5 ways millennials can prepare for Brexit uncertainty

Brexit. Whether you voted for it or not, one thing is for sure—it's coming! With all the uncertainties looming over the finite details as politicians are still unable to secure a deal, it's a good idea for millennials to prepare for the road ahead.

Here are some statistics to bring the situation into light, as well as some points you might want to consider to ensure Brexit doesn't have a negative impact on your financial situation.

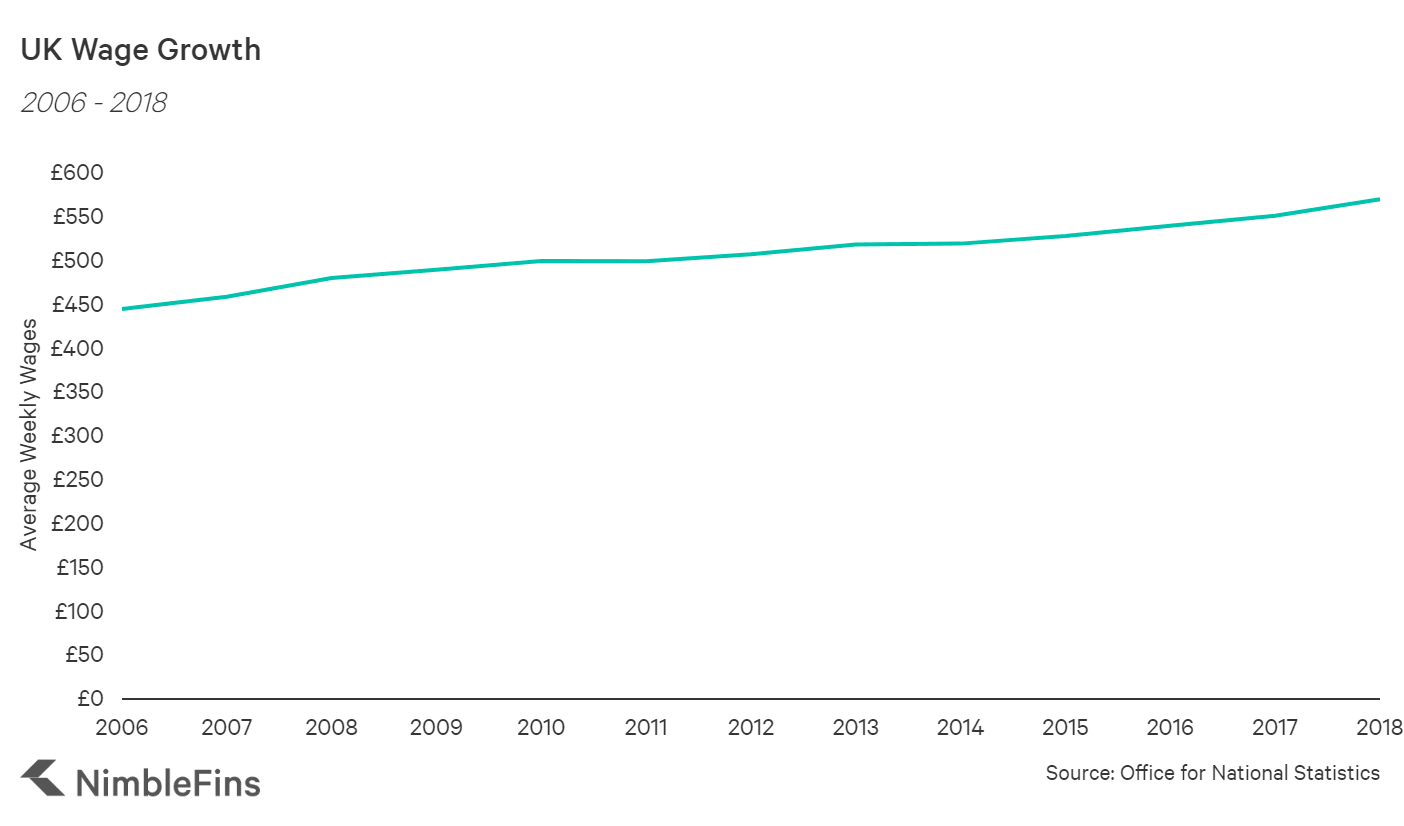

How Have Wages Grown Since Brexit?

Wages have been on a steady incline since the 2008 financial crash. Though, with Brexit looming there's every chance things could change. Plus, we can never be truly sure that another recession isn't around the corner so it's a good idea to get your finances in order just in case. According to the Office for National Statistics, the rate of growth has seen the average weekly wage rise at the following levels:

| UK Weekly Wage Growth | |

|---|---|

| 2006 | £443.6 |

| 2007 | £457.6 |

| 2008 | £479.1 |

| 2009 | £488.5 |

| 2010 | £498.5 |

| 2011 | £498.3 |

| 2012 | £506.1 |

| 2013 | £517.4 |

| 2014 | £518.3 |

| 2015 | £527.1 |

| 2016 | £538.6 |

| 2017 | £550.0 |

| 2018 | £569.0 |

So just what steps can millennials take?

Get smart with your finances

With an uncertain time ahead, now is as good a time as any to get real about your spending habits. One of the best ways is to comb through the last 3 months of your bank statement. Look at those expensive gym memberships you don't use, or unnecessary takeaways—just where are you spending your money, and how can you make better financial decisions?

Apps such as Moneybox also help you save by rounding up each purchase you make to the nearest pound, moving this into a separate account. You can then use this money to pay off household debts, or towards important investments such as a house deposit. You'll be surprised how quickly your savings build up, especially if you get on track with your finances too.

Avoid rash investments

Investing in the stock market might seem like an attractive proposition, but it's important to make sure you invest both at the right time, and in the right stock. At a time when Britain is about to leave the EU, this could make for uncertain times in the markets.

If you do go ahead and invest, it's also important you know how the process works. Go Forex is a free app in which you can pretend to invest real money against live markets. It also has plenty of help and guidance to help you understand how investing works, and how to limit your losses especially when just starting out.

Remember, you should never invest more than you can afford to lose. Investing in the stock market is also not a "get rich quick" scheme. It can take years before investments turn a decent profit, and there is also no guarantee you won't lose it all in the event of a crash, which can't be ruled out with Brexit around the corner.

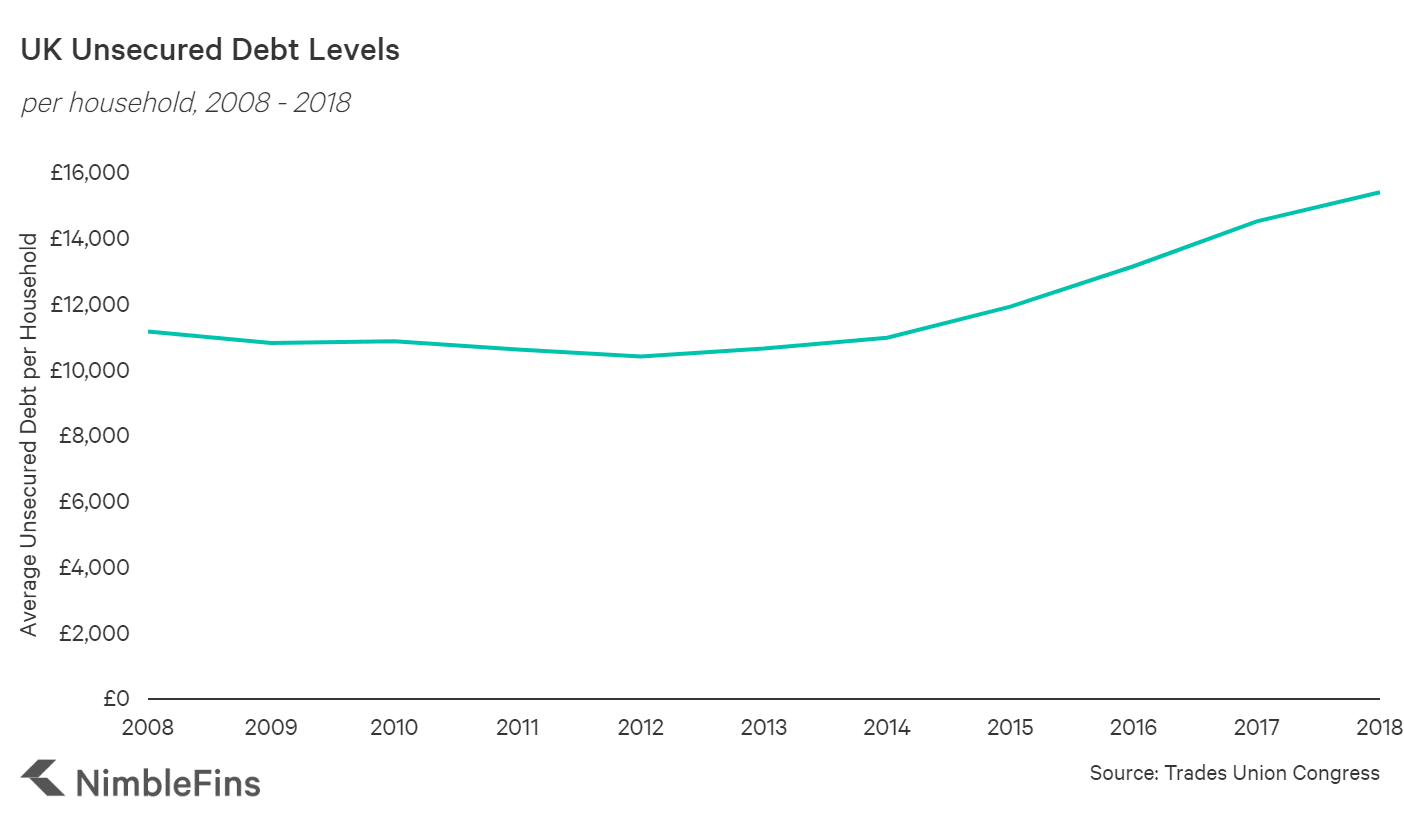

Manage personal debts

Personal debt can be crippling, especially if you're not on top of your spending and are struggling with repayments. Here is where average level of personal debt in the UK has stood since 2008:

| UK Household Debt | |

|---|---|

| 2008 | £11,146 |

| 2009 | £10,800 |

| 2010 | £10,855 |

| 2011 | £10,600 |

| 2012 | £10,390 |

| 2013 | £10,633 |

| 2014 | £10,960 |

| 2015 | £11,906 |

| 2016 | £13,133 |

| 2017 | £14,499 |

| 2018 | £15,385 |

Source: Trades Union Congress (TUC) analysis

The level of personal debt each household in the UK has on average is rising at a sharp rate, with the current figure standing at £15,385. If this sounds familiar to you, then reducing your personal debt during Brexit uncertainty should be a priority.

You may wish to seek advice about consolidating your debt, as well as the best way to manage your repayments. Either way, without ridding yourself of debt it will continue to eat up your spending not to mention potential savings.

Start a side hustle

In 2018, 384,000 people were made redundant in the UK, according to Statistica. While Brexit doesn't necessarily mean more redundancies are on the cards, it's always a good idea to have another income brewing in the background, aka a Side Hustle.

More and more people are increasingly working as freelancers or setting up their own business as well as working full time. Not only does this increase income, but also helps with security should more job cuts be announced in your industry.

Conclusion

Brexit is a stark reminder that our finances are not to be taken lightly, with millennials being no exception to this. By getting smarter with your spending habits, saving where possible and increasing your income stream, you are more likely to fare better in the event that Brexit does have a negative economic impact. Either way, by getting financially savvy now it will definitely benefit you in the long run.