Are notice savings accounts worth it?

If you're looking for a home for your savings you may think you’ve a binary choice between fixed or easy-access.

However, notice savings accounts provide savers with a third option and can be considered a sort of hybrid between the two. While you can access your cash in a notice account, you must notify your savings provider in advance.

Let’s take a closer look at how notice accounts work, and whether it’s worth stashing your cash into one.

How does a notice savings account work?

Interest rates on notice savings accounts are usually variable which means they can change at any time. Despite this, rates are usually quite generous, and the top notice accounts often beat easy-access deals.

You’re allowed to deposit funds into a notice account as often as you like, so they’re similar to easy-access accounts in this regard.

Importantly, you can access your cash when you save in a notice account. The catch is that you must give prior notice before making a withdrawal. Notice periods typically range from 30 to 180 days. Accounts with the longest notice periods usually pay the highest rates of interest.

Notice savings accounts have become more popular in recent years. However, they’re still far less common than easy-access or fixed accounts. Notice accounts remain a rarity among big-name providers. Despite this, a number of challenger banks have carved out a reputation for offering competitive notice accounts. Secure Trust Bank and OakNorth Bank are two providers that regularly feature in the notice account best-buy tables.

Can the interest rate change on a notice savings account?

Similar to easy-access, interest rates on notice savings accounts are usually variable. This means they can change after you open an account. However, if you have funds in a notice account you shouldn't overly worry about the rate changing in future. That’s because if your savings provider decides to chop its rate it must also notify you in advance.

This notifice period should at least be as long as withdrawal notice period on the account. For example, if you have savings in a 90-day notice account and your provider wishes to reduce the interest rate, you can expect at least 90 days’ notice before any change takes place. This rule means that you should have enough time to move your money to another account before you lose out.

Is it worth saving in a notice account?

A notice a savings account can be a good option if you’re looking to boost the interest rate on your cash, but you don’t wish to lock away cash for a long period of time. Remember, market-leading notice savings accounts usually beat rates offered on easy-access accounts.

It’s worth knowing that notice accounts can be decent if you value flexibility when it comes to accessing your savings. For example, if you’ve a big event planned, such as a wedding or a house purchase, you’ll probably want to access your savings a few months down the line, but not immediately. Therefore, stashing your cash into a notice account with a short notice period might be a good option. That’s because you’ll have access to your cash when you need it and, in the meantime, you’ll be able to boost the interest rate on your cash.

Ultimately, the question of whether you should opt for a notice account will depend on your personal circumstances, and how much you value being able to access your cash with relative ease.

Note: If you definitely won't need access to your savings within a year or so, you may wish to opt for a fixed savings account. Fixed accounts usually trump both easy-access and notice accounts when it comes to interest rates. A fixed account may also be for you if you crave the certainty of a guaranteed interest rate. Remember, interest rates on fixed savings accounts do not change. In contrast, interest rates on easy-access and notice savings accounts are variable.

How do interest rates on notice savings accounts compare to easy-access or fixed offerings?

When it comes to interest rates, fixed rate savings accounts often come out on top. As a rule of thumb, the longer the fixed term, the higher the interest rate you can expect to earn.

However, in the current February 2026 market, we are seeing a 'flat' or 'inverted' curve: the best six-month fixed rates (currently around 4.15% from Al Rayan) actually outperform many one-year fixed rates (averaging 4.12%). Furthermore, the best notice accounts (paying up to 4.5% AER) are currently beating both six-month and one-year fixed products, providing a higher yield for those who can plan their withdrawals in advance.

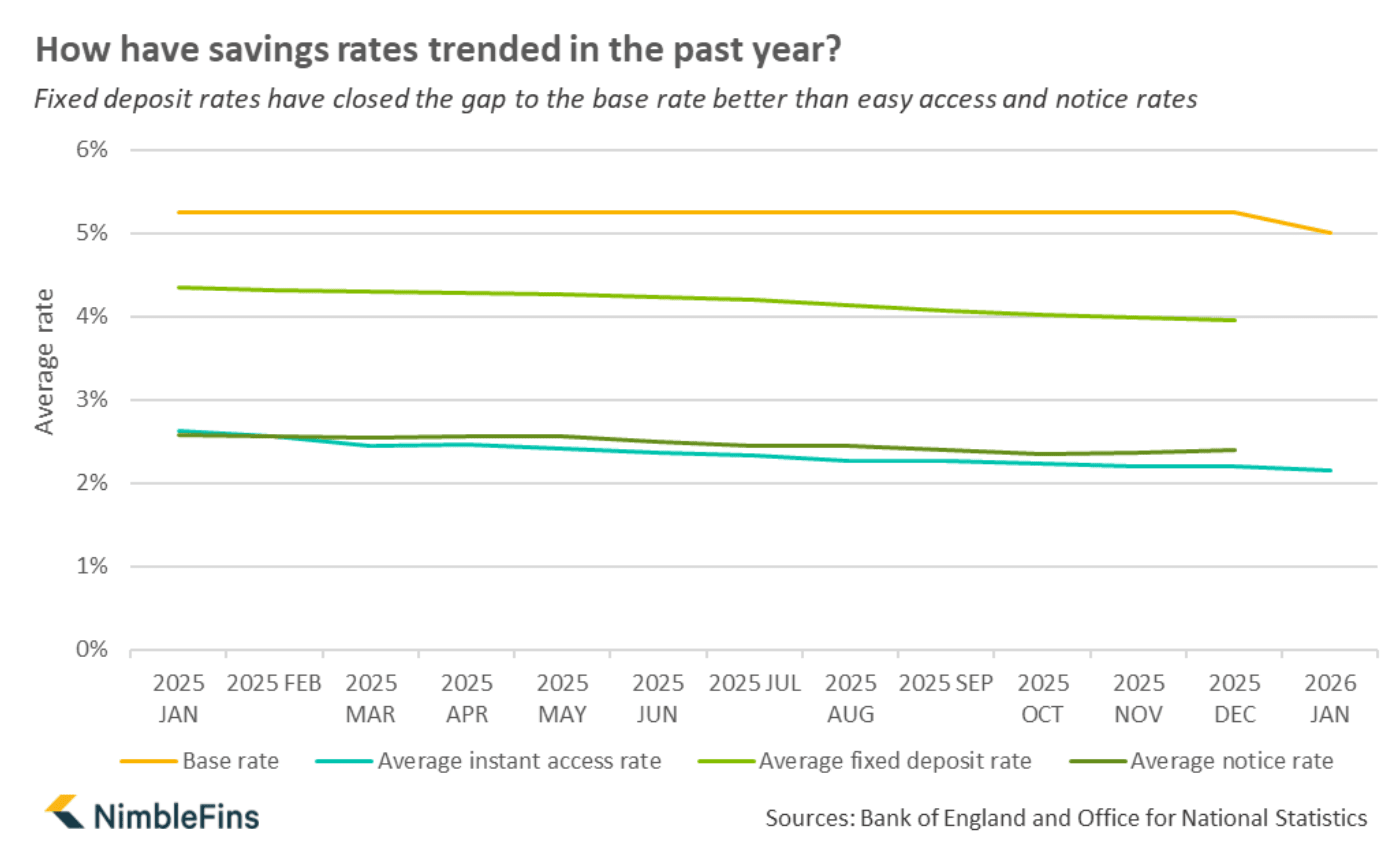

The chart below shows how average notice savings rates are nearly spot on easy access rates:

As you can see, in early 2026, notice rates continue to be just a touch higher than easy access rates, on average, but there's not much in it.

As notice accounts are essentially a hybrid between fixed and easy-access, interest rates on notice accounts have historically sat in the middle. To put it another way, a market-leading notice account should be likely to pay a higher interest rate than an easy-access alternative. And historically, notice accounts were likely to pay less than the top one-year fixed account.

Keep in mind that interest rates on savings accounts can change often. So, to ensure you bag yourself the highest rate possible, it's worth comparing rates from of all types of savings account before you open one.

To keep on top of the market-leading savings rates, take a look at our best savings accounts guide.