The guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement. Read our full disclosure here.

What does a Pet Insurance Excess Mean?

Best pet insurance deals for your pet

Quickly compare 25+ providers. Pay from £2.82 a month.*

The excess is the amount a pet owner pays towards any pet insurance claim. Here we explain the types of excess you might come across, an example illustrating how payments are shared between pet owner and insurer, discussion of when to choose a higher excess and information on how excess might change for older pets.

- What are the types of pet insurance excess?

- How much will I pay towards a vet claim? An example

- When do you pay the excess?

- Should you opt for a higher excess?

- Will I pay a higher excess for my older pet?

Types of Excess

The excess on a pet insurance policy is generally a compulsory, fixed £ amount. While a £100 excess remains a common benchmark, the latest 2026 data shows a wider spectrum: typical fixed excesses now range from £60 to £125, though some premium providers have increased their standard fixed excess to as much as £199. Your policy may also include an optional voluntary amount (fixed £ or %) which you may opt to pay on top of the compulsory amount in order to reduce your premium.

Some insurers also require that you pay a copay, which is a percentage of vet fees. The copay percentage is calculated after the fixed £ excess. It's becoming more common for pet insurers to institute a copay once a pet hits a certain age (and claims are likely to increase).

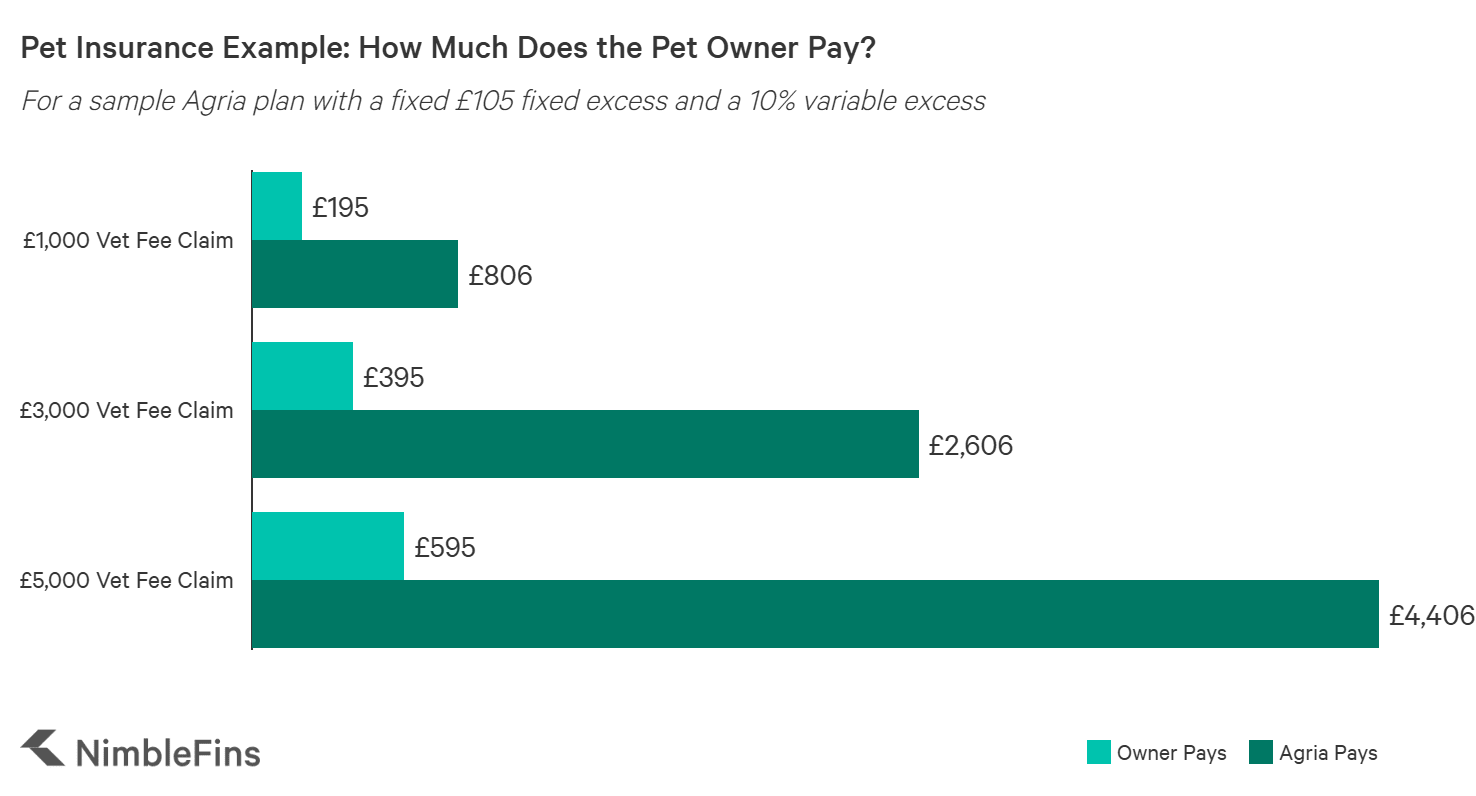

Pet Insurance Example

How much are you really out of pocket when you make a claim on a vet bill? To see how this works in 2026, let's look at a high-performing plan (like Agria). On a £1,000 vet bill with a £105 fixed excess and a 10% variable excess (copay), the calculation is: (£1,000 - £105) * 10% = £89.50. Adding the fixed excess back in, the pet owner pays £194.50. Here's the breakdown:

| Excess Example with £1,000 vet bill, £105 fixed excess and 10% copay | |

|---|---|

| Starting Vet Fees | £1,000 |

| Owner excess contribution | -£105 |

| Owner copay contribution (10% of remaining £895) | -£89.50 |

| Insurer pays: | £805.50 |

| Pet owner pays: | £194.50 |

One question that many people have is, 'If my claim is for more than my limit, does the pet insurer pay the full limit or do they pay that less the excess?' The short answer is, it depends. Each insurer will have their own policy for this; and some insurers may change their policy, in which case it will take a year to transition everyone to the new policy as renewals come up.

For example, we recently reached out to Animal Friends to ask about this. They said this was one of the things that changed a recent policy update. Now, the excess is NOT removed from the vet fee. So a customer would be able to claim the full limit.

How a Pet Insurance Excess Works

The excess is generally taken from the first claim on a new condition. For example, if you submit a claim for a £300 vet fee and your excess is £100, then your insurer will pay £200 of the claimed amount.

On most Lifetime types of pet insurance, in which the the vet fee limit resets each year you renew, you pay the excess on the first claim for each condition each year. For example, if you claim for an ongoing condition periodically over three years, you'd pay the excess three times—once per year for the same ongoing condition.

If you make multiple claims in one year and they are for different conditions, you'd pay the excess multiple times—once for each different condition.

But on a Max Benefit we've seen policies where the excess is either payable per condition (just once per condition) or per condition per year (so every year you claim for each condition). Be sure to check your documents.

And remember, if there is a % copay component of your excess, then you pay that % of all vet bills after the fixed £ excess is taken into consideration.

Optional Higher Excess = Lower Premiums

Many insurers allow you to choose your excess to manage costs. For instance, Tesco Pet Insurance currently offers fixed excess tiers of £60, £120, or £200. However, be aware that opting for a higher total excess (e.g., choosing £150 over £75) typically only saves you around 8% to 10% in annual premiums—a saving that is often wiped out by the cost of just one single claim.

Our observations of the market tell us that it only pays to choose a higher excess if you don't make any claims in a year. Generally speaking, if you make a claim then you would be better off financially on a more expensive policy with a lower excess. You can learn more in our article analyzing the High Excess vs. Low Excess Dilemma.

If you would like a plan with both a relatively low excess and a low price, there are some decent, cheap Lifetime pet insurance options available in the UK that you may find suitable.

Excess Changes for Older Pets

In the current market, insurers are introducing mandatory copays much earlier than in previous years. The "older" pet excess is often a fixed £ excess + a % copay of remaining vet fees. You may see these changes begin as early as age 4 for Lifetime Pet Cover, age 5 for Healthy Pets (15% copay), or age 5 for select breeds with providers like Tesco and the PDSA.

Here you can read more about pet insurance for older pets.

Understanding your excess is critical in today's economy as veterinary costs continue to climb. The average pet insurance claim has now risen to £668, and UK insurers are currently paying out a record £3.2 million every single day to cover treatments. With payouts at an all-time high, choosing the right excess balance is the most effective way to ensure your pet remains covered without your premiums becoming unaffordable.