What is Landlord Home Emergency Insurance?

Often offered as an additional extra to standard landlord insurance polices, landlord home emergency cover offers an added layer of protection in case the unexpected happens.

Specially, in the case of an emergency (e.g. a water pipe bursts), landlord home emergency cover can help you recoup the costs of repairing the damage, for example, buy covering the costs of calling out a contractor out of hours to look at the issue. You will also find that many landlord home emergency policies provide access to a 24/7 helpline, so you get the advice and support when you need it most.

But do you really need landlord home emergency coverage? And if you do decide to opt for it, what is and isn’t included and importantly, how much is this going to cost you? Let’s take a look at the specifics of landlord home emergency cover so you can see for yourself if it’s a worthwhile investment.

What counts as an 'emergency'?

This is a good question, and the answer varies between insurance providers. Broadly speaking, most insurers deem an emergency to fulfill one or more of the following criteria:

- Causes permanent damage to your property

- Makes your property uninhabitable

- Put the health and safety of your tenants at risk

- Fundamentally makes your property unsafe

A good example of something that would be classed as an emergency is the complete failure of your heating system. However,if a pipe was found to be leaking slightly under the kitchen sink in your rental property this would not fulfill the necessary criteria to be deemed an emergency and would therefore not be covered under your home emergency insurance policy! Actually, these types of non-emergency repair and maintenance issues won't be covered by any type of insurance or service plan, and as the landlord you must pay for a handyman yourself to fix them.

So, what other kinds of events are covered in a typical landlord home emergency insurance policy or service plan? Let's take a look...

What does Landlord Home Emergency Insurance cover?

It is important to remember that what is covered by a landlord home emergency plan will vary depending on the provider. Generally speaking, however, you will find that a good policy will cover events such as:

- Failure or breakdown of your main heating and plumbing systems

- Failure or breakdown of domestic utility systems such as electricity and gas

- Blocked drains and sewers

- Damage to your roof that has resulted in internal property damage

- Damage to any windows, doors or locks that comprises the security of your property

- Damage or loss of the only available set of keys to gain access

- Sudden infestation i.e. pests/vermin

You might also find many policies cover the costs of overnight accommodation for your tenants as well if your property has become uninhabitable as a result of any of the above events. This may also be covered under your landlord insurance buildings policy.

What is not covered by Landlord Home Emergency Insurance?

It is good to be aware of the types of issues that typically aren't covered by landlord home emergency plans, to avoid being caught out. Again, each policy will be different and the list of exclusions may be shorter or longer depending on your landlord insurance provider. Being familiar with your policy is crucial, and this could save you a lot of time, stress and money if you find yourself in an emergency and discover that your policy doesn’t cover what you thought it did!

As a guide, we've listed some of the most common exclusions we've found below:

- Damage or failure to boilers more than 15 years old

- Damage or failure to boilers and other utility systems that have not been routinely serviced

- Any emergency occurring whilst the property has been unoccupied for a specified period of time

- Damage or failure occurring as a result of wear and tear

- Routine maintenance and repair

- Damage or failure as a result of faulty materials, design, workmanship or improper maintenance

- Repairs already covered by your standard landlord buildings insurance and contents insurance policy.

It’s also important to be aware of the fact that most insurance providers will not cover any known damage, issues or failure of systems occurring within, say, 14 days of the policy start date. This is to avoid claims being made by landlords who are aware of an issue/problem before they take out a policy and want to be compensated to avoid paying out themselves!

Remember to read the specific details of your policy carefully so you are familiar with not only what emergencies you are protected against (because this can really vary from one policy to the next), but when this protection starts.

How much does Landlord Home Emergency Insurance cost?

Depending on your provider and whether you are purchasing landlord home emergency cover as a stand alone policy or an additional add on will affect the price you will ultimately pay.

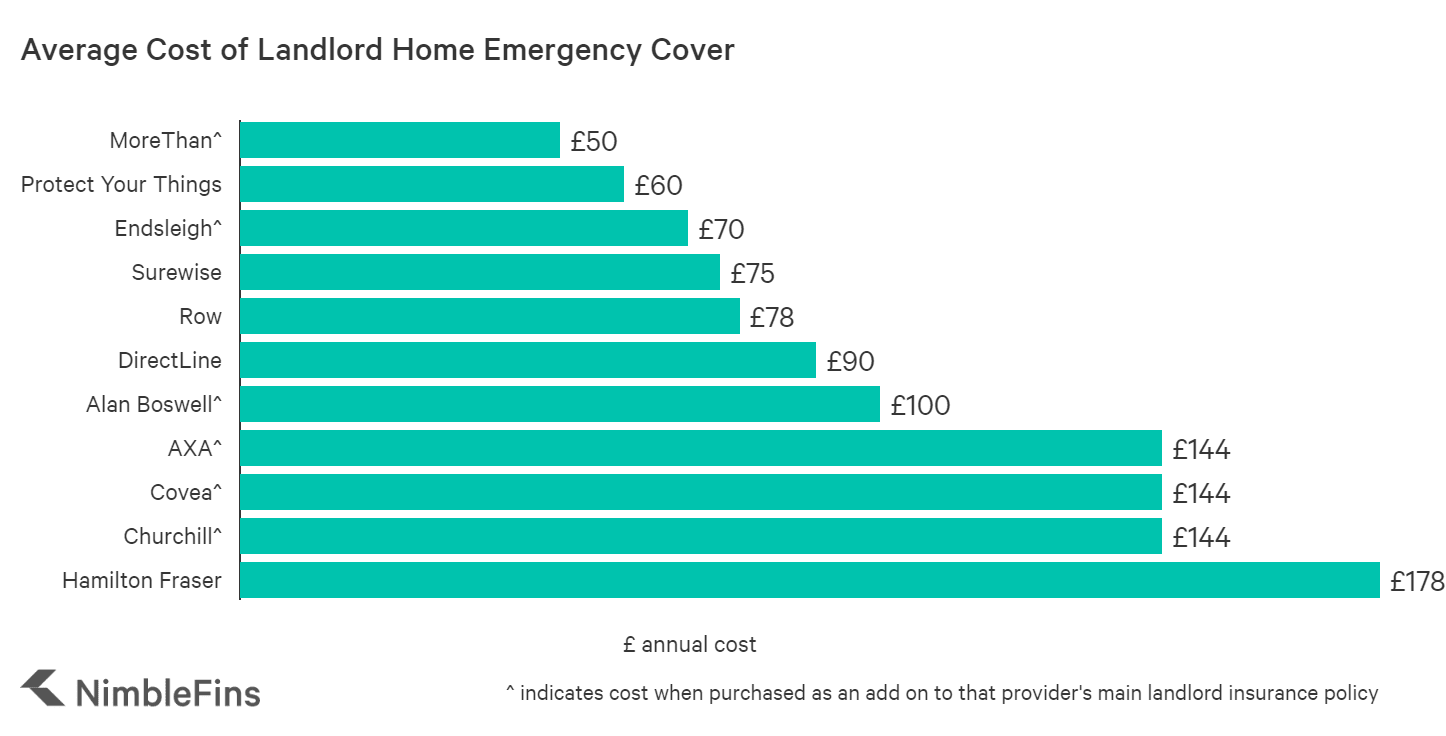

To give you an idea, we've compiled sample quotes for landlord home emergency protection for a 1 bedroom flat, located in a mid-sized town in the UK with a rebuild cost of £200,000. Some of these quotes reflect the price when purchased alongside that same providers main landlord insurance policy and some reflect the cost if purchased as a stand-alone policy.

| Average cost of Landlord home emergency insurance (£ annual) | |

|---|---|

|

MoreThan | £50^ |

|

Protect Your Things | £60 |

| £70^ | |

|

Surewise | £75 |

|

Row | £78 |

| £90 | |

| £100^ | |

| £144^ | |

|

Covea | £144^ |

|

Churchill | £144^ |

|

Hamilton Fraser | £178 |

^indicates cost when purchased as an add on to that provider's main landlord insurance policy

The cost of landlord home emergency insurance can vary widely, and you will find that you tend to get a better deal when you choose to purchase this as an addition to your standard landlord insurance policy as opposed to buying a standalone plan. From our sample quotes we have found the average cost of landlord emergency home insurance to be £103 for 12 months of cover.

It is simple and easy to compare providers online, and we always recommend taking a look at smaller companies or newcomers (e.g. 24/7 Home Rescue) as well as the bigger names on the market to ensure you get the best deal.

Of course, the cost of landlord emergency home cover depends on a variety of factors, such as the type and size of your property and any excess you opt for. For this reason your estimates may be higher or lower than those shown above. These are simply intended to be used as a guide so you can decide whether this additional level of cover is worth the investment.

You might now find yourself asking the question ‘do I really need landlord home emergency insurance?’, and that is understandable. Questioning the necessity of any additional type of insurance that is ultimately going to cost you more money in the long-run is natural, especially as you’ll already be paying for standard landlord insurance cover. Let's take a look...

Do I really need Landlord Home Emergency Insurance?

To offer some perspective on the matter, it might do well to remember what your responsibilities are as a landlord. First and foremost, you have a duty to ensure your tenants are safe. In the case of an emergency, such as burst pipe, this can be extremely distressing for both your tenants and you, and can also be potentially dangerous.

Ensuring you have a plan in place in case an emergency happens makes a lot of sense, and can take some of the immediate pressure off of both you and your tenants.

It is also worthwhile considering what the data says about home emergencies. During our research we found that the on average, the frequency of claims for home emergency insurance sits around 20%, according to the FCA. This means that 1 in 5 people claim on this type of insurance, so home emergencies are perhaps not as rare as you might think.

With the average claims pay out being £193 across 16 key home emergency providers we sampled, and the average cost of the cover itself starting at £103... it’s definitely worthwhile considering to ensure you are protected when it really matters.

Important Information

Most, if not all types of insurance are dependent on you (the policy holder) adhering to certain conditions that are specified within your documentation. As a landlord, you have a responsibility to ensure that your rental properties are safe for your tenants and the property itself is maintained to a suitable standard. This is important to keep in mind as we have already established that landlord home emergency insurance does not cover damage or failure due to wear and tear or improper maintenance.

Ensuring you are fulfilling your duties and responsibilities as a landlord is therefore crucial so as to limit your chance of falling into one of these pitfalls.

As a rule of thumb and to ensure you have the best possible chance of successfully claiming on your landlord home emergency insurance, it's important to do the following:

- Ensuring appliances and utility systems are serviced annually, or as often as recommended: this includes gas equipment, electrical and water systems—to reiterate, if you haven’t had the required maintenances performed along the way, your landlord home emergency plan might not pay up!

- Ensuring you and your tenants are aware of fire safety regulations: as a landlord, you must enforce proper fire safety e.g. keeping fire escape routes clear, providing and maintaining smoke and carbon monoxide alarms

- Take immediate or appropriate action if your tenant(s) report any issue that comprising the safety of the property: if you don't, you could face legal action

- Keep a record of all safety certificates: this is important, especially if you are asked to provide proof of regular servicing and maintenance for a claim

Not adhering to the above could comprise the success of any claim you make for landlord home emergency insurance but more importantly, the safety of your tenants! You can check out what responsibilities you have as a landlord here, as well as information on your safety and maintenance requirements.