Tradesman Insurance | Quotes & Requirements

Find Tradesman insurance quotes today.

Powered by QuoteZone.

Compare Quotes

- Rated 4.7 out of 5 stars on Reviews.co.uk

- Over 300,000 QuoteZone quotes completed per month

- Fill out only one form

The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

As seen on

Tradesman Insurance

As a tradesman, you face enormous financial risks if you don't have the correct insurance coverages set up. Our in-depth guides are designed to tell you everything you need to know about the insurances available to you, including what you must have vs what's optional, plus an average cost breakdown for each trade.

If you're looking for a personalised insurance policy to help protect your business, fill out a quote form and get quotes from some of the UK's top insurance providers. Once in touch, you'll have the chance to ask any questions you might have, and pick the policy that best fits you and your business.

Popular Types of Insurance for Tradesmen

Almost all businesses, irrespective of specific trade, require some form of insurance to operate. Here are the basic types of cover you might need as a tradesman:

| Common Types of Tradesman Insurance | What it Covers | |

|---|---|---|

| 1 | Public Liability | Legal costs and compensation payments due to injury or damage claims against your business |

| 2 | Employers' Liability | Covers against injury or illness claims against you by employees. Required by law if you have employees |

| 3 | Professional Indemnity | Protects if clients believe your service or advice was negligent |

| 4 | Tools and Equipment | Pays for a replacement if your equipment is accidentally damaged, lost or stolen |

| 5 | Personal Accident/Income Protection/Critical Illness | Financial cover if you're unable to work due to injury or illness |

| 6 | Contract Works | Covers your work on-site in the event of an incident (e.g. fire or vandalism) |

| 7 | Business Vehicle Insurance | Keeps you insured on the road if you're using your vehicle for business purposes |

Do I Need Tradesman Insurance?

If you're working as a self-employed tradesman or running your own trades business then making sure you have the correct coverage is vital, and in some cases (such as Employers' Liability or Business Use Vehicle insurance) is required by law. While coverage such as Public Liability is not a legal requirement, it might be a condition of certain work contracts. And knowledgeable customers will certainly ask if you have public liability insurance in place and may even as to see your certificate of insurance.

If you're being employed by somebody else full-time then they should provide you with coverage—make sure to double check before working what you are and aren't covered for.

Public Liability insurance for Tradesmen

Tradesman Public Liability Insurance covers you if a client, third-party or member of the general public claims your work has caused property damage or injury to them. According to analysis of the latest Office for National Statistics (ONS) and ABI data, for 2026 the average public liability settlement will rise to approximately £18,200 in the UK. For a tradesperson today, the financial risk of an uninsured claim is more severe than ever, as even minor property damage or accidental injuries can lead to payouts that threaten the survival of a small business

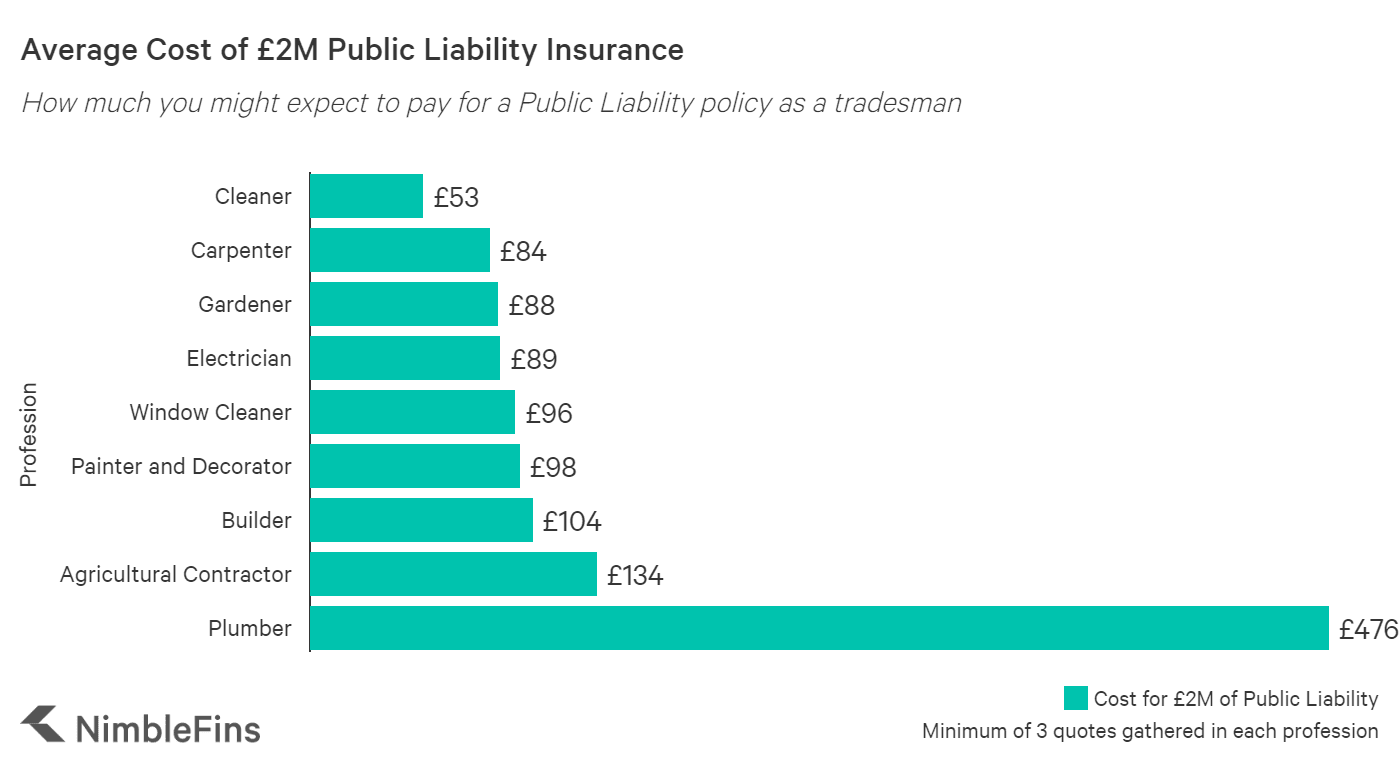

Cost of Public Liability insurance for Tradesmen

The average cost of Public Liability insurance varies dependent on insurers previous experience insuring individuals and businesses within each industry. You may also find your price varies depending on a number of different factors, such as:

- No prior claims or convictions

- More years of experience

- Working in safer locations (away from big cities, airports, power stations etc.)

Certain trades also have unique factors that may impact the final cost of your policy—for example, whether or not a builder works with asbestos or not.

Employers' Liability insurance for Tradesmen

If you employ any members of staff, irrespective of whether they're part-time, on a one-off, paid cash in hand or even a family friend, you're legally required to hold a form of Employers' Liability insurance. It'll cover any compensation award/legal costs accrued if somebody becomes unwell or is injured as a result of their work for you.

In 2026, the Health and Safety Executive (HSE) remains strict regarding mandatory coverage. You can be fined up to £2,500 for every single day you employ someone without appropriate Employers' Liability insurance in place. Furthermore, you can face a fine of up to £1,000 if you fail to display your insurance certificate or refuse to make it available to HSE inspectors upon request.

Professional Indemnity insurance for Tradesmen

Professional Indemnity Insurance protects you if a client believes you've been professionally negligent. This could include something along the lines of:

- They took your advice and incurred damages as a result

- A design you created for them had a fault and needed to be redone upon completion

- The client believes the outcome of a piece of work you've done for them isn't as agreed

- You offer training and certification as part of your business, and somebody believes your training was inadequate and caused damages

It's important to make sure your Professional Indemnity is up-to-date—it'll help protect you against any claims made from work you've completed in the past or are in the process of completing.

While it isn't mandatory to hold a form of Professional Indemnity, this list can give you a good idea of the professions that are most likely to need a policy before taking on contract.

Tools insurance for Tradesmen

Tradesman tools insurance protects your equipment against some of the unpredictable risks that can occur while you work. This includes accidental loss, some form of damages and theft or vandalism. Most forms of tools and business equipment can be covered (from hammers and screwdrivers to laptops and mobile phones) so if you do have any expensive equipment it's worth considering.

Keep in mind that Tools insurance won't cover you for most events that would be covered under a warranty (such as a mechanical or electrical failure) so make sure these are all up-to-date to ensure you're fully protected.

Business Vehicle Insurance

If you're using your own vehicle to support your business, such as by driving your tools from one client site to the next, then your insurer will require you to hold a form of business use vehicle insurance. This'll cover you for the additional wear and tear your car gathers for the additional mileage you're putting on it, plus some of the additional risks business use typically creates (such as driving on unfamiliar roads or during peak traffic).

Driving without appropriate insurance risks voiding your cover, so make sure to inform your insurer and see which level of coverage would suit you best.

Self-Employed Tradesman Insurance

Self-employed or sole trader tradesman need to protect themselves against risks of accidents affecting third parties (with public liability insurance), accidental injury affecting any employees (with employers' liability insurance), being sued for proving negligent professional designs or advice (with professional indemnity insurance), theft of tools and equipment, injury preventing you from working, and more.

FAQs

Tradesman insurance is a combination of the policies listed above, designed to protect you and your business in the event of an accident or incident. Before signing up to a policy, consider what your business does and what risks you're likely to be exposed to.

While public liability is not a legal requirement for tradesman it may be requested by a tradesman's clients (and could be a contract condition), plus public liability is a must-have protection for any tradesman given the risky nature of the work.

Claiming on your Tradesman insurance shouldn't be much more complicated than claiming on your home or vehicle insurance. Your claim is likely to be more successful (and processed more efficiently) if you can quickly provide your insurer with some of the following details:

- The time and date of the accident

- Details about what happened, where it happened, and who was impacted

- What you're claiming for, the damages to you, and how much you expected to be compensated

- Contact details for any other parties involved

- If possible, photographs of the incident

Accidents are unavoidable, but you can take steps to reduce the chances of them happening. Here's some tips that will help keep you protected, whether a claim is made against you or you're the one making a claim.

- Try to keep clients and members of the public away from areas you are working. Take extra precaution where sharp tools, debris, wires etc. are involved

- Keep the areas where you work as tidy as possible to reduce trip/damage hazards

- Log all incidents, no matter how small

- For professional indemnity claims, be clear with the client about what is achievable and make sure to have all deliverables (and any due by dates) agreed in writing

- Read through your insurance documentation and ensure that you are complying with all terms, conditions and/or requirements of the policy

All quotes were gathered for a male tradesman in NW London with less than 2 years experience. Each individual article has a breakdown of additional insurance costs if you'd like to know the cost of other coverages. No fewer than 3 quotes were gathered to generate our cost averages. These figures were adjusted in 2026 to represent market premiums for new entrants to the trade today.