What Can Affect The Cost of Private Health Insurance?

Compare many health insurance companies to save money

- Get on-hand support from health insurance broker of the year, Assured Futures, through Confused.com

- Compare quotes from Bupa, AXA, Aviva, Vitality and more

- Get a quote in minutes

You may be wondering why you are paying what you are for your private health insurance. Indeed, you mind find yourself asking why you are paying more or less than your family, friends and co-workers. Well, there might a few reasons why.

When you apply for any type of insurance, be that car, life, travel or in this case, private health insurance, your insurer will price their policies based on the perceived level of risk you present as a customer. Customers deemed to be less risky will face lower premiums and those who are considered to be higher risk, and therefore more likely to make a claim, will face higher costs.

It's a fickle game, so we've broken down the main factors that can affect the cost of your private health insurance. Whilst some of these are sadly unavoidable there are others that you as a consumer can control and may even help you save a little bit of money along the way.

Table of contents

- What factors can affect the cost of Private Health Insurance?

- How can I save money on Private Health Insurance?

What factors affect the cost of Private Health Insurance?

Age

It may come as no surprise but the older we get, the more likely we are to get sick or injured. One of the main things insurers will take into account when assessing your application for private health insurance is your age. This is because they see older people as inherently more 'risky' and more likely to make a claim.

The table below gives you an idea of just how large a role age plays in determining the cost of your private health insurance, based on 2026 market data. We compiled quotes for a non-smoking individual looking to take out a standard plan with mid-tier cover, and an excess limit of £250. The numbers below are based on market averages, but note any figures you are quoted may be higher or lower depending on your circumstances.

| Average Private Health Insurance Cost Calculations By Age | Monthly premium |

|---|---|

| 30 years old | £50 |

| 40 years old | £70 |

| 50 years old | £90 |

| 60 years old | £130 |

| 70 years old | £170 |

As you can see, there is a huge difference and the younger you are, the cheaper your premiums are likely to be. A 30 year old might expect to pay an average of around £50 per month for their private health insurance, whilst a 70 year old can expect to pay more than three times this amount — an average of £170! This is because younger people are assumed to be healthier and far less likely to be diagnosed with critical illness or suffer injury, both of which are associated with high medical costs.

Now, how an insurer uses this information can vary — some insurers will use age bands (e.g. 50-60), so as you get older and move up an age band your premium will increase accordingly. Others will raise your premiums ever so slightly each year to reflect your increasing age, so these increases are often more gradual. Be aware that some health insurance providers have a maximum age that you can take out a policy!

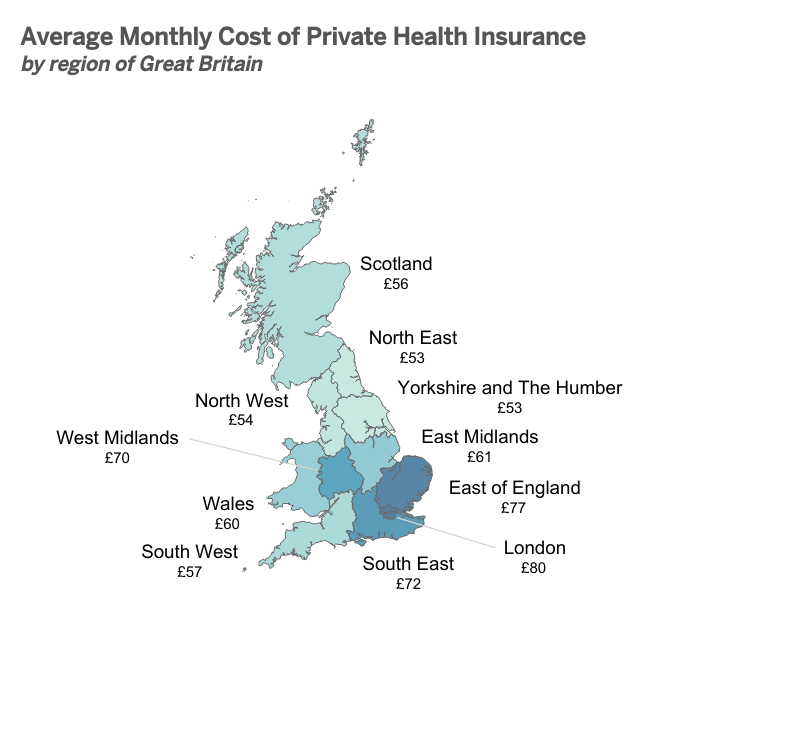

Location

Yes, sadly your location can be a factor that insurers use to determine your premiums. Certain areas in the UK are thought to carry more health risks than others, London for example due to the fact it is heavily populated and with that comes higher levels of pollution.

Others areas are simply more expensive overall, meaning medical costs are also more pricey (Sorry again, Londoners!).

According to 2026 market research, location continues to play a significant role in premium calculations, with London and the South East typically seeing higher premiums due to increased treatment costs in these areas.

Take a look at the map and table below to see what a difference your postcode can make!

| Average Private Health Insurance Cost Calculations By Region | Monthly premium |

|---|---|

|

London | £80 |

|

East | £77 |

|

South East | £72 |

|

West Midlands | £70 |

|

East Midlands | £61 |

|

Wales | £60 |

|

South West | £57 |

|

Scotland | £56 |

|

North West | £54 |

|

North East | £53 |

|

Yorkshire & The Humber | £53 |

As shown above, the average cost of private health insurance varies widely across the UK. The region with the cheapest premiums is Yorkshire and The Humber. It may come as no surprise to see private health insurance is the most expensive in London.

Remember though, these figures are based on quotes we received at the time of writing, for a mid-tier plan and for an individual of a certain age. You may find you are quoted a price that is more or less than those listed above, so do take these with a pinch of salt. They are designed to be used for guidance only and to illustrate the relative cost of private health insurance in different areas.

Your medical history

If you have any pre-existing medical conditions, albeit something you currently or previously suffered from, this will likely affect your premiums. Your insurer will take this evidence of poor past health and assume you are more likely to get ill or injured in the future. Hence, higher premiums.

When you take out private health insurance, the amount of information about your medical history you disclose upfront depends on the type of medical underwriting you choose. There are two main types:

- Moratorium underwriting: with this type of medical underwriting you won't need to disclose information about your medical history to your insurer when you apply for private health insurance. However, you will need to provide this should you wish to make a claim, and your insurer may also need information form your GP, too. This is usually the default underwriting option, and is usually cheaper

- Full medical underwriting: if you choose full medical underwriting you will need to complete a full health questionnaire and let your insurer know of any pre-existing medical conditions you have. Your insurer may also request information from your GP, too. This option is typically more expensive, however, your insurer will outline from the start what is and is not covered so each party is clear on the terms of the policy

You can find out more about medical underwriting here.

Your lifestyle

Some behaviours are deemed to be ‘unhealthy’ and increase your risk of certain conditions. For example, smoking cigarettes is the leading cause of lung cancer in the UK, accounting for more than 70% of cases.

Smoking and drinking excessive amounts of alcohol are things your insurer will look at when assessing your application, and if you engage in these habits then it’s likely your premiums will be higher. It is for this reason that many insurers offer their customers incentives and rewards for engaging in healthy behaviours, such as keeping fit and active — Aviva and Vitality for example offer discounts on gym memberships and other health services when you take out a private health insurance policy with them.

Your level of cover

Naturally the level of cover and number of benefits you opt for will determine how expensive your premiums are. Choosing a more ‘budget’ option, which provides less protection, will be cheaper than opting for a more comprehensive level, which may provide full treatment and diagnosis cover.

Based on 2026 market research, more comprehensive plans with outpatient cover typically cost around 45-50% more than basic inpatient-only plans. Mid-tier plans, which include inpatient care plus limited outpatient cover, sit between these two options.

The lowest level of cover is, on average, almost half the price that you might pay for the most comprehensive level of protection. Our research found more basic plans to cost around the £50 mark, whereas opting for the full package can cost you around £100 per month. As you'd expect, mid-tier cover sits quite nicely in between the two, averaging around £75 per month. (roughly)

An easy way of saving money on your private health insurance is to sit down and think about how much cover you realistically need. If you are someone who rarely gets sick and adopts a healthy lifestyle then you may not need to pay extra for more comprehensive cover. Instead, a simpler plan might suit your needs.

Your claims history

The number of claims you have made in the past can affect the cost of almost any type of insurance when it comes to renewal, and private health insurance is no different.

Whilst the extent to which your claims history affects this can vary from insurer to insurer, generally it’s a good rule of thumb to try and avoid making multiple, small claims where possible. It’s good practice to sit down and think about whether you can feasibly self-fund instead of claiming from your insurer, as the more times you claim during your policy term the higher your premiums are likely to be.

Many insurers offer a No Claims Discount which rewards customers who make few or no claims with lower premiums, so it’s definitely something to think about.

Inflation

Inflation is a term we hear all the time though many of us aren’t quite sure what it means. According to the Bank of England, inflation is simply a term used to describe the increase in prices over time. The rate of inflation relates to how quickly these prices are going up.

So how does inflation affect the cost of your private health insurance?

Well, it makes sense if you think about it. Inflation affects the cost of goods and services over time.

Example: If last year you could purchase a basket of goods for £100, but the same basket of goods this year costs you £102, then the rate of inflation would be 2%.

So, it makes sense that cost of private health insurance will rise too, in line with inflation.

Medical inflation

You may be thinking, 'NimbleFins, haven’t you just described medical inflation?'

And the answer to that is, not quite. Medical inflation is a slightly different.

It is the term used to describe advances and trends in medicine, for example, breakthrough drugs and therapies. Medical breakthroughs are fantastic of course, as they lead to better quality care and more effective treatment. However, they can be really expensive! According to 2026 industry data, medical inflation typically runs at 8-10% annually, higher than general inflation, due to the costs of new treatments, drugs, and medical technology. There is no real way around this, so medical inflation is something your insurer must take into account when deciding the cost of your private health insurance.

How can I save money on Private Health Insurance?

It's not all doom and gloom, and there are simple and effective ways you can potentially save money on your private health insurance. We've put together a handy guide detailing everything you need to know, so be sure to check this out here.

Now, whilst we all like to save a few pennies, we strongly recommend prioritizing cover over cost. Your health is the most important thing, and ensuring your cover is tailored to your specific needs can help you rest easy knowing you are well protected should the unexpected happen.