The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

What Factors Affect your Car Insurance Premium?

According to our 2026 analysis, factors like age, vehicle choice, and driving history can swing car insurance premiums by 300% or more. With the average cost of comprehensive car insurance recently tracked at £559 annually (as of Q4 2025), these risk factors represent a massive financial divide.

For example, a young driver might face quotes over £1,100 higher than the national average, while a driver in a low-risk postcode with a clean record could pay hundreds less, making it vital to understand what's driving your specific quote.

Insurance companies price policies based on the level of perceived risk a motorist presents, and they price accordingly. Below our team has broken out the major factors that insurers consider when deciding just how risky you'll be to insure—these apply whether you're buying from a small or large auto insurance company. Use this important information to help you find cheap car insurance.

Number of claims and convictions filed in the last 5 years

Part of getting a car insurance quote involves answering questions about claims and accidents you've had in the past five years. You'll even be asked if you've been involved in accidents that were not your fault or for which no claim was made. You'll need to disclose this information, plus say if you've had any motoring convictions, driving licence endorsements or fixed penalties, or if you've been disqualified from driving in the past five years.

It's important to understand that claims and convictions raise the cost of car insurance. For example, our car insurance experts ran tests and found that car insurance with claims and conditions can cost 20% extra with a SP30 speeding conviction.

No Claims Discount

Having a No Claims Discount (NCD) can be a pretty straightforward path to lower auto insurance premiums. Your NCD is essentially a percentage reduction to your premium, earned if you haven’t made a claim in a certain period of time.

For every year you drive without making a 'fault' claim, your No Claims Discount (NCD) grows. While individual scales vary by insurer, a typical discount starts at 30% after one year and can climb to as high as 75% after five or more claim-free years. Most UK insurers cap the maximum discount between 5 and 9 years, though the financial impact remains substantial throughout the life of your policy.

Making a claim will reduce or eliminate your NCD. Generally speaking, the more claims you make, the more the NCD is reduced until is it totally lost. For instance, the first accident may result in your NCD being knocked back by two years. Keep in mind that every insurer operates a different set of NCD rules, both in terms of earning and losing your NCD.

Driving experience

One significant factor that impacts the cost of your motor insurance is how many years of driving experience you have. Generally speaking, more years on the road translates into lower premiums, as drivers with more experience are expected to be less likely to have a crash. Insurers will get this information in different ways. For instance, you may be asked how long you've had a licence or what year you first received your licence.

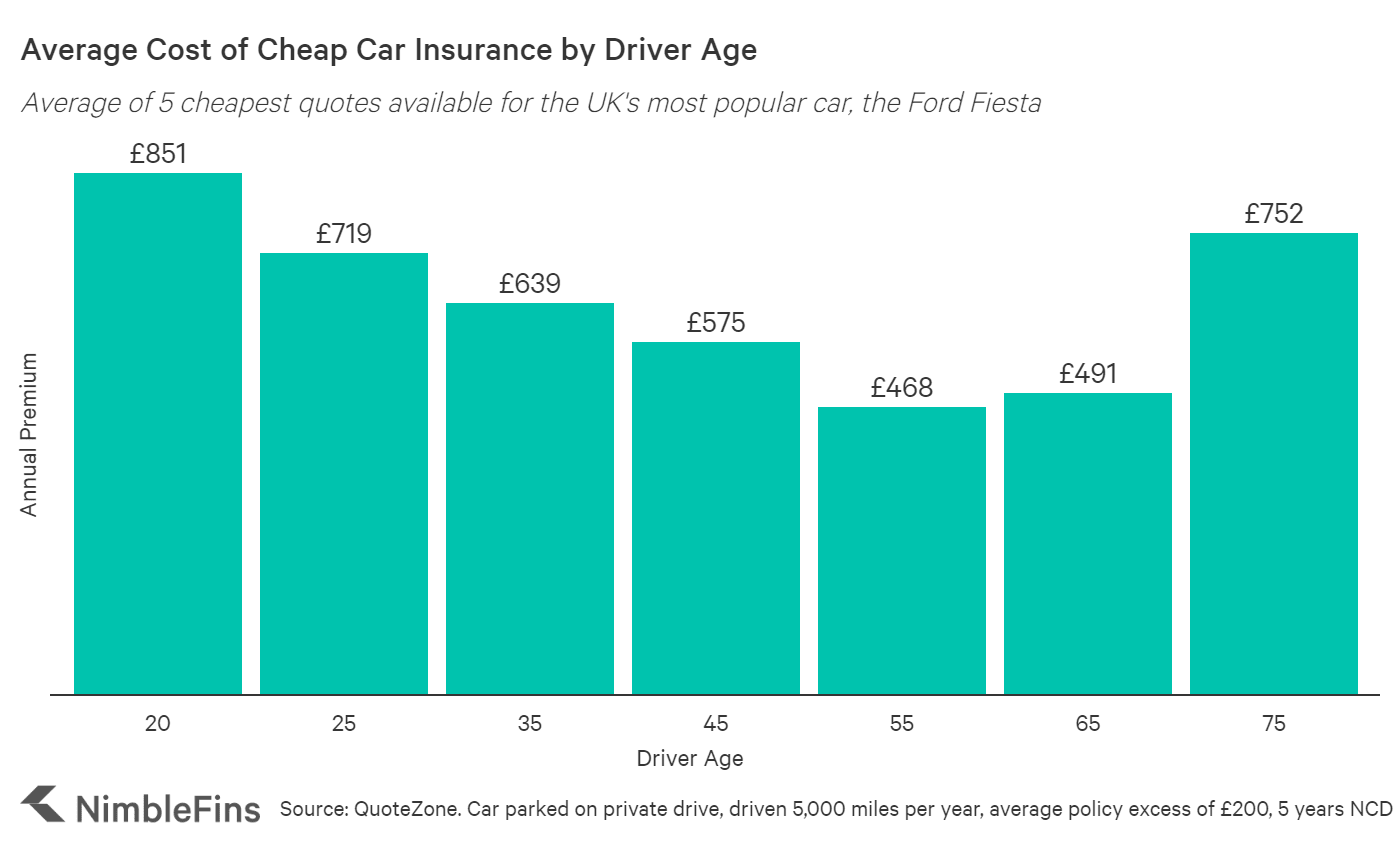

Age

Driver age factors quite heavily into your car insurance premium price. In fact, the NimbleFins data studies on the Average Cost of Car Insurance and the Average Cost of Motorcycle Insurance indicate that drivers in their 20's can pay 50% more than drivers in their 40's. Teenagers can pay double, or even more. Younger drivers (and those much older) tend to have the most accidents, file the most claims and cost the insurance companies more than other age groups—hence the high prices.

You Health

Certain medical conditions must be declared to the DVLA; and some insurers will ask about medical conditions as well. If you're asked about (and have) a medical condition that an insurer thinks could increase the risk of you being involved in an accident, then your premium could be impacted.

Gender

Our analysis of 5 top car insurers found, very surprisingly, that women garner slightly higher premiums than men—but only by a few percentage points. Your marital status may also play a role in the price of your auto cover.

Your Car

Many facts about your car will play a role in the price an insurer will quote you. Here are a few of the biggies:

- How expensive is your car? Luxury, sports and SUV vehicles which are more expensive are also more costly to repair or replace in the event of accident or theft. Cars with more premium trim levels typically cost more to insure.

- How big is your car's engine? Typically, larger engines cost more to insure.

- How old is your car? We've found that car insurance premiums tend to be highest for brand new cars, but that premiums may creep up again after cars pass a certain age (around 10 years).

- Is your car popular with thieves? Thieves increasingly target vehicles with high resale value or parts demand. According to the latest 2025/2026 theft data, the Toyota RAV4 is currently one of the most targeted vehicles in the UK (with 7.58 thefts per 1,000 cars), followed closely by the Range Rover Sport and the Toyota C-HR. Popular models like the Ford Fiesta and VW Golf also remain high on the list due to the sheer volume of them on the road.

- Is your car in a high insurance group? All vehicles are categorised into an insurance group, which range from group 1 to group 50. Cars in higher insurance groups typically cost more to insure, because they would cost more for an insurance company to repair or replace.

Occupation

You might think you drive the same regardless of your job title, but the insurers take a different view. They use historical data to determine which jobs tend to result in higher claims, and price accordingly. While it's critical to be honest on your insurance application about your job, if there are different ways to describe your job accurately, it can be worth pricing policies with these different occupations.

For instance, we recently tested Comprehensive car cover prices on a Ford Fiesta for a Manager, a Catering Manager and an Accounts Manager. The Accounts Manager came out cheapest at £925 per year, while the Catering Manager cost 14% more at £1,055 annually. The premium for a nondescript "Manager" was £974, right in the middle. Clearly, the Accounts Manager should be specific about their job to secure a lower premium whilst the Catering Manager would pay less by stating their occupation is simply "Manager."

Where you Keep your Car

Since the number of cars stolen in the UK has risen 30% over the past three years (according to RAC Insurance), you can be sure that insurance companies want to know where you keep your car—especially at night. Cars living on the street will usually cost more to insure than, say, a car stored on a private drive or in a garage. This is a detail you'll most likely be asked about during car insurance applications.

When, Why and How Much you Drive

It may surprise you but insurers care when and why you're behind the wheel. If you regularly drive for business purposes, you'll probably pay higher insurance rates than if you just use your car for social purposes. The same is true if you tend to drive during peak hours, as accidents are statistically more likely when there are more cars on the road.

Also, those driving more miles each year tend to pay more—this makes some sense, as the more you're on the road, the more likely you are to be involved in an accident. Be careful to be honest about your expected annual mileage when you sign up for auto insurance, however, as you don't want an insurer to say a claim isn't valid because you mislead them on your application by understating your annual mileage.

When You Buy Your Car Insurance Policy

You may not realize it, but when you buy your car insurance can have a massive impact on the price you'll pay. In fact, our study of how the timing of your car insurance purchase affects price found a 50% reduction in car insurance rate if you buy 3 weeks in advance of the coverage start date, versus buying a plan that starts today.

Parting Thoughts

As you can tell by now, there are so many factors that go into determining your car insurance premium that prices can vary drastically from person to person, and there may be extenuating factors. For example, someone insuring an accident damaged car may need to pay more. What is best or cheapest for one person will not be best or cheapest for the next.

But understanding what is important to the insurers can help you get a handle on why you're seeing car insurance prices in a certain range, know how you can reduce your premiums (e.g., via a NCD) or even help you recognize a good deal. For information on finding the best insurance company for your needs, see our article on best, cheap car insurance companies.