Millenials Spend More on Takeaways Than They Save for Retirement

Where Do Millenials Spend Their Extra Money?

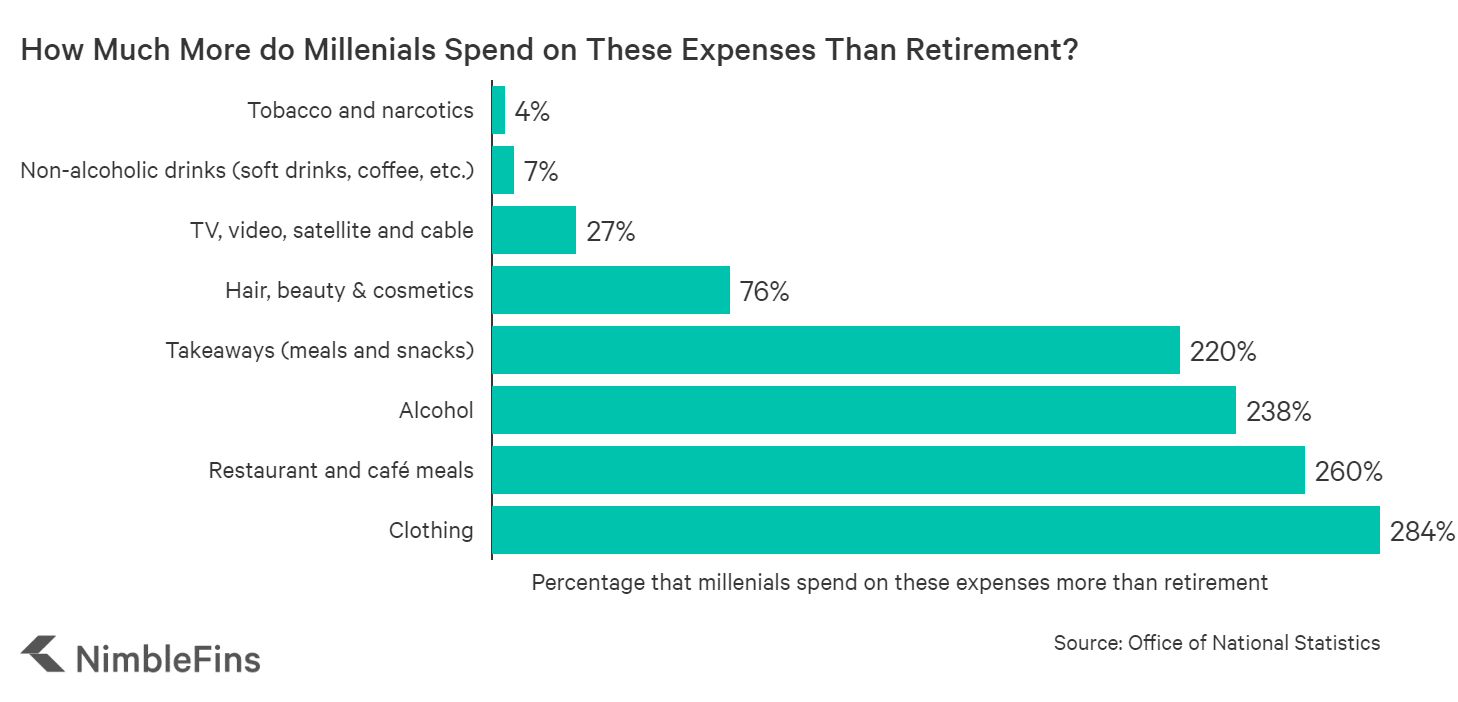

It seems that most millenials aren't practicing one of the most common pieces of personal finance advice: start saving early for retirement. We analysed data from the Office of National Statistics (ONS) and found that millenials spend more each week on eating out, clothes, tv, alcohol, smoking and hair & makeup than they do on saving for retirement. For example, when compared to the amount of money millenials save and invest, they spend 76% more on hair and cosmetics, 220% more on takeaways, 238% more on alcohol and 284% more on clothes.

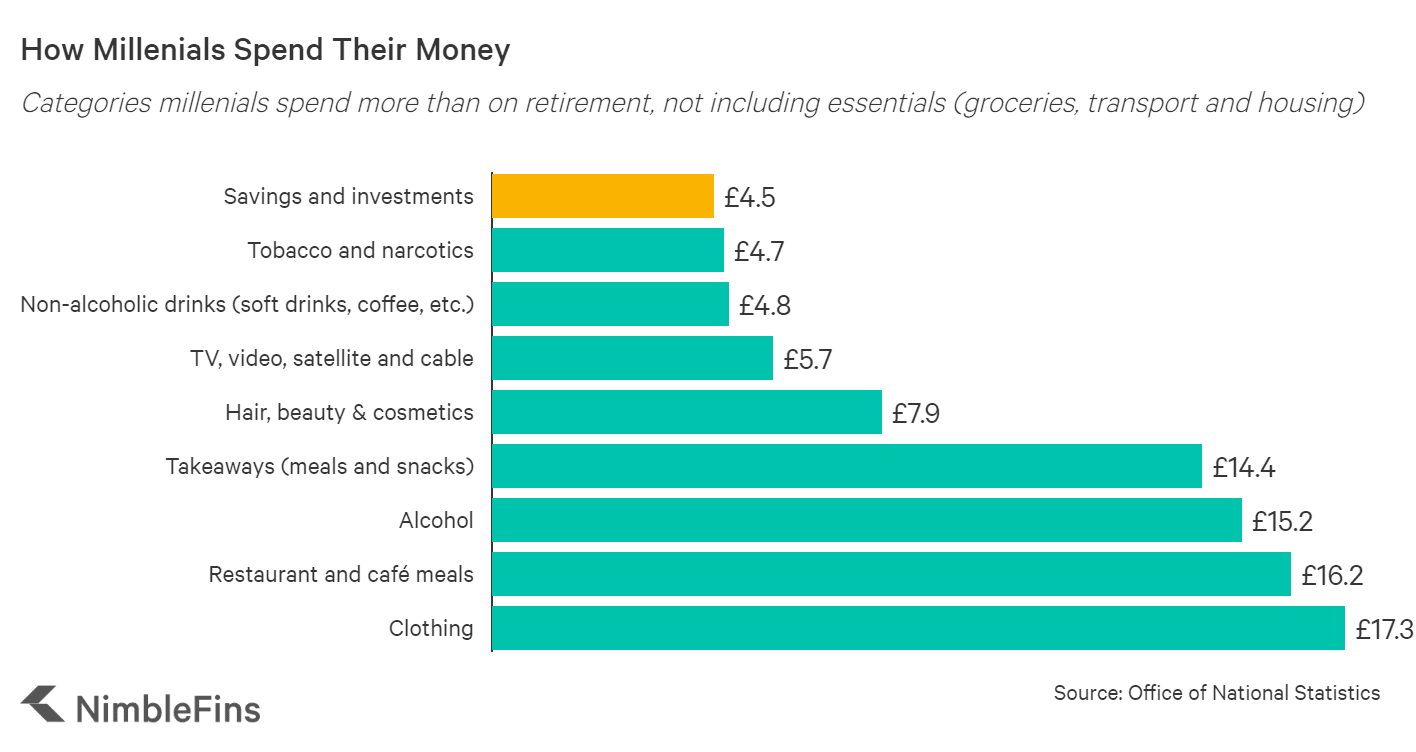

Each week, the average millenial household puts away just £4.50 into savings or investing for the future. Households in this age group take home over £500 per week after taxes, of which 60% is spent on essentials like food (£43 for groceries, plus another £33 is spent eating out), housing (£171) and transport (£67). The other 40% is spent on expenses like drinking, smoking, clothing, entertainment and, to a much lesser extent, saving and investing. Here is some of how millenials spend their paychecks each week:

| Where Millenials Spend Their Extra Money | Per Week | Per Month | Per Year |

|---|---|---|---|

| Tobacco and narcotics | £4.7 | £20.37 | £244.4 |

| Non-alcoholic drinks (soft drinks, coffee, etc.) | £4.8 | £20.80 | £249.6 |

| TV, video, satellite and cable | £5.7 | £24.70 | £296.4 |

| Hair, beauty & cosmetics | £7.9 | £34.23 | £410.8 |

| Package holidays | £13.4 | £58 | £697 |

| Takeaways (meals and snacks) | £14.4 | £62.40 | £748.8 |

| Alcohol | £15.2 | £65.87 | £790.4 |

| Restaurant and café meals | £16.2 | £70.20 | £842.4 |

| Clothing | £17.3 | £74.97 | £899.6 |

| Savings and investments | £4.5 | £19.50 | £234.0 |

Saving can certainly be difficult for millenials given the high cost of living in some cities. For example, London is one of the more expensive cities for millenials to live in across Europe. That said, there are ways to increase savings, such as by cooking at home more often or taking domestic holidays such as renting a caravan. In fact, millenials could double their savings and investing rates by drinking 30% less, decreasing the amount spent at restaurants by 28%, or spending 26% less on clothes.

Alternatively, money saved could be used to reduce household debt levels, which continue to rise in the UK.

Why Under 30s Should Save Now

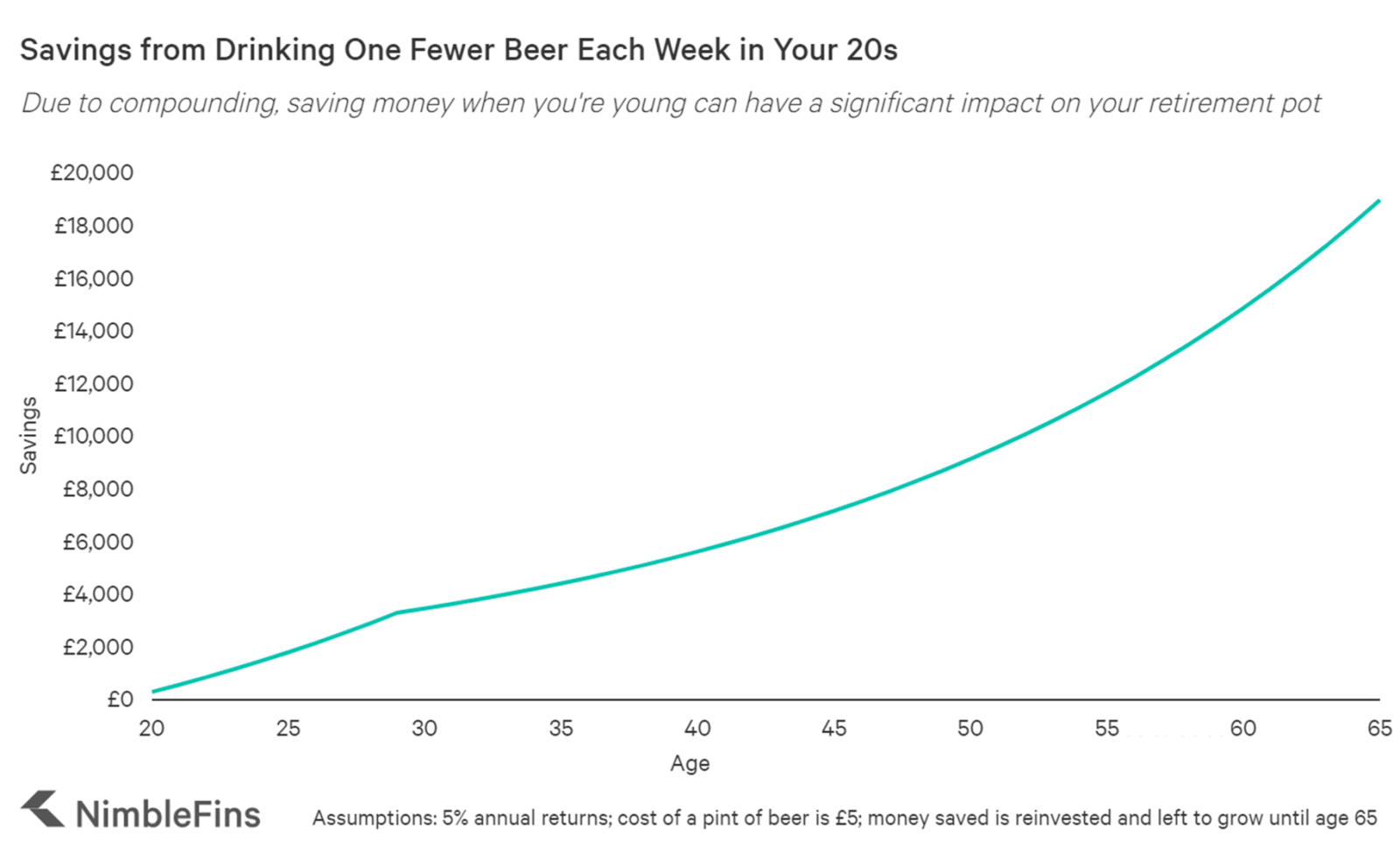

By drinking one fewer beer each week whilst in their 20s, a person could have nearly £20,000 saved by age 65. Assuming a pint of beer costs £5, by having one less pint each week you'd sock away £260 per year (52 weeks per year times £5 = £260) or £2,600 over the ten years from age 20 through 29. Assuming your money grows at 5% a year (which it may or may not), the £2,600 you saved in your 20s could turn into £18,941 by your 65th birthday. Money invested early benefits from compounding—so while retirement feels a long way off when you're young, those who start saving early are likely to have a larger nest egg to fund retirement.

How Do Millenials Prioritise Saving vs Other Age Groups?

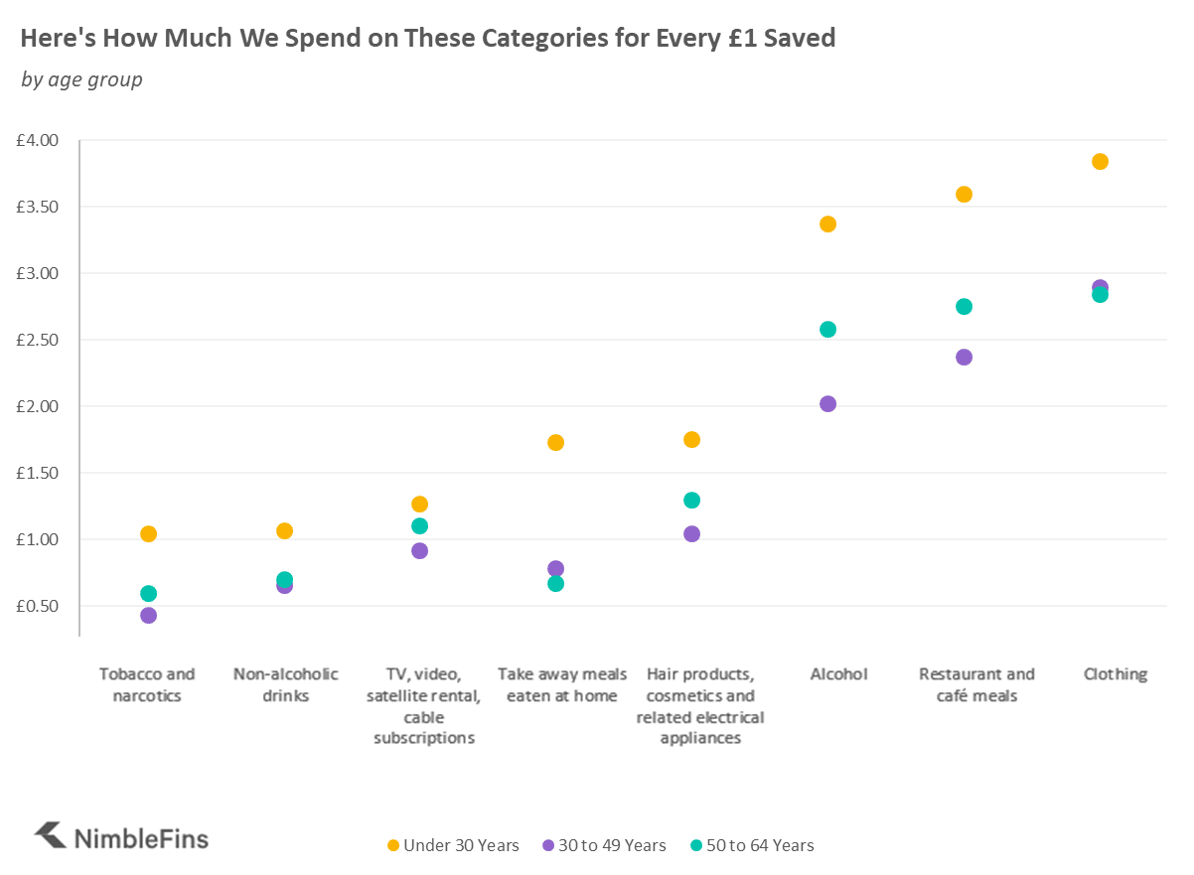

Millenials are much worse at saving money than other age groups. The age group best at prioritising saving for retirement over spending is 30 to 49 year olds. As you can see in the chart below, people in this age bracket spend around half of what millenials spend on extras, for each pound put away for retirement or a rainy day. For example, for every £1 saved a millenial spends £1.70 on takeaways while those aged 30 to 49 spend only £0.80 on takeaways.

Millenials can become more financially savvy by increasing their rate of savings now, rather than wait until they're older.

Methodology

To understand how under 30s prioritise saving and investing for the future over spending their money on other expenses, we analysed household expenditure data from the Office of National Statistics for households where the household reference person is less than 30 years old. We then compared this to data for the 30 to 49 and 50 to 64 age groups, to see how saving and spending patterns differ between the age groups which are preparing for retirement. We didn't include 65+ age groups since this is the age by which many people would like to retire and would therefore no longer be "saving for retirement." The most recently available data is the financial year ending 2018.