Brits are Buying More Expensive Cars

The number of cars registered in Great Britain continues to increase each year, as it has for nearly the past 75 years. In fact, the rise is generally quite reliable, with the number of licensed cars rising 1% to 2% in most recent years. However, digging deeper into the data we identified trends regarding the types of cars people are buying. That is, Brits are buying a significantly higher proportion of luxury/premium cars now than they did in 2012.

Increasing Proportion of Luxury/Premium Cars

Diving into statistics from the Department for Transport, we found that there's been a consumer shift towards luxury/premium cars in Great Britain over the past few years. Analysis of license data from premium/luxury brands (e.g., BMW, Audi, Mercedes, Land Rover, Mini, Jaguar, Lexus, Porsche, Alfa Romeo, Jeep, etc.) and mass market brands (e.g., Ford, Vauxhall, Volkswagen, Nissan, Toyota, Peugeot, Renault, Honda, Citroen, Hyundai, etc.) showed that luxury/premium car brands comprised about 24% of all cars in 2019 in Great Britain compared to the 18% they represented in 2012, with the proportion of mass market brands declining by 6 percentage points from 82% to 76% over the same time period.

Luxury/Premium Car Trends

In the seven years from 2012 to 2019, there was a 51% increase in the number of luxury/premium cars licensed in Great Britain. In terms of actual cars, the number of luxury/premium cars on the road increased from 4.957 million in Q1 2012 to 7.480 million in Q1 2019—an increase of 2.523 million cars.

For instance, there were just under 1 million Audis in Great Britain at the beginning of 2012. By March 2019, the number of Audis increased 67% to over 1.6 million cars on the road. Similarly, other high end brand car makers have been increasing their presence dramatically in Great Britain, with 16 out of the top 20 we looked at increasing their numbers by double digits in seven years. Lotus, Daimler and Alfa Romeo were the only premium makers with fewer cars licensed in Great Britain in 2019 than in 2012.

| Top 20 Premium Cars in GB | 2012 (Q1) | 2019 (Q1) | Percentage Change (2012 - 2019) |

|---|---|---|---|

| BMW | 1,271,553 | 1,820,582 | 43% |

| AUDI | 990,268 | 1,651,540 | 67% |

| MERCEDES | 995,530 | 1,516,900 | 52% |

| LAND ROVER | 531,081 | 793,558 | 49% |

| MINI | 409,541 | 747,258 | 82% |

| JAGUAR | 286,577 | 361,778 | 26% |

| LEXUS | 119,820 | 154,332 | 29% |

| PORSCHE | 97,112 | 145,547 | 50% |

| ALFA ROMEO | 104,734 | 86,353 | -18% |

| JEEP | 71,855 | 80,942 | 13% |

| BENTLEY | 18,308 | 23,968 | 31% |

| ASTON MARTIN | 15,556 | 20,111 | 29% |

| TESLA | 53 | 12,730 | 23919% |

| LOTUS | 12,388 | 11,322 | -9% |

| FERRARI | 7,139 | 10,529 | 47% |

| MASERATI | 4,636 | 10,191 | 120% |

| ROLLS ROYCE | 8,901 | 9,669 | 9% |

| INFINITI | 702 | 9,603 | 1268% |

| DAIMLER | 6,252 | 5,387 | -14% |

| LAMBORGHINI | 903 | 2,393 | 165% |

| Top 20 Premium Cars | 4,952,909 | 7,474,693 | 51% |

| All Premium Cars | 4,956,538 | 7,479,841 | 51% |

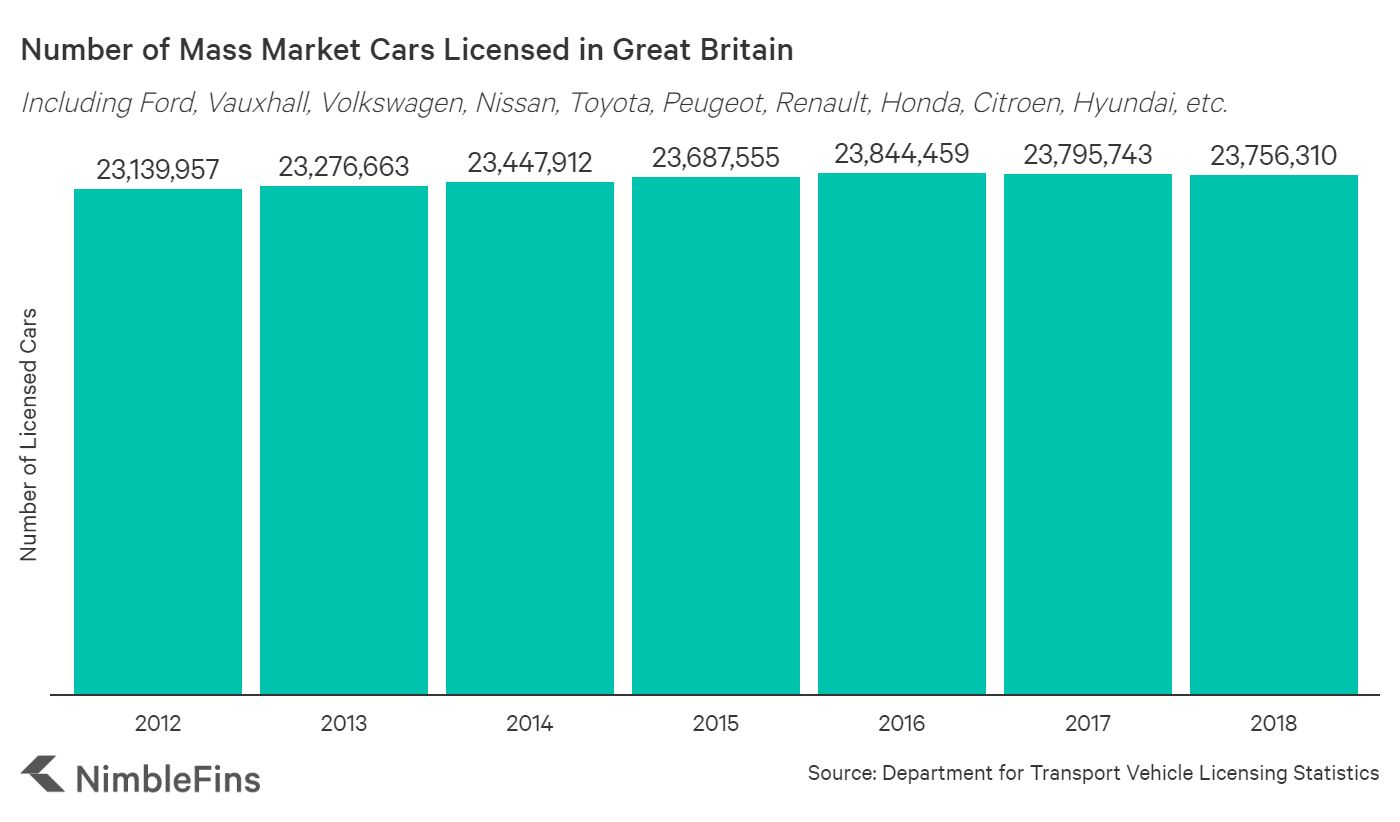

Mass Market Car Trends

In contrast, the number of mass market cars has remained relatively flat overall, growing only 3% in the past seven years—there were 23.151 million mass market cars on the road in Q1 2012 and 23.809 million by Q1 2019.

However, while the demand for mass market cars has remained relatively flat there have certainly been significant shifts in terms of which brands are most popular with consumers. For example, the number of Hyundais, Kias, Skodas and Dacias increased over 50% from 2012 to 2019. Offsetting these gains there are now 20% fewer Peugeots, 30% fewer Renaults and 46% fewer Saabs on the road now than there were in 2012. These shifts are, in part, due to complicated car alliance and ownership structures in the auto industry, through which cars are rebranded from time to time.

| Top 20 Mass Market Cars in GB | 2012 Q1 | 2019 Q1 | Percentage Change (2012 - 2019) |

|---|---|---|---|

| FORD | 4,322,587 | 4,204,309 | -3% |

| VAUXHALL | 3,501,532 | 3,297,629 | -6% |

| VOLKSWAGEN | 2,290,218 | 2,722,263 | 19% |

| TOYOTA | 1,354,892 | 1,501,960 | 11% |

| NISSAN | 1,170,606 | 1,516,142 | 30% |

| PEUGEOT | 1,840,021 | 1,431,248 | -22% |

| RENAULT | 1,597,890 | 1,068,500 | -33% |

| HONDA | 1,030,211 | 1,053,461 | 2% |

| CITROEN | 1,079,200 | 986,092 | -9% |

| HYUNDAI | 439,021 | 821,060 | 87% |

| KIA | 362,182 | 796,584 | 120% |

| SKODA | 426,906 | 733,625 | 72% |

| FIAT | 723,301 | 692,900 | -4% |

| VOLVO | 498,022 | 564,186 | 13% |

| MAZDA | 507,908 | 554,278 | 9% |

| SEAT | 343,711 | 528,389 | 54% |

| SUZUKI | 329,970 | 438,551 | 33% |

| MITSUBISHI | 246,164 | 228,357 | -7% |

| DACIA | 7 | 140,612 | 2008643% |

| SAAB | 202,056 | 99,754 | -51% |

| Top 20 Mass Market Cars | 22,266,405 | 23,379,900 | 5% |

| All Mass Market Cars | 23,151,241 | 23,808,678 | 3% |

Car Finance Used by Many

How are consumers paying for these more expensive cars? Despite a recent pullback in car finance popularity, consumers are still relying on car financing a lot more than they used to. From Q4 2012 to Q1 2019 when the number of cars on the road only increased 10.3%, the number of (used and new) cars bought through financing from a dealer rose 67%, implying that a larger proportion of cars is purchased through car financing instead of cash. Additionally, the value of car financing has increased even more—124% over the same time period—suggesting that consumers are borrowing larger amounts for each car purchase.

Methodology

To identify trends in consumer desire for premium cars and mass market cars in Great Britain, we analysed vehicle licensing statistics from the Department of Transport. We compared licensing data from year end in 2012 and 2019, having grouped car makes into either "mass market" or "premium" categories as follows:

Mass Market Cars

- ABARTH

- ACURA

- ALPINA

- ALPINE

- AVTOVAZ

- BUICK

- CHEVROLET

- CHEVROLET GMC

- CHRYSLER

- CITROEN

- DACIA

- DAEWOO

- DAIHATSU

- DATSUN

- DODGE

- DODGE (USA)

- DOUGLAS

- DS

- FIAT

- FORD

- GEELY

- GENERAL MOTORS

- GREAT WALL

- HONDA

- HYUNDAI

- ISUZU

- KIA

- LADA

- LANCIA

- MAZDA

- MERCURY

- MITSUBISHI

- NISSAN

- OLDSMOBILE

- OPEL

- PEUGEOT

- PLYMOUTH

- PONTIAC

- RENAULT

- ROVER

- SAAB

- SATURN

- SEAT

- SKODA

- SSANGYONG

- SUBARU

- SUZUKI

- TATA

- TOYOTA

- VAUXHALL

- VOLKSWAGEN

- VOLVO

Premium Cars

- ALFA ROMEO

- ASTON MARTIN

- AUDI

- BENTLEY

- BMW

- BUGATTI

- CADILLAC

- CORVETTE

- DAIMLER

- DAIMLER CHRYSLER

- FERRARI

- HUMMER

- INFINITI

- JAGUAR

- JAGUAR LAND ROVER

- JEEP

- KOENIGSEGG

- LAMBORGHINI

- LAND ROVER

- LEXUS

- LINCOLN

- LOTUS

- MASERATI

- MAYBACH

- MCLAREN

- MERCEDES

- MINI

- PORSCHE

- ROLLS ROYCE

- TESLA

We also analysed car financing data from the Finance & Leasing Association to understand how consumers are affording this shift towards premium and luxury cars.