The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

Which Type of Pet Insurance is Best for Me?

As seen on

Pet Insurance Policy Types Explained

Pet insurance is meant to help pay for vet fee bills, but some types of policies really fall short and can leave a pet owner paying more than their fair share. When buying pet insurance, it's critical to learn about the different types of policies as some may not suit your needs. There are four types of cover—accident only, time limited, maximum benefit or lifetime—but these vary considerably in terms of coverage levels and premiums. We'll explain what each type covers and how premiums differ across the four policy types—as well as other important features and considerations—so you can decide which is best for you.

Compare Cheap Pet Insurance

Pet cover can help with vet bills. Protect yourself from expensive vet bills.

Accident Only

While premiums are typically cheapest on accident-only policies, they offer the least comprehensive coverage as they only protect against accidents/injuries—not illnesses. Generally speaking, illnesses (e.g., tumour, ear infection, joint pain) suffered by your beloved pet will not be covered under an accident-only policy.

According to the Money Advice Service, 70% of pet insurance claims are for illness, not accidents. While this figure is a few years old, it remains the primary benchmark for the industry in 2026. Data from the Association of British Insurers (ABI) supports this trend, noting that the 'vast majority' of the record £1.2 billion paid out in 2024 was for the treatment of health conditions, which often require long-term veterinary care.

The takeaway? Since the majority of pet insurance claims are related to illnesses not accidents/injuries, an accident only policy can leave you uninsured for significant vet bills.

- Covers accidental injury only (not illnesses)

- £ cover limit for each injury

- Each injury typically only covered for 12 months

In the end, accident only policies are not usually the best option for saving money on pet insurance. Not only are illness the most common type of claim but pet insurance claims for illnesses can easily reach into the hundreds or thousands of pounds—accident only plans won't offer any help for these types of vet bills.

In fact, accident only cover is so inferior that many insurance providers don't even offer this type of cover.

Typically, there is a set maximum amount you can claim per accident and over the life of the policy. For instance an accident only policy limit may be £2,500 per accident and £15,000 over the policy lifetime (which is extended every time you renew). In this case, for example, your policy would cover say up to six accidents that cost £2,500 each in vet fees.

Examples of Common Accident Only Claims

- Broken Leg

- Swallowed Foreign Object

- Broken Tooth

- Sprain or Joint Injury

- Eye Wound

- Cuts, Bruises, Bites

- Torn nail

Time-Limited

Time limited policies are slightly better than accident only policies, because they will cover illness as well as accidents—but only for a short time. Time limited plans are capped both in the £ amount of reimbursement for an injury/illness and also the length of time that treatment is covered. When you hit either the set limit (e.g., £4,000) or the set time period (e.g., 12 months) your cover for that injury or illness will stop.

- Covers illness and injury

- £ cover limit for each injury or illness

- Each illness or injury only covered for 12 months

Time-limited policies can really catch a pet owner unaware as they are most suited to short-term issues, not long-term problems. Ongoing or recurring vet bills will not be covered beyond 12 months. For example, if your dog suffers from an ear infection when he is two years old, then ear infections when he is three or older will not be covered as they fall beyond the usual 12-month window of coverage on a time-limited policy.

Additionally, it is important to note that illnesses such as ear infections are usually deemed "bilateral"—meaning both the left and right sides count as the same illness. A claim for hip dysplasia in one hip starts the 12-month clock ticking on claims for both hips.

Older pets may only be eligible for time-limited policies, not max benefit or lifetime cover. Many insurers won't offer lifetime or maximum benefit cover to older pets, as they are more likely to suffer from ongoing health problems. Typically, once dogs reach 8 or 9 years of age they are not eligible for lifetime policies, although some breeds may hit this threshold at 5 years of age.

Time-Limited Policies Most Appropriate for...

- Older pets (may not be eligible for some Lifetime policies)

- Short-term injury or illness protection

Maximum Benefit Per Condition

Maximum benefit policies provide a capped amount of money to use towards a given condition (illness or injury). So long as you keep renewing the policy, there is no time limit on using this money. For instance, on a maximum benefit policy with a £2,000 per condition limit, your dog's ear infections could potentially be covered over many years, up until the total reimbursement for ear infections hits the £2,000 cap (so long as you renew each year).

- Covers illness and injury

- £ cover limit for each injury or illness

- No time limit

Maximum benefit policies generally provide a higher level of coverage than time-limited policies, because claims will continued to be paid over time up to the £ limit so long as the policy is in effect.

As with time-limited policies, illnesses such as ear infections are usually deemed "bilateral"—meaning both the left and right sides count as the same illness and draw upon one pot of claims money, not two.

Maximum Benefit Policies Most Appropriate for...

- Younger pets

- Shorter-term injury or illness protection

- Recurring illnesses, so long as expected lifetime vet bills per condition are relatively low

- Medium level of coverage

Lifetime

Lifetime policies offer the highest level of coverage for your pet. Lifetime policies typically cover both accidents and illnesses and the amount of money you can use each year resets every time you renew the policy.

- Covers illness and injury

- £ cover limit per year that resets when you renew

- No time limit for cover (so long as you keep renewing the policy)

Lifetime policies are typically the most expensive (all else equal), but if you can afford the extra few pounds per month then we think it's safer to pay up for it. Doing so will give you peace of mind that unexpected vet bills will be covered, year after year, even for recurring issues.

Note: some "lifetime" policies have a maximum limit per condition (e.g., ear infection, tumours, etc.) per year, others don't. If there is such a limit on a lifetime policy, it resets each time you renew your policy. But this is certainly something to check before buying a policy.

Lifetime Policies Most Appropriate for...

- Younger pets

- Long-term injury or illness protection

- Recurring/ongoing ailments

- Highest vet fee limits

Summary of Coverage Types

Below we've summarized the typical features of the different types of pet insurance policies available in the UK.

Comparing Pet Insurance Policy Types

| Policy Type | Covers Accident and Illness? | Is there a Limit on the Time a Condition is Covered (e.g., 12 Months)? | Is there a Limit on the £ Claim per Condition? |

|---|---|---|---|

| Accident Only | Accident | Yes | Yes |

| Time Limited | Accident and Illness | Yes | Yes |

| Maximum Benefit | Accident and Illness | No | Yes |

| Lifetime | Accident and Illness | No | Possibly, but will reset each year |

As you can see above, only max benefit and lifetime policies will protect against recurring or ongoing (i.e. chronic) health issues. If you think that isn't a problem, remember there are a lot of recurring or chronic pet health issues that could affect your dog or cat, such as diabetes, arthritis, kidney disease, allergies, ear/eye infections, skin masses, etc.

And to truly get the best long-term protection against chronic and recurring issues, lifetime cover is typically the best option because the vet fee limits reset each year (vs max benefit, where once you use up the limit there you're out of money to treat that condition for good, because it doesn't reset each year).

Best Dog Insurance

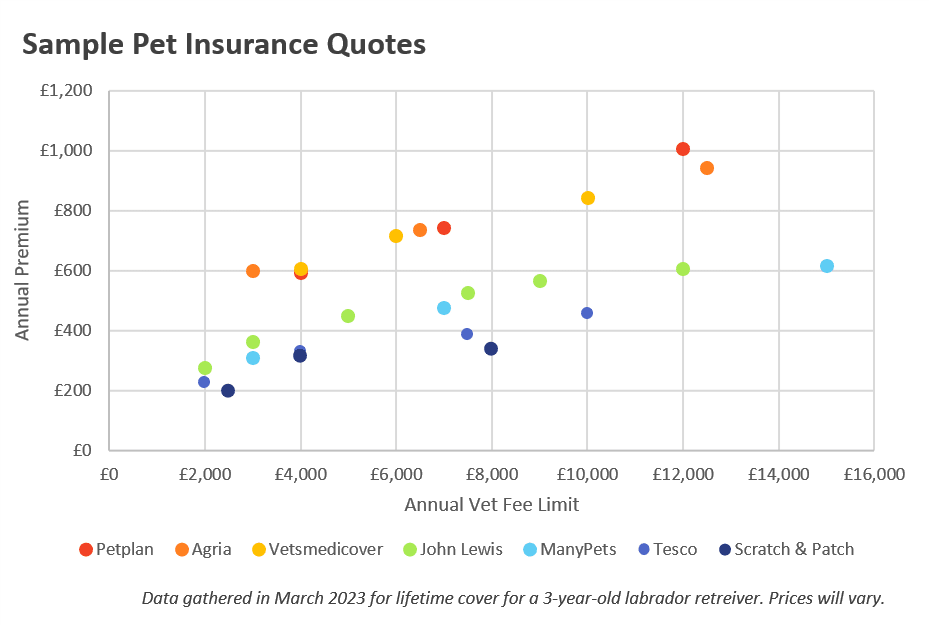

In our personal and professional experience, lifetime pet insurance is the best type of dog insurance because the limits renew each year to protect recurring or chronic conditions. Which company is best? That depends. You may think the best is a company like Petplan, which has a long history of being the largest pet insurance company in the UK, longstanding relationships with practically every vet in the country and reliable service from a specialist. They may cost more initially, however, as you can see in the chart below. But they say they won't increase your premium as a direct result of making a claim, so in the long run they could end up cheaper.

Note, these prices are meant to illustrate how different brands broadly sit in the marketplace; they are not exact quotes or indicate which is best for you.

Some people might think a cheap initial premium is best for their situation, so may prefer a company like ManyPets or Scratch & Patch. But cheaper policies often include less robust features. For example, taking a quick look at the companies above, Tesco doesn't cover behavioural problems, most of ManyPets' lifetime policies don't cover dental illness, and Scratch & Patch doesn't cover dental illness plus there are lower sub-limits for claims like MRI/CT scans, behavioural problems, alternative therapies, dental injury and cruciate ligaments. And these companies may increase your premium if you claim.

Animal Friends is another very popular brand, famed for its transparency—communicating well with customers and telling you what you need to know in plain English. They're another specialist provider with a wide range of products suitable for a range of budgets and needs. One bit to lookout for there is the inner limits for some claims.

(Note: the prices reflect a 10% year 1 discount from Petplan. VetsMediCover has ceased offering new policies; a common market alternative, Agria, currently offers a 10% introductory discount.)

Some of our favourite dog insurance companies, who we've partnered with, are listed below.

You can compare policies from many companies here to find the best dog insurance for you:

Pet insurance comparison

We've gathered data from a leading pet insurance provider to illustrate how premiums vary by policy type, in this case for dog insurance. The chart below shows monthly premium estimates for a 3-month-old male Cockapoo, for accident-only, time-limited, maximum benefit and lifetime policies. As coverage goes up with policy type, so do premiums.

Getting it Right

Choosing the right type of policy is crucial. Due to the exclusion of pre-existing conditions on most policies, switching to a different insurance policy later may not be a feasible option for you. If you switch policies or insurers, any illnesses you've ever claimed for in the past will typically be excluded in your new policy—a crucial point to understand when learning about how pet insurance works.

While there are a few options for buying a new pet insurance policy that covers pre-existing conditions, there are limitations and difficulties with doing so. For example, only one company covers recent pre-existing conditions, and this policy will cost more and limit the amount of cover for pre-existing conditions. Other options only cover a pre-existing condition after the pet has been healthy for 2 years—so these are no help for recurring or long-term conditions.

If you can budget for a lifetime policy, the extra cost each month may well be worth it in the long run. Taking out the cheapest policy available (e.g., accident only or time limited) may not be the best financial decision, as not only is coverage limited on cheaper policies but upgrading to a more comprehensive policy later (e.g. a lifetime policy) may be difficult as a result of pre-existing conditions.

Bilateral Conditions: This is important!

Have you heard of bilateral conditions? It's a common phrase in pet insurance policy wordings. "Bilateral conditions" means any condition affecting right and left sides or paired organs or body parts of your pet, such as (but not limited to) ears, eyes, cruciate ligaments, hips and patellae.

Bilateral conditions are really important to understand because they can limit your cover if you have time limited or max benefit cover—they aren't a concern with lifetime policies. When applying a time limit or maximum benefit to cover, pet insurance companies typically consider bilateral conditions as one condition.

In plain English this means that, for example, an eye infection in one eye starts the clock (in the case of a time limited policy) or starts using the vet fee limit (in the case of a max benefit policy) for BOTH eyes. So an eye infection in the left eye treated in July 2023 on a 12-month time limited policy means that an eye infection in 2025 wouldn't be covered (even if you keep renewing the policy year after year).

Bilateral conditions can severely limit the effectiveness of time limited and max benefit policies.

What features do the best pet insurance policies have?

The list of desirable features will vary from person to person, as some people will care about features that other people couldn't give a tuppence about (a good example of this is cover for your dog in Europe—totally irrelevant if your dog never leaves the island). But, that said, let's discuss some of the key features to look for to find the best policy for you.

- The £ vet fee limit: The most important feature is really the vet fee limit. What to look out for here? Is there is a time limit on when you can use it (e.g. 12 months from first signs)? Does the limit apply to each condition (max benefit)? Or does the vet fee limit renew each year (lifetime cover)? Are there any sublimits (that is, lower limits for certain types of claims like MRIs, alternative therapies, etc.)? Also, is the limit high enough? Some problems can easily cost many thousands of pounds to treat, or more.

- Will making a claim increase your renewal price? In 2026, most pet insurance providers state that renewal premiums are influenced by your claims history. Nearly all pet insurance companies say that the renewal premium can be affected by your claims history. Tesco and John Lewis continue to include wording in their policy summaries stating that premiums can increase significantly—in some cases up to 100%—following a claim for a chronic condition. One exception to this is Petplan (read about them here or get a quote here)—they specifically say you won't pay more at renewal for previous claims. (See below for industry-wide data on this.)

- Time to claim: We think this is a big but often overlooked feature to consider. Some insurers only give you 60 days to submit a claim. That might sound like a lot of time to get your ducks in a row, but 60 days can pass in the blink of an eye and leave you unable to be reimbursed for what should be a legitimate claim. We like long claims windows (e.g. 1 year with Petplan and Manypets) compared to shorter claim windows (e.g. 60 days with Purely Pets or 90 days with Animal Friends). But companies with shorter claims windows might be cheaper so you may prefer this, if you're organised—but be sure to clock the claims window so you're not caught out.

- Can your vet submit claims on your behalf? Most pet insurance companies are willing to pay the vet directly. But as we've found through personal experience, vets may be more likely to submit pet insurance claims on your behalf (for direct payment to them) to some pet insurance companies compared to others. In large part, this is dependent on the size of the insurer. Large insurers like Petplan and Manypets are likely to be commonly used by your fellow pet owners, so your vet is probably accustomed to their forms and processes. And they have online claims systems, avoiding paperwork. Some insurers even have claims systems the vet can access (e.g. Animal Friends' Pawtal claims system).

- Excess: The excess is the amount you pay per condition (usually, per year). The excess on a pet insurance policy in the UK is typically around £100 but this can vary. It's good to check this to be sure you could pay the excess if you need to make a claim. Also, check the policy details to see how the excess changes when your pet gets older. It's somewhat common for an insurer to change a fixed excess (e.g. £100) into a fixed + variable excess (e.g. £100 + 20%) for older pets. This change typically kicks in at around age 7 or 8 for dogs; perhaps later for cats. But some insurers start adding the variable excess component even earlier (e.g. age 6 with Purely Pets; age 5 for select dog breeds with PDSA). Some insurers don't impose a variable excess component for older pets. Including a variable component can help keep the premium lower, but means you pay more when you claim. How much do you care about this?

- Putting your pet to sleep and cremation or burial costs: At the end of the day, most pets are put to sleep to help them avoid suffering. It's somewhat rare for a pet to die of natural causes on their own without intervention. Will your pet insurance cover it? If yours doesn't, and you aren't aware of this, it can make a very distressing time even more distressing to find out your pet insurance won't help with these costs. Some insurers don't cover any of these costs, some cover euthanasia only, some cover euthanasia as well as cremation or burial. When covered, the costs may be covered under vet fee limits or there may be a lower sublimit (e.g. £200).

- Dental illness: Most policies cover dental injury (e.g. your dog chips a tooth carrying a heavy log) but only some cover dental illness (e.g. periodontal disease like gingivitis/inflammation of the gums that can lead to tooth root abscesses, bone infection of the jaw, or even a disease-induced jaw fracture). Unfortunately, dental illness is pretty common for dogs and many are likely to need treatment (e.g. tooth removal) during their lifetime. (Note: pet insurance won't cover dental cleaning, however—not even the best policies!)

There are many, many other features to consider. Above, we touched on some of the important ones/ones that might be overlooked. If you'd like us to discuss any others, please let us know in the comments section below!

Example: Real-Life Story

I personally have two examples of why lifetime pet insurance offers the best cover. First, my dog developed allergies when he war around 2 years old. As a result, he developed lesions on his tummy that he licked incessantly and serious ear infections. That meant monthly or even bi-weekly visits to the vet when he had bad flare ups. In addition to consults and medicines to treat the ear infections and lesions, he had blood work to try to identify the source of the allergy. This went on for years and cost more than I even remember. Since we have lifetime pet insurance this was all covered (except for the excess, which we paid each year for the condition). We've now figured out his food and how to manage any minor flare ups so it's largely under control, but on occasion if he now develops a related problem we can zip to the vet to get treatment, and have it covered.

Also, my poor dog developed a strange hop on his right rear leg, where he avoids putting it down every step or two while he's trotting along. The vet recommended x-rays, then a visit to a specialist, who ordered an MRI (the MRI alone cost thousands of pounds). Long story short, the vets could find nothing specifically wrong, and told us to come back if it gets worse or he seems to be in any pain (after treatment with anti-inflammatories, which had no impact on the hop, the vets decided he is not in pain now, luckily). Since we have lifetime pet insurance, we know that if things change in the future, we can go back to the vet and have it covered.

If we had accident only or time limited cover, we certainly would not be covered for these ongoing conditions. Max benefit might be enough, if the cover limit was high enough to encompass all of the past and future costs for each condition. But we feel that lifetime pet insurance offers the best protection for us since the limits renew each year to cover these longer-term issues.

FAQs

It's generally best to get a lifetime policy if you can afford it, because these policies have limits that renew each year to protect against long-term or recurring conditions. The next best is usually considered max benefit.

Yes, lifetime pet insurance covers accidents, as well as illnesses.

There are four type of pet insurance in the UK marketplace: Accident Only, Time Limited, Max Benefit and Lifetime. Read more about the best type of cover, Lifetime pet insurance.

Pet insurance primarily covers vet bills for accidents and/or illnesses, depending on the type of policy you buy. Pet insurance can also cover third party liability (dogs only), holiday cancellation cover, euthanasia, cremation/burial, loss of a pet and more. Read more in our article What Does Pet Insurance Cover?.

The best type of dog insurance is lifetime cover, because these types of policies have limits that renew each year. Renewing limits protect against long-term or recurring conditions over the course of your dog's life. The next best type of cover is usually considered to be max benefit.

Lifetime pet insurance is better because the vet limits renew each year; in contrast, max benefit plans stop reimbursing for vet bills after you've hit a maximum limit for each illness or injury. Lifetime plans are therefore better at covering long-term or recurring conditions.

Where to Get Pet Insurance Quotes

To get quotes from a range of UK dog insurance brands including Scratch and Patch and Animal Friends, click the blue button below to access our pet insurance comparison tool.

Compare Pet Insurance Quotes

Panel includes Animal Friends, Scratch and Patch, Lifetime Pet Cover and more.

Comparing Pet Insurance Companies: Does Premium Increase After a Claim?

There can be difficulties with switching pet insurance after a claim whilst keeping cover for pre-existing conditions (because few companies offer cover for pre-existing conditions). But if you claim, there's a good chance your pet insurance premium will increase. If this happens, pet owners can feel trapped paying a higher premium, unable to switch. How likely is it that your premium will increase after a pet insurance claim? We took a look to find out, scouring pet insurer websites and policy wordings. Here's what we found for over a dozen companies:

| Pet Insurance Company | Can Premium Increase if You Claim? | Language | Source |

|---|---|---|---|

| Agria | Yes | Premiums are adjusted at renewal based on your pet’s age and your claims history. | Agria |

| Animal Friends | Yes | "We review your premium price on an annual basis and there are multiple factors that may cause pricing changes, either up or down... These include your pet’s age, claims history, your location, the average cost of vet treatment at the time, changes in tax rates etc." | website |

| Direct Line | Yes | "We may change any details relating to your policy and premium on each anniversary date of the start of your insurance. Your pet’s medical history and claims’ history will be taken into account." | policy wording |

| EveryPaw | Yes | "... changes due to new information arising from our own experience suggesting that our future claims experience is likely to be better or worse than previously assumed. This information includes changes to the number and types of claims we expect to pay or changes to the average expected amount paid per claim ... [and] changes to your circumstances such as the age of your pet, your claims history..." | policy wording |

| Healthy Pets | Unknown | We've reached out to enquire and will update this table when we have more information. | Healthy Pets |

| John Lewis | Yes | "Unfortunately, once a pet has been taken ill, in general they’re more likely to get ill again. That’s why, if a claim is paid, the price you will pay next year can double." | policy wording |

| Lifetime Pet Insurance | It seems so | "If the health of your pet changes, your premiums are likely to increase in cost." | website |

| LV= | Yes | "A number of factors impact your price, such as your pet’s age, claims you’ve made, increased veterinary costs and advancements in veterinary medicine." | policy wording |

| ManyPets | Yes | "Making claims can affect your renewal price as this will affect our health prediction for your individual pet." | website |

| More Than | Yes | "If a claim is paid, the price you will pay next year can double. There is no limit to how much your renewal price can increase over time." | website |

| Petplan | No | "We don’t directly increase premiums for claims – and it’s why we don’t offer no-claims discounts." | website |

| Purely Pets | Yes | "Like humans, our pets are more likely to be affected by illness as they get older. This means that every year your insurance premium will increase even if you haven’t made a claim. This increase will be significant if you have claimed." | website |

| Scratch & Patch | Yes | "This means that based on the information you have provided to us, your pet’s age and medical history, any claims made and future expected treatment and claims costs, we may change the terms and conditions of your cover, your premium or not offer to renew your policy. Please be aware that the chances of your pet getting ill increases as they age and this means your insurance premium will also increase. This increase could be significant if you have made a claim." | website |

| Tesco | Yes | "A claim being paid can cause your renewal price next year to double." | policy wording |

| Vetsmedicover | Yes | "As Lifetime cover provides cover for all conditions over the life of your pet, you must be able to afford to pay the yearly premiums which will increase at renewal based on the age of your pet, claims history and other cost such as enhancements to veterinary treatments." | website |

As you can see in the table above, of the companies we've checked, Petplan is the best in terms of not increasing your premium as a direct result of a claim. (Of course, your premium will still probably increase every year with any pet insurance company, regardless of claims, due to rising health risks with age.) Want a quote from Petplan? Click below. Or read more about them in our review here.

- Range of Vet Cover

- £3,000 - £12,000

- Types of Plans

- Time Limited and Lifetime

- Dental Cover

- Dental illness and injury covered

- Excess

- £75 - £120