How do car insurance companies make money?

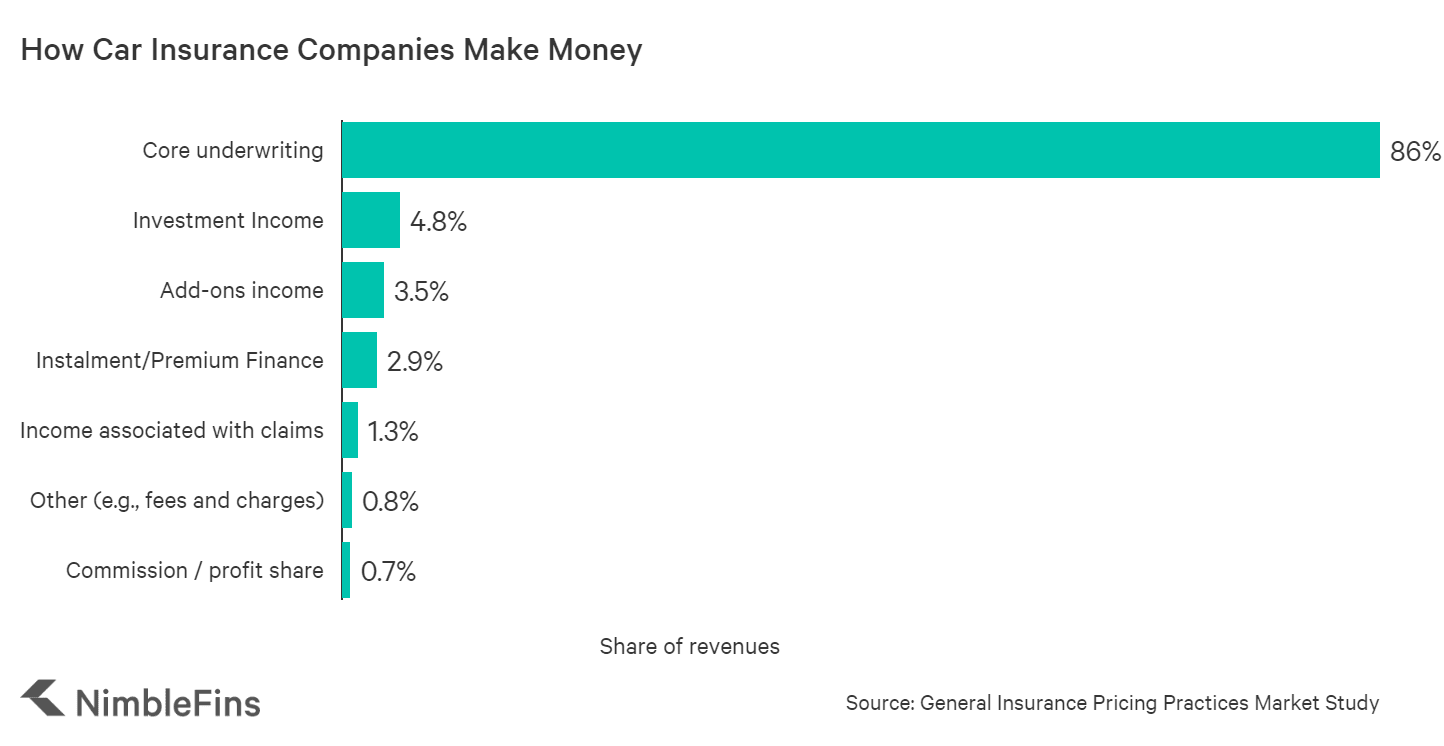

According to the FCA's General Insurance Pricing Practices Market Study, motor insurers earn 86% of their money from core underwriting activities (that is, premiums earned from selling motor insurance policies). The other 14% of income comes from non-core activities like selling add-ons (e.g., legal or breakdown cover), premium finance (charges earned when customers pay monthly instead of annually), investments, fees & charges (e.g., cancellation charges) and even money earned through claims.

| How do car insurance companies make money? | Share of revenues |

|---|---|

| Core underwriting | 86.0% |

| Investment Income | 4.8% |

| Add-ons income | 3.5% |

| Instalment/Premium Finance | 2.9% |

| Income associated with claims | 1.3% |

| Other (e.g., fees and charges) | 0.8% |

| Commission / profit share | 0.7% |

| Total | 100% |

Are car insurance companies profitable?

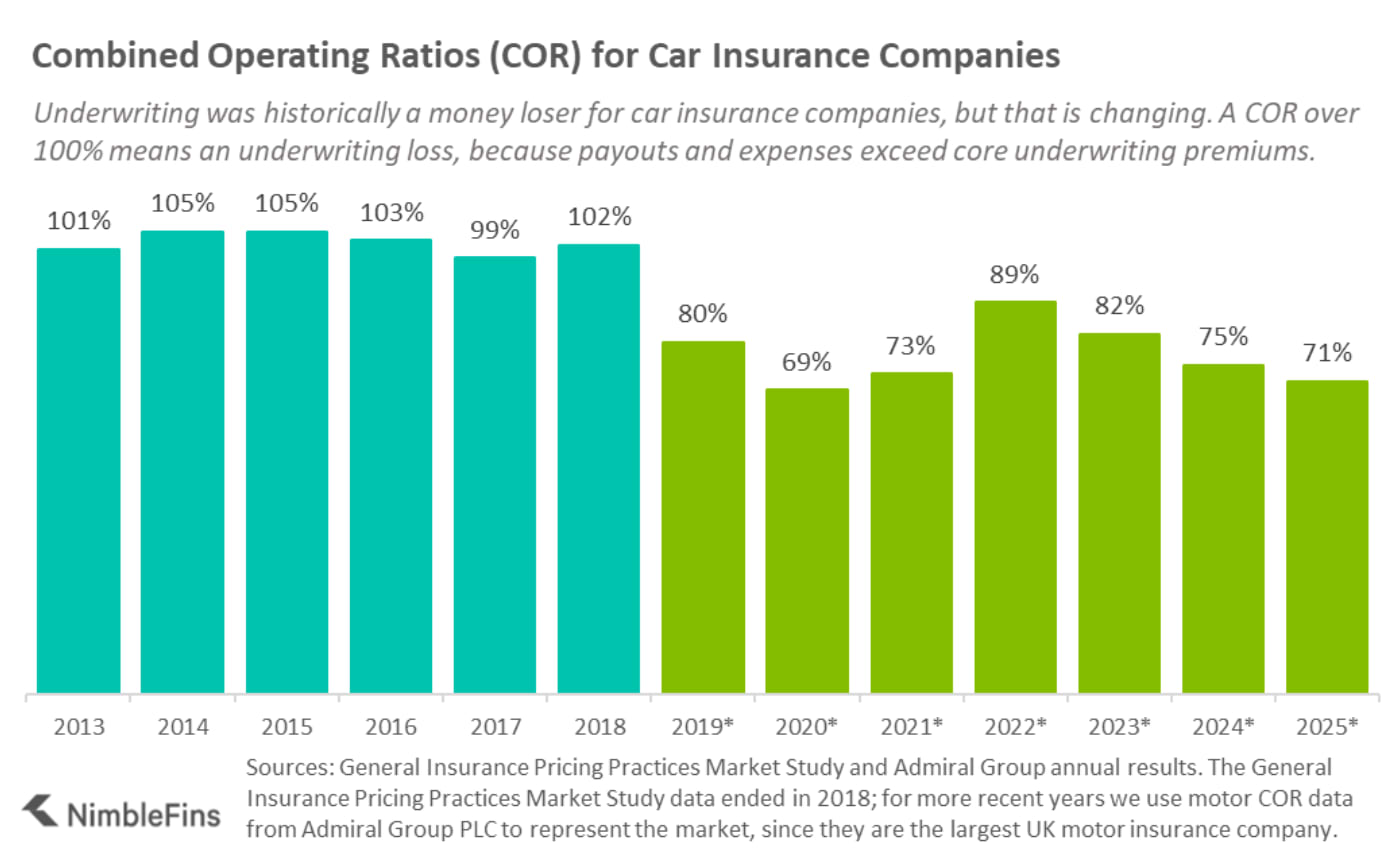

While core underwriting generates the lion's share of revenues (86%), underwriting has not generally been considered to be profitable for car insurers. The Loss Ratio (i.e., claims/premium) for car insurers was historically around 75%, which does mean car insurers pay less in claims than they take in premiums. However, once you factor in the expenses of running an insurance business (e.g., staff, IT, etc.) then car insurers typically have spent more on expenses and claim payouts than they earned in core underwriting premiums. This information reflects data from the General Insurance Pricing Practices Market Study.

Since the General Insurance Pricing Practices Market Study has not been updated lately, to understand car insurance profitability in more recent years, the NimbleFins car insurance experts have studied the annual reports of the Admiral Group PLC—we believe Admiral would be a good proxy for the market as a whole, since Admiral is the largest UK motor insurance company.

This more recent data from 2019 through 2025 shows that car insurance has generally become more profitable for insurance companies in the past few years. In fact, in H1 2025 the Admiral Group PLC's motor insurance COR was 71%, a drop from 88.9% in 2022.

This means that motor insurance companies rely on non-core sources of revenue like add-ons to stay in business. But the largest source of non-core revenues might be a surprise—it's investments (not fees & charges, as some policyholders might believe). Let's look at all of the core and non-core revenue sources for UK car insurers.

Underwriting

Underwriting accounts for 86% of car insurance revenues on average, and is considered "core revenue". The primary source of income for car insurers is premiums earned on sold car insurance policies. In return, car insurers agree to pay out on valid claims. As mentioned above, core underwriting is not usually profitable for motor insurance companies—that is, premiums earned are not usually sufficient to cover claims payouts and business expenses.

Investments

Car insurance companies typically have investment portfolios composed of a mix of assets like stocks, bonds and other investments. This portfolio of assets generates revenues including interest payments, dividends and capital gains, which typically account for 4.8% of total revenues (or 34% of non-core revenues). This means that investments are the highest non-core contributor to income.

Add-ons

Insurance companies make extra money above and beyond their core underwriting activities by selling extra features as add ons. According to the FCA's General Insurance Pricing Practices Market Study, the share of revenue from add-ons ranges from 20% to 81% of total non-core revenue—with add-ons accounting for 25% of non-core revenue on average. Add-ons account for 3.5% of total income.

While top-tier policies might be laden with extra features, lower-tier policies can be enhanced and customised by adding these extra features. Common car insurance add ons include:

- Breakdown

- Legal expenses

- Personal accident

- Key cover

- Enhanced courtesy car

The largest share of add-on revenue comes from legal expenses (48%) followed by breakdown cover (22%) and courtesy car (11%). They also found that one in three (32%) of motor insurance customers are sold at least one add on.

Premium finance

Premium finance is money earned by insurers for lending funds to policyholders, enabling customers to make monthly instalment payments instead of paying upfront. Just as a credit card holder pays finance charges for borrowing money, an insured customer typically pays finance charges if they opt to pay monthly, because they're borrowing money to do so.

Premium finance accounts for around 2.9% of total income and 21% of non-core income on average. Of 7 major insurers analysed by the FCA, the amount earned on premium finance was between £3 and £110 per policy.

Some insurers (e.g., NFU Mutual) don't charge any extra to make monthly payments, but most do. In fact, many insurers charge north of 20% APR to customers wanting to make monthly payments. While the APR is variable with some providers (e.g., AXA and Direct Line), insurers charging a fixed APR typically charge between 21% and 27.5% APR.

Revenue associated with claims

While insurers lose money on claims, they also make money on claims. Motor insurers earn income from referral fees, rebates and profit shares (e.g., from 3rd party repair businesses). For example, an insurer could get a fee for referring a customer to a partner chain of repair centres. Revenues associated with claims account for 1.3% of total income and 9% of non-core income on average.

Fees & charges

A further 0.8% of total revenues (6% of non-core revenue) comes from others sources like fees and charges. Many insurers charge for a policyholder to make a change to their policy (e.g., to change the vehicle or address) or to cancel a policy early. The average cost to cancel car insurance is around £55 after the cooling-off period.

Proft share / commissions

Finally, car insurers also earn money through profit share arrangements with intermediaries.