Aviva Landlord Insurance Review: The Provider For You?

Aviva Landlord Insurance Review: The Provider For You?

Good for

- Great customer ratings

- Seamless claims process

- Quick call out times

- Unlimited buildings and contents sum

Bad for

- Online chat feature can be unhelpful

- Customer service is inconsistent

- Rent guarantee and malicious damage by tenants not offered

As seen on

Aviva is one of the largest and oldest insurance companies operating in the UK, so you may be wondering: just how good is their landlord insurance?

Well, according to Moody’s credit rating agency they appear to be pretty stable with Aviva achieving a credit rating of aa3, meaning it’s considered a reliable and very capable insurance provider. Similarly, Aviva scores a whopping 4/5 in their Trustpilot ratings indicating a ‘great’ customer experience—a very strong score indeed for an insurance company.

However, during our research into Aviva landlord insurance we found that not all ratings were quite so glowing. Fairerfinance.com compared customer ratings and found that Aviva scored only 59% for customer happiness, and 55% for customer trust (note, these are not landlord insurance specific ratings).

In this review we cover all you need to know about Aviva landlord insurance, from a discussion of features to an in-depth analysis of customer comments, so you can judge whether this really is the landlord insurance provider for you.

In This Review

- Aviva Landlord Insurance: Overall Review

- How to Claim

- Aviva Landlord insurance: discounts and savings

-

Compare Landlord Insurance

Only one form to fill out. Find the insurance you need today.

Aviva Landlord Insurance Overall Review

Acting as one of the largest insurance providers with over 15.5 million customers in the UK alone, Aviva has been providing advice and insurance for more than 320 years. These facts alone may be very appealing to any landlord looking to find a knowledgeable and dependable insurer who will protect them against the risks of the rental property game.

Indeed, independent credit rating agency Moody’s has given Aviva a rating of Aa3 for their home insurance cover, meaning they consider Aviva to be a stable and capable insurance provider. Not only that, but we think that Aviva’s landlord insurance offer is a good quality product on the market in terms of features.

Aviva also appears to be a hit amongst its own customers - Finder.com found that 78% of Aviva home insurance buyers would recommend it to a friend and customer feedback on Trustpilot gives Aviva an average rating of 4.0 out of 5 across its 28,000 reviews.

Taken together, it would seem Aviva is a top contender for landlord insurance and is a provider worthy of consideration. However, Aviva does appear to fall short of expectations in some areas.

Aviva scored only 59% for customer happiness and 55% for customer trust in a customer experience review conducted by Fairerfinance which paints Aviva in a slightly less positive light. Many customers call out difficulty in contacting customer service and even when they do, this is often met with unhelpful advice or with the call being cut off altogether.

The positives surely outweigh the negatives, and from our research it seems Aviva is certainly worth taking a look at. We know that landlord insurance can be a confusing and jargon heavy subject area, especially to any landlord that is new to the game. So, have broken down the specifics of Aviva’s landlord insurance offer for you. Let’s take a look…

Why choose Aviva Landlord insurance?

Aviva is proud of their standard landlord insurance policy offer, and it certainly includes some desirable features. Here are few key benefits we feel are particularly good for you to know:

- Online discounts: according to Aviva, 28% of their customers saved at least 20% in November 2020 (no more recent update)

- Excellent claims management team: available 24/7, 365 days a year. Aviva states that 98% of claims were paid in 2018! (again, we can't find more recent data for this stat...)

- Quick callout times: Aviva state they will send a tradesperson out to your property in 4 hours

- Insure up to 3 properties at a time

- Manage your policy easily online

- Their no-claims discount rewards especially cautious landlords

Aviva Landlord insurance reviews and ratings

Aviva Customer Ratings Trustpilot Rating 4.0 out of 5 Aviva insurance scored 4.0 out of 5 stars across over 30,000 reviews on Trustpilot, indicating a ‘great’ customer experience. However, it is important to note that this rating covers the whole of Aviva and not just its landlord insurance offer.

Let’s take a look at what Aviva’s own customers have to say about their experience...

What does Aviva Landlord insurance do well?

We reviewed hundreds of customer testimonials and generally speaking, customers praised Aviva for their excellent customer service and feeling valued. Some also highlighted that the process of making a claim is particularly smooth, essential if you need to make a claim quickly if you experience an emergency or significant damage to your property.

“No issues since taking out policy. Regular correspondence from the company with an annual overview of what is covered.”

“They are easy to talk to and customer service is good.”

“They provide a reliable service at an affordable price and always make me feel like a valued customer.”

“Claims process is really easy.”

“I have been a customer of this brand for many years, and every single customer interaction I have had with them has been without friction.”

What could Aviva Landlord insurance improve on?

Although the positive reviews overwhelmingly outweigh the negatives for Aviva landlord insurance, there are a few drawbacks highlighted by customers we would like to draw your attention to.

Some comment on the fact that compared to other landlord insurance providers, Aviva is a slightly more premium offer and may not necessarily be the best value. Others call out the fact that it can be very difficult to contact Aviva as they encourage you to make use of their online technical support, such as their chat feature, leaving some questioning whether they are actually speaking to a human advisor, or simply a robot.

This has led customers to become frustrated, especially given the importance of insurance and at times requires clear answers in a timely manner. For this reason, Aviva may not be the best option out there for less tech-savvy landlords.

“A bit expensive, online only so difficult to get through.”

“They constantly increase prices for loyal customers.”

“Commercial landlords insurance is not worth the paper it’s written on...I have paid Aviva for years. The one time I made a claim for business interruption due to tenants unable to pay rent due to Coronavirus... Aviva dismisses any claims due to the virus unless it’s specifically named in the policy.”

“If you have any queries or need help it’s almost impossible to speak to a human, even their 'chat' is a robot chat.”

“Aviva home insurance emergency call out Was NON EXISTENT. TWO calls later and NOBODY arrived or telephoned. They want to charge an excess of £450 for a claim!”

“Had so much trouble trying to buy a policy through Aviva Online. I kept ending up at a dead end on the website, they were not able to give me adequate technical support over the phone, and their live chat was unavailable.”

How much is Aviva Landlord insurance?

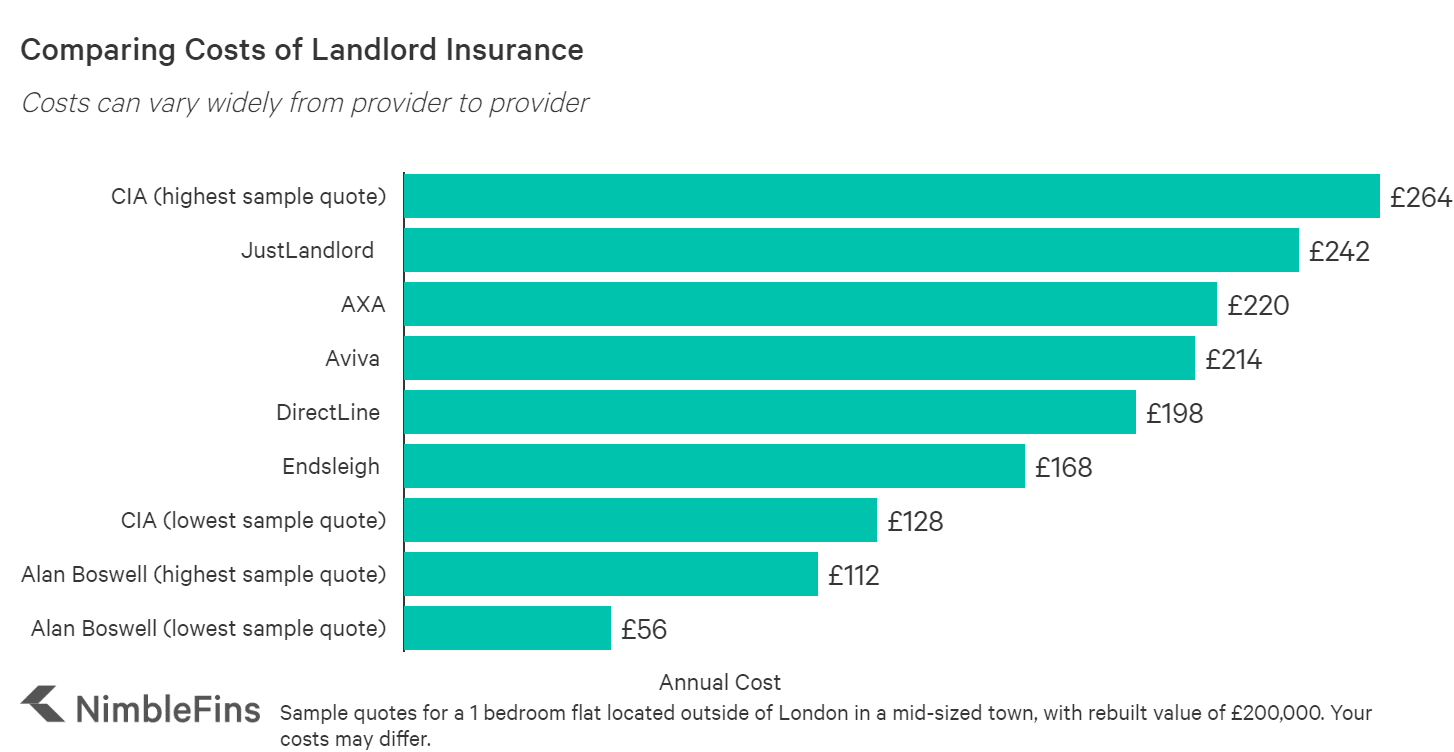

We have compiled quotes for a 1 bedroom flat located outside of London in a mid-sized town, with a rebuild value of £200,000. We found that for a no-frills policy with buildings insurance and property owners liability of £5million as standard, Aviva landlord insurance is slightly more expensive than many of its competitors. In fact, we’ve calculated the sample quote is 10% higher than the average of like-for-like quotes shown below.

Costs can really vary so it's important to check prices from multiple sources and understand what's includedLandlord insurance quote comparison for a 1 bedroom flat (£annual) CIA

£264 (highest sample quote) JustLandlord

£242 AXA

£220 Aviva

£214 DirectLine

£198 Endsleigh

£168 CIA

£128 (lowest sample quote) Alan Boswell

£112 (highest sample quote) Alan Boswell

£56 (lowest sample quote) However, Aviva do offer their buildings and contents insured for an unlimited sum if the property is unlisted, has 5 bedrooms or less and is made of brick, stone, slate and tile which may explain the price premium. This offer may be particularly attractive to landlords renting smaller flats, especially in the bigger cities!

Of course, these quotes are intended to be used as a guideline, and your quotes may be higher or lower depending on your own individual circumstances.

What is/isn’t covered by Aviva Landlord insurance?

As standard, AVIVA offers quite a competitive landlord insurance package compared to others on the market. These include:

- Buildings insurance (unlimited^): cover will protect you against damage or loss caused by a variety of events such as fire, flood, storm, water escaping from or freezing within in-home appliances, theft, subsidence and landslides

- Landlord contents (unlimited^): if any contents, such as furniture or removable appliances you provide for your tenants are damaged or lost as a result of, say, any of the above events, Aviva will cover the cost of repairing or replacing these (note: max. Single item limit of valuables up to £2,000)

- Loss of rent and cost of alternative accommodation: for example, if your property becomes uninhabitable due to any of the reasons stated above

- Replacement locks (limit of £1,000): this also includes external doors, domestic safes and alarm systems

- Landlord liability (£5m): if you own the property outright, Aviva’s landlord insurance will cover the costs if a third party makes a claim against you for suffering sickness, injury or if their property is damaged as a result of your actions or your property

^Note: unlimited sum valid if the property is unlisted, has 5 bedrooms or less and is made of brick, stone, slate and tile

Optional add-ons

As with all landlord insurance providers Aviva also provides some additional cover options that aren’t included in their policy as standard. Whilst not mandatory, these are worth considering to offer you an additional layer of protection against the risks associated with being a landlord.

- Landlord fixtures and fittings: covers accidental damage to any service pipes, cables, fixed glass, sanitary fittings (e.g. bathroom sink) as well as non-portable entertainment items you might provide to your tenants

- Accidental damage to buildings: covers accidental damage to the buildings except where this is listed as an exclusion (see exclusions section below)

- Landlord home emergency cover: in the event of an emergency (e.g. a heating breakdown) will cover the costs of labour and materials needed to fix the issue, as well as temporary accommodation for tenants if your property is made uninhabitable (both up to the value of £1,000). Note, this does not cover dual-purpose boilers, day-to day maintenance costs or the breakdown of domestic appliances (e.g. washing machine).

- Legal costs (up to £1000): Aviva will provide 24/7 access to a legal helpline if you require advice as well as covering legal fees up to £100,000 if a tenant chooses to make a claim against you. However, Aviva will not cover any claim related to the letting out of a property (i.e. between you, as the landlord, and your tenants) such as contract disputes or eviction proceedings.

Missing features

There are some features that either aren’t offered in Aviva’s standard cover or aren’t available to purchase as an add on. These features are worth knowing about as they do provide that added layer of protection if something were to happen and could save you a lot of money, so going without these could be risky.

- Landlord rent guarantee: unlike loss of rental income, landlord rent guarantee insurance will cover you if a tenant is unable to make rental payments regardless of whether your property is habitable or not (e.g. if the tenant has recently lost their job). Aviva does not offer rent guarantee in their landlord insurance offer, so ensuring you have a stable source of income from your rental payments is incredibly important, so think carefully about whether you would be comfortable proceeding without this security.

- Malicious damage and theft by tenants: whilst Aviva’s standard landlord insurance offer will cover you against malicious (i.e. intentional) damage by third parties unlawfully allowed on your property, Aviva will not cover you if your property or any contents you provide for your tenants are lost or damaged purposefully by the tenants themselves.

Exclusions: What isn’t included?

As with almost any type of insurance, landlord insurance often contains some exclusions that are good to be aware of so you don’t get caught out. Aviva is no different, and we’ve outlined a few key ones we’ve found below. Note, the full list is much longer, so make sure to read up on the exclusions to avoid getting caught out.

- Any damage or events that you were aware of before the policy start date: a common exclusion that is often missed, so make sure you triple check when your cover officially starts!

- Breakdowns and faults: Aviva’s landlord insurance will not cover you in the events, say, the boiler in your property breaks down

- Damage resulting from faulty materials or poor workmanship this is quite self-explanatory, but Aviva will not pay out if you try to claim for damage that has occurring due to e.g. poor building materials or a poor quality installation

- War and terrorism: If your property is damaged as a result of events associated with these (e.g. if, rather unfortunately, your property suffers damage from a nuclear attack) you will not be covered

- Any gradually occurring damage i.e. natural wear and tear or damage that would be expected as a result of aging

- Damage caused by frost, damp, dry-rot

- Damage to fences, gates and hedges due to storm or fallen trees

Another key point to remember as a landlord of a rented property is that if your property is unoccupied for longer than the period of time outlined in your policy, any damage or losses that occur within this time will often not be covered by your insurer, and Aviva landlord insurance is no different in this respect. So always read your policy wording carefully and know your rights!

How does Aviva Landlord Insurance Compare to Competitors?

To better understand the value of Aviva Landlord insurance you need to look at it in the context of other available options. We compared it to other plans in the market so you can see which may be more suitable for you.

Aviva Landlord Insurance vs Direct Line Landlord Insurance

Direct Line is one of the UK’s largest and most reputable insurers, earning 5 stars for features, making them one of the best landlord insurance products on the market. With over 250,000 existing landlord insurance policy holders it is certainly a popular choice and has won multiple awards to boot. Its comprehensive cover includes buildings, contents and landlord liability included as standard.

However, just like Aviva Direct Line offer a range of optional add-ons such as malicious damage by tenants, loss of rental income and legal expenses meaning you can curate the right policy for your needs. Direct Line also offer some discounts for new and existing landlords, such as a 10% multi-property discount if you’re looking to insure 15+ properties!

Bottom Line: If you’re looking for award-winning coverage from a reputable insurer then Direct Line may be another option to consider — their extensive range of policy add-ons also gives you the freedom to tailor your policy to suit your specific needs.

Aviva Landlord Insurance vs AXA Landlord Insurance

With top-notch landlord insurance features and an ‘excellent’ customer experience rating of 4.3 out of 5 according to Trustpilot, AXA is certainly a firm favourite amongst experts and consumers alike. And for good reason; this multiple-award winning provider goes the extra mile, offering a 24 hour glass-replacement service, inflation protection and free access to a 24 hour emergency helpline for emergencies and legal advice.

Whilst we found AXA to be a slightly more premium option than Aviva, they do make up for this by offering an exceptional level of standard cover which includes accidental damage and malicious damage by tenants — something that Aviva offer only as an add-on. With a range of discounts for both new and existing customers, it is certainly worth considering spending that little bit extra for a comprehensive level of protection.

Bottom line: AXA could be an ideal choice for landlords looking for a policy that covers (almost) all the bases, without the need to factor in extra costs incurred by adding on optional extras. Whilst our research found it to be slightly more pricey, AXA offer some of the most comprehensive standard landlord insurance cover on the market.

Aviva Landlord Insurance vs Alan Boswell Landlord Insurance

One of the most affordable insurers we sampled from, Alan Boswell certainly doesn’t lack in its cover. As standard, they cover many of the ‘essentials’ including buildings, contents, landlord liability, employer's liability as well as accidental damage and malicious damage by tenants!

That being said, for landlords looking for rent guarantee, legal expenses or landlord home emergency insurance — this will come at an extra cost. However, with excellent expert and customer ratings across the board and a low sample price to boot… it’s certainly worth considering.

Bottom Line: our research found Alan Boswell to offer excellent coverage at a fraction of the price, making it one of the best landlord insurance offers we have come across. For landlords looking for a value offer that is trusted by experts and customers alike, Alan Boswell may be the landlord insurance provider for you.

How to make a claim on Aviva Landlord insurance

The contact details for making a claim can be found in the Landlord documents (policy wording) that Aviva will provide you if you choose to take out landlord insurance.

- Aviva Landlord insurance phone number: 0345 030 6945

- Online: aviva.co.uk/make-a-claim

Before you decide to make a claim, we recommend that you read your policy wording carefully to ensure that you are indeed covered. If you are, Aviva may ask you to provide certain details and documentation such as your policy number, photographic evidence of your loss or damage, receipts and invoices so it’s always a good idea to have these handy, or be prepared to acquire these if necessary.

Aviva Landlord insurance: Discounts and savings

It’s well worth being aware of tips and tricks at your disposal that will help you to save a little bit on Aviva’s landlord insurance.

- Aviva does offer a 10% discount on landlord insurance for existing customers

- Aviva also state that customers can often get a discount when shopping online, stating that 28% of their customers saved at least 20% in November 2020

FAQ’s

Yes and no.

If you cancel within the 14-day cooling off period after receiving your policy, you will receive a full refund if your cover hasn’t yet started. If it has started and there have been no claims thus far, Aviva will refund you the amount proportional to the time left on your policy (note: where a claim has been notified or paid, you will not be eligible for refund and the payment will still be due).

If you choose to cancel after this 14-day cooling off period you can, but this will incur a fee of £29 (plus any Insurance Premium Tax if applicable).

If you’re looking for Aviva Landlord insurance promotional codes or special offers, they do occasionally pop up throughout the year. They’re usually advertised on the Aviva website, so keep your eyes peeled for when they do pop-up. You may find them on a few ‘discount code’ websites, but these quickly expire, so don’t be surprised if the code is rejected when you enter it.

If you opt for Aviva's standard Landlord insurance package (i.e. with no add ons) you will not be covered if the boiler breaks downs in one of your rental properties. However, Aviva does offer landlord home emergency insurance, which is available to purchase alongside their main policy. Home emergency insurance specifically covers events like boiler breakdowns (note: some exclusions do apply!), so it's worth looking in to.

'Accidental damage' can cover you in the event of one-off accidents to your properties building or contents. Examples where accidental damage cover would apply include things like if your tenant accidentally spills red wine on the carpet leaving a stain, or if a leaky roof causes internal water damage.

Aviva offers accidental damage cover as an optional add when you purchase landlord insurance with them. You can choose between two different levels of coverage ('extra' and 'limited') depending on your needs, so if this is of interest to you then it's well worth considering.

Aviva's standard landlord insurance will cover you against certain incidents (e.g. theft) if your property is vacant, but only if the vacant period is less than that outlined in your policy. If your property is vacant for longer than this period of time you must notify Aviva immediately, and you will typically find you are not covered for certain damages that occur after this period.

Yes, during our research we found that Aviva is featured on many popular comparison sites, such as Simply Business and GoCompare. Comparing quotes is one of the best ways to save money on landlord insurance!

No, it doesn't. Aviva will not pay out on any claims for damage as a result of wear, tear or gradual deterioration.

Aviva allows you to insure up to 3 properties at a time. Any more than this however and Aviva will sadly not be able to accommodate you, so you would be better off opting for an insurance provider that specializes in multiple property cover.

Unfortunately, standard homeowners insurance isn't equipped to cover the additional risks that landlords face when renting out properties to others such as rent guarantee, legal expenses and liability to name just a few! Don't be caught out by assuming homeowners insurance is enough and always invest in specialist landlord insurance to ensure you are protected.