LV= Landlord Insurance Review: The Insurance You've Been Looking For?

LV= Landlord Insurance Review: The Insurance You've Been Looking For?

Good for

- Good features

- Discounts for new and existing customers

- Excellent customer feedback

- Cheaper than many of its rivals

Bad for

- Rent guarantee and home emergency cover not offered

- Cancellation fees

Compare Landlord Insurance

Only one form to fill out. Find the insurance you need today.

With over 7 million customers LV= is one of the UK's leading insurance companies, offering a range of comprehensive policies covering car insurance, pet, travel and home insurance to name but a few.

LV= have been in business for a while — over 170 years in fact! — so naturally it has earned itself an impressive set of accolades and a reputation for being both popular and reliable amongst its customers. LV= has been recognized by Which? as a recommended provider for its car insurance and home insurance cover, and has earned itself an impressive 4.5 out of 5 on Trustpilot, indicating an 'excellent' customer experience.

But how does LV= fair when it comes to their landlord insurance offer? In this review we'll take an in-depth look at just how well LV= compares to it's big name rivals to give you all the information you need to decide whether LV= is the right choice for you.

In This Review

- LV= Landlord Insurance: Overall Review

- How to Claim

- LV= Landlord insurance: discounts and savings

- FAQ’s

As seen on

LV= Landlord Insurance Overall Review

LV= have positioned themselves as a leading provider of insurance, with over 7 million customers in the UK they certainly don't appear to be lacking in popularity. Indeed, LV= were named the UK's No.1 insurer for customer service according to a survey conducted by UKCSI (granted, this was a few years ago, back in 2020...), this alone could be enough to instill confidence in landlords looking for a good insurance policy!

Time and time again LV= have been recognized not only for their customer service but also their policy features. Which? has recognized them as a recommended provider of both car and home insurance and they've receive a host of other 5 star ratings and awards for their home insurance, travel insurance and pet insurance. This means they have been recognized as providing some of the best and most comprehensive products on the market!

Given LV='s glowing track record you might expect them to provide one of the best landlord insurance options, too. Well, when we take a look at their landlord insurance specifically we are still met with good news—their policy features are not the absolute best you can find, but they are above average compared to the rest of the market.

During our research we failed to find other landlord insurance specific product and customer ratings for LV=, which makes it slightly more difficult to make easy comparisons to its rivals. Nevertheless, LV= as a whole appears to be highly regarded amongst its customers, having earned an almost perfect Trustpilot rating of 4.5 out of 5 which indicates an 'excellent' customer experience.

Whilst this may not represent their landlord insurance offer specifically, it does suggest that LV= are doing something right. In fact, across the 83971 customer reviews that have been left (at time of writing), 97% have given a rating of 3 stars of more! Even more impressively, 80% of these customers have awarded LV= a perfect 5 out of 5!

So, it would appear that LV= is certainly worthy of consideration and remains popular for both experts and customers. However, in order to understand how their landlord insurance compares to its competitors we need to take a closer look at what is and isn't included, what the customers themselves have to say and importantly, how much this is all going to cost you.

Let's first take a look at why you should be considering LV= if you are a landlord in need of insurance...

Why choose LV= Landlord insurance?

LV=’s standard landlord insurance offer is certainly impressive, and there are some nice benefits that would appeal to any landlord looking for a value offer. Here's a few we feel are particularly noteworthy:

- Multi-award winning provider: LV= has cemented itself as one of the UK's most trusted insurance providers, winning multiple awards in the process. For example, they were named the UK's No.1 insurer for customer service according to a survey conducted by UKCSI (however this was a few years ago).

- Incentives and discounts: LV= provides some nice incentives that can save you some money on your policy, for example, they are currently offering^ new customers a 5% discount when they purchase landlord insurance online (excluding landlord legal).

- Excellent customer feedback: LV= are consistently praised by their customers for their service and product features; they have been rated 4.5 out of 5 on Trustpilot across over 82,000 reviews, indicating an 'excellent' customer experience.

^ Note, this discount is correct at the time of writing December 2025.

LV= Landlord insurance reviews and ratings

|

LV= Customer Ratings | |

|---|---|

|

Trustpilot Rating | 4.5 out of 5 |

|

Feefo Rating | 4.6 out of 5^ |

^Note: Feefo rating has been adjusted to 5 star scale; reflects an actual rating of 9.2 out of 10

As you can see, overall (i.e. not landlord insurance specifically) LV= performs very strongly across the board.

With an 'excellent' 4.5 rating across 63,000+ reviews on Trustpilot, it's not only the experts that recognize the quality that LV= has to offer.

Taken together, LV= appears to be both a popular and reliable insurance provider with it's landlord insurance regarded as offering a more comprehensive level of coverage compared to some of its rivals, for example HomeProtect and CIA.

Let's take a look at what some of their verified landlord insurance customers have to say...

What does LV= Landlord insurance do well?

We reviewed feedback left by hundreds of customers and noticed many commented on the accessibility of LV='s online portal, stating it is easy to use and hassle-free as all their insurance documents can be found in one place. New and existing customers were also pleased with the discounts available to them, with many combining their policies into a package deal — this alone speaks volumes as it suggests existing customers were more than happy with the service they have received so far!

Along with their knowledgeable customer advisors and competitive prices, LV= has also earned praise for its more specialist cover not offered by many of its rivals, for example properties that have experienced subsidence in the past.

"I’m with LV for everything. Own house, Landlord Ins and 2 vehicles."

“Simplicity of LV= account is a winner for me. User account, several policies linked in one account, all documents available on online account. I merged all my car, home, landlord policies with LV=.”

“I recently purchased a landlord policy for buildings and landlord contents which fitted my needs - the service and communication was good and the price was much more competitive than alternative quotes. The level of cover was also more generous than comparison quotes. I also have my home insurance with LV so I believe I may have obtained a discount for having multiple policies in place....so far i am happy with the service received.”

“I needed help with Landlord Buildings Insurance. The young man I spoke to was very knowledgeable, helpful and polite. Really gave me the impression he knew what he was talking about.”

“Many insurers won’t offer Contents only insurance for properties which have historically experienced subsidence/underpinning, despite minimal risk. LV does offer Contents cover in such cases. It is much appreciated.”

“Very good for value for money and reputable company.”

What could LV= Landlord insurance improve on?

Although the positive reviews overwhelmingly outweigh the negatives, there were a few pieces of feedback we thought would be worth taking into consideration if you are thinking about purchasing landlord insurance through LV=.

We found that almost all negative pieces of feedback were due to frustration at the lack of rewards for loyal customers, with many expressing their disappointment over increased renewals fees and premiums. We also found a couple of other customers were not so happy with the advice and information they received, citing it as 'useless'.

"... The references are there in the document but they arguing that because I - me personally - did not get them and because Experian got the references as part of the Credit Check, it does not count. As a result they are declining the claim..."

“I was an existing customer with 3 car insurance, hone insurance and landlord insurance . In your auto renewal the price was hiked 50%. I was expecting a slight increase in premium because we had a claim this year for stone theft (our first claim in 15 years). I went on price comparison sites and you came up cheapest with £238 ish . I phoned and spoke to you but you said the price I had on price comparison site was because I hadn’t put in the recent claim . I went back to look and I had put that I had got no years without claim so I bought the insurance from the price comparison site.”

“Insurance is expensive, being a loyal customer isn't worth it.”

“I wanted to get some advice, speak to a real person who could answer my concerns and nothing, nobody to help me because it all had to be done online, I still don't know what I paid for and I still don't know if I have the right cover, absolutely useless.”

“I have had double insurance with them for years. However , out of interest, I checked on a comparison site and was amazed at the difference in price! I then did a new quote on line for L&V using same details as old policy and was quoted £100 less than my renewal quote. I rang and complained and was told I would have to let the old policy run out and take out the new policy , which I did. Why do they try and rip off loyal customers?”

“As an existing customer I would have expected LV= to offer their best price on renewal. Instead I find a number of price comparison websites offering much better prices for the same level of cover. When queried by telephone with LV= I was told that they couldn't match the price comparison websites offers!”

Of course, any review left by a frustrated customer should be taken with a pinch of salt as context is very important here. It may be that key pieces of information related to renewals and discounts were overlooked by these customers. Nevertheless, this does not invalidate their experiences and is certainly worth bearing in mind should you wish to take out landlord insurance cover with LV=.

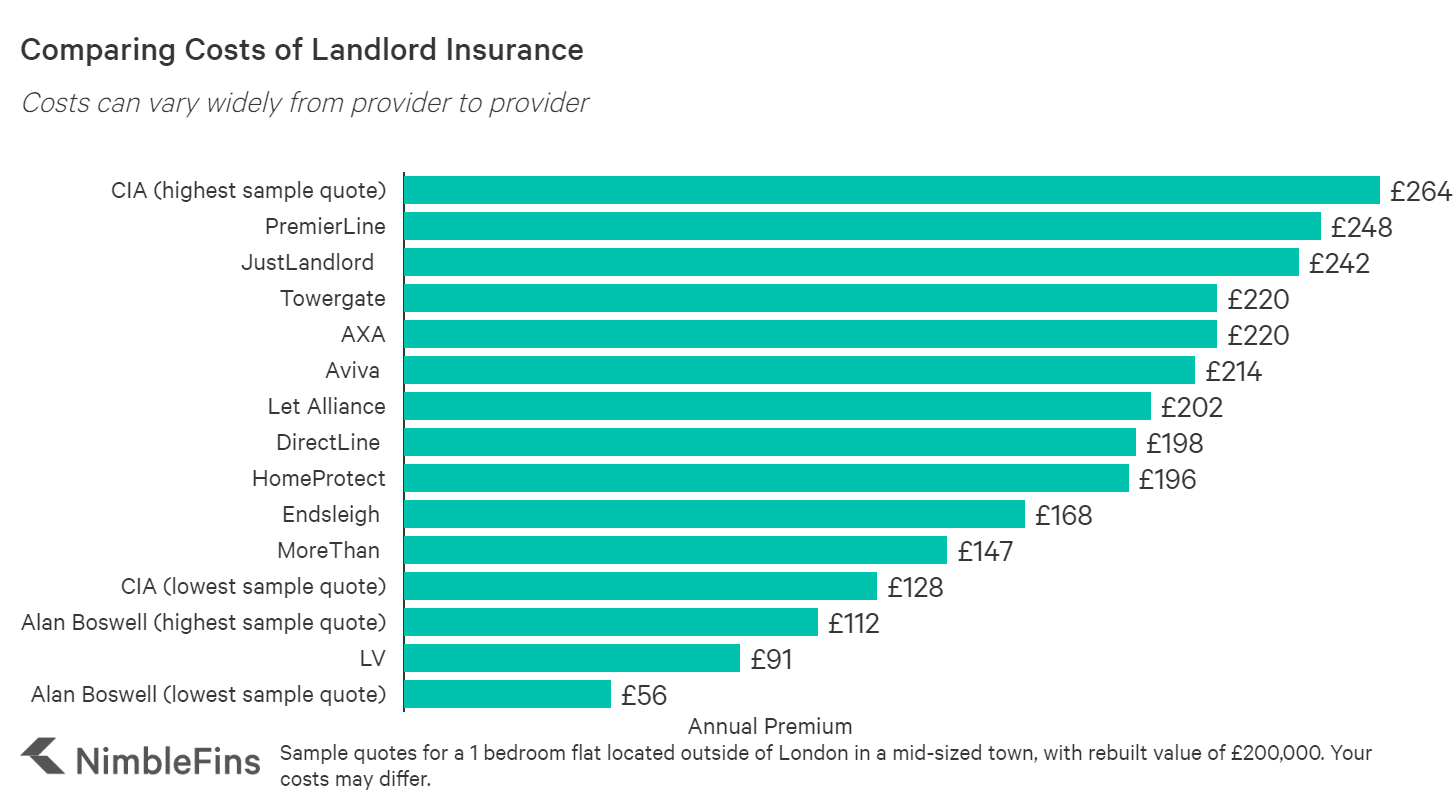

How much is LV= Landlord insurance?

We have compiled quotes for a 1 bedroom flat located outside of London in a mid-sized town, with a rebuild value of £200,000. We found that for a no-frills policy with buildings insurance and property owners liability of £5million as standard, LV=’s landlord insurance was the second cheapest provider compared to the range of insurers we sampled from.

In fact, we’ve calculated our sample quote was 51% lower than the average price of all like-for-like quotes shown below!

| Landlord insurance quote comparison for a 1 bedroom flat (£annual) | |

|---|---|

|

CIA | £264 (highest sample quote) |

|

PremierLine | £248 |

|

JustLandlord | £242 |

|

Towergate | £220 |

|

AXA | £220 |

|

Aviva | £214 |

|

Let Alliance | £202 |

|

DirectLine | £198 |

|

Home Protect | £196 |

|

Endsleigh | £168 |

|

MoreThan | £147 |

|

CIA | £128 (lowest sample quote) |

|

Alan Boswell | £112 (highest sample quote) |

|

LV | £91 |

|

Alan Boswell | £56 (lowest sample quote) |

Of course, these quotes are intended to be used as a guideline and your quotes may be higher or lower depending on your own individual circumstances.

Nevertheless, considering it is less pricy that many of its competitors, such as DirectLine, Endsleigh and JustLandlords , you may be wondering if LV='s standard landlord insurance cover offers you less protection.

Let’s take a look at what is and isn’t included to see if the low price is worth it.

What is/isn’t covered by LV='s Landlord insurance?

Despite the low price point, LV= does provide a comprehensive level of cover within their standard landlord insurance offer. Here is some of what was included in our sample quote, for which we had selected to include both buildings and contents cover:

- Buildings insurance (up to £1m rebuild): covers the cost of repair if your property is damaged as a result of events such as fire, storm, subsidence, heave, settlement as well as theft or attempted theft. This also includes landlords fixtures and fittings, too!

- Landlords contents (up to £10,000/£25,000/£50,000): if any of the contents you provide to your tenants are lost or damaged as a result of any of the events above (as well as any others outlined in your policy) this will cover the cost of repairing or replacing these.

- Loss of rental income and alternative tenant accommodation (up to £75,000 with buildings cover; or £25,000 with contents cover alone): similarly to the above, if you end up losing rent due to the fact your property has been made uninhabitable, LV= will also protect you against these losses as well as covering additional costs and expenses towards suitable alternative accommodation for your tenants for the period of time needed to make your rental property habitable again.

- Accidental damage to builds and contents: if the property structure or any of the contents you provide for your tenants are lost of damaged by accident, LV= will cover costs associated with replacement or repair. A good example of 'accidental damage' if where a tenant spills a glass of red wine over your fitted cream carpet, leaving an unsightly stain!

- Landlord liability (£5m): this will cover the costs if a third party makes a claim against you for suffering sickness, injury or if their property is damaged as a result of your actions or your property

- Replacement locks: covers the cost of replacing locks to external doors and windows if your tenants keys are lost or stolen

- Unauthorized use of metered utilities (up to £5,000): will help cover the costs following unauthorized use of these services supplying your property, for which you are legally responsible

- Trace and access (up to £5,000): covers the cost of finding the source of a water or oil leak and repairing any damage caused in gaining access

- Malicious damage and theft by tenants: if a tenant intentionally loses or damages your property or any contents that you supply, LV= will cover the costs associated with repair and or replacement. Note, this is subject to appropriate tenant referencing checks being carried out pre-tenancy, such as references, photo ID and credit checks)—be sure to check the general conditions section of your policy for this

LV= also provide an incredibly useful tool online that allows you to compare their level of coverage with some of their big-name rivals, such as DirectLine, Saga, MoreThan and AXA — make sure to check this out here.

Optional add-ons

- Landlord legal expenses (up to £100,000): LV= will provide access to a legal advice helpline as well as covering the cost of unexpected legal fees associated with e.g. eviction/repossession, pursuing rent arrears, pursuing and defending claims relating to property disputes as well as defending criminal prosecutions brought against you (e.g. Gas Safety Regulations) and HMRC tax disputes

- Landlord home emergency cover: LV= can protect you in the event of an emergency at your rental property (e.g. a boiler breakdown, plumbing emergencies, failure of electrical power or gas supply, pest infestations like wasps or rats, lost or stolen property keys). Remember, these types of emergencies can and do happen, and having an appropriate plan of action in place can save you a lot of stress and money.

Note, this legal expenses cover will only cover claims that have a 50% or higher chance of success, so do take this into account beforehand.

Missing features

There is one sometimes desirable feature that isn't offered in LV='s standard cover and isn't available to purchase as an add on.

- Landlord rent guarantee: Unlike loss of rental income, landlord rent guarantee insurance will cover you if a tenant is unable to make rental payments regardless of whether your property is habitable or not (e.g. if the tenant has recently lost their job). LV= does not provide rent guarantee cover with their landlord insurance offer so think carefully about whether you would be comfortable proceeding without this security especially is your rely on these payments as a primary source of income or to help with paying off your mortgage!

Exclusions: What isn’t included?

As with almost any type of insurance, landlord insurance often contains some exclusions that are good to be aware of so you don’t get caught out. LV= is no different, so we’ve outlined a few key ones below that are good to be aware of:

- Any damage or events that you were aware of before the policy start date: a common exclusion that is often missed, so make sure you triple check when your cover officially starts!

- War, pollution, nuclear attacks etc.: If your property is damaged as a result of events associated with these events (e.g. if, rather unfortunately, your property suffers damage from a nuclear attack) you will not be covered

- Any damage resulting from faulty design, materials or poor workmanship

- Any gradually occurring damage i.e. natural wear and tear or damage that would be expected as a result of aging

- Damage caused by frost, damp, dry-rot

- Damage caused by pets or other animals

- Damage to gates and fences caused by flood, storm, falling trees or branches

- Loss or damage deliberately caused by you, your spouse/partner, any other family member or employee

- Legal liability to any employees

- Malicious damage or theft caused by your tenants unless you’ve obtained references, photo ID and credit checks

Note, the full list of exclusions is much longer, so be sure to read your landlord insurance policy carefully!

Another key point to remember as a landlord of a rented property is that if your property is unoccupied for longer than the period of time outlined in your policy, any damage or losses that occur within this time will often not be covered. LV= offers an unoccupancy period of 45 days (longer than some of it's rivals!), but we always recommend minimizing the length of time your rental property is vacant regardless to avoid the risk of theft or burglary, for example.

How does LV= Landlord Insurance Compare to Competitors?

To better understand the value of LV= Landlord insurance you need to look at it in the context of other available options. We compared it to other plans in the market so you can see which may be more suitable for you.

LV= Landlord Insurance vs Alan Boswell Landlord Insurance

One of the most affordable insurers we sampled from, Alan Boswell certainly doesn’t lack in its cover. As standard, they cover many of the ‘essentials’ included buildings, contents, landlord liability, employer's liability as well as accidental damage and malicious damage by tenants!

That being said, for landlords looking for rent guarantee, legal expenses or landlord home emergency insurance — this will come at an extra cost. However, with excellent expert and customer ratings across the board and a low sample price to boot… it’s certainly worth considering.

Bottom Line: our research found Alan Boswell to offer excellent coverage at a fraction of the price, making it one of the best landlord insurance offers we have come across. For landlords looking for a value offer that is trusted by experts and customers alike, Alan Boswell may be the landlord insurance provider for you.

LV= Landlord Insurance vs CIA Landlord Insurance

Specializing in non-standard property and tenant types, CIA works with a panel of leading insurers to ensure you get the right level of coverage. This means it is excellent for comparing cover and prices, however, this does also mean it can vary depending on the insurer who has underwritten your policy. At the lower end, our research found CIA to be one of the cheapest options on the market, but at the highest end we found it to be one of the most expensive, so it's certainly worth taking a look!

Nevertheless, CIA offer a high level of standard cover — typically this includes buildings, contents, accidental damage, loss of rental income and employer's liability. CIA also offers rent guarantee which provides an added layer of financial protection should you want it.

Bottom line: with excellent customer feedback, CIA could be perfect for landlords looking for comprehensive cover with the freedom to tailor their cover to suit their needs. CIA is also an excellent contender for landlords renting non-standard properties or to more risky tenants.

LV= Landlord Insurance vs Direct Line Landlord Insurance

Direct Line is one of the UK’s largest and most reputable insurers, and considered to be one of the best landlord insurance products on the market. With over 250,000 existing landlord insurance policy holders it is certainly a popular choice and has won multiple awards to boot. Its comprehensive cover includes buildings, contents and landlord liability included as standard.

Direct Line offers a range of optional add-ons such as malicious damage by tenants, loss of rental income and legal expenses meaning you can curate the right policy for your needs. Direct Line also offer some discounts for new and existing landlords, such as a 10% multi-property discount if you’re looking to insure 15+ properties!

Bottom Line: If you’re looking for award-winning coverage from a reputable insurer then Direct Line may be another option to consider — despite the fact Direct Line appears to be more pricey than LV=, we do find it to be worth it.

How to make a claim on LV='s Landlord insurance

You can find all the information you need to make a claim on LV='s website as well as in your policy documentation, but we’ve listed the key contact number below:

- LV= claims number: 0800 032 2811 (open 24/7)

Before you decide to make a claim, we recommend that you read your policy wording carefully to ensure that you are indeed covered. If you are, you may be asked to provide certain details and documentation such as your policy number, photographic evidence of your loss or damage, receipts and invoices so it’s always a good idea to have these handy, or be prepared to acquire these if necessary to avoid delay.

LV= landlord insurance: Discounts and savings

At the time of writing, LV= offer a nice incentive to new customers who choose to take out a landlord insurance policy with them.

- 5% discount for new customers when they purchase landlord insurance online (exludes landlord legal expenses)

You can also check out our ultimate guide to simple tips and tricks you can use to help you save a few extra pennies as well, here.