Personal loan for home renovation: financing your home improvements

Planning a home renovation but not sure how to pay for it? You're not alone. Whether you're considering a new kitchen, adding an extension, or refreshing your bathroom, a personal loan is one way to spread the cost without dipping into your savings.

This guide explains how personal loans for home improvements work, what they typically cost, and what to consider before applying. It covers unsecured and secured options, the application process, and some alternatives worth knowing about.

Always make sure you can afford repayments before taking out any form of credit.

What are home improvement loans?

A home improvement loan is typically an unsecured personal loan used to fund renovation work. Rather than securing the debt against your property, the lender assesses your creditworthiness and ability to repay. You receive a lump sum upfront and repay it in fixed monthly instalments over an agreed term.

Once funds are released, there are generally no restrictions on which home improvement projects you use them for, whether that's an essential repair like a boiler replacement or a larger project such as a loft conversion.

Types of home improvement loans

When looking at financing options, you'll broadly encounter two categories:

Unsecured personal loans do not require you to put up your home or any other asset as security. They tend to offer borrowing amounts from around £1,000 up to £25,000 or more depending on the lender, with faster approval times. Because the lender takes on more risk, interest rates are generally higher than for secured borrowing.

Secured loans use your home as collateral, allowing you to borrow larger amounts, sometimes significantly more than an unsecured loan. Rates are typically lower, but if you cannot keep up with repayments you risk losing your home.

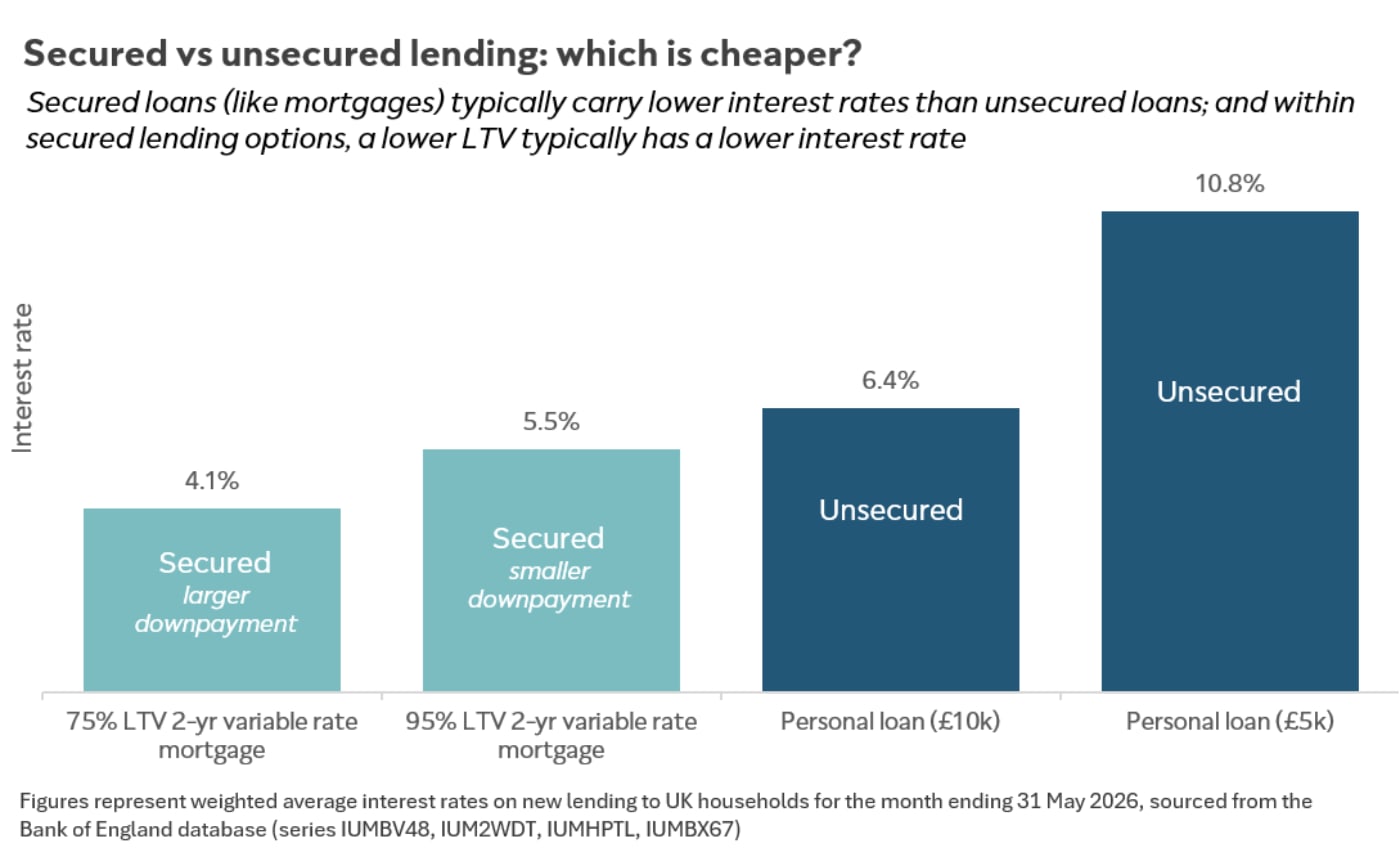

The chart below shows how interest rates for unsecured personal loans are, on average, higher than secured loans. According to Bank of England data from May 2026, the interest rate is 10.8% on a typical £5,000 unsecured personal loan, which is around 2x the typical rate on a 2-year variable rate mortgage.

Your home may be repossessed if you do not keep up repayments on your mortgage.

How home improvement loans differ from other financing

Unlike remortgaging, which involves renegotiating your entire mortgage deal, a personal loan is a separate agreement that does not affect your existing mortgage terms. Unlike a credit card, it offers a fixed interest rate and a defined repayment schedule, so you know exactly when the debt will be cleared.

The trade-off is that personal loans typically carry higher interest rates than secured borrowing, though they carry no direct risk to your property.

When might a home improvement loan be worth considering?

A personal loan may be worth considering for home improvements if:

- Your project costs fall broadly in the range where unsecured borrowing is practical

- You want fixed monthly payments to help with budgeting

- You'd prefer not to use your home as collateral

- You need funds relatively quickly

That said, whether a personal loan is appropriate depends on your individual circumstances, including your income, existing debts, and credit history. Eligibility and the rate you're offered will vary between lenders.

Common projects funded through personal loans

People commonly use personal loans to fund a range of renovation work, including kitchen and bathroom upgrades, loft conversions, boiler replacements, window replacements, and garden landscaping. The cost of these projects varies widely depending on the scope of work, materials, and location in the UK.

Pros and cons of home improvement loans

Advantages:

- Fixed interest rates and predictable monthly payments

- No collateral required for unsecured loans

- Funds can typically be received relatively quickly after approval

- Can be used flexibly across different types of renovation work

Disadvantages:

- Higher interest rates than secured loan options

- Monthly repayments increase your regular outgoings

- Early repayment charges may apply with some lenders

- Lower borrowing limits compared to secured products

Home improvement loan rates in 2026

The rate you are offered on a personal loan depends on a number of personal factors. The representative APR advertised by a lender must be offered to at least 51% of successful applicants, but many borrowers will receive a different rate depending on their credit profile, income, and the amount and term they apply for.

Factors that affect your personal loan rate

- Credit score and credit history

- Income and affordability

- Employment status

- Existing level of debt

- The amount you want to borrow and over how long

It's worth using a lender's eligibility checker or a soft-search comparison tool before submitting a full application. These tools give an indication of whether you're likely to be accepted and what rate you might be offered, without leaving a mark on your credit file.

Total cost of borrowing

When comparing loans, it's important to look beyond the monthly payment. Longer repayment terms reduce your monthly outgoings but increase the total amount of interest you pay overall. For example, borrowing £10,000 at 8.9% APR over 3 years would cost less in total interest than spreading the same loan over 5 years, even though the monthly payments would be higher on the shorter term.

Always make sure you can afford repayments.

Some lenders offering home improvement loans in 2026

Several high street and online lenders offer personal loans that can be used for home improvements. The details below are based on publicly available information and are subject to change. Rates and loan limits depend on your personal circumstances, and eligibility is assessed by each lender individually.

NimbleFins is a credit broker, not a lender.

HSBC currently offers personal loans for home improvements from £1,000 to £30,000 for standard customers, or up to £50,000 for HSBC Premier account holders. The representative APR for loans between £7,500 and £20,000 is 6.2%. Repayment terms of up to 8 years are available depending on the amount borrowed.

TSB offers unsecured home improvement loans from £1,000 to £25,000 (or from £300 to £50,000 for existing TSB current account holders). The representative APR is 5.9% for loans between £7,500 and £25,000 over 1 to 5 years. Same-day funding may be available for existing TSB current account holders who apply before 6pm.

Santander offers personal loans from £1,000 to £25,000 with fixed monthly repayments. According to Santander's website, the maximum APR they could offer is 29.9%, and eligibility requires a minimum age of 21 and a regular income meeting their thresholds.

These are examples only. Rates, limits, and eligibility criteria vary, and the rate you are offered may differ from any advertised representative APR. You should compare options carefully and check eligibility before applying.

How to apply for a home improvement loan

The application process for a personal loan is typically straightforward. Here is what to expect:

- Check your credit report using a free service such as Experian or similar, to understand your starting position

- Use eligibility checkers or soft-search comparison tools to identify lenders likely to accept you without impacting your credit score

- Compare rates, terms, fees, and total repayable amounts across lenders

- Gather the documents you're likely to need (see below)

- Submit a formal application once you've chosen a lender

- Review and sign your loan agreement if approved

- Receive funds, typically within a few working days of approval

Note: NimbleFins has been acquired by ClearScore. ClearScore provides a free credit score and report service.

Documents typically required

- Proof of identity (passport or driving licence)

- Proof of address (recent utility bill or bank statement)

- Proof of income (recent payslips, P60, or bank statements)

- Confirmation of employment status if relevant

Application tips

- Avoid making multiple full credit applications in a short space of time, as each one leaves a mark on your credit file

- Apply for an amount you can realistically afford to repay each month

- Check whether early repayment charges apply if you might want to pay off the loan early

- Budget for unexpected project costs and do not borrow more than you need

Alternatives to a personal loan for home improvements

A personal loan is not the only way to fund home improvements. Depending on your project size and financial situation, the following may also be worth exploring:

Secured loans

For larger projects, a secured loan uses your home as collateral and can allow you to borrow more at a lower interest rate than an unsecured loan. However, secured lending carries the risk of repossession if you cannot keep up with repayments.

Remortgaging

Remortgaging involves switching to a new mortgage deal, potentially releasing equity to fund renovations. This may offer lower interest rates for larger amounts, but comes with arrangement fees, valuation costs, and potentially a longer commitment. It is regulated mortgage activity and independent advice from a qualified mortgage adviser may be appropriate.

Your home may be repossessed if you do not keep up repayments on a mortgage or any other debt secured on it.

0% purchase credit cards

0% purchase credit cards may be suitable for smaller renovation costs if you can clear the balance before the promotional period ends. Once the 0% period expires, any remaining balance will attract the standard rate, which can be high.

Government grants and schemes

Grants may be available for energy efficiency improvements and certain accessibility modifications. Gov.uk provides information on current schemes, which can change, so it is worth checking what is currently available in your area.

Savings

Using existing savings avoids interest costs entirely. If your project is not urgent, saving up first may work out cheaper overall than borrowing, depending on current savings rates versus loan rates.

Compare loans with ClearScore: Smart borrowing made simple

With ClearScore, you can compare loan offers and check your eligibility without affecting your credit score. Soft searches are only visible to you. When you're ready to apply, the lender will do a hard search, which can affect your score.

Here's how it works:

1. Check your eligibility first — See which loans you're likely to be accepted for before you apply. We use a soft search, only visible to you, and it won't affect your score — so you can explore with confidence.

2. Compare real, personalised offers — No generic rates or estimates here. You'll see actual loan offers tailored to your credit profile, with transparent terms and no hidden surprises. Compare interest rates, monthly payments, and total costs side by side to find your best match.

3. Apply with confidence — Once you've found the right loan, you can apply directly through ClearScore. Your credit score and report are available to track throughout, helping you stay in control of your financial journey.

Why choose ClearScore for loan comparison?

- Free forever—No hidden fees or charges to use our comparison service

- Up to 45 lenders—Access a wide range of loan providers in one place

- Soft credit checks—Check eligibility without impacting your credit score

- Personalised matching—See offers based on your credit profile, not generic rates

- Track your progress—Monitor your credit score weekly to unlock better deals over time

Whether you're consolidating debt, financing a big purchase, or investing in your future, ClearScore helps you find loans that fit your credit profile and financial goals.

Compare loan offers on ClearScore

NimbleFins has been acquired by ClearScore

FAQs on personal loans for home improvements

Can I use a personal loan for home improvements?

Yes. Personal loans can be used for home improvement purposes and there are generally no restrictions on the type of renovation work you fund, once the loan is approved.

What is the difference between secured and unsecured home improvement loans?

Unsecured loans do not require collateral and tend to have faster approval times, but typically carry higher interest rates and lower borrowing limits. Secured loans use your home as security, which can mean lower rates and higher borrowing amounts, but your property is at risk if you cannot repay.

How long does it take to receive funds?

Timescales vary by lender, but many will transfer funds within a few working days of a successful application. Some lenders offer same-day or next-day transfers for existing customers.

Can I get a home improvement loan with a poor credit history?

It may be possible, though your choice of lenders will likely be more limited and the rate offered may be higher. Specialist lenders sometimes cater for applicants with a less-than-perfect credit history. Using a soft-search eligibility checker can help you understand your options without affecting your credit score.

Is it better to save or borrow for home improvements?

This depends on factors including the urgency of your project, your current savings level, and the difference between available savings rates and loan rates. For essential or time-sensitive repairs, borrowing may be necessary. For non-urgent projects, saving up first can avoid interest costs entirely.

What if renovation costs exceed my loan amount?

Unexpected costs are common in renovation projects. It is generally advisable to budget a contingency of around 10 to 20% on top of quoted costs. If your project does run over, you may need to consider using savings, scaling back the work, or exploring additional financing options.

Important information

- NimbleFins is a credit broker, not a lender.

- NimbleFins has been acquired by ClearScore. References to ClearScore on this site, including in relation to credit scores, credit reports, and financial product offers, reflect that relationship.

- Always make sure you can afford repayments before taking out any credit product.

- Your home may be repossessed if you do not keep up repayments on a mortgage or any loan secured on your home.

- This article is for information purposes only. It does not constitute financial advice and no personalised recommendation has been made. Eligibility for any credit product is assessed by the lender and depends on your individual circumstances. Always compare products carefully and consider seeking independent financial advice if you are unsure.