AXA Landlord Insurance Review: Is This The Provider For You?

AXA Landlord Insurance Review: Is This The Provider For You?

Good for

- Award winning product

- Multiple property coverage

- Prompt cash back payments

- Managing your policy online

- Many optional add-ons

Bad for

- Long call times

- More premium price

- Rent guarantee and emergency home insurance cover not offered

As seen on

AXA is an international powerhouse, offering insurance to over 105 million customers worldwide. These numbers alone sound impressive, indeed, market intelligence firm S&P global issued them with an overall credit rating of AA- which indicates high quality, and low risk.

However, customer reviews paint a somewhat different picture. Trustpilot gives AXA a positive average rating of 4.3/5 through nearly 7,000 reviews whilst TopCashback gives a rather disappointing 2 out of 5 (although arguably this should be taken with a grain of salt given this is across only 114 customer reviews).

But how trustworthy is AXA landlord insurance really? We’ve sifted through hundreds of customer reviews and dissected their policies to give you an unbiased, comprehensive review of AXA and how it compares to other landlord insurance options.

In This Review

- AXA Landlord Insurance: Overall Review

- How to Claim

- AXA Landlord insurance: discounts and savings

-

Compare Landlord Insurance

Only one form to fill out. Find the insurance you need today.

AXA Landlord Insurance Overall Review

Operating as one of the largest insurance providers in the world, with over 300 years’ experience supporting its customers, it might seem natural to place a lot of confidence in AXA for protecting you against the risks that come with renting property out to tenants.

It is important however to take a look at the wider picture, which includes real landlord specific customer feedback as well as how its landlord cover holds up against other reputable providers on the market.

AXA’s landlord insurance performance is rated consistently high across the board, with solid features on offer for their commercial and residential landlord insurance product.

As far as customer reception goes, it has earned an 'excellent' 4.3 out of 5 from Trustpilot.

Taken together, it would seem that AXA is worthy of consideration if you are thinking about taking out landlord insurance optionslandlord insurance or considering making the move from your existing provider. Let’s take a deep-dive into the ins and outs of AXA landlord insurance and see if they really do hold up to the test.

Why choose AXA Landlord insurance?

AXA landlord insurance cover comes with some desirable features which may sway some landlords looking for a value offer. These include:

- Award winning claims management team: AXA won Claims Initiative of the Year - Insurer at the British Insurance Awards 2015

- 24 hour glass replacement service: applies to windows, doors or partitions

- Inflation protection: AXA uses recognized independent cost indices to amend your sums insured to reflect inflation

- Multiple properties: Cover up to 10 properties in one policy (including automatic cover for newly acquired or newly erected property or property under construction)

- Access to helplines: Free 24 hour emergency as well as legal and tax helplines

AXA Landlord insurance reviews and ratings

AXA Customer Ratings Feefo Rating 4.5 out of 5 Trustpilot Rating 4.4 out of 5 Finder Rating^ 3.8 out of 5 (landlord insurance specific) ^Finder Rating based on 81 customer reviews, use as guidance only

AXA landlord insurance is considered to be one of the highest quality offers on the market in terms of features. In terms of customer feedback AXA also performs well judging by its Feefo and Trustpilot ratings, scoring 4.5 and 4.4 respectively, indicating an ‘excellent’ customer experience. However, both of these ratings apply to AXA as a whole—that is, mainly car and home insurance, and not their landlord insurance offer specifically, so bear this in mind.

Looking at landlord insurance specific customer feedback paints a slightly different picture, with AXA scoring a 3.8 out of 5 on Finder. This rating is based on a smaller sample size however, with only 400 customer reviews. Whilst this doesn’t mean this customer feedback is any less valuable, we would recommend using these ratings as a guide only.

What does AXA Landlord insurance do well?

We sifted through hundreds of customers reviews to see what features of AXA’s landlord insurance, as well as AXA itself, have customers singing their praises. During our research we found a few key themes that continued to be highlighted and these include their excellent customer service, competitive prices and ease of online application.

Many customers have also commented on AXA’s willingness to payout and the speed with which they do so. Assuming to follow the conditions AXA outline with regards to making a claim, it would appear that AXA’s landlord insurance offer is certainly one to consider.

Here is a sample of customer comments:

"Been with Axa for many years, have home, landlord and car insurance with them. Excellent response to any correspondence you have with them. Wouldn’t use anyone else."

“Very competitive price, easy to complete cover online.”

“AXA have provided me with excellent service and have been very helpful when I contact them. Highly recommend this company.”

“Very good, excellent service always. I have bought AXA products in the past and I have always received exceptional service.”

“It was straightforward and very competitively priced! All documents are easy to view via the online portal!.”

“The process of obtaining my quotation and arranging cover was very straightforward.”

What could AXA Landlord insurance improve on?

Nobody is perfect, and AXA is no exception here. Although reviews are overwhelmingly positive, we did find that some customers called out poor customer service, for example not answering phone calls and not contacting them back about an existing issue. Others highlighted difficulty in successfully making a claim as well as frustration that AXA charge a higher price compared to competitors for seemingly less value.

“My policy renews shortly so I'll be taking all my policies elsewhere if they don't care to employ enough staff to take care of existing paying customers.”

“Worst insurer ever promised manager call backs and nothing happens - complaints logged and no call back letter or anything.”

“They will do literally anything to avoid paying out and their customer service is nonexistent.”

“Had a pipe concealed behind tiled walls leaking...AXA has so far sent 2 different people to survey, both initially agreed scope of works and reported back...3 months in and no progress, AXA seem to want to dodge any responsibility and keep sending people to site until they get a report that suits them.”

“Renewal price was twice the price of other competitors. Loyalty counts for nothing evidently.”

“I've Premium Landlord insurance with AXA...I had a claim. It was my very first claim. Our ensuite started to leak...And the living room sealing was damaged with the leak water. AXA refused my ensuite claim..I still don't understand why.”

As with any product review context is important. Sometimes frustration and complaints are a result of customers simply not knowing or understanding what is covered under their policy. The documentation given to you when you agree to take out landlord insurance is often full of jargon and can be a lot of information to digest, so of course details can be overlooked.

Take this scenario, for example. If you find that there is a leak in one of your rented properties and you wish to make a claim, you may find that your policy will cover the costs of fixing the damage caused by the leak, rather than the leak itself. It sounds almost counter-intuitive and may lead to you to becoming quite annoyed with your insurance provider when they tell you this is outlined in your policy documentation.

It is for these reasons that we always recommend reading your policy wording carefully so you know your rights and don’t get caught out.

How much is AXA Landlord insurance?

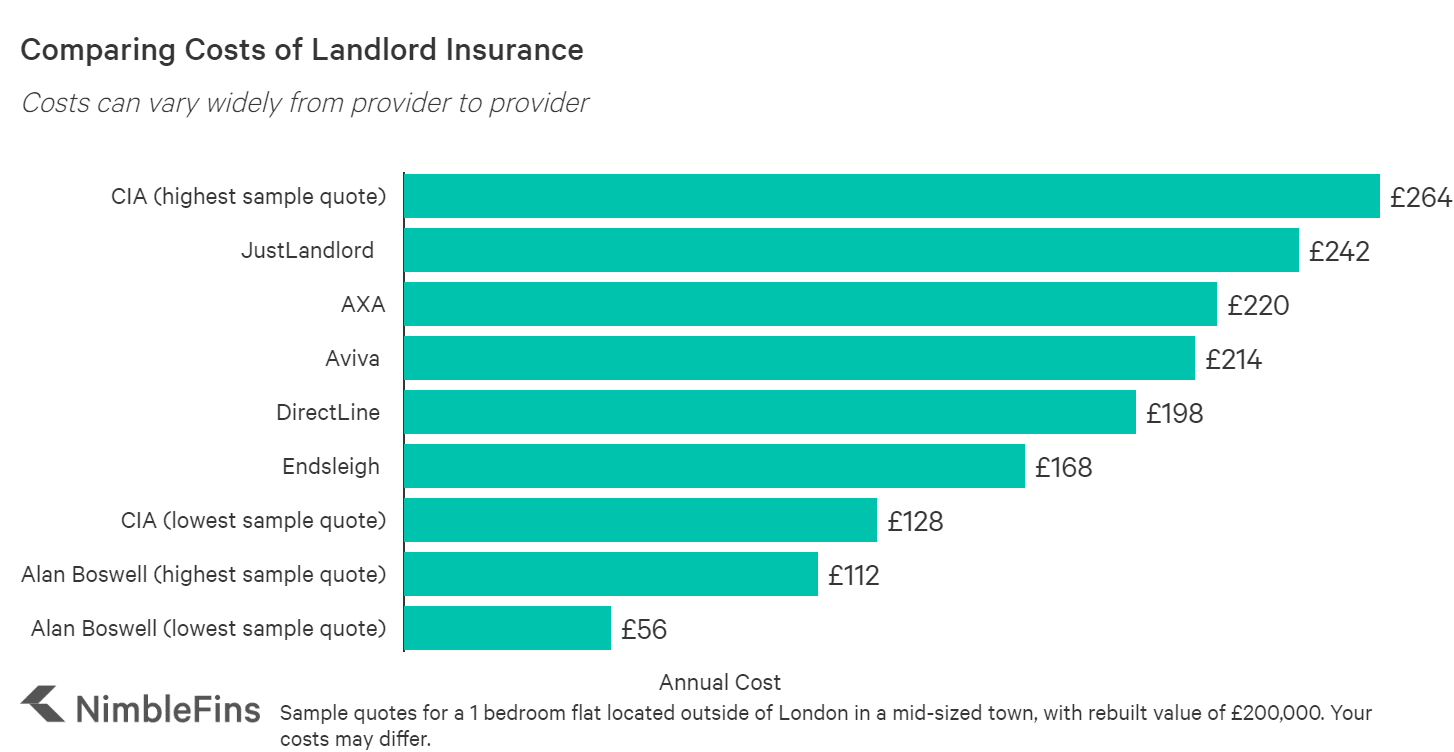

We have compiled quotes for a 1 bedroom flat located outside of London in a mid-sized town, with a rebuild value of £200,000. We found that for a no-frills policy with buildings insurance and property owners liability of £2million, AXA landlord insurance is slightly more expensive than many of its competitors. Their sample price was £220, which was the second highest out of the six popular landlord insurance providers we checked.

Costs can really vary so it's important to check prices from multiple sources and understand what's includedLandlord insurance quote comparison for a 1 bedroom flat (£annual) CIA

£264 (highest sample quote) JustLandlord

£242 AXA

£220 Aviva

£214 DirectLine

£198 Endsleigh

£168 CIA

£128 (lowest sample quote) Alan Boswell

£112 (highest sample quote) Alan Boswell

£56 (lowest sample quote) Of course, these quotes are intended to be used as a guideline, and your quotes may be higher or lower depending on your own individual circumstances.

What is/isn’t covered by AXA Landlord insurance?

As part of their standard landlord insurance cover, AXA offers a nice selection of benefits that are in line with what you would expect. These include:

- Buildings Insurance: to cover the cost of rebuilding or repairing your flat if it is damaged or destroyed

- Property Owner’s Liability: flexibility to choose between £1m to £10 million limit

- Cables and underground pipes cover: including damage to utilities such as electricity, gas and water AXA will part for any costs incurred

- Rehousing your tenants in alternative accommodation: for example, if your rented property is damaged and can’t be lived in (20% of the sum insured for the damaged building for a maximum of 24 months from the date of damage)

- Subsidence, ground heave and landslip cover: often a requirement for some mortgage providers, AXA can provide cover if your property is damaged due to land shifts, but in some cases this cover is not included as standard

- Eviction of squatters expenses: up to £15,000 per claim

- Landlord fixtures and fittings

- Cover for up to 10 properties in one policy

- Student Tenant Exclusion: Standard policies decline students (though AXA offers separate student rental product)

- Unoccupancy: Once your property becomes unoccupied, you’ll have 45 days full cover, after which your cover will be reduced and an unoccupancy condition applied. Certain types of damage are excluded if the property is unoccupied.

Optional add-ons

As with all landlord insurance providers AXA also provides some additional cover options that aren’t included in their policy as standard. Whilst not mandatory, these are worth considering to offer you an additional layer of protection against the risks associated with being a landlord.

- Loss of rental income: for example, if your property is damaged rendering your property uninhabitable. This also includes the costs of re-letting the property if needed, to minimize the loss of income.

- Landlord employers liability insurance: if you employ someone, by law you must have employers liability insurance (note: there are some exemptions). This will cover compensation payments and legal costs if an employee suffers a work-related illness

- Landlords contents insurance: covers the costs of repair or replacement of the contents inside the property that you provide for your tenants in the event of e.g. a flood or fire

- Malicious damage and theft by tenants: covers the cost to repair or replace property intentionally damaged or stolen by tenants (e.g. if a tenant purposely breaks a window). This is subject to a few conditions that you must follow, for example carrying out internal and external inspections of the buildings at least every 6 months (or as frequently as required as detailed in your agreement) as well as tenant identification and referencing

- Accidental damage: applies to your properties structure, floor and fittings in case these are damaged accidentally, for example, if your tenant spills wine on the carpet, leaving a stain

Missing features

There are some features that either aren’t offered in AXA’s standard cover or aren’t available to purchase as an add on. These features are worth knowing about as they do provide that added layer of protection if something were to happen and could save you a lot of money, so going without these could be risky.

- Landlord rent guarantee: Unlike loss of rental income, landlord rent guarantee insurance will cover you if a tenant is unable to make rental payments regardless of whether your property is habitable or not (e.g. if the tenant has recently lost their job). AXA does not offer rent guarantee in their landlord insurance offer – ensuring you have a stable source of income from your rental payments is incredibly important, so think carefully about whether you would be comfortable proceeding without this security.

- Landlord home emergency cover: In the event of an emergency (e.g. a heating breakdown) AXA will not will cover the costs of labour and materials needed to fix the issue, although they do provide a 24/7 landlord emergency helpline offering advice and details of qualified contractors who can assist you.

Exclusions: What isn’t included?

As with almost any type of insurance, landlord insurance often contains some exclusions that are good to be aware of so you don’t get caught out. AXA is no different, and we’ve outlined a few key ones we’ve found below.

- AXA will not cover legal liability arising from or contributed by inhalation, ingestion or the presence of asbestos in any property or land

- Any damage inflicted by wind, rain, hail, snow, flood and/or theft on moveable property in the open e.g. walls, fences, posts, hedges and gates

- You will not be covered for any damage caused by using the property for illegal activities

- Damage caused by vermin or insects

- Damage caused by corrosion, rust, dry rot

- Damage to property caused by faulty design/materials, frost, gradual deterioration or change in water table level

Remember though, this is just a snap-shot and the full list is much longer. Also, another key point to remember as a landlord of a rented property is that if your property is unoccupied for longer than the period of time outlined in your policy, any damage or losses that occur within this time will often not be covered by your insurer. So, always read your policy wording carefully and know what you have signed up for.

How does AXA Landlord Insurance Compare to Competitors?

To better understand the value of AXA Landlord insurance you need to look at it in the context of other available options. We compared it to other plans in the market so you can see which may be more suitable for you.

AXA Landlord Insurance vs Direct Line Landlord Insurance

Direct Line is one of the UK’s largest and most reputable insurers, and they’re considered to be one of the best landlord insurance products on the market. With over 250,000 existing landlord insurance policy holders it is certainly a popular choice and has won multiple awards to boot. Its comprehensive cover includes buildings, contents and landlord liability included as standard.

Just like AXA, Direct Line offers a range of optional add-ons such as malicious damage by tenants, loss of rental income and legal expenses meaning you can curate the right policy for your needs. Direct Line also offer some discounts for new and existing landlords, such as a 10% multi-property discount if you’re looking to insure 15+ properties!

Bottom Line: If you’re looking for award-winning coverage from a reputable insurer then Direct Line may be another option to consider — their extensive range of policy add-ons also gives you the freedom to tailor your policy to suit your specific needs.

AXA Landlord Insurance vs LV= Landlord Insurance

One of the UK’s leading providers, LV= specializes in many different insurance areas. This multi-award winning provider receives glowing customer feedback so is certainly a firm favourite amongst experts and customers alike.

Though some customers have noted higher renewal fees and lack of rewards for loyal customers, we found LV= to be one of the cheapest providers we sampled from so it might be worth taking a look. Even with its low price LV=’s coverage certainly packs a punch — its extensive cover includes £5m landlord liability, accidental damage, malicious damage by tenants as well as loss of rental income as standard.

Bottom Line: Don’t be fooled by the low premiums, LV= is certainly an option for price-savvy landlords looking for a value offer without compromising on cover.

AXA Landlord Insurance vs Aviva Landlord Insurance

Aviva is one of the UK's largest insurance providers and have been in the business for more than 320 years. Whilst customer reviews are somewhat mixed, its cover for landlords is pretty solid and independent credit rating agency Moody consider them to be a reliable and capable insurer. What is more, Aviva do offer online discounts, quick call out time, no-claims discounts and a seamless claims process from an award winning claims management team!

Our research found Aviva to be slightly cheaper than AXA and their cover is certainly impressive—loss of rental income, £5m landlord liability, buildings, and contents are included as standard, and Aviva also offers a selection of optional add-ons which allows you to tailor your policy to suit your needs.

it is important to note though that Aviva's cover is missing malicious damage by tenants, so it may not be suited to those landlords renting to more 'risky' tenants!

Bottom Line: another great option for those looking for landlord insurance cover from a reputable insurer who offers a variety of discounts and incentives to boot.

How to make a claim on AXA landlord insurance

If you need to make a claim on AXA’s landlord insurance it is vital you first read your policy wording and summary to ensure you are protected. If you believe you are, you should contact AXA’s claims number or email as soon as possible which can be found in the policy summary and online:

- AXA Landlord insurance phone number: 0345 600 2715 (open Mon-Fri, 9am-5pm)

- AXA Landlord insurance email: [email protected]

AXA’s Landlord documents (policy wording) includes key conditions you must meet and agree to in order for you claim to be considered, these include things such as allowing access to the property and providing full details of the loss or damage along with any additional evidence (e.g. photographs) or information AXA require.

Failure to comply with these conditions could result in delays to your claims process or your claim being dismissed entirely, so we would recommend speaking to an advisor who will give you all the information you need to take your claim forward.

AXA landlord insurance: Discounts and savings

It’s well worth being aware of tips and tricks at your disposal that will help you to save a little bit on AXA’s landlord insurance.

- AXA does offer a 10% discount when you purchase landlord insurance online, an easy way to save a few pennies!

- AXA also offer 0% interest on instalments when you choose to pay monthly, which can offer you peace of mind if you’re unable to pay the cost of landlord insurance upfront

FAQ’s

Yes and no.

If you cancel your policy within the 14-day cooling off period after receiving your documentation then you are eligible for a full refund if your policy hasn’t started yet. If it has started, you will be refunded the amount proportional to the amount of time left on your policy.

However, if you choose to cancel after this 14-day period you’ll still receive a proportional refund based on the amount of time left on your policy, but you will be charged a £35 cancellation fee.

If you’ve made a claim or had one registered against before you wish to cancel, you will not be eligible for a refund in any of the above scenarios and will also be charged the £35 cancellation fee.

Yes, they do! AXA offer commercial landlord insurance with a range of features, including cover for up to 10 properties and property owners' liability of up to £10 million. You can check out AXA's commercial landlord insurance offer here.

If you’re looking for AXA Landlord insurance promotional codes, they do pop up throughout the year. They’re usually advertised on the AXA website as a ‘special offer’, so keep your eyes out for when they do pop-up. You may find them on a few ‘discount code’ websites, but these quickly expire, so don’t be surprised if the code is rejected when you enter it.

AXA's Landlord insurance does not cover the breakdown of boilers as a result of old age or fair wear and tear. Whether this is covered by your policy will depend on your specific circumstances, and you'll need to discuss this with AXA directly. If you find you are not covered, it's certainly worth taking a look at landlord home emergency insurance, as this cover you for these types of events.

'Accidental damage' can cover you in the event of one-off accidents to your properties building or contents. Examples where accidental damage cover would apply include things like if your tenant accidentally spills red wine on the carpet leaving a stain, or if a leaky roof causes internal water damage.

AXA offers accidental damage cover as an optional add when you purchase landlord insurance with them, so if this is of interest to you then it's well worth considering.

AXA's standard landlord insurance will cover you if your property is vacant(i.e. unoccupied) for up to 45 consecutive days. If your property is vacant for longer than this period of time you must notify AXA immediately, and you will typically find you are not covered for any damages that occur after this period.

Yes, during our research we found that AXA is featured on many popular comparison sites, such as Simply Business and GoCompare. Comparing quotes is one of the best ways to save money on landlord insurance!

No, it doesn't. AXA will not pay out on any claims for damage as a result of wear, tear or gradual deterioration.

One of the perks of AXA's landlord insurance is that you can insure up to 10 properties under one policy. Any more than this however and AXA will sadly not be able to accommodate you, so you would be better off opting for an insurance provider that specializes in property portfolio cover.

Unfortunately, standard homeowners insurance isn't equipped to cover the additional risks that landlords face when renting out properties to others such as rent guarantee, legal expenses and liability to name just a few! Don't be caught out by assuming homeowners insurance is enough and always invest in specialist landlord insurance to ensure you are protected.