any business that deals in person with members of the public (e.g., clients), so most photographers need this. Professional indemnity cover can also be important to protect a photographer from customers who are unhappy with your work, for example if there is a misunderstanding or you have an equipment failure.

Since photography equipment is so expensive, equipment/tools cover is also of high importance to most photographers—the cost of your cameras, lenses, batteries, memory cards, a computer, editing software, lighting equipment and other accessories can really add up, costing thousands of pounds at a bare minimum. Business equipment/tool cover can protect these items against accidental damage or theft.

Employers' liability insurance is required by law as soon as you hire someone to work for you, even a part-time assistant. Whether or not you need other types of business insurance as a photographer will depend on the specific risks you face. Other coverages you might want include personal accident, product liability, commercial property, business interruption insurance, etc.

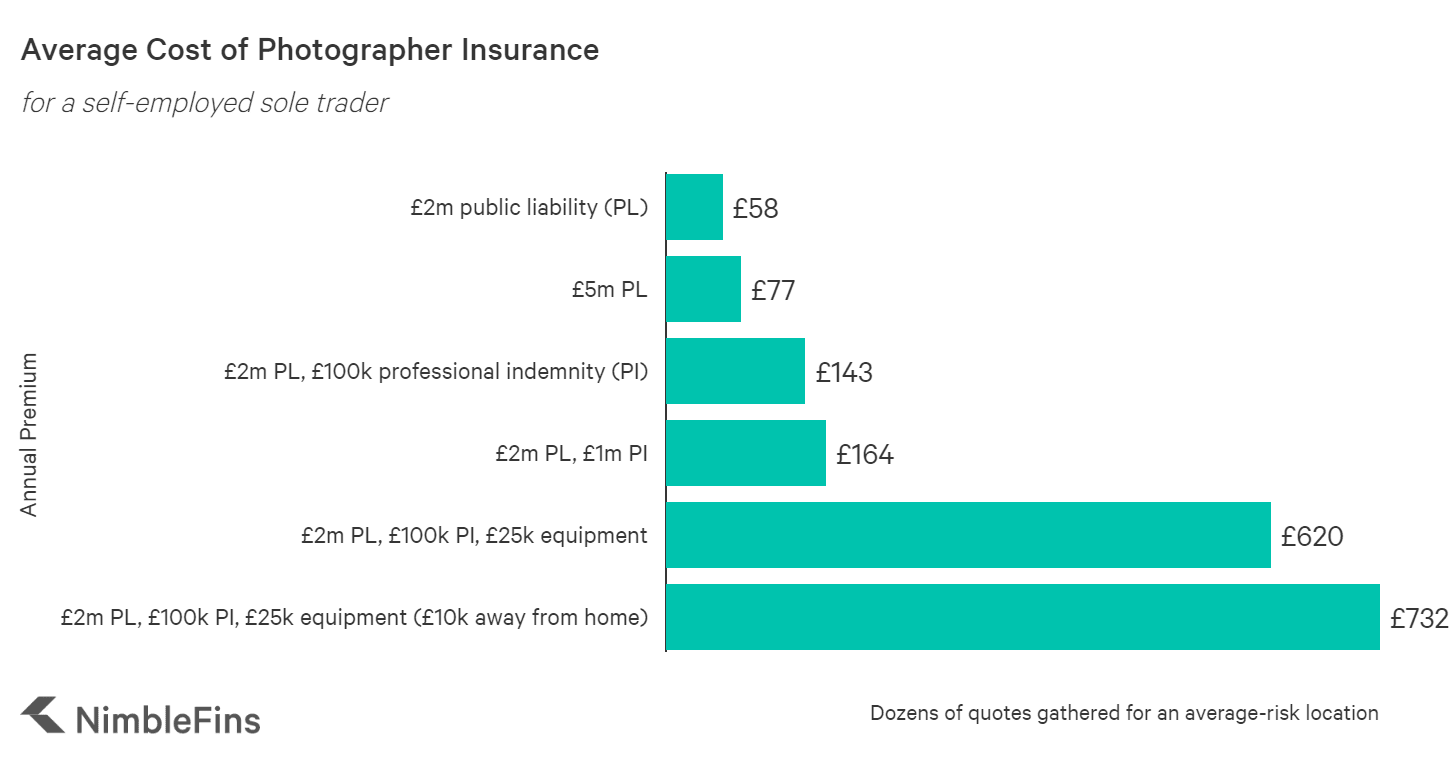

How Much is Public Liability Insurance for a Photographer?

The average cost of public liability insurance for a photographer starts from around £58 a year for two million of cover. But a photographer's business insurance costs can quickly rise to 10X that amount or more depending on the additional coverages you need.

Increasing the public liability limit won't add much to your premium—for instance, increasing from £2m to £5m of public liability cover only increases the premium by around £20. Adding professional indemnity to public liability will roughly triple the cost of your business insurance.

| Average Cost of Photographer Insurance | |

|---|---|

| £2m public liability (PL) | £58 |

| £5m PL | £77 |

| £2m PL, £100k professional indemnity (PI) | £143 |

| £2m PL, £1m PI | £164 |

| £2m PL, £100k PI, £25k equipment | £620 |

| £2m PL, £100k PI, £25k equipment (£10k away from home) | £732 |

Equipment insurance, however, can cost significantly more. For example, £25k of equipment cover could add in the ballpark of £450 a year; expand this cover to include cover away form home (which many photographers might need) and your premium goes up another £100 or so (assuming you travel with only £10k of your £25k worth of equipment in this example).

Your business insurance rates will also depend on where you live and even the size of your contracts (if you opt for professional indemnity cover). And if you need to buy employers' liability insurance for any employees, expect to pay in the ballpark of £200 for the cost of employers' liability to cover one person.

These prices reflect the average of dozens of sample quotes we gathered for a test case to get a rough idea of prices (for each situation we took the average of the 3 cheapest quotes we found online); your premiums might vary significantly depending on your situation and the details of your application. For instance, if you carry out underwater or aerial photography, your risks are higher and your insurance rates will increase as a result.

FAQs

Public liability insurance is essential for photographers, and any other profession where you're dealing directly with members of the public (e.g., in the case of a photographer, your client and their guests at a wedding). Public liability insurance protects you against people claiming you have injured them or damaged their property through your work.

The cost of photographer liability insurance starts from as little as £58 a year (around £5 a month) for a self-employed sole trader, but costs can quickly rise as you add on additional coverages.

Yes, insurance can protect a wedding photographer financially against situations like injury to a member of the public or damage to their property (see public liability insurance); dissatisfied clients (professional indemnity cover); theft or damage to their cameras and other equipment; injury to an employee (see employers' liability insurance); etc. This applies to most photographers, not just wedding photographers.

Yes, the right insurance is crucial to protect a photographer's business—this includes if you are a freelancer. As a self-employed sole trader you may face risks such as injury to the public, property damage, dissatisfied clients, equipment theft, etc. Without insurance, you could be liable for defence costs and settlements due to client injury, or paying to replace stolen equipment yourself, for example.

Photographer Employment and Earnings Statistics

Most photographers earn in the region of £22,000 to £26,000 on average in the UK, but annual salaries can range from under £15,000 to £46,000 or more depending on your experience level and the type of work you do. Here are some statistics on how much photographers earn from various sources.

| How much does a photographer earn? | Average |

|---|---|

| Per hour (source: Payscale) | £11 to £52 |

| Freelance photographer (source: Indeed) | £77 per day |

| Freelance photographer (source: Indeed) | £22,000 per year (range: £7,500 to £46,000) |

| Photographer in London (source: Glassdoor) | £26,000 per year |

| Photographer in the UK (source: Payscale) | £22,000 per year (range: £15,000 to £32,000) |

| Photographers, audio-visual and broadcasting equipment operators (source: Office for National Statistics) | £26,887 |