Find Good, Cheap Van Insurance | Quotes

Benefits of comparing van insurance with NimbleFins

- You can save up to £685*

- 4.8 out of 5 stars on Reviews.co.uk**

- Cheap quotes from 60+ providers

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

As seen on

Van Insurance

If you’re driving on public roads, holding a valid van insurance policy is a legal requirement. Plus a good policy can help to protect you, your van and other drivers and vehicles if an accident occurs. In this article, we’ll cover everything you need to know about the different types of policy available, go over the average cost of some of these policies and answer any questions you might have.

If you’re wondering what your policy might look like, fill out a quote form with our partner QuoteZone, whose search engine includes dozens of van insurance providers including RAC, Admiral, Budget, Churchill, Gladiator, Swinton, Hastings Direct and more.

- Where can I get van insurance quotes?

- What insurances can a van driver/owner buy?

- FAQs

- Does a van really need insurance?

- How much does van insurance cost?

- More information on van insurance

Where can I buy van insurance?

Save £££ on van insurance with NimbleFins.

- You can save up to £685*

- 4.8 out of 5 stars on Reviews.co.uk**

- Cheap quotes from up to 60 providers

As is the case when buying anything, it's good to compare as many options as possible to find the best deal you can get. If you'd like us to take the hassle off of your hands, then fill out a quote form with our partner QuoteZone—they work with over 60 brands, leading the market for van insurance.

There are three main ways to consider when looking to get cheap van insurance:

Buying Direct

Many of the UK's top insurers will happily insure your van. And while you will find some of them on comparison websites, many of them save their best offers for customers who come to them direct (thus cutting out the middle man). Comparing each provider individually can take a little bit of time, but you'll know you're comparing the best deals each insurer has to offer (as opposed to the standard prices you might find on comparison websites).

Here's a list of some of the UK's biggest companies offering van insurance:

- Admiral Van insurance

- Direct Line Van insurance

- Aviva Van insurance

- Lloyds Van insurance

- AXA Van insurance

- Churchill Van insurance

- Gladiator Van insurance

- Hastings Van insurance

- Swinton Van insurance

- Tesco Van insurance

- LV Van insurance

- Zenith Van insurance

- Brightside Van insurance

- Acorn Van insurance

- Asda Van insurance

- Adrian Flux Van insurance

Insurance Price Comparison Sites

By far the most time-effective way to get quotes for your van insurance, price comparison websites offer you quotes based from a short form you fill out for them. They then gather the prices of that quote from their approved suppliers and present them to you, usually over email or online.

Price comparison websites are great for comparing the prices of multiple providers in a short period of time, and can help you get the best deal possible if you don't want to go through each supplier individually. Be aware that you're unlikely to find any of the special offers that going direct or through a broker might get you, but these companies typically make up for that with separate offers/benefits, such as free movie tickets, discounts at restaurants or other small rewards.

Here's some of your best options for price comparison on van insurance:

- The Van Insurer

- QuoteZone

- Go Compare

- Compare the Market

- Confused

- MoneySupermarket

Using a Broker

An insurance broker is somebody who searches through many companies and quotes to find the cheapest deal to fit your needs. You simply give them the details of your van and your requirements (level of cover, optional extras) and they'll go away and bring you back the best options. While brokers have become less popular with the rise of price comparison websites, they remain an excellent option for anybody who prefers a personal touch.

Also, brokers often have close relationships with the insurers they take their quotes from, meaning they can find you deals that don't go out to the rest of the market. And it can be useful to have a market expert to talk to before signing up so you can get an idea of what other people's quotes typically consist of and how much they cost. You'll also find brokers on comparison sites (like our partner QuoteZone).

Types of Van Insurance

When looking at van insurance, the level of coverage you select will define what exactly you're covered for and how much it will cost you. Van insurance, much like car, typically comes in 3 levels:

Here is a quick overview of what is covered by the different types of van insurance:

| Types of Vehicle Insurance | Third Party Only | Third Party, Fire and Theft | Comprehensive |

|---|---|---|---|

| Repair if your vehicle is damaged in an accident |

|

|

|

| Repairs if your vehicle is damaged in a fire or stolen |

|

|

|

| Compensation if other people are injured in an accident |

|

|

|

| Damage to other people’s property |

|

|

|

Third Party Only (TPO)

Third Party Only is the most basic level of cover, and is the minimum level of insurance required by the government before you can head out onto the road. Third Party will cover you for any damages you’re at fault for to other drivers and vehicles, as well as any accidental damage to other people’s property—such as walls or light posts.

Third Party does not cover you for any damages you incur if you’re responsible for the accident, such as any medical expenses or repairs to your vehicle, so you’ll have to cover those costs yourself, nor will it compensate you if your vehicle is stolen.

Third Party, Fire and Theft (TPFT)

Third Party, Fire and Theft offers you the same protections for damages to others as TPO, but will also compensate you if your vehicle is damaged as a result of a fire or stolen. Similarly to TPO, it won’t cover you financially in any way, so any damages you incur in an accident you’re at fault for will be yours to cover.

TPFT can be a useful option for some drivers who don’t expect to be at fault for any accidents, but would like to protect their vehicle against things out of their control. And while you might expect to pay more for it than TPO, our research indicated this is often not the case—insurance companies might assume that the riskiest drivers default to the lowest level of coverage, and that smarter, safer drivers are more likely to look for more protection.

Comprehensive

Comprehensive van insurance offers you the highest possible level of protection. It includes everything in the previous two levels, but adds cover for any damages you incur in the event of an accident. It’ll cover you irrespective of who is at fault for your accident, and includes some additional incidents such as flood damage.

While it can be the most expensive option (although often isn't, as explained below) the additional protections are usually good value for money. Consider the costs if you were ever at fault for an accident, and what the implications might be of having to repair or replace your van versus the cost of an annual comprehensive policy.

FAQs

'Any driver' van insurance (as opposed to 'insured' or 'insured + named') allows anybody to drive your vehicle and still be covered. It will typically come in age categories (usually over 21, over 25 or over 30) and means you're insured while somebody who meets the age criteria is behind the wheel.

It's extremely popular with big businesses that typically have a lot of different people driving the same vehicle. While naming each driver on the policy may be more cost effective (allowing insurers to conduct background checks on each driver), an 'any driver' policy can save you admin time taking people on and off of the policy when required, and give you peace of mind that your vehicle is insured at all times.

Multi van insurance, often referred to as fleet insurance, allows you to insure multiple vehicles under one single policy. It's considerably more time effective than insuring each one individually, and insurers will often offer discounts the more vehicles you insure with them.

It'll be worth shopping around and seeing what the best deal is, and if the vans in your fleet vary a lot in power and size then it may be cheaper to insure some/all of them individually, but many business owners enjoy the convenience of having one, single provider that they can contact if something ever does go wrong.

Business van insurance, often referred to as commercial van insurance, covers your van if its used to support your business. This could include things such as:

- Carrying stock

- Moving tools from one location to the next

- Making deliveries to customers

- Driving to work or between customers

Instead of a business van insurance policy, a private van insurance policy can cover social use only. That is, a vehicle is not driven in any way connected to work—not even to commute. If you're using the van for any type of business-related driving then look into upgrading to a 'business van insurance' policy. Read more in our article What’s the difference between private and business van insurance?

Hire and reward refers to the use of your vehicle in return for payment. This can include things such as courier work or taking passengers from A to B. If you're not carrying passengers or using your vehicle in return for payment directly, for example as part of normal business operations, such as taking tools to a client's site, then you'll only need a form of commercial vehicle insurance.

Vans/people carriers used to move things in return for payment, however (perhaps for a taxi company or a digital app) would need a form of courier insurance to be properly covered. Courier insurance is a complicated business due to the risks of carrying goods and passengers, so check with your provider before signing up to see what their policy is.

Does a van really need insurance?

Absolutely—vans in the United Kingdom are legally required to hold a form of insurance before being driven on public roads. The only exception to needing insurance is if the van isn't in use and is kept off the road, such as in a secure garage or on your drive.

The punishments for being caught driving uninsured are severe. Even if you're not involved in an accident, you can be fined up to £300 and issued with 6 penalty points.

If the case goes to court, which may happen if an accident has occurred and there are damages involved, then the court is within their power to issue you an unlimited fine and to disqualify you from driving permanently. Police may also seize (and in some cases destroy) any vehicle that has been driven uninsured.

Make sure you've got the correct coverage too—if you've failed to obtain the appropriate license (for example, if you're using your social, domestic & pleasure policy for business purposes) then your insurer may void your coverage and the law will view you as having driven uninsured.

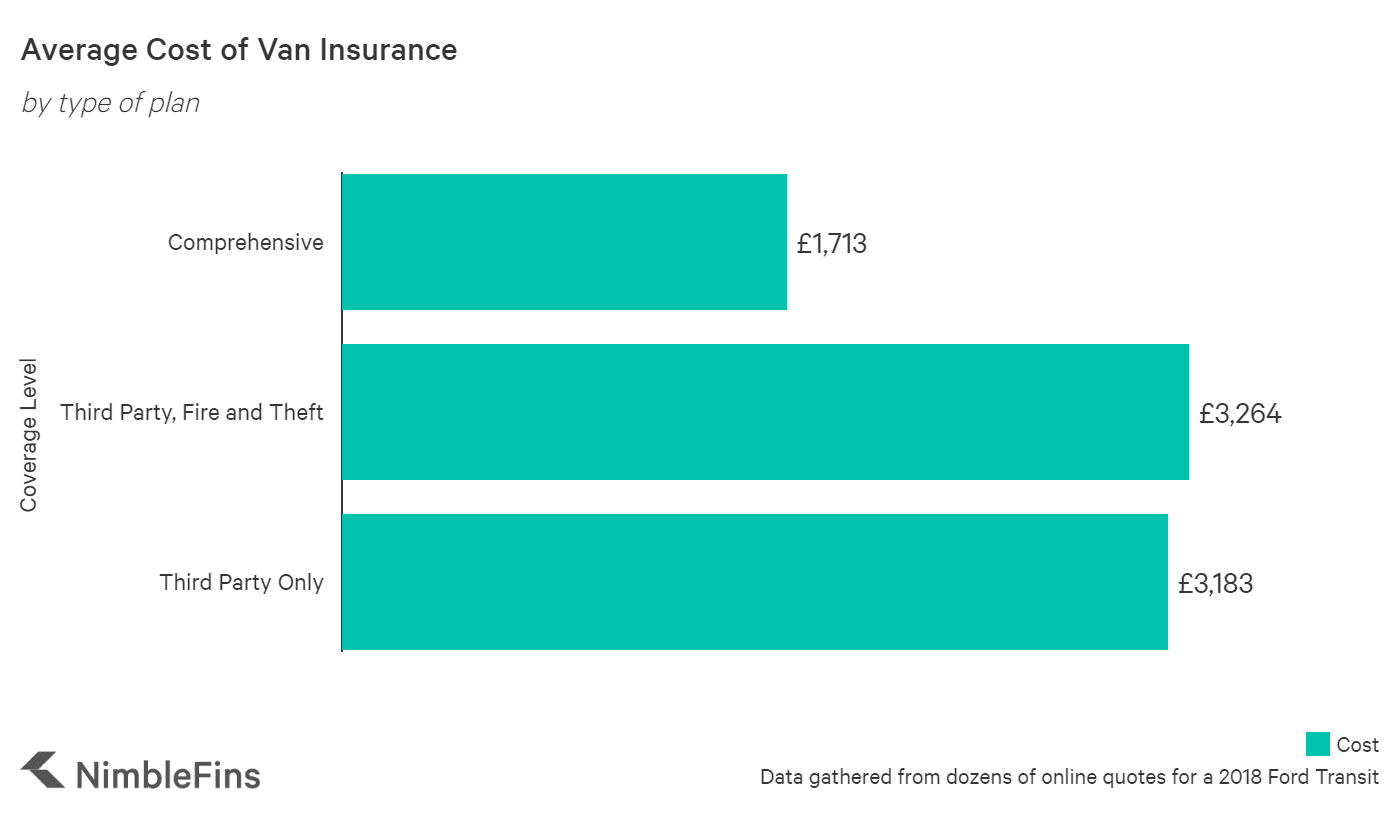

How much does van insurance cost?

The average cost of comprehensive van insurance is just over £1,700 per year. Interestingly, over the dozens of quotes we gathered, comprehensive was by far the cheapest plan, by almost 50%. So despite paying for much more protection, you'll actually be saving money on your van insurance by opting for the higher coverage level.

This may be due to a few reasons. Firstly, insurers might find that historically riskier drivers automatically choose the lowest coverage level, assuming it's going to be the cheapest. However, safer drivers (less likely to be involved in an accident) are more risk averse, and so prefer higher levels of coverage, despite being unlikely to ever require it.

| Average Cost of Van Insurance | Cost |

|---|---|

| Comprehensive | £1,713 |

| Third Party, Fire and Theft | £3,264 |

| Third Party Only | £3,183 |

How can I save money on my van insurance?

Saving money on your van insurance is quite similar to the methods you might use when trying to save on car or motorbike insurance. Here's some ideas on how you might save:

- Choosing a different level of coverage: Check prices for all three types of van insurance before you buy. Surprisingly, you might be able to save money buying a comprehensive policy.

- Picking a van that is cheaper to insure: Vans in a lower insurance group and worth less are typically cheaper to insure.

- Comparing quotes from multiple providers: Prices can vary by 300% or more from one insurer to another, so checking the market is always a good idea if you’re hunting for a discount.

- Increasing your voluntary excess: A higher excess means you’ll pay more towards a claim, which can lower your premium (but it’s not always worth it).

- Paying annually instead of monthly: Monthly payments can add 20% or more to your van insurance costs due to the finance charges.

- Installing a black box: Telematics policies enable the insurer to track your driving style, rewarding safe drivers with lower premiums.

- Strong No Claims Discount: A no claims discount of 5 years or more can save you up to 75% on your van insurance premium.

- Avoid optional extras: Extras can add significantly to a premium, so think about whether or not you really need them before making a purchase; also look for policies that include extras as standard without an extra charge.

- Lower mileage per annum: All else equal, fewer miles means less change of a collision; but be honest because if you lowball your mileage your insurer could invalidate your insurance.

Some more van specific methods might include:

- Smaller vehicle frame: Smaller vehicles are easier to manoeuvre and take up less space on the roads.

- Increased security: Alarms and trackers make it easier to find your van if it's stolen.

- Business advertisement on van: Studies prove that thieves are less likely to steal a van if it has a company's contact details and location on it, so insurers may offer a discount if your van is easily identifiable as belong to you/your business.

And it's important to keep in mind that many other factors affect the cost of van insurance, from whether you use the van for business or private use, or even if there is signwriting on the van.

Van Broker Reviews

The Van Insurer, who partners with dozens of van insurance providers, has created a brilliant table of customer ratings for brokers that sell van insurance. Because while price is certainly top of mind for most people, it's also important to get a handle on how well a company fares when it comes to customer service, ease of purchasing, making documentation readily available, etc. Here are the results. Before buying a policy, you might also want to check Reviews.co.uk or Trustpilot for the latest customer reviews.

While we have ranked the brokers by overall score below, keep in mind that ratings based on a handful of reviews (e.g., Swiftcover, Zenith, Hughes, etc.) are not as reliable.

| Rank | Van Insurance Broker | # of Customer Reviews | Overall Rating (out of 5 stars) | Customer Service | Documentation | Ease Of Purchase | Policy Features | Value For Money |

|---|---|---|---|---|---|---|---|---|

| 1 | Swiftcover Insurance | 2 | 5 | 5 | 5 | 5 | 5 | 5 |

| 2 | Zenith Insurance | 9 | 5 | 5 | 5 | 5 | 5 | 5 |

| 3 | Zenith Plus Insurance | 9 | 5 | 5 | 5 | 5 | 5 | 5 |

| 4 | Hughes Insurance | 4 | 4.6 | 5 | 5 | 5 | 4 | 4 |

| 5 | Post Office Insurance | 103 | 4.44 | 4.55 | 4.42 | 4.54 | 4.38 | 4.49 |

| 6 | Hastings Direct Insurance | 86 | 4.37 | 4.3 | 4.36 | 4.49 | 4.29 | 4.39 |

| 7 | Direct Choice Insurance | 6 | 4.26 | 4.33 | 4.17 | 4.5 | 4 | 4 |

| 8 | Gladiator Insurance | 161 | 4.23 | 4.49 | 4.3 | 4.46 | 4.35 | 4.23 |

| 9 | Geoffrey Insurance Services | 1 | 4.2 | 4 | 4 | 5 | 4 | 4 |

| 10 | Budget Insurance | 167 | 4.12 | 4.21 | 4.11 | 4.27 | 4.25 | 4.26 |

| 11 | Grove & Dean Insurance | 6 | 4.08 | 4.4 | 4 | 4 | 4.2 | 3.8 |

| 12 | Principal Insurance | 22 | 4.05 | 4.33 | 4.07 | 4.4 | 4.07 | 4.07 |

| 13 | One Call Insurance | 18 | 4.04 | 4.06 | 4 | 4.22 | 3.76 | 4.06 |

| 14 | Quoteline Direct Insurance | 62 | 4.03 | 4.24 | 4.06 | 4.33 | 4.29 | 4.22 |

| 15 | Octagon Insurance | 24 | 4.01 | 4.05 | 3.91 | 4.6 | 4.19 | 4.24 |

| 16 | Admiral Insurance | 83 | 3.96 | 3.91 | 4.14 | 3.94 | 3.79 | 3.76 |

| 17 | GoSkippy Insurance | 49 | 3.95 | 3.95 | 3.9 | 4.19 | 4.05 | 4.14 |

| 18 | Dial Direct Insurance | 63 | 3.89 | 3.98 | 3.98 | 4.18 | 3.98 | 3.84 |

| 19 | Autonet Insurance | 98 | 3.78 | 3.74 | 3.52 | 4.1 | 3.78 | 3.88 |

| 20 | Autonet Plus Insurance | 98 | 3.78 | 3.74 | 3.52 | 4.1 | 3.78 | 3.88 |

| 21 | Autonet Protect Insurance | 98 | 3.78 | 3.74 | 3.52 | 4.1 | 3.78 | 3.88 |

| 22 | Autonet Protect Plus Insurance | 98 | 3.78 | 3.74 | 3.52 | 4.1 | 3.78 | 3.88 |

| 23 | Flux Direct Insurance | 75 | 3.68 | 3.76 | 3.7 | 3.83 | 3.7 | 3.58 |

| 24 | iGO4 Essential Insurance | 12 | 3.68 | 3.67 | 3.6 | 4 | 3.88 | 3.75 |

| 25 | iGO4 Insurance | 12 | 3.68 | 3.67 | 3.6 | 4 | 3.88 | 3.75 |

| 26 | iGO4 More Insurance | 12 | 3.68 | 3.67 | 3.6 | 4 | 3.88 | 3.75 |

| 27 | More Than Insurance | 29 | 3.64 | 3.57 | 3.75 | 3.6 | 3.57 | 3.54 |

| 28 | Van Quote Direct Insurance | 52 | 3.51 | 3.69 | 3.59 | 3.97 | 3.71 | 3.69 |

| 29 | The Insurance Factory | 13 | 3.42 | 3.11 | 3.88 | 3.44 | 4 | 3.75 |

| 30 | Performance Direct Insurance | 19 | 3.25 | 3.64 | 3.36 | 3.4 | 3 | 3.4 |

| 31 | RAC Insurance | 12 | 3.23 | 3.17 | 3.17 | 2.67 | 3.5 | 3.67 |

| 32 | Nova Insurance | 15 | 3.13 | 3.08 | 3.33 | 3.25 | 3.17 | 3 |

| 33 | One Insurance Solution | 12 | 3.04 | 3.25 | 3.38 | 3.38 | 3.57 | 3.25 |

| 34 | Churchill Insurance | 9 | 2.75 | 2.75 | 2.25 | 2.75 | 3 | 3 |

| 35 | First Insurance | 13 | 2.35 | 2.86 | 2.88 | 2.86 | 2.71 | 2.63 |

| 36 | Acorn Insurance | 17 | 2.2 | 2 | 1 | 2 | 2 | 4 |

| 37 | Complete Van Cover Insurance | 5 | 1.2 | 1 | 1 | 1 | 2 | 1 |

| 38 | Masterquote Insurance | 1 | 1.2 | 1 | 2 | 1 | 1 | 1 |

Additional Information on Van Insurance

Optional Extras

As with any form of insurance, you're likely to find a number of extras available to you at sign-up. Here's a quick rundown on what they are.

| Common Extras for Van Insurance | |

|---|---|

| Legal Cover | Offers financial protection for any legal expenses incurred due to an accident that wasn't your fault |

| Breakdown | Provides assistance if your vehicle breaks down, such as if your battery dies or a tyre punctures. |

| Goods in Transit | Covers you for against theft, loss or damage while transporting your product, tools or equipment |

| Courtesy Vehicle | A replacement vehicle if yours is out of action |

| Windscreen Cover | Usually not automatically covered by your policy, pays for repairs or replacement if your windscreen is chipped |

| Personal Accident | Offers compensation if you are severely hurt while driving your van |

No—you'll need a separate policy for your van in order to drive it legally.

You can claim back VAT on a van purchase, but there's no VAT on van insurance. Instead, there's another tax on insurance called Insurance Premium Tax (IPT).

Note, if you do use your van for personal purposes (even things as simple as driving down to the local shops or into town) then you won't be able to claim VAT back on the purchase of it.

However, typically you are able to reclaim VAT on any business-related running/maintenance costs (such as repairs or parking fees) or any accessories you've added to the vehicle to support your business (such as internal racking or a dash cam).

If you have any additional questions, have a look at the Government's guide to reclaiming VAT.

The Motor Insurance Database has information on all vehicles insured in the UK. Click through the link, and make a subject access request, which will tell you who your vehicle is currently insured with (and who you were previously insured with, up to the last 7 years).

These requests are usually free, but during busy periods there can be a small administrative fee.

Insurance companies are required by law to allow you to cancel your policy during the first 14 days— a "cooling off" period. Be cautious of a couple of things, however—you may incur a cancellation fee, so check this with your provider, and the insurer may ask to see proof that you've either sold the vehicle or taken on an alternative policy. This is simply due to the fact that it's illegal to drive a van on the roads with no forms of insurance, and they're covering themselves from a legal perspective if you are involved in an accident after cancelling with them.

No—your van insurance will typically not include any tools coverage, but you may be able to add it to your policy for an additional cost (providing your insurer offers it). Your insurer may ask during the signing up process if you'd like to add a goods in transit policy

Find van insurance today.

Powered by QuoteZone.

Get Quotes

- Rated 4.8 out of 5 stars on Reviews.co.uk

- Fill out one form, get up to 60 quotes

- Buy online or by phone

Note regarding savings figures: *For information on the latest saving figures, pay-less-than figures, and pay-from figures used for promotional purposes, please click here.