The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Car Insurance for Convicted Drivers

Getting a motoring conviction is expensive. Our NimbleFins car insurance experts found that car insurance rates with a conviction cost up to 20% more with a SP30 speeding conviction.

Recent Ministry of Justice data for 2024/25 confirms that fines remain the most common outcome for motoring offences, applied in 96% of cases. The average fine issued by courts has risen to £384 as of late 2025, reflecting updated sentencing guidelines introduced in April 2024. This direct cost is often only the beginning, as a conviction can lead to much larger long-term increases in annual insurance premiums.

Best Car Insurance for Convicted Drivers

Below, our NimbleFins car insurance experts report on how some of the larger car insurance providers like Admiral, Hastings and Allianz stood out for pricing policies for drivers with a conviction. For our sample driver, some insurance providers wouldn't offer cover, and the amount they raise their premiums by varies considerably.

Compare convicted driver car insurance now

- You can save up to £515*

- 4.8 out of 5 stars on Reviews.co.uk**

- Cheap quotes from 100+ providers

The cheapest and best policy for you will vary depending on all of the factors of your application, so it's critical to compare quotes yourself. Other providers not mentioned may give you the best rates. Please use this information for general informational purposes only as you will certainly differ from our sample driver. It's critical to compare deals yourself to find a cheap car insurance company—especially if you have a conviction.

Car insurance for drivers with a speeding conviction

The big insurers typically raise premiums under 20% for a SP30 speeding conviction. Of the main insurers, we found that Allianz (previously 'Flow') was the cheapest for drivers with a speeding conviction, raising rates 16% for our sample driver. Drivers with speeding convictions are deemed to be more dangerous and a higher insurance risk, so rates typically rise after a conviction. But some insurers raise rates more than others.

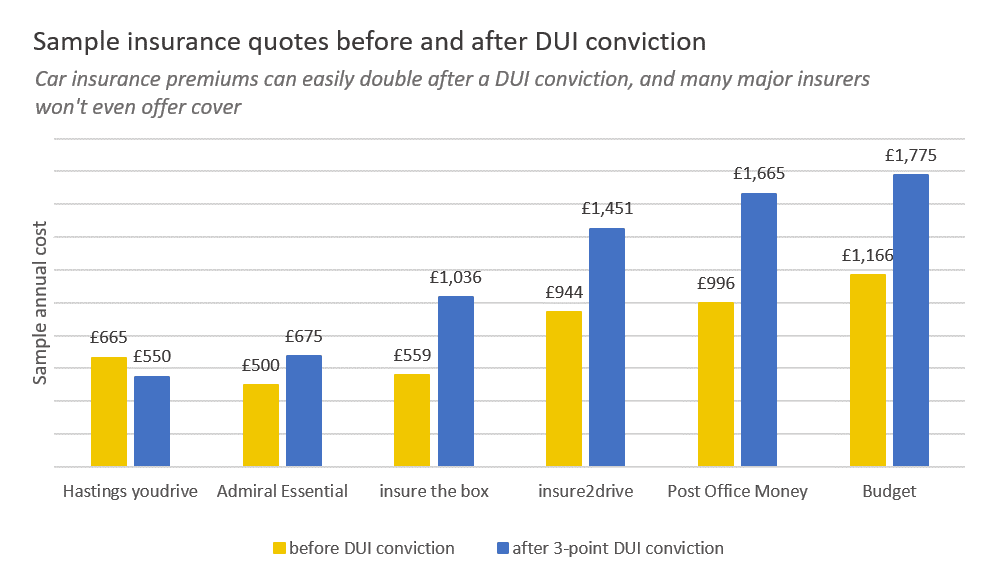

Car insurance for drivers with a drink and drug driving conviction (DUI)

For those with a drink and drug driving conviction, our research showed that the majority of the big insurers will not even offer cover, even at a high premium. But Hastings offered the most competitive quotes via their youdrive telematics offering. And Admiral was the large insurance company likely to provide the best quotes for non-telematics cover post DUI conviction (the cheapest being Admiral Essential but higher tiers of cover were also available). Expect rates to go up 50% or more in most cases after DUI.

In general, fewer insurers are willing to insure motorists after these types of under-the-influence convictions. Those with a DUI will have a more limited selection of options and other than Admiral, may need to look at niche providers. For example, our sample driver could not get quotes from Allianz, Direct Line (including their Churchill and Privilege brands), Aviva (including QuoteMeHappy) or AXA (including Swiftcover). Other large companies may underwrite cover to convicted motorists who use a specialist broker who can work on their behalf.

Car insurance for drivers after an at-fault accident

At-fault accidents can increase car insurance rates by 20% or more, but our research showed that Admiral tends to raise rates the least after a claim (on a percentage basis), but Allianz (previously 'Flow') had the cheapest for our sample driver (due to a lower rate pre-accident).

How to get convicted driver insurance

While the cost of insurance will surely be higher if you have a conviction, having points on your licence does not mean you won't be able to find cover.

Most comparison sites and household-name insurance companies are equipped to handle motor insurance for convicted drivers—to an extent. That is, they can pretty easily handle a driver with a few points for speeding, for example.

That said, the ease with which a driver can get cover does depend how many points you have and what offences you committed. The higher the perceived risk, the harder it will be to find cover. Especially at an affordable price from a cheap car insurance company.

Drivers with more serious offences may need to go to a specialist provider or broker to find convicted driver insurance. One Sure Insurance and Adrian Flux are examples of brokers that specialise in convicted driver insurance.

What information you'll need to provide

In addition to the normal questions a driver is asked about their history, like what type of licence you hold and the number of years you've held it, you'll also need to answer questions about your convictions. This is so that the insurer can properly assess the risk and price your insurance correctly.

Here are examples of what a convicted driver insurer will want to know before supplying a quote:

- Date of the conviction

- Did you receive penalty points?

- Were you fined for the conviction?

- Did the conviction result in a driving ban?

How long do points stay on your licence?

Motoring convictions affect insurance for 4 or 11 years, depending on the offence.

Is driving without insurance a conviction?

Yes, driving without insurance is conviction code LC20, which is worth 3 to 6 points and stays on your record for 4 years from the date of the offence.

Can insurance companies find out about convictions?

Yes, car insurance companies will find out about convictions. They check driving records with the MyLicence system, which holds a record of all motoring convictions.

When you get quotes through a comparison site, the quotes you receive back will not reflect your conviction (unless you've told them in the quote forms). This is because comparison sites won't check the MyLicence system. However, that doesn't mean you can cheat your way through the system.

Car insurers will check your driving record with MyLicence. If you haven't disclosed convictions then when the insurer finds out the truth they will invalidate your insurance.

Do I have to declare spent convictions to insurance companies?

No, according to Under the Rehabilitation of Offenders Act 1974 you no longer have to declare spent conviction to insurance companies. Once they are spent, they no longer count against you.

Common Types of Convictions

While there are dozens of conviction codes, as you might expect some are more common than others. The most frequently committed offences relate to speeding, drink driving, driving uninsured, driving whilst using a mobile phone and traffic light offences. In fact, 85% of motoring convictions are for speed limit offences.

The table below show the number of points for each of these common offences, and how long they last on your driving record (and therefore, how long they impact your insurance rates!).

| Code | Offence | Penalty Points | Years on driving record from date of offence |

|---|---|---|---|

| SP30 | Exceeding statutory speed limit | 3 to 6 | 4 years |

| DR10 | Driving with alcohol level above limit | 3 to 11 | 11 years |

| IN10 | Driving uninsured | 6 to 8 | 4 years |

| CU80 | Driving whilst using a mobile phone | 3 to 6 | 4 years |

| TS10 | Traffic lights offence | 3 | 4 years |

| SP50 | Exceeding motorway limit | 3 to 6 | 4 years |

| LC20 | Driving not in accordance with a licence | 3 to 6 | 4 years |

| CD10 | Driving without due care and attention | 3 to 9 | 4 years |

| SP60 | Undefined speeding offence | 3 to 6 | 4 years |

| SP10 | Speeding, goods vehicle | 3 to 6 | 4 years |

Number of Motoring Convictions UK

Home Office statistics for 2024 reveal a significant upward trend in enforcement, with 3.1 million motoring offences resulting in a fixed penalty notice (FPN) or court prosecution.

Speeding continues to dominate the charts, accounting for 2.71 million (87%) of these offences. This surge is largely attributed to the expanded use of AI-powered and average speed cameras, which now detect 96% of all speeding violations in England and Wales.

As of the August 2025 DVLA snapshot, there are 42,504,180 full and provisional licence holders in Great Britain. Our analysis shows that over 3.02 million drivers currently have penalty points on their record, meaning approximately 7.1% of all GB drivers have a conviction. Of these, 2,144,200 (71%) hold 3 points, while 634,200 (21%) have 6 points. Interestingly, the number of drivers facing disqualification with 12 or more points has reached 10,000, a record high.

In the table below is a snapshot of DVLA driver licence data (August 2025).

| Points on Record | Number of Drivers | % of Convicted Drivers |

|---|---|---|

| 3 Points | 2,144,200 | 71% |

| 6 Points | 634,200 | 21% |

| 9 Points | 181,200 | 6% |

| 12+ Points | 60,400 | 2% |