Secured vs unsecured personal loans: what's the difference?

If you need to borrow a significant sum, one of the first decisions you'll face is whether to take out a secured or an unsecured loan. The difference between the two goes beyond the interest rate—it affects how much you can borrow, how long you have to repay, and critically, what is at risk if you fall behind on payments.

This guide explains how each type of loan works, the key trade-offs involved, and the questions worth asking before you apply.

Your home may be repossessed if you do not keep up repayments on your mortgage or any other debt secured on it. Always make sure you can afford repayments before borrowing.

NimbleFins is a credit broker, not a lender.

What are secured and unsecured personal loans?

Personal loans fall into two broad categories. The key distinction is whether the loan is tied to an asset you own.

What is a secured personal loan?

A secured personal loan requires you to offer an asset—most commonly your home—as collateral. This gives the lender a legal charge over that asset. If you stop making repayments, the lender has the right to repossess the property to recover the outstanding debt.

Because the lender's risk is lower, secured loans typically come with lower interest rates and higher borrowing limits than unsecured alternatives. However, the risk to you is substantially greater. MoneyHelper, the government-backed guidance service, recommends exploring all other borrowing options before securing a loan against your home.

What is an unsecured personal loan?

An unsecured personal loan does not require any collateral. The lender makes a decision based on your credit history, income, and overall ability to repay. MoneyHelper describes unsecured loans as the most common form of personal borrowing in the UK, typically used for amounts between £1,000 and £25,000, with repayment terms usually running from one to five years.

If you miss payments on an unsecured loan, the consequences are serious—your credit score will be damaged and the lender can take legal action to recover the debt—but your home is not directly at risk in the way it would be with a secured loan.

Key differences between secured and unsecured loans

Collateral and risk

The most important difference is what you stand to lose. Secured loans put your home or other assets at risk. If you cannot maintain repayments, the lender can ultimately seek a court order to repossess that asset.

Unsecured loans carry no direct asset risk. In a worst-case scenario, you face damaged credit and potential court action, but not the loss of your home.

Loan amounts and repayment terms

| Feature | Secured loans | Unsecured loans |

|---|---|---|

| Typical amount | £3,000 to £250,000+ | £1,000 to £25,000 |

| Repayment period | 3 to 25 years | 1 to 7 years |

| Rate type | Often variable | Usually fixed |

Secured loans are generally suited to larger borrowing amounts. Unsecured loans are more appropriate for shorter-term needs up to £25,000, according to guidance from MoneyHelper.

Interest rates

Secured loans generally carry lower interest rates, because the lender's risk is reduced by the collateral you provide. Unsecured loans tend to cost more in interest, particularly if your credit score is not strong or the amount you want to borrow falls outside the range lenders compete hardest on.

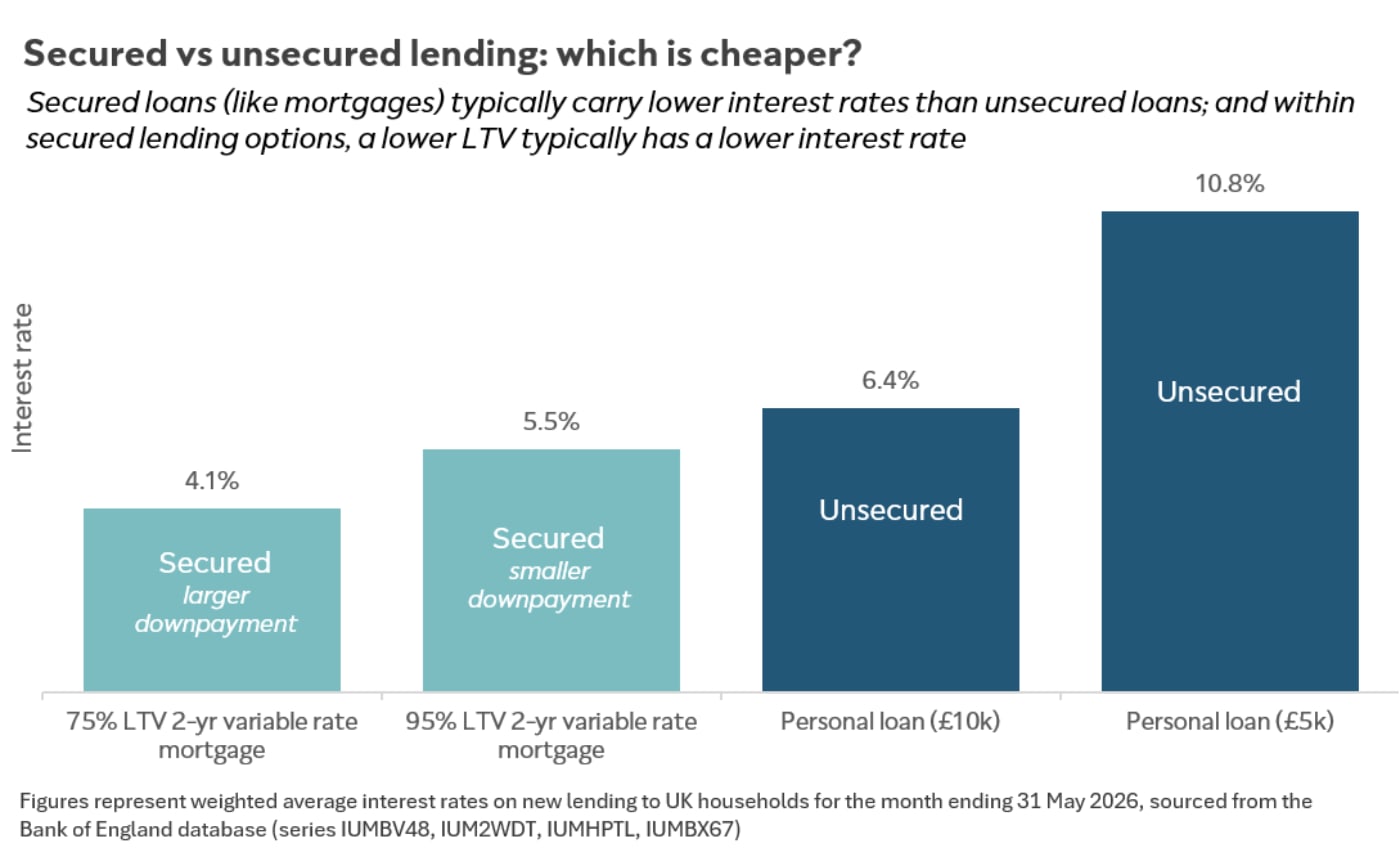

Bank of England data illustrates this clearly. As of May 2026, the average rate on a 75% LTV variable rate mortgage (a secured loan) sat at just 4.1%, rising to 5.5% for a 95% LTV equivalent, where the lender carries more risk due to the smaller deposit. By contrast, the average rate on £10,000 unsecured personal loans was 6.4%, and £5,000 unsecured personal loans averaged 10.8%. The pattern reflects both the secured/unsecured divide and the risk profile of borrowers (because smaller unsecured loans attract a wider, more credit-diverse pool of applicants, pushing average rates higher).

| Secured vs. unsecured loans | Average interest rates |

|---|---|

| 75% LTV 2-yr variable rate mortgage | 4.1% |

| 95% LTV 2-yr variable rate mortgage | 5.5% |

| Personal loan (£10k) | 6.4% |

| Personal loan (£5k) | 10.8% |

Source: Bank of England 31 May 2026

It is worth noting that the lower rate on a secured loan may not result in lower total cost if the loan is spread over a much longer term, or if arrangement and legal fees are added to the balance.

Approval and eligibility

| Aspect | Secured loans | Unsecured loans |

|---|---|---|

| Credit requirements | More flexible | Typically strict |

| Poor credit | May be considered (subject to affordability) | Often declined or higher rate |

| Approval time | Several weeks (valuation required) | Days to a few weeks |

| Documentation | Property valuation and legal checks required | Income and identity verification |

Eligibility for any loan is determined by the lender based on your individual circumstances. Approval is not guaranteed, and the rate advertised may not be the rate you are offered.

Pros and cons of secured loans

Advantages

- Lower interest rates: Collateral reduces the lender's risk, which can translate into a lower APR compared to unsecured options.

- Higher borrowing limits: Secured loans can allow borrowing well above the £25,000 ceiling common with unsecured products.

- Longer repayment terms: Spreading repayments over a longer period reduces monthly payment pressure, though it increases the total interest paid.

- May be accessible with poor credit: Some lenders will consider applicants who may not qualify for unsecured lending, subject to affordability checks.

Risks and disadvantages

- Repossession risk: If you stop making payments, the lender can apply to repossess your home or other secured asset. This is a serious, real risk.

- Longer approval process: Property valuations and legal checks mean approval can take several weeks.

- Variable rates: Many secured loans use variable rates. If the rate rises, your monthly payments will increase.

- Additional costs: Arrangement fees, valuation costs, broker fees, and legal expenses can add significantly to the total cost of borrowing.

- Equity reduction: Taking a loan secured on your home reduces the equity you hold in the property, which may limit your options in future.

Your home may be repossessed if you do not keep up repayments on your mortgage or any loan secured on it.

Pros and cons of unsecured loans

Advantages

- No asset risk: Your home and other assets are not used as security. Missing payments will damage your credit and may lead to legal action, but your property is not directly at stake.

- Faster approval: No property valuation is needed. Applications can often be processed within a few days.

- Fixed rates: Most unsecured loans offer a fixed interest rate, so your monthly repayments stay the same throughout the term.

- Early repayment may be possible: Some lenders allow you to repay early. However, early repayment charges may apply—check the terms before agreeing.

Disadvantages

- Higher interest rates: Without collateral, lenders charge more to compensate for the increased risk.

- Lower borrowing limits: The typical maximum of £25,000 may not be sufficient for substantial projects.

- Shorter repayment terms: A maximum term of five to seven years means higher monthly repayments compared to longer secured loan terms.

- Strict eligibility: A good credit history is generally required. Applicants with a poor credit profile may be declined or offered a significantly higher rate.

Secured vs unsecured loans: side-by-side comparison

| Factor | Secured loans | Unsecured loans |

|---|---|---|

| Collateral required | Yes (typically your home) | None |

| Typical amount | £3,000 to £250,000+ | £1,000 to £25,000 |

| Repayment period | 3 to 25 years | 1 to 7 years |

| Interest rates | Typically lower | Typically higher |

| Credit requirements | More flexible | Strict |

| Approval speed | Several weeks | Days to a few weeks |

| Asset risk | High (repossession possible) | None |

| Rate type | Often variable | Usually fixed |

| Early repayment | Varies by lender | Often allowed (charges may apply) |

Things to consider when choosing between the two

How much do you need to borrow?

If you need more than £25,000, a secured loan may be your only realistic option, as most unsecured personal loans are capped at this level. For smaller amounts, unsecured borrowing avoids putting your home at risk.

What is the purpose of the loan?

The reason you are borrowing can affect whether a secured loan is appropriate. Using a loan for home improvements means you are investing in the same property you are borrowing against. Using a secured loan for a holiday or to consolidate unsecured debt means converting lower-risk borrowing into higher-risk borrowing secured on your home—this requires careful thought.

Think carefully before securing other debts against your home

What is your credit history?

Your credit history is central to what you can access and at what cost. Borrowers with strong credit may find competitive unsecured rates available to them, avoiding the need to use their home as security. Those with a damaged credit history may find secured lending is one of the few options open to them, though eligibility and affordability will still be assessed by the lender.

Checking your credit report before applying—using a free service such as those offered by the main credit reference agencies—can help you understand what lenders are likely to see.

Can you afford the repayments long-term?

Consider not just whether you can afford repayments now, but whether you would still be able to manage them if your circumstances changed—for example, if your income fell or interest rates rose. Variable-rate secured loans carry particular risk in a rising rate environment.

The FCA requires lenders to carry out affordability checks, but it is worth doing your own careful calculation first.

Always make sure you can afford repayments before taking out any loan. If you are unsure, seek independent financial advice from a qualified adviser. Free guidance is available from MoneyHelper at moneyhelper.org.uk.

How to apply for a personal loan

Check your credit report

Before applying, review your credit file through one of the main UK credit reference agencies. Errors on your file can affect the rate you are offered or lead to an unnecessary decline. You can access your statutory credit report for free under UK law.

Use a soft search eligibility checker where possible

Many lenders offer an eligibility check that uses a soft credit search, which does not appear to other lenders or affect your credit score. This helps you understand your likelihood of approval before making a formal application.

Gather your documentation

Both loan types will require proof of identity and income. Secured loans will also need property valuation and legal checks, which take longer to arrange.

Compare lenders carefully

The interest rate is not the only thing to compare. Look at the total amount repayable, any arrangement fees, whether the rate is fixed or variable, and the terms around early repayment. The representative APR shown in advertisements is only available to at least 51% of successful applicants—the rate you are offered may be higher.

Common mistakes to avoid

- Borrowing more than you need: Interest is calculated on the amount borrowed. Only take what you genuinely need.

- Underestimating the risk of secured borrowing: Repossession is a real outcome for borrowers who default on a secured loan. Do not treat this risk lightly.

- Focusing only on the monthly payment: A longer term reduces monthly payments but increases total interest paid. Compare the full cost of borrowing, not just the monthly figure.

- Not reading the full terms: Variable rates can increase. Early repayment charges can be substantial. Make sure you understand exactly what you are agreeing to.

- Applying to multiple lenders at once: Multiple hard credit searches in a short period can affect your credit score. Use soft search tools first.

Summary

Secured and unsecured personal loans serve different borrowing needs. Secured loans can provide access to larger sums at lower rates, but they come with serious risk to your home or other assets. Unsecured loans cost more in interest but keep your property safe.

The right approach depends on how much you need, your credit history, your ability to sustain repayments, and how comfortable you are with the risks involved. Before committing to either type of loan, it is worth comparing the full cost of borrowing across multiple lenders and, if you are unsure, seeking independent financial advice.

Free, impartial guidance on personal loans and debt is available from MoneyHelper and Citizens Advice.

Your home may be repossessed if you do not keep up repayments on your mortgage or any loan secured on it. Always make sure you can afford repayments. NimbleFins is a credit broker, not a lender. Nothing in this article constitutes personal financial advice. If you are unsure which borrowing option is right for your circumstances, consult a qualified independent financial adviser.